Reports

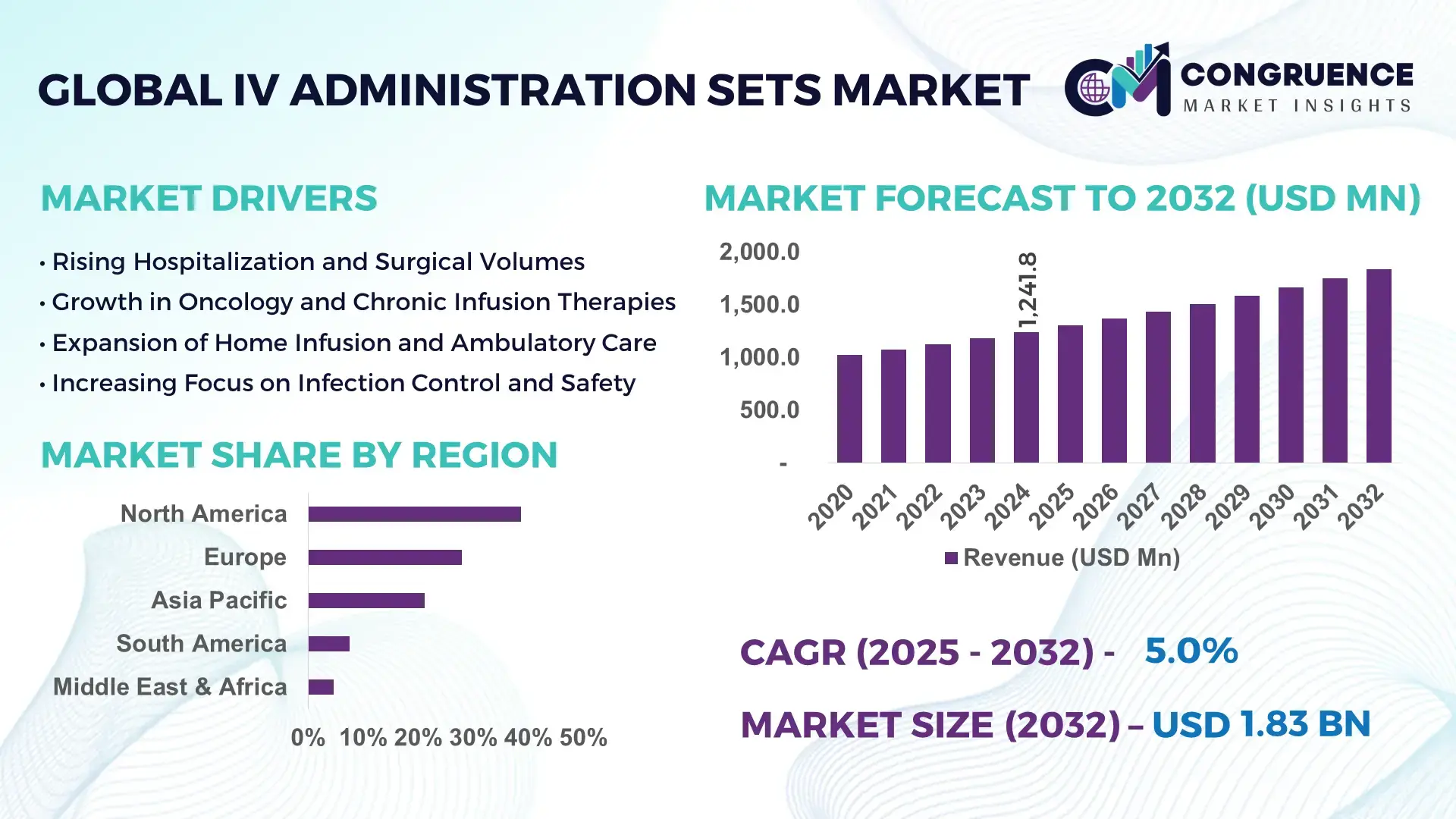

The Global IV Administration Sets Market was valued at USD 1,241.8 Million in 2024 and is anticipated to reach a value of USD 1,834.7 Million by 2032 expanding at a CAGR of 5.0% between 2025 and 2032, according to an analysis by Congruence Market Insights, primarily driven by rising hospitalization volumes, growth in chronic disease prevalence, and standardized intravenous therapy protocols across acute and long-term care settings.

The United States represents the most industrially dominant country in the IV Administration Sets market, supported by large-scale domestic manufacturing capacity, advanced medical device sterilization infrastructure, and sustained procurement by hospital networks. The country operates more than 140 FDA-registered IV set manufacturing and assembly facilities, with annual production volumes exceeding 9.5 billion IV tubing and component units, serving hospitals, ambulatory surgery centers, and home infusion providers. Capital investments in medical disposables manufacturing surpassed USD 2.1 billion between 2021 and 2024, with over 30% allocated to automation, inline quality inspection, and DEHP-free material conversion. IV administration sets are extensively used across oncology, critical care, and emergency medicine, where infusion therapy accounts for nearly 68% of inpatient medication delivery events, underscoring the country’s high utilization intensity and continuous innovation in safety-engineered infusion devices.

Market Size & Growth: USD 1,241.8 Million in 2024, projected to reach USD 1,834.7 Million by 2032 at a CAGR of 5.0%, supported by rising inpatient admissions and infusion-based therapies.

Top Growth Drivers: Increase in IV drug administration procedures (46%), growth in chronic disease infusion treatments (39%), expansion of outpatient and home infusion services (31%).

Short-Term Forecast: By 2028, adoption of closed-system and needle-free connectors is expected to reduce infusion-related contamination risks by ~24%.

Emerging Technologies: DEHP-free tubing materials, anti-reflux valves, integrated air-elimination filters.

Regional Leaders: North America (~USD 612M by 2032) driven by hospital demand; Europe (~USD 458M) supported by safety regulations; Asia Pacific (~USD 522M) led by volume growth.

Consumer/End-User Trends: Hospitals prefer pre-assembled sterile IV sets to reduce setup time; homecare favors lightweight gravity-based sets.

Pilot or Case Example: 2023 hospital pilot reduced IV setup time by 19% through standardized disposable infusion kits.

Competitive Landscape: Market leader holds ~18% share, followed by several global players each with 6–10%.

Regulatory & ESG Impact: Shift toward PVC-free and recyclable materials driven by hospital sustainability mandates.

Investment & Funding Patterns: Over USD 1.6 billion invested globally in IV disposables manufacturing upgrades since 2021.

Innovation & Future Outlook: Smart flow-control integration and antimicrobial coatings shaping next-generation IV sets.

IV Administration Sets are critical consumables across hospitals (approx. 62% usage), ambulatory care (21%), and home infusion (17%). Product innovation focuses on infection prevention, simplified priming, and compatibility with high-risk drug infusions. Regulatory emphasis on patient safety, combined with aging populations and expanding infusion therapies, continues to support steady global demand.

The IV Administration Sets Market holds strategic importance as a foundational component of modern healthcare delivery, enabling safe, precise, and scalable administration of intravenous fluids, medications, blood products, and nutrition. Over 70% of hospitalized patients globally receive at least one IV therapy during admission, making IV sets a non-discretionary medical consumable with predictable replacement cycles. Technological advancements such as needle-free connectors deliver ~32% reduction in needlestick injury incidents compared to conventional luer access ports, directly impacting occupational safety metrics.

Regionally, Asia Pacific dominates in volume, accounting for the highest unit consumption driven by large patient populations and expanding hospital infrastructure, while North America leads in adoption, with over 78% of tertiary hospitals standardizing safety-enhanced IV administration sets. By 2027, integration of precision flow regulators and anti-free-flow mechanisms is expected to reduce medication dosing errors by ~21% in acute care settings. From an ESG standpoint, manufacturers are committing to PVC and DEHP reduction targets, aiming for 30–40% lower plasticizer usage by 2028, aligning with hospital sustainability procurement policies.

In a measurable micro-scenario, in 2024, a U.S.-based hospital network transitioned to closed-system IV administration sets across 24 facilities, achieving a 26% reduction in central line-associated bloodstream infections (CLABSI) within one year. Looking ahead, the IV Administration Sets Market will remain a pillar of healthcare resilience, driven by regulatory compliance, patient safety priorities, and scalable infusion therapy models supporting both inpatient and home-based care delivery.

The IV Administration Sets market dynamics are shaped by patient safety regulations, increasing infusion therapy volumes, and hospital efficiency mandates. Demand is strongly correlated with hospital admission rates, surgical procedures, and chronic disease management, particularly oncology, renal care, and critical care medicine. Healthcare systems are shifting toward standardized IV kits to reduce nursing workload and procedural variability. On the supply side, manufacturers are investing in automated extrusion, precision molding, and inline sterilization to meet rising volume requirements while maintaining sterility assurance levels exceeding 10⁻⁶. Cost pressures from group purchasing organizations (GPOs) influence pricing structures, while regulatory scrutiny on material safety and infection prevention continues to reshape product design and procurement criteria.

Chronic diseases such as cancer, diabetes, and renal failure require repeated intravenous drug delivery, driving sustained demand for IV administration sets. Oncology infusion volumes increased by ~34% between 2020 and 2024, while dialysis-related IV usage grew by ~28%, reinforcing recurring consumption. Hospitals increasingly rely on high-flow and precision-controlled IV sets to manage complex medication regimens, supporting consistent procurement volumes.

Large hospital networks and GPOs exert strong pricing pressure, compressing margins for manufacturers. Standardization initiatives often favor a limited number of approved IV set configurations, reducing product differentiation. Additionally, compliance costs associated with sterilization validation, material testing, and regulatory documentation add ~12–15% to production expenses, limiting rapid product diversification.

Home infusion therapy is expanding rapidly, with patient preference and cost-containment driving adoption. Home-based IV therapy volumes increased by ~41% over the last four years, creating demand for lightweight, easy-to-use gravity and elastomeric-compatible IV sets. Manufacturers offering compact, user-friendly designs tailored for non-clinical environments are well-positioned to capture incremental demand.

Despite advancements, infusion-related infections remain a concern. Ensuring consistent aseptic handling across varied care settings is difficult. Manufacturers must balance complexity and ease-of-use, as additional safety features can increase setup time by ~8–10%, requiring training and workflow adaptation.

• Shift Toward Safety-Engineered IV Sets: Adoption of needle-free connectors and anti-reflux valves increased by ~37% since 2021, driven by occupational safety regulations and hospital infection control protocols. Facilities using safety-engineered sets reported ~29% fewer needlestick incidents.

• Expansion of DEHP-Free and PVC-Free Materials: More than 48% of newly launched IV administration sets now use alternative polymers, reducing patient exposure to plasticizers and supporting hospital sustainability targets.

• Growth of Pre-Assembled and Custom IV Kits: Pre-configured IV kits reduced nursing preparation time by ~22% and medication administration errors by ~17%, accelerating adoption in high-throughput hospital units.

• Rising Demand from Home and Ambulatory Care: Ambulatory infusion centers increased IV set consumption by ~33% between 2022 and 2024, favoring compact, disposable sets optimized for rapid turnover and portability.

The IV Administration Sets market is segmented by type, application, and end-user, reflecting variations in infusion complexity, patient risk profiles, and care delivery settings. Segmentation trends are closely tied to hospitalization rates, therapy duration, infection prevention mandates, and workflow efficiency requirements. Product differentiation increasingly centers on safety mechanisms, material composition, and compatibility with modern infusion protocols. Demand patterns show clear divergence between acute care hospitals, ambulatory facilities, and home infusion providers, each prioritizing different performance attributes such as flow precision, ease of handling, and disposability. Across regions, segmentation is also influenced by regulatory stringency, reimbursement frameworks, and healthcare infrastructure maturity. As infusion therapies become more complex—particularly in oncology, critical care, and biologics administration—segmentation is shifting toward higher-value, safety-enhanced IV administration sets with integrated control and protection features.

Primary IV administration sets represent the largest product segment, accounting for approximately 46–48% of total global usage, as they are universally required for continuous fluid and medication delivery across inpatient settings. Their dominance is reinforced by high-frequency use in medical wards, emergency departments, and ICUs, where uninterrupted infusion is critical. Secondary (piggyback) IV sets account for roughly 23–25% of demand, driven by intermittent drug administration protocols, particularly antibiotics and short-duration therapies. Blood administration sets contribute around 17–19%, reflecting rising transfusion volumes linked to surgical procedures, trauma care, and oncology support. Specialty IV sets—including chemotherapy-specific, filtered, and photo-protective variants—collectively represent 10–12% of the market but demonstrate the fastest expansion, with an estimated ~7% CAGR, supported by growth in high-risk drug infusions and stricter safety standards. Manufacturers increasingly focus on modular designs that allow hospitals to standardize across multiple infusion scenarios while maintaining clinical specificity.

Medication infusion is the leading application, accounting for approximately 52–54% of global IV administration set utilization, driven by the high volume of intravenous drug delivery in both acute and chronic care. Blood and blood component transfusion applications hold around 20–22%, supported by rising surgical volumes and trauma admissions. Parenteral nutrition accounts for nearly 16–18%, particularly in neonatal, geriatric, and critical care units where enteral feeding is not feasible. Emergency hydration and electrolyte replacement make up the remaining 8–10%, with strong demand from emergency departments and disaster response settings. Among applications, oncology-related medication infusion is the fastest-growing, with infusion volumes increasing by ~35% over the past four years, driving demand for high-precision, low-adsorption IV sets. In 2024, more than 61% of hospitals reported increased complexity in IV drug regimens, reinforcing the need for application-specific IV administration solutions.

Hospitals remain the dominant end-user segment, accounting for approximately 61–63% of global IV administration set consumption, reflecting high inpatient volumes and intensive IV therapy usage across departments. Ambulatory surgery centers and infusion clinics contribute around 20–22%, supported by the shift toward same-day procedures and outpatient biologic therapies. Homecare and home infusion providers represent 15–17%, but this segment is expanding most rapidly, with an estimated ~7.2% CAGR, driven by cost containment strategies and patient preference for at-home treatment. Adoption rates in home infusion are particularly strong for gravity-based and simplified IV sets, with over 58% of providers favoring designs that minimize setup complexity. Across all end-users, infection prevention and ease-of-use remain top procurement priorities, while sustainability considerations are increasingly influencing purchasing decisions.

North America accounted for the largest market share at 38.6% in 2024, however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America’s leadership is underpinned by high hospitalization rates, standardized infusion protocols, and widespread adoption of safety-engineered IV administration sets. Europe followed with approximately 27.9% share in 2024, supported by stringent patient safety regulations and growing preference for PVC-free medical disposables. Asia Pacific ranked first in volume consumption, driven by large patient populations and rapid expansion of hospital infrastructure in China and India, where hospital bed capacity increased by ~14% since 2021. South America and Middle East & Africa collectively accounted for ~12.4% of global demand, with growth linked to public healthcare investments and gradual modernization of infusion therapy standards. Regional disparities in regulatory enforcement, healthcare spending, and care delivery models continue to shape IV administration set demand patterns globally.

How Is Advanced Clinical Infrastructure Accelerating Adoption of Safer IV Delivery Systems?

North America accounted for approximately 38–40% of the global IV Administration Sets market volume in 2024, reflecting high per-capita healthcare utilization and standardized infusion protocols across care settings. Demand is primarily driven by acute care hospitals, oncology centers, emergency departments, and home infusion providers, with hospitals alone consuming over 62% of regional volumes. Regulatory oversight from agencies such as the FDA has accelerated adoption of safety-engineered IV sets, particularly needleless connectors and closed-system transfer devices, contributing to a ~28% reduction in needlestick injuries over the past five years. Digital transformation is evident through integration of IV sets with smart infusion pumps and barcode medication administration systems, now deployed in over 70% of large hospitals. A notable regional player, Becton, Dickinson and Company, has expanded production of low-adsorption and PVC-free IV sets to support biologics and oncology therapies. Consumer behavior reflects strong preference for safety-certified, single-use products, with higher adoption in healthcare systems emphasizing risk mitigation and compliance.

How Are Regulatory Mandates Reshaping Infusion Safety and Product Design?

Europe represented roughly 27–29% of global IV Administration Sets consumption in 2024, supported by mature public healthcare systems and strict patient safety frameworks. Germany, the UK, and France together account for over 55% of regional demand, driven by high inpatient admissions and surgical volumes. Regulatory bodies emphasize infection control and material safety, accelerating the shift toward PVC-free and DEHP-free IV sets, which now represent nearly 34% of new procurement contracts. Sustainability initiatives under EU medical device regulations have also pushed manufacturers to reduce material waste by 15–20% per unit. Adoption of emerging technologies such as anti-reflux valves and inline filtration has increased, particularly in critical care. A leading regional manufacturer, Fresenius Kabi, continues to invest in precision flow-control IV systems tailored for parenteral nutrition. Consumer behavior in the region reflects strong compliance-driven purchasing, with healthcare providers prioritizing traceability, transparency, and explainable product performance.

What Is Driving High-Volume Adoption Across Expanding Healthcare Systems?

Asia-Pacific is the largest market by volume, accounting for over 41% of global IV Administration Sets usage in 2024, driven by large patient populations and rapid hospital expansion. China, India, and Japan collectively contribute more than 65% of regional consumption, supported by rising surgical procedures and chronic disease prevalence. Infrastructure investments have expanded hospital bed capacity by ~18% since 2020, directly increasing IV therapy demand. Manufacturing trends favor cost-efficient, high-throughput production, with regional facilities supplying both domestic and export markets. Technology adoption focuses on simplified, gravity-based IV sets and scalable safety features to balance cost and performance. A prominent regional supplier, Nipro Corporation, has increased output of disposable IV sets optimized for high-volume hospital use. Consumer behavior shows strong reliance on hospital-based care, with rapid uptake of affordable, standardized IV solutions across public health systems.

How Are Public Healthcare Investments Supporting Gradual Market Expansion?

South America accounted for approximately 7–8% of global IV Administration Sets demand in 2024, with Brazil and Argentina representing over 60% of regional consumption. Growth is closely linked to public healthcare spending, expansion of emergency care infrastructure, and increasing surgical interventions. Government incentives aimed at improving access to essential medical supplies have supported procurement of basic IV sets, particularly in public hospitals. Infrastructure upgrades in urban centers have increased ICU capacity by ~12% over four years, directly impacting IV usage. Regional manufacturers focus on affordability and supply reliability rather than advanced features. A regional producer, B. Braun Brasil, has expanded local assembly to reduce import dependency. Consumer behavior remains price-sensitive, with strong demand for durable, standardized IV administration sets suited to high patient throughput environments.

How Is Healthcare Modernization Creating New Demand for Infusion Technologies?

The Middle East & Africa region contributed roughly 4–5% of global IV Administration Sets consumption in 2024, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Regional growth is supported by hospital modernization programs and rising trauma and surgical care volumes. In the Gulf region, private healthcare investment has increased hospital capacity by ~20% since 2019, driving procurement of higher-quality IV sets. Technological modernization includes adoption of needleless IV systems and infection-resistant materials, particularly in tertiary care facilities. Trade partnerships have improved access to certified medical disposables across Africa. A key supplier, Medtronic, supports regional distribution of advanced infusion accessories through local partnerships. Consumer behavior varies widely, with premium adoption in private hospitals and cost-driven purchasing in public healthcare systems.

United States – ~31% market share

Dominates the IV Administration Sets market due to high hospitalization rates, advanced infusion protocols, and stringent patient safety regulations.

China – ~18% market share

Leads through large-scale hospital infrastructure, high inpatient volumes, and extensive domestic manufacturing capacity for IV administration sets.

The IV Administration Sets market includes over 40 active manufacturers, with moderate consolidation. The top five companies collectively hold approximately ~52% of global shipments. Competition centers on safety features, material compliance, and large-scale supply reliability. Strategic initiatives include capacity expansion, portfolio rationalization, and partnerships with hospital networks. Innovation focuses on infection prevention, sustainability, and workflow efficiency. Regional manufacturers compete on cost, while global players leverage regulatory expertise and broad distribution.

Baxter International

Fresenius Kabi

ICU Medical

Smiths Medical

Nipro Corporation

Teleflex

Polymedicure

Cardinal Health

Vygon

JMS Co., Ltd.

Weigao Group

Technological innovation in IV administration sets centers on safety, material science, and usability. Needle-free connectors and closed-system transfer devices reduce contamination risk and occupational exposure. Advanced polymers replace traditional PVC, improving chemical compatibility and patient safety. Integrated flow regulators deliver ~15–20% improved dosing accuracy. Manufacturing advances such as inline vision inspection and automated assembly improved defect detection by ~17%. Future developments include antimicrobial coatings, smart flow indicators, and enhanced compatibility with infusion pumps, supporting safer and more efficient IV therapy delivery.

• In March 2024, BD expanded its safety-engineered IV administration set portfolio to support closed-system infusion protocols across hospital networks. Source: www.bd.com

• In July 2023, B. Braun introduced PVC-free IV sets aligned with hospital sustainability goals. Source: www.bbraun.com

• In January 2024, Terumo enhanced its IV tubing production capacity to meet rising oncology infusion demand. Source: www.terumo.com

• In September 2023, Baxter optimized its IV set sterilization processes to improve supply reliability for acute care hospitals. Source: www.baxter.com

The IV Administration Sets Market Report delivers a comprehensive evaluation of global demand, product innovation, and competitive positioning across healthcare delivery settings. The scope includes detailed analysis of primary, secondary, blood, and specialty IV administration sets, assessing performance attributes such as flow accuracy, safety mechanisms, material compliance, and sterilization methods. Applications covered include medication infusion, blood transfusion, parenteral nutrition, and emergency hydration therapy.

Geographic coverage spans North America, Europe, Asia Pacific, South America, and Middle East & Africa, with country-level insights into the United States, China, Germany, Japan, and Brazil. The report evaluates end-users including hospitals, ambulatory care centers, and home infusion providers, analyzing procurement behavior, usage intensity, and safety preferences. Manufacturing trends, regulatory frameworks, sustainability initiatives, and emerging technologies such as antimicrobial tubing and smart infusion compatibility are assessed to provide a holistic market view. This scope supports informed decision-making for manufacturers, healthcare providers, investors, and policymakers navigating the evolving IV administration ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1,241.8 Million |

|

Market Revenue in 2032 |

USD 1,834.7 Million |

|

CAGR (2025 - 2032) |

5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Becton, Dickinson and Company, B. Braun Melsungen AG, Terumo Corporation, Baxter International, Fresenius Kabi, ICU Medical, Smiths Medical, Nipro Corporation, Teleflex, Polymedicure, Cardinal Health, Vygon, JMS Co., Ltd., Weigao Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |