Reports

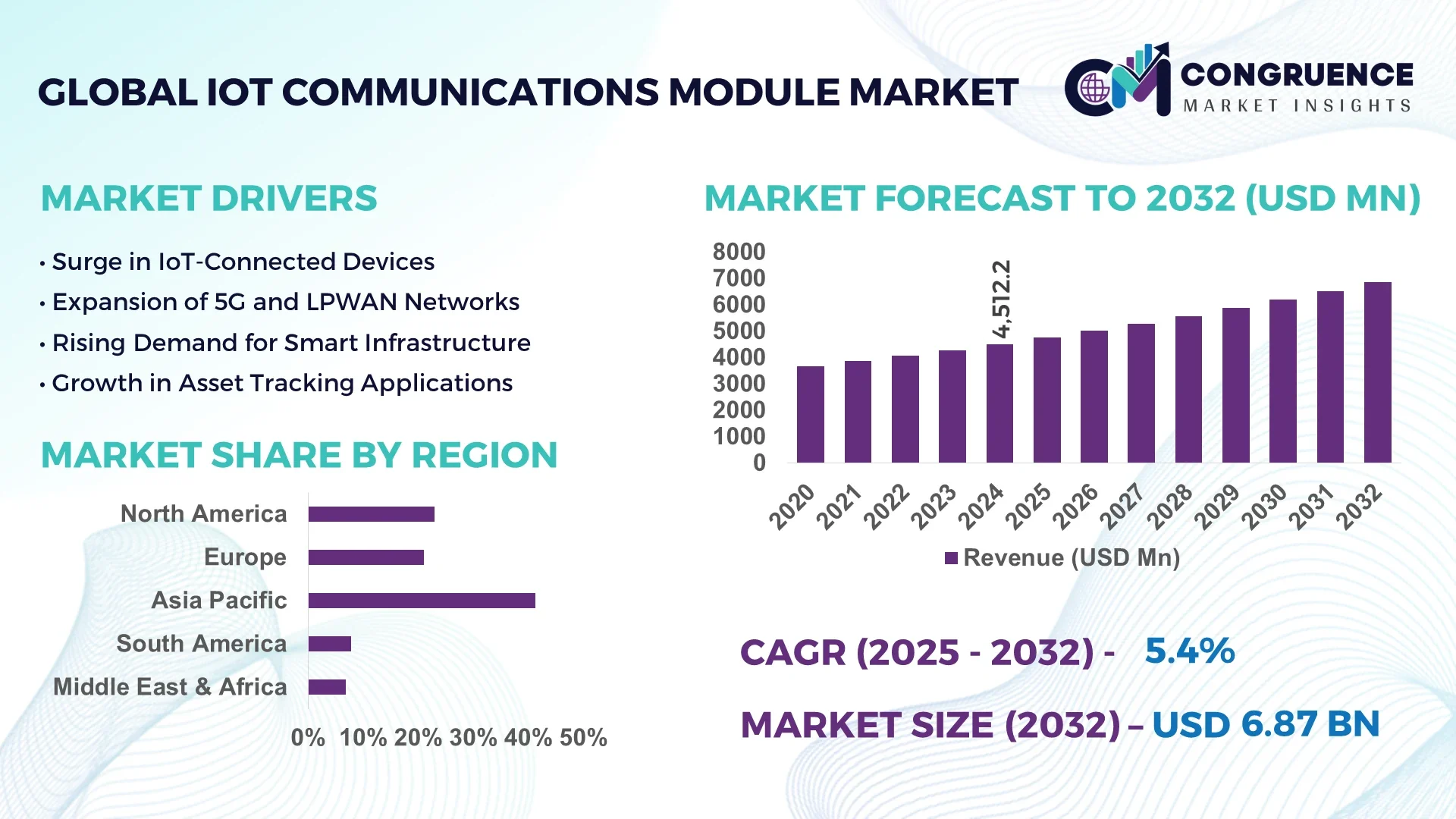

The Global IOT Communications Module Market was valued at USD 4512.17 Million in 2024 and is anticipated to reach a value of USD 6872.43 Million by 2032 expanding at a CAGR of 5.4% between 2025 and 2032.

In the United States, the market continues to see a surge in innovation, with over 80 high-capacity production plants dedicated to IOT communications modules. The country has witnessed over USD 1.2 billion in new investments since 2022, focusing on module integration in industrial automation, smart energy, and vehicle telematics, with robust R&D activities in 5G-compatible chipsets and low-power wide-area technologies.

The IOT Communications Module Market is witnessing dynamic shifts driven by the proliferation of smart devices and embedded systems across key industry verticals such as automotive, healthcare, utilities, and manufacturing. Industrial automation remains a leading sector, contributing over 28% to market demand, while the smart grid segment shows accelerated module adoption due to rising energy efficiency mandates. Recent innovations include ultra-compact modules with integrated GNSS, NB-IoT, and Cat-M1 support, offering improved signal stability and extended battery life. Regulatory frameworks supporting spectrum allocation and green compliance are catalyzing growth, particularly in Asia-Pacific and Europe. Regionally, North America continues to lead in early adoption of LTE-M modules, while Asia-Pacific countries, especially South Korea and Japan, are rapidly investing in 5G-based IoT networks. The evolving market landscape is shaped by edge computing integrations and AI-driven diagnostics, which are redefining performance expectations and application flexibility. Future developments are likely to be dominated by miniaturized, AI-enhanced modules built for real-time analytics and resilient machine-to-machine communication across low-latency environments.

Artificial Intelligence (AI) is revolutionizing the IOT Communications Module Market by driving efficiency, enabling predictive maintenance, and optimizing data transmission processes. AI-powered algorithms embedded into communication modules now allow devices to make autonomous decisions based on real-time data processing. These smart modules enhance adaptive communication protocols, reducing latency and improving data integrity in mission-critical applications such as industrial automation, precision agriculture, and connected mobility systems.

In industrial IoT environments, AI-integrated modules enable faster failure detection through real-time machine learning analytics, significantly lowering unplanned downtime. For example, smart factories employing AI-enabled modules have reported up to 40% improvement in operational uptime and 25% increase in data throughput efficiency. Additionally, AI helps compress and route massive volumes of sensor data more intelligently, optimizing bandwidth and reducing power consumption in battery-constrained IoT ecosystems.

In the IOT Communications Module Market, AI is also helping improve network reliability through intelligent channel switching and adaptive modulation techniques. These features are increasingly critical for modules deployed in fluctuating signal environments, such as underground infrastructure and remote industrial locations. As more organizations shift towards edge-based processing, AI-enhanced modules ensure localized decision-making capabilities, cutting dependence on cloud latency. This progression is setting the stage for hyper-efficient IoT ecosystems that support real-time command execution and seamless multi-device orchestration. With rising adoption of smart cities and autonomous systems, AI's integration in communication modules is becoming indispensable for scalable and resilient IOT infrastructures.

“In 2024, a leading Asian telecom firm successfully deployed AI-optimized NB-IoT modules across 5,000 urban water meters, achieving a 60% reduction in data transmission latency and a 30% extension in battery life per device, enhancing real-time leak detection capabilities.”

The expansion of smart manufacturing processes is a major driver propelling the IOT Communications Module Market forward. With Industry 4.0 initiatives accelerating globally, communication modules are playing a central role in enabling machine interconnectivity, predictive maintenance, and real-time production analytics. As of 2024, over 70% of leading manufacturing hubs in Europe and North America have incorporated IOT modules to support fully connected supply chains and automated equipment monitoring. These modules allow seamless data transmission between robotic systems and central processing units, thereby reducing machine downtime by up to 35% and boosting operational throughput. Enhanced interoperability, made possible by multi-band and multi-protocol modules, is critical for supporting diverse industrial applications across varied legacy systems. This strategic integration of smart communication technologies is enabling industries to meet production demands while maintaining agility and cost control.

One of the primary restraints impacting the IOT Communications Module Market is the limited compatibility of advanced modules with legacy infrastructure, particularly in developing economies and older industrial systems. Many factories and municipal systems still operate on outdated communication protocols that are incompatible with newer module technologies such as Cat-M1 or NB-IoT. As a result, full-scale adoption becomes cost-prohibitive due to the need for infrastructure overhaul. In 2024, nearly 40% of medium-sized enterprises in Latin America and Africa reported delays in IoT deployments owing to high integration costs and the lack of universal communication standards. This technological gap hinders the rapid scalability of IOT modules and restricts their widespread adoption, particularly in sectors like utilities and transport where infrastructure modernization is both complex and expensive. Incompatibility challenges also increase maintenance overheads and limit the operational lifespan of communication hardware.

The deployment of 5G infrastructure is opening new opportunities in the IOT Communications Module Market, particularly for use in smart cities and intelligent transportation systems. 5G's high-speed, low-latency network capabilities are ideal for communication modules that support real-time video surveillance, autonomous vehicle coordination, and responsive traffic management. As of early 2025, more than 100 smart city projects globally—including those in Seoul, Singapore, and Helsinki—have initiated 5G-based IOT deployments. These initiatives require compact modules with rapid data exchange capabilities and high energy efficiency, driving demand for next-generation chipsets. Additionally, environmental monitoring systems within these cities benefit from always-connected modules that can transmit critical air, noise, and waste data at higher frequencies with greater reliability. The scalability of 5G is unlocking module applications in newer domains, including public safety systems and connected street lighting, thereby providing a significant growth pathway for module developers and integrators.

Cybersecurity remains one of the most pressing challenges facing the IOT Communications Module Market. As billions of connected devices exchange sensitive operational and user data, communication modules become potential entry points for cyberattacks. In 2024 alone, there were over 1.5 billion cyber intrusion attempts globally targeting IoT-enabled infrastructures, particularly in sectors like healthcare, finance, and critical infrastructure. Many legacy modules lack built-in encryption or secure boot capabilities, making them vulnerable to data breaches and unauthorized access. Furthermore, firmware vulnerabilities in deployed modules often go unpatched due to lack of remote update capabilities, increasing long-term security risks. Enterprises are forced to invest heavily in threat detection and secure firmware development, inflating deployment costs and slowing adoption. Addressing this challenge requires a unified framework for secure module design, along with mandatory compliance standards for authentication, encryption, and over-the-air (OTA) updates.

Proliferation of Multi-Band Cellular Modules: Manufacturers are increasingly integrating multi-band support—such as LTE-M, NB-IoT, and 5G NR—into a single module to enhance compatibility across diverse geographic and regulatory landscapes. In 2024, more than 45% of newly launched modules featured dual or triple-band support, reducing the need for multiple product lines. This consolidation supports global logistics networks and enables OEMs to standardize device configurations, saving time and reducing operational costs in multinational deployments.

Edge AI Integration in Communication Modules: The integration of edge AI processing within IOT communications modules is enabling real-time data analysis and reducing reliance on cloud infrastructure. In logistics and smart grid applications, modules equipped with embedded AI processors have reduced latency by up to 70%, optimizing machine response times and lowering bandwidth usage. These intelligent modules are now being adopted in agriculture drones, predictive maintenance systems, and telemedicine devices for on-site analytics and decision-making.

Miniaturization and Energy Efficiency Gains: With the rise of wearables, portable sensors, and embedded medical devices, module miniaturization has become a design priority. In 2024, the average size of commercial IoT modules decreased by 18%, enabling seamless integration into compact systems. Simultaneously, innovations in low-power chipsets have improved energy efficiency, with some modules now offering over 10 years of battery life under LPWAN configurations.

Surge in Automotive Telematics Adoption: Connected vehicle ecosystems are driving up the demand for automotive-grade IOT communication modules. Advanced modules now support vehicle-to-everything (V2X) communication and over-the-air (OTA) software updates. By mid-2025, more than 60% of newly produced electric vehicles in Europe and China are expected to feature embedded IoT modules for navigation, diagnostics, and remote monitoring, pushing automotive integration to the forefront of the industry’s growth trajectory.

The IOT Communications Module market is segmented by type, application, and end-user, reflecting the broad scope of its deployment across industries. In terms of type, modules vary in terms of connectivity technologies—such as NB-IoT, LTE-M, 2G/3G, 4G, and emerging 5G modules—catering to different latency, coverage, and bandwidth needs. Applications range from smart metering and asset tracking to industrial automation and connected healthcare. End-users include automotive manufacturers, utility providers, smart city authorities, and logistics firms. Each segment has shown a measurable shift in adoption trends, with 5G-enabled modules gaining rapid traction and edge-intelligent solutions penetrating critical real-time industries. These segmentation dynamics underline the evolving technological requirements and diverse deployment environments across global markets.

Among various module types, 4G LTE modules currently dominate the IOT Communications Module market due to their balance between bandwidth capacity and broad network availability. These modules are widely adopted in smart meters, mobile healthcare devices, and logistics tracking solutions, offering reliable mid-tier connectivity for real-time data transmission. 5G-enabled modules represent the fastest-growing segment, driven by the increasing demand for ultra-low-latency applications in autonomous driving, industrial robotics, and remote healthcare. These modules enable real-time analytics, high-speed communication, and are well-suited for bandwidth-heavy operations in high-density urban environments. NB-IoT and LTE-M modules are also gaining traction, particularly in asset tracking and agriculture, due to their long battery life and cost-effective deployment in low-data-rate scenarios. Meanwhile, 2G/3G modules are still in use in certain developing regions but are steadily declining as global network upgrades continue. Hybrid modules that support multiple generations are increasingly favored for their flexibility in transitioning legacy systems to modern networks.

Smart metering remains the leading application within the IOT Communications Module market. These modules are essential for automated utility systems, allowing real-time monitoring of electricity, water, and gas consumption. Utilities across Europe and Asia-Pacific have rolled out millions of connected meters equipped with cellular IoT modules to streamline billing and grid performance. The fastest-growing application is industrial automation, especially in smart factories using predictive maintenance and real-time system monitoring. With over 45% of global manufacturers adopting automation tools embedded with IoT modules, this segment is rapidly expanding to enhance efficiency and reduce downtime. Connected healthcare and telemedicine applications are also growing, driven by the demand for continuous patient monitoring and remote diagnostics. Additionally, sectors such as environmental monitoring, agriculture, and smart homes are integrating communication modules for enhanced sensing, control, and analytics—though these remain niche in overall adoption but vital in specialized use cases.

The utilities sector is the leading end-user, as it extensively deploys IoT communications modules for smart grid and metering systems. These deployments enhance energy efficiency, monitor consumption patterns, and support government mandates for digital infrastructure modernization. In 2024 alone, over 60 million smart meters were upgraded globally using embedded communication modules. Automotive and transportation industries are the fastest-growing end-users, spurred by innovations in electric vehicles, autonomous systems, and V2X communications. Fleet operators and OEMs are leveraging real-time telematics modules to monitor vehicle health, navigation, and driver behavior. Healthcare providers, logistics firms, and agriculture companies also represent vital end-user segments. Hospitals are adopting wearable monitoring solutions with IoT modules, logistics firms are deploying asset tracking across global routes, and precision farming techniques rely on module-integrated sensors for soil and weather data. Together, these industries contribute significantly to the diversified demand structure of the IOT Communications Module market.

Asia-Pacific accounted for the largest market share at 41.3% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

The Asia-Pacific region continues to dominate the IOT Communications Module market due to the high consumption of smart devices, dense manufacturing ecosystems, and a thriving consumer electronics base. China, in particular, leads in module production, while Japan and South Korea remain technology pioneers in smart factory integrations and 5G-enabled communication systems. Strong governmental investment in industrial automation and widespread smart city initiatives further reinforce the region’s position.

Globally, the IOT Communications Module market is witnessing robust growth driven by rising connectivity requirements in automotive, energy, healthcare, and manufacturing sectors. Demand for modules with multi-mode connectivity, such as 5G, LTE-M, and NB-IoT, is accelerating. Regulatory reforms supporting smart infrastructure, along with sustainability goals, are propelling demand for efficient, low-power communication devices. Additionally, cloud-managed connectivity and device lifecycle management solutions are gaining momentum across enterprises. While legacy 2G/3G module demand declines, next-generation LPWAN and 5G modules are being rapidly adopted. The market is also benefiting from advances in edge computing, AI-enabled modules, and digital twin technology across multiple regions and industries.

Accelerated Industrial Digitalization Enhancing Demand

North America held a substantial 27.8% share in the global IOT Communications Module market in 2024, reflecting strong adoption across key industries including automotive, smart grid, and logistics. U.S.-based automotive OEMs and industrial IoT vendors are aggressively deploying high-performance modules for applications ranging from real-time tracking to connected infrastructure. The Infrastructure Investment and Jobs Act in the U.S. has spurred modernization across public systems, increasing demand for embedded communication modules in transportation and utility sectors. Additionally, widespread integration of edge-AI and cloud platforms is enhancing the performance of IoT networks. Canada’s smart city programs and investment in connected healthcare are further boosting module uptake across critical sectors.

Sustainability-Driven Innovation Fuels Technology Shift

Europe accounted for 18.5% of the IOT Communications Module market in 2024, with Germany, the UK, and France leading demand for connected technologies. The European Green Deal and mandates for energy-efficient infrastructure are accelerating the integration of smart modules into utility grids and building systems. Industrial automation across German manufacturing and digital transformation within the UK’s transportation network are further boosting deployment. Regulatory bodies like the European Telecommunications Standards Institute (ETSI) are encouraging uniformity in module specifications to support seamless 5G and LPWAN rollouts. Additionally, the EU’s increasing investment in IoT-enabled environmental monitoring systems is shaping demand across the region.

Massive Deployment Across Manufacturing and Smart Cities

With over 41.3% market share in 2024, Asia-Pacific stands as the largest regional contributor to the IOT Communications Module market. China remains the hub of global module manufacturing, benefiting from its extensive electronics supply chain and rapid urbanization. India and Southeast Asia are driving further demand through smart agriculture and nationwide connectivity programs. Japan’s leadership in robotics and embedded systems, combined with South Korea’s high-speed 5G infrastructure, provides an advanced environment for IoT adoption. Manufacturing automation, coupled with initiatives like China’s "New Infrastructure Plan" and India’s "Digital India" campaign, are accelerating the deployment of smart modules in utilities, logistics, and mobility platforms.

Infrastructure Expansion Creates Emerging Growth Pockets

In 2024, South America accounted for approximately 5.9% of the IOT Communications Module market, led by Brazil and Argentina. Brazil’s investments in smart utility metering and urban mobility solutions are primary drivers of module demand. The region is witnessing growing adoption in agriculture for crop monitoring and irrigation management through low-power IoT devices. Trade policies favoring tech imports and government-backed digitization programs have paved the way for expanded connectivity infrastructure. Additionally, Brazil’s electric vehicle segment and public health surveillance systems are starting to integrate communication modules to boost real-time analytics and operational transparency, especially in urban centers.

Smart Infrastructure Push and Digital Adoption on the Rise

The Middle East & Africa region held a 6.5% market share in the IOT Communications Module market in 2024, with the UAE and South Africa emerging as innovation centers. Demand is being shaped by smart city projects, oil and gas monitoring systems, and connected construction platforms. The UAE’s Vision 2031 and Smart Dubai initiatives emphasize full digital integration, creating new opportunities for advanced communication modules. South Africa is seeing increased demand in energy and logistics as utility firms implement IoT-enabled grids and fleets. The region is also witnessing partnerships for 5G deployment and LPWAN infrastructure expansion, supporting wider IoT adoption.

China – 29.7% market share

High production capacity combined with aggressive domestic consumption in industrial IoT and consumer electronics.

United States – 21.4% market share

Strong end-user demand from automotive, healthcare, and smart infrastructure sectors supported by rapid digital transformation.

The IOT Communications Module market is marked by intense competition, driven by rapid technological evolution and increasing integration of connectivity solutions across industrial and consumer sectors. Over 120 active global and regional competitors are operating in this space, each vying for a technological edge through enhanced module performance, miniaturization, energy efficiency, and multi-network compatibility. Companies are investing heavily in R&D to deliver advanced modules that support 5G, NB-IoT, LTE-M, and Wi-Fi 6, while maintaining cost-efficiency and scalability.

Strategic collaborations and joint ventures are shaping the competitive landscape. Several leading players have formed alliances with telecom providers, chipset manufacturers, and cloud service platforms to deliver vertically integrated solutions. Mergers and acquisitions continue to redefine market boundaries—allowing firms to expand their IP portfolios, enter new geographic markets, and improve time-to-market. Notable trends include the bundling of communication modules with edge AI processing units, and the growing focus on software-defined connectivity management. Manufacturers are also prioritizing regulatory compliance and global certification to streamline cross-border deployments, particularly in emerging economies. Competition remains especially fierce in Asia-Pacific and North America due to advanced manufacturing capabilities and high consumption of connected devices.

Quectel Wireless Solutions Co., Ltd.

Telit Cinterion (formerly Telit Communications PLC)

Sierra Wireless Inc.

u-blox Holding AG

Thales Group (IoT Division)

Fibocom Wireless Inc.

Sunsea AIoT Technology Co., Ltd.

Neoway Technology Co., Ltd.

MultiTech Systems, Inc.

Murata Manufacturing Co., Ltd.

Laird Connectivity

Semtech Corporation

Cavli Wireless

The IOT Communications Module market is experiencing rapid technological advancement driven by innovations in wireless connectivity, miniaturization, and energy efficiency. Current-generation modules are now equipped with multi-mode capabilities, supporting a mix of 5G, NB-IoT, LTE-M, LoRaWAN, and Wi-Fi 6E standards, enabling seamless global communication across diverse network infrastructures. These modules are becoming increasingly compact and power-efficient, making them ideal for integration into space-constrained or battery-powered applications, including wearables, asset trackers, and smart meters.

Emerging trends include the adoption of embedded SIM (eSIM) and integrated SIM (iSIM) technologies, which enhance security, remote provisioning, and network flexibility. As of 2024, over 60% of newly deployed industrial modules in Europe and Asia-Pacific support iSIM capabilities, reflecting their rising importance in secure device authentication and lifecycle management. Additionally, edge intelligence is being incorporated into communication modules, allowing for local data processing, anomaly detection, and latency reduction without relying solely on cloud infrastructure.

Furthermore, advancements in chipsets from major semiconductor vendors are enabling ultra-low-power designs with higher data throughput and enhanced interference resilience. Smart antenna systems and AI-enhanced signal processing have also emerged to improve module performance in challenging environments. With the growing need for global connectivity, modules now frequently offer integrated GNSS and multi-band support, reducing hardware complexity and improving application reliability across transportation, logistics, healthcare, and manufacturing sectors.

• In February 2024, Quectel launched the CC660D-LS, a compact 5G RedCap module that offers 150 Mbps download and 50 Mbps upload speeds. Designed for cost-sensitive industrial applications, it supports enhanced power savings and is optimized for large-scale deployments in smart metering and wearable devices.

• In November 2023, u-blox unveiled the NORA-W4 module, integrating Wi-Fi 6 and Bluetooth 5.3 in a single compact package. Targeted at industrial automation and connected healthcare, the module improves throughput and latency while ensuring backward compatibility for legacy systems.

• In March 2024, Fibocom introduced a new LTE Cat.1 bis module, MA510-GL, which provides expanded global band support, making it suitable for logistics and fleet tracking solutions. The module features advanced positioning with integrated GNSS and ultra-low power modes.

• In July 2023, Sierra Wireless enhanced its LPWA (Low Power Wide Area) product line by integrating cloud-native management features into its HL7810 module series. The update allows seamless deployment, monitoring, and remote firmware upgrades in large-scale IoT networks.

The IOT Communications Module Market Report offers a detailed and structured analysis of the global landscape, covering key dimensions including types, applications, technologies, and regional dynamics. It encompasses a wide range of communication module types such as cellular (5G, LTE-M, NB-IoT), LPWAN (LoRa, Sigfox), Wi-Fi, and Bluetooth modules, with a growing emphasis on hybrid and multi-mode solutions tailored for flexible deployments. The report evaluates both hardware innovations and embedded software developments that enable real-time connectivity, network efficiency, and seamless integration in IoT ecosystems. This report provides extensive insights into application areas including industrial automation, smart metering, healthcare monitoring, automotive telematics, logistics tracking, and consumer electronics. Each application is assessed based on demand trends, integration levels, and compatibility with emerging connectivity standards. Particular attention is given to end-user industries such as manufacturing, utilities, transportation, energy, and smart cities, where real-time data exchange and device interoperability are mission-critical.

Geographically, the report segments the market into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It evaluates regional infrastructure readiness, government incentives, and deployment maturity to determine market penetration and growth potential. The study also identifies emerging niches such as wearable IoT, eSIM-integrated modules, and AI-powered edge communication modules, which are gaining traction for specialized use cases. This comprehensive overview equips stakeholders with the insights required to evaluate competitive positioning, technological shifts, and regional opportunities, thereby supporting strategic planning and investment decisions in the IOT Communications Module ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4512.17 Million |

|

Market Revenue in 2032 |

USD 6872.43 Million |

|

CAGR (2025 - 2032) |

5.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

|

|

Customization & Pricing |

Available on Request (10% Customization is Free) |