Reports

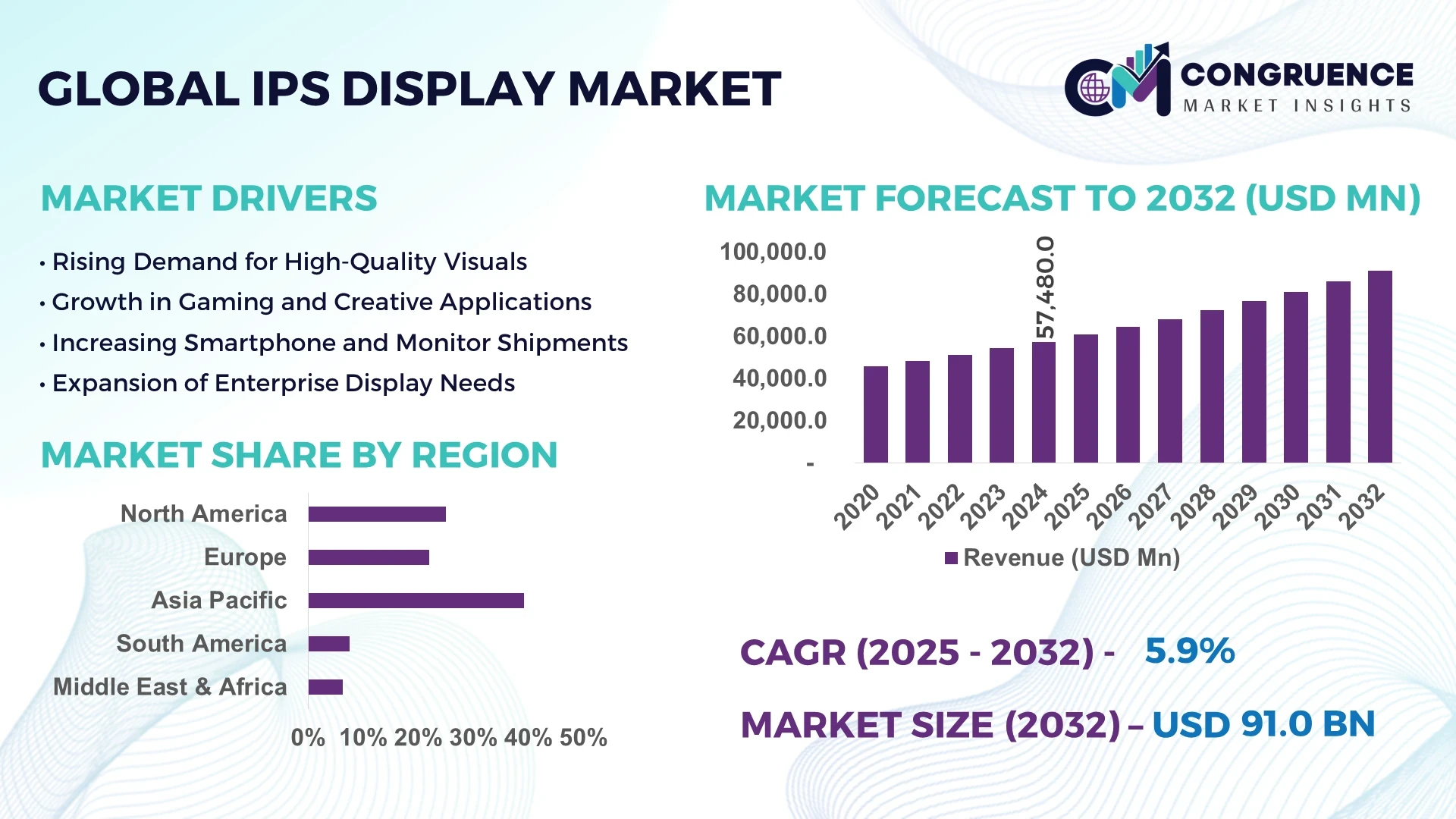

The Global IPS Display Market was valued at USD 57,480 Million in 2024 and is anticipated to reach a value of USD 90,993.94 Million by 2032, expanding at a CAGR of 5.91% between 2025 and 2032.

Japan currently leads the IPS Display market, driven by significant technological advancements and high demand for high-quality display panels across consumer electronics, automotive, and industrial applications.

The IPS (In-Plane Switching) display technology has witnessed widespread adoption due to its superior color accuracy, wide viewing angles, and enhanced brightness, making it highly favored for applications such as smartphones, tablets, monitors, and televisions. The market is fueled by increasing demand for displays that provide a premium visual experience in a variety of sectors, including consumer electronics, automotive, and medical industries. The adoption of IPS displays has grown in line with the demand for better screen technology, with manufacturers focusing on integrating enhanced features like 4K and OLED display options to meet the evolving consumer demands. Key players in the market are continuously working towards reducing production costs while improving the efficiency and durability of IPS panels to capture a larger share of the growing market.

Artificial Intelligence (AI) is significantly shaping the future of the IPS Display market by enhancing the overall user experience and improving display functionalities. AI technologies such as machine learning and deep learning are being integrated into IPS displays to optimize display settings based on real-time environmental conditions, user preferences, and content being displayed. AI-powered adaptive brightness adjustment, for example, automatically modifies the screen brightness depending on surrounding light conditions, providing better visibility and energy efficiency. Additionally, AI algorithms are being employed to enhance color accuracy and contrast, improving the overall image quality and creating more vivid, lifelike visuals.

AI is also playing a role in predictive maintenance, reducing downtime for commercial IPS displays by identifying potential issues before they occur, helping businesses minimize repair costs and downtime. AI-enabled features are also being used in the creation of more interactive displays, such as in digital signage and smart home applications. Machine learning enables these displays to adjust content and layout dynamically, responding to factors like the time of day, weather, or specific user behavior.

In the automotive sector, AI integration is helping IPS displays adapt to specific conditions like road visibility, providing the driver with optimal visibility based on real-time environmental data, enhancing safety and driving comfort. AI is also expected to play a key role in improving the resolution and performance of IPS displays in advanced applications like AR/VR, as these technologies demand ultra-high-definition displays.

"In 2024, a major smartphone manufacturer integrated AI-driven display technology into their latest flagship model, enabling real-time optimization of screen settings based on user behavior and ambient lighting conditions."

The rapid growth of the global consumer electronics industry has significantly increased the demand for IPS displays due to their superior image quality and consistent color reproduction. With over 1.4 billion smartphones sold globally in 2024, many of them now feature IPS panels, offering better viewing experiences compared to traditional displays. Additionally, 4K and 8K televisions are pushing manufacturers to use IPS technology, which ensures wider viewing angles, particularly important in large living spaces. The gaming monitor segment has also surged, with gamers favoring IPS displays for their faster response times and color accuracy, fueling further demand.

Despite their advantages, IPS displays remain more expensive to produce than other display technologies such as TN (Twisted Nematic) panels. The production of IPS panels requires advanced manufacturing processes, multiple layers of alignment, and premium materials, which drive up the cost. For example, while TN panels may cost up to 30% less to manufacture, IPS panels involve more intricate electrode arrangements and sophisticated alignment layers. As a result, manufacturers in cost-sensitive markets often choose cheaper alternatives, limiting the mass adoption of IPS technology. Furthermore, fluctuating prices of liquid crystal materials and color filters further add to cost uncertainties.

The adoption of IPS display panels is expanding rapidly in the automotive and medical equipment industries due to their exceptional image clarity, wide viewing angles, and stability under extreme conditions. In automotive applications, IPS panels are used in infotainment systems, digital dashboards, and rear-seat entertainment due to their ability to perform well under varying lighting conditions. The global automotive display shipments surpassed 180 million units in 2024, with a notable share using IPS technology. In the healthcare sector, IPS displays are integrated into diagnostic equipment, surgical monitors, and patient interfaces due to their precision and reliability, especially in critical medical environments.

The IPS display market faces strong competition from OLED and AMOLED technologies, which offer even higher contrast ratios, deeper blacks, and flexibility in design. OLED displays, now used in a growing number of flagship smartphones and premium TVs, are capturing market share by offering thinner and more energy-efficient designs. As production costs for OLEDs continue to decline, many manufacturers are shifting focus away from IPS. Additionally, AMOLED panels dominate in the wearable device market due to their flexibility and lower power consumption, leaving IPS displays with limited room for growth in that segment. This competitive pressure is challenging IPS panel manufacturers to innovate or lose relevance.

• Growth in Gaming Monitors and High Refresh Rate Displays: The IPS Display Market is experiencing a surge in demand from the gaming sector. Gaming monitors featuring IPS panels are now offering refresh rates as high as 360Hz, which was previously only achievable in TN panels. IPS displays provide better color accuracy and wide viewing angles, making them ideal for immersive gaming experiences. In 2024, over 45% of gaming monitors shipped globally used IPS technology. Major gaming hardware manufacturers are releasing high-end IPS displays, catering to esports professionals and content creators who prioritize both performance and visual fidelity.

• Proliferation of IPS Displays in Automotive Infotainment: Automotive manufacturers are increasingly integrating IPS displays into infotainment and dashboard systems. These displays offer superior sunlight readability and consistent performance under varied temperature and lighting conditions. In 2024, over 60% of newly launched premium cars included IPS-based central console displays. The integration of touchscreens, voice-enabled UI, and AI-powered driver-assistance displays in vehicles is driving demand for high-performance IPS panels, particularly in electric and autonomous vehicles, which rely heavily on digital interfaces.

• Adoption in Industrial and Medical Equipment: Industrial and medical sectors are shifting toward IPS displays due to their reliability, durability, and clarity. Medical devices such as surgical monitors and diagnostic imaging systems use IPS panels for their ability to present detailed, color-accurate visuals. Industrial control panels and human-machine interfaces (HMIs) also favor IPS due to their resistance to color shifts and wide viewing capabilities. In 2024, nearly 35% of industrial-grade monitors featured IPS technology, particularly in Europe and Asia-Pacific, where healthcare digitization and smart manufacturing are rapidly evolving.

• Emergence of Ultra-Wide and Curved IPS Displays: The demand for ultra-wide and curved IPS monitors is on the rise, especially among professionals in video editing, graphic design, and financial trading. These displays allow for multi-window functionality without the need for multiple screens, improving workflow efficiency. In 2024, shipments of ultra-wide IPS monitors grew by over 22%, with North America and East Asia accounting for the majority of demand. Curved IPS displays are also gaining ground in the gaming and home entertainment segments, offering a more immersive experience while maintaining color consistency and visual clarity.

The IPS Display Market is segmented based on type, application, and end-user verticals. IPS technology has penetrated a wide range of sectors owing to its enhanced visual output and display precision. Types include Advanced Super IPS, Professional IPS, Horizontal IPS, and eIPS. Applications range from consumer electronics and automotive to industrial and medical equipment. End-users span individual consumers, corporate professionals, automotive OEMs, and healthcare institutions. Among all, consumer electronics dominate the volume of shipments, while automotive and medical applications show fast-paced adoption. Each segment contributes uniquely to the evolving demand patterns and technology developments in the IPS Display Market.

The IPS Display Market is classified into Advanced Super IPS (AS-IPS), Enhanced IPS (e-IPS), Horizontal IPS (H-IPS), and Professional IPS (P-IPS). Among these, Enhanced IPS (e-IPS) led the market in 2024 with the highest market share due to its cost-effectiveness and improved transmittance, making it highly suitable for consumer electronics like smartphones, tablets, and monitors. Professional IPS (P-IPS), offering ultra-high color accuracy, is gaining traction in the creative industries such as video editing and graphic design. H-IPS is widely used in high-end monitors, particularly in healthcare and industrial control systems. AS-IPS displays, although limited in deployment, are utilized where higher brightness and viewing angles are necessary. The fastest-growing type is Professional IPS, driven by the surge in demand for color-critical applications and content creation tools. Its precision in displaying a wide color gamut has made it a preferred choice for high-performance display monitors globally.

The application spectrum of IPS Displays includes Consumer Electronics, Automotive Displays, Industrial Equipment, Medical Devices, and Digital Signage. Consumer Electronics emerged as the leading segment in 2024, contributing to over 50% of global shipments. IPS panels are extensively used in smartphones, tablets, TVs, and monitors due to their excellent viewing angles and high-resolution capabilities. Automotive Displays are the fastest-growing segment owing to the transition toward digital dashboards and in-vehicle infotainment systems. The adoption of IPS panels in mid-range and premium vehicle categories has expanded considerably, particularly in Asia-Pacific and Europe. In Industrial Equipment, IPS displays are favored in factory automation systems, offering durability and clear visuals. Medical Devices also increasingly depend on IPS technology for accurate diagnostics and imaging. Digital Signage, although niche, is gaining traction in smart retail and advertising spaces. The growing need for high-performance displays across all these applications continues to fuel the demand for advanced IPS solutions.

The key end-user categories in the IPS Display Market include Individual Consumers, Enterprises, Automotive OEMs, Healthcare Institutions, and Industrial Users. Individual Consumers remain the dominant end-user segment, with widespread use of IPS displays in personal computing, gaming, and home entertainment systems. As of 2024, over 70% of premium smartphones and nearly 60% of monitors sold globally featured IPS panels. Enterprises are integrating IPS displays for collaborative work environments, digital whiteboards, and high-end computing setups. Automotive OEMs are rapidly incorporating IPS technology into dashboard and infotainment interfaces, particularly in electric and luxury vehicles. Healthcare Institutions represent the fastest-growing end-user segment, driven by the integration of IPS displays in diagnostic monitors, telemedicine equipment, and surgical visualization systems. Industrial Users rely on IPS displays for control room interfaces and HMI systems. The market’s end-user diversity is a major driver of product innovation and long-term sustainability in the IPS Display ecosystem.

Asia-Pacific accounted for the largest market share at 39.2% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.9% between 2025 and 2032.

The Asia-Pacific region continues to dominate due to the strong presence of key display panel manufacturers in countries such as China, South Korea, and Japan. Mass production of IPS panels for smartphones, televisions, and automotive applications in these countries has boosted regional demand. In contrast, North America is witnessing growing demand due to increased adoption of high-performance displays in gaming, automotive infotainment, and medical devices. U.S.-based tech giants and an expanding healthcare IT infrastructure are key contributors to this trend. Europe followed Asia-Pacific with a 28.4% share, driven by the automotive sector and rising industrial automation. South America and the Middle East & Africa, though smaller in share, are showing gradual uptake in consumer electronics and digital signage adoption.

Growing Demand for IPS Displays in Professional and Medical Applications

North America is witnessing a sharp rise in IPS display adoption across sectors such as professional content creation, medical imaging, and automotive dashboards. In 2024, the U.S. accounted for over 78% of the region’s total IPS display consumption, driven by demand from creative professionals and enterprise IT setups. Medical institutions are rapidly deploying IPS displays for diagnostics and surgical imaging due to their superior color accuracy and wide viewing angles. Additionally, gaming monitor sales surged by 31% across North America, with IPS panels becoming the standard in high-refresh rate displays. Canada’s smart healthcare and education reforms are also boosting demand for IPS-enabled systems in public services and infrastructure.

Automotive Integration and Industrial Digitization Fueling Demand

In Europe, the IPS Display Market is being heavily influenced by the automotive and industrial automation sectors. Germany, holding 35.6% of the regional market share, has seen widespread integration of IPS panels in next-gen infotainment systems, head-up displays, and instrument clusters. France and the U.K. are embracing digitization in healthcare and education sectors, further pushing IPS panel deployments. As smart factories and industrial control interfaces gain popularity, the demand for durable, high-clarity IPS displays continues to grow. Moreover, over 52% of new vehicles launched in 2024 in Western Europe featured IPS-based digital interfaces, reflecting the shift toward high-performance vehicle interiors.

Mass Production and Consumer Electronics Surge Boost Regional Leadership

Asia-Pacific maintained its leadership position in 2024, accounting for 39.2% of the global market, primarily due to high-volume production and consumption of IPS-based devices. China and South Korea together contributed over 60% of the region’s market share. Chinese panel manufacturers ramped up production capacity, reducing unit costs and boosting accessibility for consumer-grade displays. Meanwhile, South Korea’s leading role in high-end OLED-IPS hybrid technology fueled growth in premium smartphones and tablets. Japan contributed significantly to the healthcare and automotive segments, where IPS displays are used for precision imaging and dashboard displays. Regional demand is also rising in Southeast Asia due to the smartphone and gaming boom.

Consumer Electronics Growth and Educational Tech Adoption Lead Market Gains

South America is gradually emerging as a promising market for IPS displays, with Brazil accounting for 44.1% of the regional market share in 2024. The growing adoption of smart TVs, tablets, and smartphones with IPS panels is driving consumer electronics sales. Argentina and Chile are increasing investments in educational technology, where digital learning tools and IPS-based screens in classrooms are gaining popularity. The rise of eSports and content creation, especially among youth populations, is fostering demand for affordable IPS monitors. Despite infrastructure limitations, urban regions in South America are witnessing increased retail and B2B demand for commercial-grade IPS displays used in digital signage and retail kiosks.

Rising Investments in Healthcare and Smart Cities Support Market Expansion

The Middle East & Africa region is showcasing steady growth in the IPS Display Market, led by nations like the UAE and South Africa. The UAE contributed 33.8% of the region’s total demand in 2024, with heavy investments in healthcare technology and smart infrastructure development. IPS panels are becoming integral to hospital imaging systems, digital education, and AI-integrated traffic control rooms. South Africa is pushing digitization in public schools and medical centers, where IPS monitors are valued for their clarity and robustness. The increasing popularity of smart TVs and tablets in urban areas is also propelling regional sales. Corporate digital transformation projects across the GCC nations continue to favor IPS displays for conference and productivity tools.

China – 28.3%: Dominates due to large-scale IPS panel manufacturing and high domestic consumption in smartphones and TVs.

United States – 21.7%: Strong demand from gaming, healthcare, and professional sectors drives substantial market share.

The IPS Display Market remains highly competitive with a strong presence of global electronics and display technology giants. The market is dominated by companies that have vertically integrated manufacturing capabilities, allowing for better quality control and cost efficiency. As of 2024, South Korean and Chinese companies lead in production volume, with South Korea accounting for over 32% of global IPS panel output. Meanwhile, Chinese firms are rapidly increasing their market share by offering cost-effective displays for consumer electronics and industrial applications. Japanese manufacturers continue to maintain a strong foothold in high-end and professional-grade IPS displays, especially in healthcare and graphic design sectors. U.S.-based companies focus on innovation and premium displays for sectors like gaming, medical imaging, and creative media. Technological advancements in OLED-IPS hybrid technology, mini-LED backlighting, and ultra-thin form factors are key differentiators among competitors. Strategic collaborations, continuous R&D investments, and expanding production capacities are core strategies used to secure market leadership and broaden global distribution networks.

LG Display Co., Ltd.

BOE Technology Group Co., Ltd.

AU Optronics Corp.

Innolux Corporation

Japan Display Inc.

Sharp Corporation

ASUS

Dell Technologies Inc.

Acer Inc.

ViewSonic Corporation

The IPS Display Market is undergoing significant technological transformation as manufacturers integrate advanced innovations to enhance color accuracy, viewing angles, brightness uniformity, and response times. One of the most notable advancements is the fusion of IPS (In-Plane Switching) technology with mini-LED backlighting, which offers higher contrast ratios and deeper blacks while preserving IPS advantages like wide viewing angles and vibrant color reproduction. Major brands have started embedding quantum dot technology into IPS panels, achieving color gamuts exceeding 95% DCI-P3, making them suitable for creative professionals and gaming enthusiasts alike.

The proliferation of 4K and 8K IPS displays has increased, particularly in the consumer electronics and professional workstation sectors. Panels with high refresh rates of 120Hz, 144Hz, and even 240Hz are now mainstream in the gaming IPS display category. Technologies like Low Blue Light and Flicker-Free backlighting are being implemented to reduce eye strain and meet ergonomic standards, especially in office monitors.

Touchscreen IPS displays are becoming increasingly prevalent in laptops, industrial monitors, and medical equipment, often enhanced with anti-glare coatings and gorilla glass protection. Additionally, OLED-IPS hybrid displays are under research, aiming to combine the longevity and stability of IPS with OLED’s superior contrast. Manufacturers are also reducing panel thickness to sub-5mm levels to support ultra-thin and foldable devices.

• In March 2024, LG Display unveiled its new 27-inch IPS Black monitor aimed at the enterprise and creative professional segment. This panel offers enhanced contrast of 2000:1 compared to traditional IPS panels and supports true 10-bit color depth, improving accuracy for photo and video editing professionals.

• In September 2023, BOE Technology launched a new line of energy-efficient IPS displays with mini-LED backlighting designed for gaming laptops and monitors. These panels deliver peak brightness of up to 1,000 nits and a refresh rate of 165Hz, catering to the premium eSports display segment.

• In October 2023, ASUS introduced a ProArt Display PA32DC IPS OLED hybrid aimed at content creators. Though it features OLED technology, it uses IPS-based architecture for improved longevity, offering ΔE < 1 color accuracy and factory calibration for professional-grade applications.

• In February 2024, Acer announced its Nitro XV272U V IPS gaming monitor with Agile-Splendor IPS technology, designed to reduce response times to as low as 0.5 ms. The display supports HDR400 and AMD FreeSync Premium, enhancing the visual experience for high-performance gaming users.

The IPS Display Market Report provides comprehensive insights into the evolving landscape of in-plane switching (IPS) panel technologies, covering detailed analysis across display types, screen sizes, applications, and regional demand. IPS panels are known for their superior color accuracy, wide viewing angles, and consistent performance, making them widely adopted in smartphones, tablets, laptops, televisions, and professional monitors. As of 2024, the market is witnessing robust demand driven by rising consumer expectations for high-performance display technologies, especially in high-resolution and high-refresh rate segments.

The report segments the market based on panel size, including under 20 inches, 21–30 inches, and above 30 inches, with the 21–30 inches category dominating usage in consumer electronics. It also includes applications across gaming monitors, office displays, medical imaging equipment, and industrial devices. Gaming and professional-grade monitors account for a significant share due to the demand for precision and fluid display outputs.

Geographically, the study spans North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, evaluating regional trends and developments. The Asia-Pacific region, particularly China, South Korea, and Japan, is a hub for IPS panel manufacturing and innovation. The report also assesses the competitive landscape, covering new product launches, innovations in color calibration, mini-LED integration, and panel cost trends.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 57480 Million |

|

Market Revenue in 2032 |

USD 90993.94 Million |

|

CAGR (2025 - 2032) |

5.91% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

LG Display Co., Ltd., BOE Technology Group Co., Ltd., AU Optronics Corp., Innolux Corporation, Japan Display Inc., Sharp Corporation, ASUS, Dell Technologies Inc., Acer Inc., ViewSonic Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |