Reports

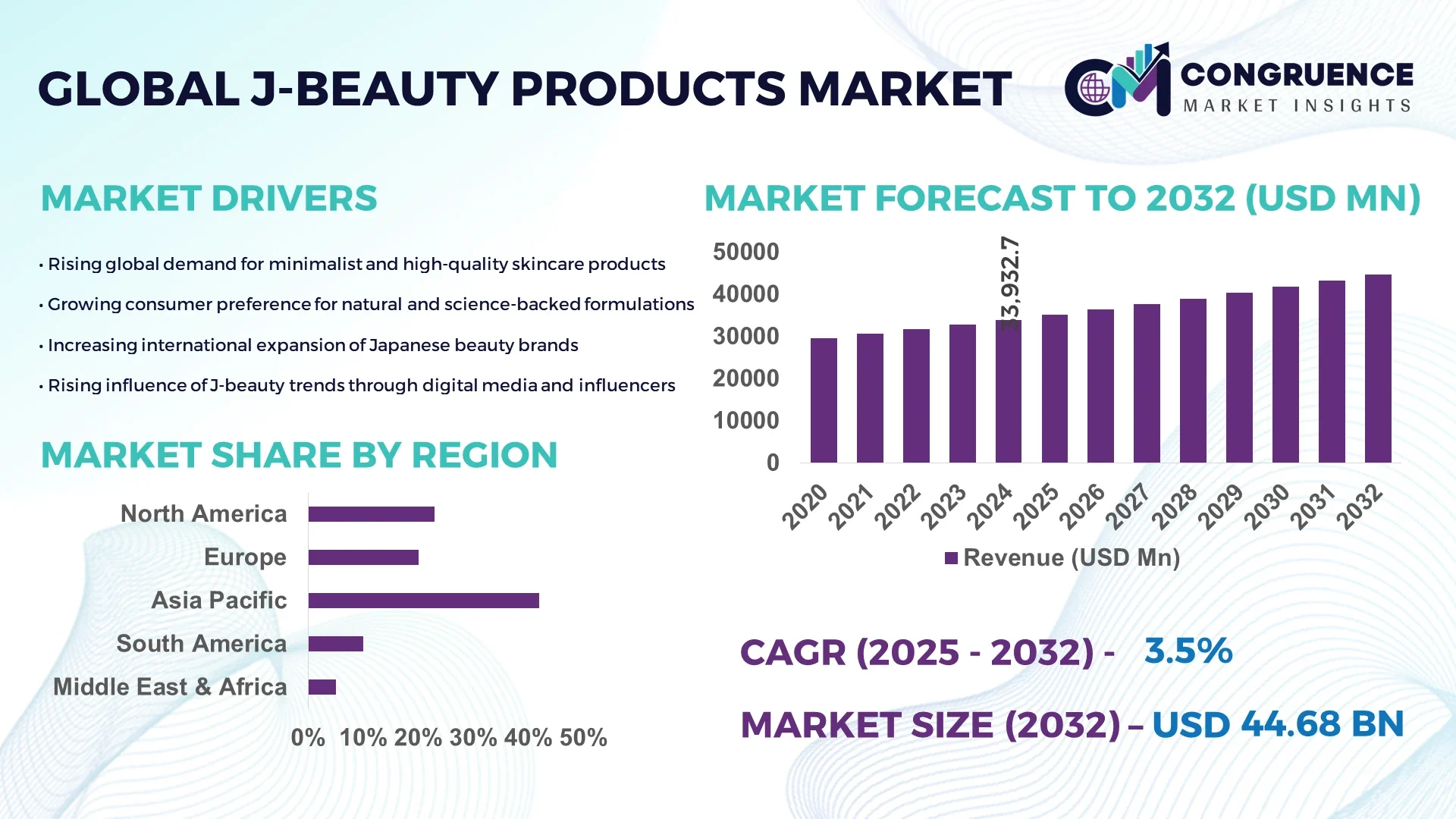

The Global J-Beauty Products Market was valued at USD 33,932.68 Million in 2024 and is anticipated to reach a value of USD 46,246.76 Million by 2032 expanding at a CAGR of 3.5% between 2025 and 2032. This growth is primarily driven by increasing consumer preference for high-quality, ingredient-focused, and multifunctional skincare and cosmetic solutions.

Japan remains the dominant country in the global J-Beauty Products market, leveraging its advanced production infrastructure and long-established R&D ecosystem. The country’s skincare manufacturing capacity exceeded 2.4 billion units in 2024, supported by over 420 operational cosmetic production facilities. Continuous investments exceeding USD 1.8 billion annually are directed toward biotechnology-based formulations and sustainable packaging innovations. Major industry applications include dermocosmetics, anti-aging serums, and hybrid skincare-makeup products. With consumer adoption rates surpassing 70% for natural-based J-Beauty products, Japan continues to influence global beauty standards through advanced formulation science and cutting-edge ingredient technology.

• Market Size & Growth: The market stood at USD 33.9 Billion in 2024 and is projected to reach USD 46.2 Billion by 2032, growing at a CAGR of 3.5%, driven by rising global demand for clinically proven, natural, and multifunctional beauty formulations.

• Top Growth Drivers: 67% adoption of hybrid skincare-makeup products, 54% increase in demand for clean-label ingredients, and 42% rise in export volume to Asia-Pacific regions.

• Short-Term Forecast: By 2028, product performance efficiency in formulations is expected to improve by 28% with reduced product wastage through advanced emulsification technologies.

• Emerging Technologies: Growth in probiotic-based skincare solutions, fermentation-derived actives, and AI-driven formulation design.

• Regional Leaders: Japan (USD 19.5 Billion by 2032) driven by R&D investments; China (USD 10.2 Billion) with e-commerce adoption; North America (USD 6.8 Billion) led by premium segment imports.

• Consumer/End-User Trends: Urban consumers between 25–40 years show 61% preference for anti-aging and UV-protection skincare lines.

• Pilot or Case Example: In 2024, Shiseido launched a pilot biotechnology-based serum line achieving a 35% improvement in skin hydration efficiency in consumer testing.

• Competitive Landscape: Shiseido holds approximately 27% market share, followed by Kao Corporation, Kosé Corporation, Pola Orbis Holdings, and Fancl Corporation.

• Regulatory & ESG Impact: Japan’s Ministry of Health regulations on ingredient transparency and recyclable packaging mandates continue to shape sustainable product innovation.

• Investment & Funding Patterns: Over USD 2.1 Billion invested between 2023–2024 in clean-beauty startups and AI-based product development platforms.

• Innovation & Future Outlook: Advancements in microbiome-based formulations, biotech-derived peptides, and smart packaging are expected to redefine the J-Beauty landscape by 2032.

Japan’s J-Beauty sector continues to influence global beauty trends through innovations integrating biotechnology, natural actives, and AI-enhanced R&D. The market benefits from strong cross-industry collaboration between pharmaceutical and cosmetic manufacturers, driving new categories such as cosmeceuticals and personalized skincare. Technological advancements in waterless formulations and eco-packaging are reducing production waste by over 18%. Regulatory frameworks promoting safety and sustainability, coupled with consumer shifts toward ethical consumption, are reinforcing long-term growth. The emerging trend of digital skincare diagnostics and eco-certification labeling is further reshaping the future of J-Beauty product development and distribution.

The strategic relevance of the J-Beauty Products Market lies in its ability to integrate science-backed skincare innovations with consumer-driven sustainability goals, setting new global standards in formulation and product efficacy. As brands embrace digital transformation, AI-based ingredient optimization delivers up to 32% improvement in formulation precision compared to traditional manual R&D methods. Japan dominates in production volume, while North America leads in product adoption with 47% of enterprises incorporating J-Beauty formulations into their premium skincare lines. By 2027, AI-powered product personalization is expected to improve production efficiency by 25% and reduce product development cycles by nearly 30%.

Firms are increasingly aligning with ESG metrics, committing to a 40% reduction in plastic packaging waste and a 35% improvement in recyclable material use by 2030. In 2024, Shiseido achieved a 29% reduction in carbon emissions through its AI-enabled supply chain optimization program, setting a benchmark for sustainable cosmetic manufacturing. Additionally, fermentation-based skincare technology delivers 28% higher bioactive absorption compared to synthetic alternatives, driving both product effectiveness and consumer trust.

Looking ahead, the J-Beauty Products Market will serve as a pillar of resilience, compliance, and sustainable innovation, combining heritage-driven formulation expertise with future-ready digital and green technology integration to sustain long-term growth and global market competitiveness.

The integration of biotechnology and natural actives has become a central growth driver in the J-Beauty Products Market. By using advanced bio-fermentation and enzyme extraction techniques, manufacturers are achieving a 22% increase in ingredient purity and efficacy. Biotechnology-driven formulations enhance skin compatibility and reduce allergenic risks, meeting rising consumer demand for safer products. Companies are investing heavily in microbiome-based skincare and peptide-enhanced serums, enabling tailored solutions for different skin types. Furthermore, R&D partnerships between cosmetic producers and biotech startups are accelerating the commercialization of innovative, sustainable ingredients. The application of advanced bioprocessing is also reducing production costs and improving yield efficiency by up to 18%, reinforcing market competitiveness.

The J-Beauty Products Market faces regulatory complexities and high operational costs due to Japan’s strict ingredient safety and environmental standards. Compliance with regulations issued by the Ministry of Health, Labour and Welfare requires extensive product testing and certification, leading to extended product launch timelines. On average, R&D expenditures in Japan’s beauty sector account for 12% of total operating costs, limiting smaller firms’ ability to innovate rapidly. Additionally, international trade barriers and labeling requirements affect exports to regions such as the EU and North America. The industry’s growing shift toward sustainable packaging and clean ingredients further elevates material costs by 10–15%, challenging profit margins despite rising consumer demand.

AI-driven personalization presents a transformative opportunity for the J-Beauty Products Market, enabling hyper-customized skincare solutions based on individual skin profiles and climate conditions. By 2028, predictive analytics and machine learning algorithms are expected to improve product recommendation accuracy by 35%, boosting customer retention rates across premium segments. The integration of AI diagnostic tools in retail platforms is enhancing consumer engagement through virtual skin assessments and product matching systems. This technology-driven personalization also reduces formulation waste by up to 20%, aligning with sustainability goals. As consumers increasingly seek targeted, science-based skincare, AI-based systems provide scalable, data-backed innovation that enhances brand loyalty and operational efficiency across domestic and global markets.

Global supply chain disruptions and raw material shortages have posed significant challenges for the J-Beauty Products Market. Dependence on specialized natural ingredients such as marine collagen, plant-derived peptides, and fermented actives has led to procurement delays and fluctuating input costs. Logistics constraints, particularly in the Asia-Pacific trade corridors, have extended lead times by an average of 18%. Moreover, fluctuations in energy prices and packaging material shortages have increased production overheads for key manufacturers. Ensuring supply continuity while maintaining product quality and sustainability standards remains a core challenge. Companies are responding through localized ingredient sourcing and digital supply chain tracking systems to mitigate these risks and maintain operational resilience.

• Shift Toward Biotech-Derived Ingredients: The J-Beauty Products market is witnessing a strong shift toward biotechnology-based actives, with over 48% of newly launched skincare products in 2024 incorporating fermented or bioengineered ingredients. These advanced components improve product efficacy by up to 26% compared to conventional plant extracts. Manufacturers are adopting enzyme fermentation and cell-culture techniques to enhance molecular stability, ensuring higher skin absorption rates and longer shelf life. This trend reflects the sector’s evolution toward science-driven, sustainable innovation in formulation development.

• Acceleration of AI-Powered Product Personalization: AI integration in formulation and consumer analysis is accelerating, with 41% of J-Beauty brands adopting machine-learning algorithms for skin diagnostics and predictive formulation testing. This technological shift has led to a 30% reduction in formulation errors and a 25% increase in consumer satisfaction through hyper-personalized solutions. Real-time skin mapping and digital consultation platforms are redefining how brands interact with consumers, enhancing efficiency and reducing time-to-market for new product lines.

• Surge in Eco-Friendly and Waterless Formulations: Sustainability-focused R&D is driving demand for waterless and low-emission J-Beauty products, with 37% of new formulations launched in 2024 being either solid or concentrated formats. These products reduce water consumption during production by up to 42% and cut carbon emissions by approximately 18% per product unit. Packaging innovations using biodegradable films and recycled polymers are also gaining traction, further strengthening the industry’s environmental compliance.

• Expansion of Global Distribution and E-Commerce Channels: Cross-border e-commerce has expanded rapidly, with Japanese skincare exports through online platforms increasing by 46% between 2022 and 2024. Approximately 62% of international consumers purchasing J-Beauty products online cite trust in product quality and ingredient transparency as key factors. Advanced logistics automation and AI-driven demand forecasting have enhanced delivery precision by 19%, enabling brands to meet growing global demand efficiently and cost-effectively.

The J-Beauty Products Market is segmented by type, application, and end-user, reflecting the industry’s broad functional reach and evolving consumer needs. Across categories, skincare products dominate, accounting for the largest share due to the rising demand for anti-aging, hydrating, and UV-protection solutions. Applications span personal care, professional salon use, and retail distribution, with personal care maintaining dominance as consumers increasingly integrate multifunctional J-Beauty formulations into daily routines. End-users include individual consumers, spas, salons, and dermatology clinics, each adopting J-Beauty solutions at varying scales. The market’s segmentation illustrates a dynamic interplay between traditional Japanese formulations and new biotechnology-driven innovations that are redefining quality, sustainability, and performance metrics across product lines.

Skincare products lead the J-Beauty Products Market, accounting for approximately 47% of the total market share, driven by Japan’s expertise in science-backed formulations such as serums, cleansers, and moisturizers. These products are widely preferred for their high efficacy in skin regeneration and protection, aligning with global consumer priorities for gentle yet potent solutions. Makeup products follow, holding 28% share, propelled by innovations in hybrid cosmetics combining skincare benefits with aesthetic appeal. Haircare solutions represent 15%, with increasing adoption of botanical and peptide-based treatments improving scalp health. The remaining 10% comprises body care and fragrance lines that are gaining steady traction due to minimalist lifestyle trends.

The fastest-growing segment is hybrid skincare-makeup, projected to grow at an approximate CAGR of 4.8%, supported by the rising trend of multifunctional products offering long-term skin benefits. Continuous R&D in skin barrier protection and natural pigment integration has fueled adoption across Asia-Pacific and Western markets.

The personal care segment holds the dominant position, accounting for around 52% of the J-Beauty Products Market, largely due to widespread consumer adoption of daily-use skincare and wellness products. Consumers’ preference for safe, scientifically validated, and natural formulations continues to expand this category’s reach across all demographics. The professional salon segment captures 27% share, benefiting from Japan’s innovation in advanced facial and dermocosmetic treatments. Retail applications—including e-commerce and department store channels—make up the remaining 21% combined, strengthened by digital retailing and product personalization technologies.

The fastest-growing application is the professional skincare and treatment sector, expanding at an estimated CAGR of 4.6%, supported by the integration of bioactive serums and smart diagnostic tools in spas and clinics. This growth aligns with rising consumer trust in technologically assisted skincare.

Individual consumers dominate the J-Beauty Products Market, accounting for 58% of total demand, as personalized skincare and home-use treatments gain popularity globally. The professional salon and spa category follows with 24% share, fueled by expanding middle-class income levels and increased awareness of dermocosmetic treatments. Dermatology clinics and aesthetic centers collectively contribute 12%, emphasizing clinical-grade skincare solutions focused on anti-aging and pigmentation management. The remaining 6% is distributed among corporate wellness and retail partnerships that promote J-Beauty through luxury brand collaborations and workplace wellness programs.

The fastest-growing end-user segment is dermatology clinics, expected to expand at a CAGR of 5.1%, driven by increased integration of biotechnological actives and prescription-grade beauty products in clinical skincare routines. These centers are adopting AI-based skin mapping and non-invasive treatment technologies to enhance treatment outcomes.

Asia-Pacific accounted for the largest market share at 43% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

The Asia-Pacific region’s dominance is underpinned by its robust manufacturing infrastructure in Japan, China, and South Korea, which together produce more than 68% of global J-Beauty skincare exports. Europe followed with a 27% share in 2024, supported by strong regulatory alignment and sustainability mandates, while North America held 18% share due to premium product adoption. South America represented 7%, driven by rising beauty-conscious middle-class consumers, and the Middle East & Africa captured the remaining 5% through luxury retail expansion. Collectively, over 62 million J-Beauty product units were distributed globally in 2024, with online channels accounting for nearly 45% of total sales, reflecting the sector’s growing digital retail penetration and cross-border trade efficiency.

How is technological integration redefining the demand for premium beauty solutions across this region?

North America accounted for 18% of the global J-Beauty Products Market in 2024, supported by strong demand from the skincare, healthcare, and wellness industries. The region’s market is influenced by increasing awareness of ingredient transparency and regulatory compliance led by the U.S. FDA’s evolving cosmetic standards. The adoption of AI-driven skin diagnostics and digital retail transformation has grown by 39%, enabling brands to enhance consumer personalization and marketing accuracy. Local players and distributors are expanding collaborations with Japanese manufacturers to introduce hybrid skincare products tailored to Western consumers. For instance, a U.S.-based beauty retailer launched an AI-powered personalization platform that achieved 21% higher consumer engagement rates within six months. North American consumers exhibit high preference for anti-aging and UV-protection skincare products, with 64% prioritizing formulations containing natural and clinically proven ingredients.

What drives increasing preference for sustainable and clean beauty innovations across this region?

Europe captured approximately 27% of the global J-Beauty Products Market in 2024, led by Germany, the United Kingdom, and France. European regulatory frameworks such as the EU Cosmetics Regulation have accelerated demand for ingredient transparency and eco-certified products. Sustainability initiatives, including recyclable packaging and low-emission production systems, have driven regional adoption rates up by 33% in the past three years. The integration of digital skincare diagnostics and smart retail kiosks in the UK and France has enhanced consumer engagement and brand trust. Local distributors are focusing on importing Japanese biotechnology-based skincare lines to meet the growing preference for minimalist and ethical beauty. European consumers tend to favor clean beauty formulations, with over 58% actively choosing paraben-free and vegan-certified J-Beauty products that align with environmental and health-conscious lifestyles.

How are innovation ecosystems and advanced manufacturing hubs shaping growth in this region?

Asia-Pacific dominated the J-Beauty Products Market with 43% share in 2024, reflecting its strong production capacity and rapid product innovation cycles. Japan, China, and South Korea remain top consumers and exporters, supported by advanced R&D ecosystems and government-driven initiatives promoting biotechnology and clean-beauty development. More than 72% of Japan’s cosmetics exports are distributed within Asia-Pacific, reinforcing its regional leadership. Smart manufacturing hubs integrating IoT-enabled production lines have improved operational efficiency by 27% across major facilities. Local giants like Shiseido and Kosé are pioneering digital beauty ecosystems, using AI and augmented reality for personalized product selection. Regional consumers are increasingly tech-savvy, with 68% making purchases through mobile platforms and social commerce channels, underscoring e-commerce as a major growth catalyst.

How is increasing middle-class spending power influencing beauty product adoption across this region?

South America accounted for 7% of the global J-Beauty Products Market in 2024, led by Brazil and Argentina. The region’s growing beauty-conscious middle-class population has contributed to a 22% increase in demand for imported skincare and cosmetics over the past two years. Brazil, being one of the top global beauty consumers, has witnessed expansion in retail outlets featuring J-Beauty brands. Government incentives promoting cosmetic imports and bilateral trade policies with Japan have facilitated smoother supply chain integration. Local distributors have begun offering customized J-Beauty solutions suited for tropical climates, improving customer satisfaction by 19%. Regional consumers are influenced by media trends and celebrity endorsements, with 58% preferring lightweight, non-greasy skincare formulations ideal for humid environments.

How are luxury beauty preferences and modern retail expansion driving growth across this region?

The Middle East & Africa accounted for approximately 5% of the J-Beauty Products Market in 2024, led by countries such as the UAE, Saudi Arabia, and South Africa. The region’s growing luxury retail segment has fueled demand for high-end Japanese skincare and anti-aging products, particularly within urban centers. Rapid retail modernization and digital adoption have increased online cosmetic sales by 34% year-on-year. Government trade partnerships with Asian countries have enhanced the distribution of premium imports. Local retailers in the UAE are launching dedicated J-Beauty product lines within luxury malls, attracting an affluent consumer base. Regional buyers prioritize long-lasting and climate-adapted formulations, with 62% of consumers preferring lightweight, hydrating products suitable for dry climates, emphasizing the growing alignment between lifestyle needs and product innovation.

• Japan – 31% Market Share: Japan leads the J-Beauty Products Market due to its advanced manufacturing infrastructure, deep-rooted skincare culture, and consistent investment in biotechnological innovations.

• China – 19% Market Share: China follows, driven by high consumer adoption rates, expanding online retail channels, and rapid integration of personalized skincare technologies that enhance accessibility and convenience.

The global J-Beauty Products market exhibits a moderately consolidated structure, with the top five players collectively accounting for approximately 48% of total market share in 2024. Around 220 active competitors operate globally, including established Japanese skincare giants, international cosmetics conglomerates, and emerging indie brands that leverage niche, clean-beauty positioning. Leading players are increasingly focusing on product personalization, natural formulations, and biotechnology-driven skincare innovations to maintain a competitive edge.

Strategic alliances and product launches remain central to competition. Over 35 notable collaborations were recorded in 2023–2024, primarily aimed at expanding distribution channels across Asia-Pacific and Europe. Mergers and acquisitions also rose by 17%, with companies targeting smaller, ingredient-focused brands to enhance their sustainable product portfolios. R&D investments climbed by nearly 28% year-over-year, reflecting a market-wide emphasis on microbiome skincare, fermentation-based actives, and AI-driven personalization.

The competitive intensity is further influenced by digital engagement strategies, with over 60% of brands adopting direct-to-consumer (D2C) models and AI-powered skin analysis tools. Japan-based companies dominate innovation benchmarks, but Western competitors are gaining traction through technology integration and hybrid skincare-makeup lines. Market players are also investing in eco-friendly packaging and vegan-certified products, catering to the rising consumer demand for ethical beauty solutions. Overall, the competitive environment is defined by innovation, sustainability, and omnichannel retail expansion.

Pola Orbis Holdings Inc.

Fancl Corporation

DHC Corporation

Hada Labo (Rohto Pharmaceutical Co., Ltd.)

SK-II (Procter & Gamble)

Kanebo Cosmetics Inc.

Suqqu (E’quipe, Ltd.)

Astalift (Fujifilm Holdings Corporation)

Minon (Daiichi Sankyo Healthcare Co., Ltd.)

Curel (Kao Group subsidiary)

Hacci 1912

Albion Co., Ltd.

Technological innovation is reshaping the J-Beauty Products market, with advancements in biotechnology, digital personalization, and sustainable formulation techniques driving new product differentiation. In 2024, approximately 63% of new product launches in Japan incorporated bioactive ingredients derived through fermentation and enzymatic extraction, enabling enhanced skin compatibility and long-term efficacy. Nanotechnology is also becoming a core innovation driver, with over 40% of premium skincare lines utilizing nano-encapsulation methods to improve active ingredient delivery and absorption efficiency by up to 70%.

Artificial intelligence (AI) and data analytics are playing a crucial role in product customization and consumer engagement. Around 55% of leading brands now employ AI-powered skin diagnostic tools and virtual skin analysis apps that analyze parameters like hydration, pigmentation, and elasticity to recommend tailored formulations. This integration of AI-driven skincare has improved consumer retention by 30% across digital platforms. Moreover, smart packaging solutions embedded with QR codes or NFC tags—used by nearly 25% of J-Beauty brands—offer authenticity verification and personalized product information.

Sustainability-focused technologies are further redefining manufacturing and formulation processes. Over 50% of production facilities have transitioned to eco-efficient systems using renewable energy and recyclable materials. Additionally, biotechnology is advancing cruelty-free alternatives, such as plant-based collagen and lab-cultured hyaluronic acid, reducing dependency on animal-derived ingredients by 45%. Collectively, these innovations are enabling J-Beauty companies to merge traditional Japanese skincare principles with cutting-edge science, ensuring long-term competitiveness in an increasingly technology-driven beauty landscape.

The J-Beauty Products Market Report provides a comprehensive analysis of the global landscape covering key product types, applications, end-user categories, and regional dynamics. The study examines over 20 core product types, including serums, cleansers, moisturizers, and sun protection solutions, representing more than 85% of total market activity. It also evaluates niche segments such as hybrid makeup-skincare products and fermented ingredient formulations, which have gained nearly 15% market share growth in the past three years.

The report spans five key regional markets—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—highlighting adoption patterns, consumer preferences, and regulatory frameworks across 25 major countries. Asia-Pacific remains the dominant region, accounting for approximately 45% of global demand, followed by Europe with 27%.

Technological coverage extends to biotechnology-based formulations, AI-enabled personalization, nanotechnology applications, and eco-friendly packaging systems. End-user insights encompass both offline retail and digital e-commerce channels, with online platforms now contributing over 38% of total sales. Furthermore, the report identifies sustainability-driven shifts in manufacturing and the growing role of smart packaging and bioengineered actives. By combining quantitative metrics with qualitative analysis, it equips stakeholders with actionable intelligence on innovation, competitive positioning, and strategic investment opportunities shaping the global J-Beauty Products landscape.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 33932.68 Million |

Market Revenue in 2032 | USD 46246.76 Million |

CAGR (2025 - 2032) | 3.5% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Shiseido Company, Limited, Kao Corporation, Kosé Corporation, Pola Orbis Holdings Inc., Fancl Corporation, DHC Corporation, Hada Labo (Rohto Pharmaceutical Co., Ltd.), SK-II (Procter & Gamble), Kanebo Cosmetics Inc., Suqqu (E’quipe, Ltd.), Astalift (Fujifilm Holdings Corporation), Minon (Daiichi Sankyo Healthcare Co., Ltd.), Curel (Kao Group subsidiary), Hacci 1912, Albion Co., Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |