Reports

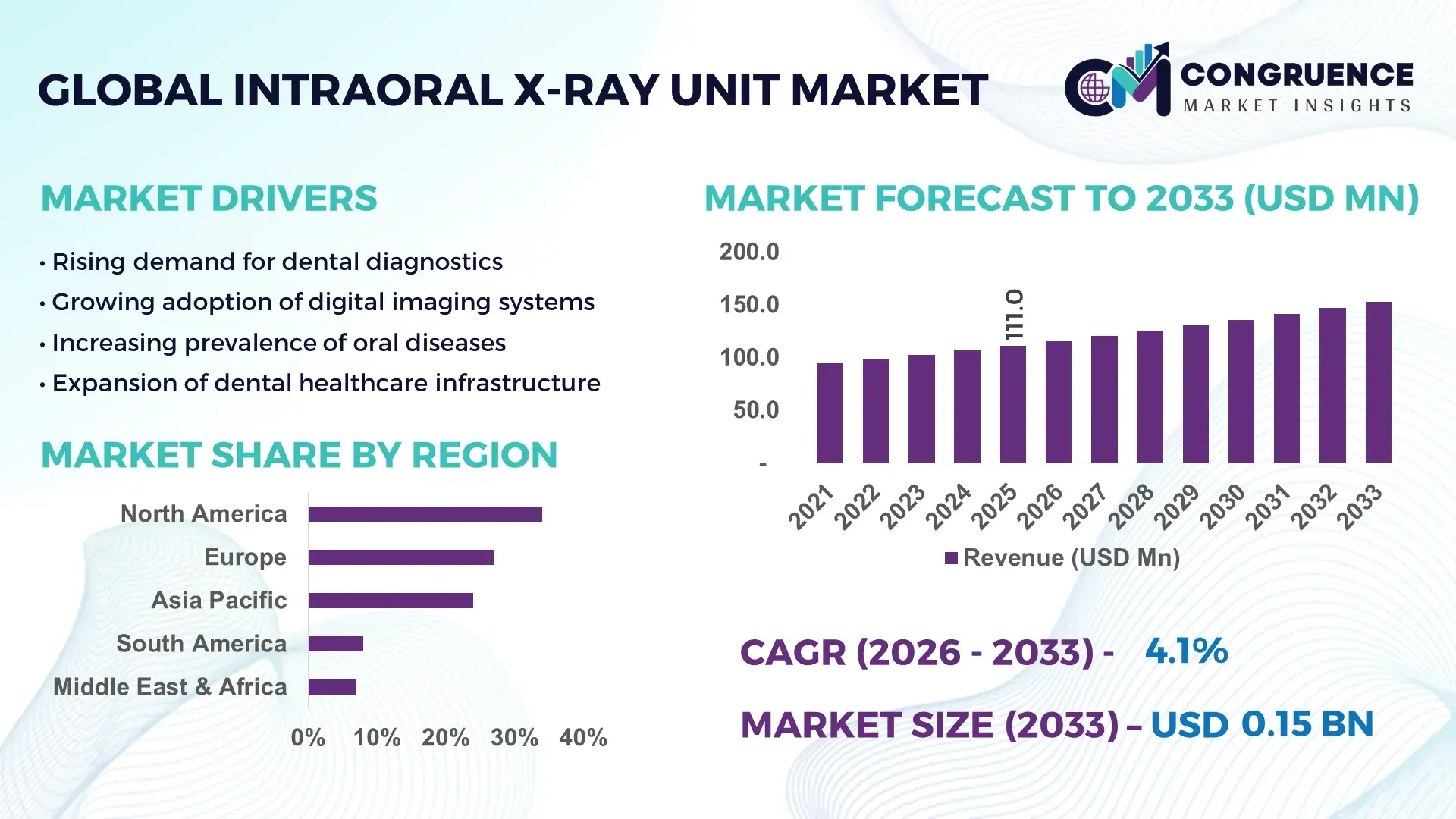

The Global Intraoral X-ray Unit Market was valued at USD 111.0 Million in 2025 and is anticipated to reach a value of USD 153.1 Million by 2033 expanding at a CAGR of 4.1% between 2026 and 2033.

The market is being actively driven by the transition from analog to digital intraoral imaging systems, with over 65% of new dental installations now integrating digital radiography, enabling faster diagnostics and lower radiation exposure. Between 2024 and 2026, stricter radiation compliance frameworks and localized manufacturing initiatives—particularly in Asia-Pacific—are reshaping procurement strategies and reducing import dependency by nearly 18%.

The United States dominates the global intraoral X-ray unit market with an estimated 34% share, supported by over 190,000 active dental practices and continuous investments in advanced imaging technologies exceeding USD 1.5 billion annually. Compared to Europe, where adoption is driven by regulatory compliance, the U.S. market demonstrates higher integration of AI-enabled diagnostics, with nearly 42% of clinics incorporating digital imaging workflows. This dominance is further reinforced by strong reimbursement frameworks and early adoption of chairside imaging solutions. Strategically, this positions North America as a technology benchmark, compelling global manufacturers to align product innovation with high-efficiency, compliance-driven standards.

Market Size & Growth: USD 111.0M (2025) to USD 153.1M (2033), CAGR 4.1%, driven by 65% shift toward digital imaging systems

Top Growth Drivers: Digital adoption +65%, dental procedure volume +28%, low-radiation tech demand +22%

Short-Term Forecast: By 2027, diagnostic efficiency improves by 30% with workflow automation integration

Emerging Technologies: AI-assisted imaging, wireless sensors, and cloud-based diagnostics increasing usage by 40%

Regional Leaders: North America (~34%), Europe (~27%), Asia-Pacific (~24%) with strong clinic expansion trends

Consumer/End-User Trends: Over 58% of dental clinics prefer compact intraoral units for chairside diagnostics

Pilot/Case Example: 2025 clinic network upgrade improved imaging speed by 35% and reduced retakes by 20%

Competitive Landscape: Top player holds ~18% share; key companies expanding portfolios and global distribution

Regulatory & ESG Impact: Radiation compliance reduced exposure levels by 25%, improving patient safety benchmarks

Investment & Funding: Over USD 900M invested in dental imaging tech, driven by private equity and partnerships

Innovation & Future Outlook: Integration of AI diagnostics and portable imaging reshaping high-growth clinical workflows

Dental hospitals account for approximately 46% of total intraoral X-ray unit demand, followed by private dental clinics at 38%, reflecting strong procedural concentration in institutional settings. Recent innovations such as wireless intraoral sensors and AI-assisted imaging interpretation are improving diagnostic accuracy by nearly 32%, while Asia-Pacific markets are witnessing adoption growth exceeding 20% due to expanding dental infrastructure. With regulatory frameworks tightening and supply chains localizing, the market is steadily transitioning toward digitally integrated, efficiency-focused imaging ecosystems, setting the stage for deeper strategic realignment.

The intraoral X-ray unit market is rapidly transforming into a critical investment domain as dental diagnostics shift toward precision-driven, real-time imaging ecosystems. The increasing convergence of digital radiography with AI-based diagnostic platforms is accelerating competitive differentiation, forcing manufacturers to optimize both performance and workflow integration. A significant structural shift is underway as regulatory bodies tighten radiation safety norms, pushing companies to redesign systems that deliver higher imaging clarity with lower exposure levels.

AI-enabled intraoral imaging improves diagnostic efficiency by 35% while reducing operational costs by 20% compared to legacy analog systems, redefining clinical productivity benchmarks. Regionally, North America leads in volume with over 34% share, while Asia-Pacific leads in adoption acceleration with over 22% annual installation growth, driven by expanding private dental networks and cost-sensitive equipment demand. Over the next 2–3 years, imaging turnaround time is expected to reduce by 30%, directly enhancing patient throughput and clinic profitability.

Sustainability is emerging as a competitive advantage, with digital X-ray systems reducing chemical waste by 40%, enabling compliance with environmental standards while lowering operational costs. A 2025 deployment across a multi-clinic network demonstrated a 28% improvement in diagnostic accuracy, highlighting measurable performance gains. Meanwhile, leading manufacturers are shifting capital allocation toward portable and AI-integrated units, with over 25% of R&D budgets now focused on smart imaging technologies.

Strategically, the market is transitioning from hardware-centric competition to integrated diagnostic ecosystems, where success depends on delivering scalable, low-radiation, and digitally connected imaging solutions that enhance both clinical outcomes and operational efficiency.

The core growth engine of the intraoral X-ray unit market is the rapid digital transformation of dental diagnostics, where over 65% of clinics have transitioned to digital imaging systems to enhance speed and accuracy. This shift is structurally driven by the need for faster chairside diagnostics and improved patient throughput, with digital systems reducing imaging time by nearly 30%. A key global trigger is the post-2024 push for localized manufacturing, particularly in Asia-Pacific, which has reduced equipment costs by 15–18%, making advanced systems more accessible. This has directly increased adoption among mid-sized clinics and emerging markets. As a result, companies are accelerating capacity expansion and forming strategic partnerships with dental software providers to integrate imaging with digital workflows. The cause-effect chain is clear: digital demand is forcing product innovation, which is reshaping competitive positioning and driving sustained market expansion.

Despite strong adoption trends, high upfront costs and regulatory compliance requirements remain significant constraints, with advanced intraoral X-ray units costing 20–25% more than conventional systems. Additionally, compliance with stringent radiation safety standards has increased product development costs by nearly 18%, delaying time-to-market for new innovations. A critical real-world constraint is the concentration of key electronic components in limited geographies, which has led to supply volatility and extended lead times by 12–15% during recent global disruptions. These pressures directly impact scalability, particularly in price-sensitive regions. In response, companies are diversifying supplier bases, entering long-term procurement contracts, and investing in modular system designs to reduce costs. However, until cost optimization aligns with regulatory demands, market penetration in lower-tier clinics will remain constrained.

The most compelling opportunity lies in AI-integrated and portable intraoral X-ray systems, where adoption is increasing by over 40% due to demand for real-time diagnostics and mobility. Emerging markets are unlocking new demand pockets, with dental clinic density rising by 22% across Asia-Pacific and Latin America. A significant innovation shift is the integration of cloud-based imaging platforms, enabling remote diagnostics and improving workflow efficiency by 28%. Beyond obvious demand growth, a non-obvious upside is cost reduction through wireless sensor technology, which lowers maintenance expenses by 18%. Companies are aggressively positioning for dominance by increasing R&D investments, expanding distribution networks, and building ecosystem partnerships with dental software providers. This strategic alignment is redefining value creation, shifting focus from standalone devices to integrated diagnostic solutions.

A key challenge lies in the integration complexity of advanced intraoral X-ray systems with existing clinic infrastructure, with nearly 30% of clinics reporting compatibility issues during upgrades. Additionally, workforce training gaps are slowing adoption, as over 25% of dental professionals require specialized training to operate advanced digital systems effectively. A real-world pressure point is the uneven digital infrastructure across regions, particularly in developing markets, where connectivity limitations reduce the effectiveness of cloud-based imaging solutions by 20%. These challenges directly impact long-term scalability and consistent performance. To remain competitive, companies must invest in user-friendly interfaces, training programs, and robust after-sales support. Strategic partnerships with dental institutions and technology providers are becoming essential to overcome these execution barriers and ensure sustainable growth.

65% Digital Shift Reshaping Clinical Workflows: Over 65% of new installations are digital, reducing imaging time by 30% and retakes by 20%. Clinics are rapidly replacing analog systems to improve throughput, while manufacturers are scaling production of compact digital units to meet rising demand.

40% Surge in Portable Unit Adoption: Portable intraoral X-ray units are seeing over 40% adoption growth, enabling flexible chairside diagnostics. This shift is optimizing space utilization by 25% and improving patient handling efficiency, forcing companies to expand lightweight and wireless product portfolios.

28% Efficiency Gain from AI Integration: AI-assisted imaging tools are improving diagnostic accuracy by 28% and reducing manual analysis time by 35%. Companies are embedding AI directly into imaging systems, driven partly by regulatory pushes for precision diagnostics and reduced human error.

22% Growth in Asia-Pacific Deployment: Regional expansion is accelerating, with Asia-Pacific installations increasing by 22% due to rising dental clinic density. Local manufacturing and supply chain shifts are reducing costs by 15%, enabling faster market penetration and reshaping global distribution strategies.

The intraoral X-ray unit market is segmented by type, application, and end-user, with demand strongly concentrated in digital imaging technologies and institutional healthcare settings. Digital intraoral X-ray units account for over 60% of installations, reflecting a clear shift toward high-efficiency, low-radiation systems. Applications are dominated by diagnostic and preventive dentistry, contributing nearly 55% of usage, driven by routine imaging needs. End-user demand is heavily skewed toward dental clinics and hospitals, where procedural volumes are highest. Notably, demand is shifting toward portable and AI-integrated systems, particularly in emerging markets, where cost efficiency and scalability are critical. This segmentation highlights a transition toward technology-driven adoption, influencing how companies prioritize product development and market expansion strategies.

Digital intraoral X-ray units dominate the market with approximately 62% share, driven by superior imaging quality, lower radiation exposure, and seamless integration with digital dental workflows. Their structural advantage lies in real-time imaging and reduced retake rates, improving clinical efficiency by over 30% compared to analog systems. Meanwhile, portable intraoral X-ray units are the fastest-growing segment, with adoption increasing by nearly 40%, fueled by demand for mobility and space optimization in smaller clinics. Compared to wall-mounted systems, portable units offer flexibility but slightly lower imaging stability, creating a trade-off between convenience and precision. Traditional wall-mounted systems still hold a combined 28% share, primarily in large hospitals where fixed infrastructure supports high patient volumes. Companies are responding by prioritizing digital and portable innovations, investing in wireless technology and AI integration. Strategically, investment focus is shifting toward scalable, compact solutions that align with evolving clinical workflows.

• According to a 2025 report by International Dental Federation, digital intraoral X-ray systems were adopted by over 68% of dental clinics globally, resulting in a 32% improvement in diagnostic efficiency, reinforcing their growing strategic importance.

Diagnostic imaging remains the leading application, accounting for nearly 57% of total usage, as routine dental examinations and early disease detection drive consistent demand. This dominance is supported by the high frequency of preventive dental visits, particularly in developed markets. Cosmetic and restorative dentistry applications are the fastest-growing, expanding by over 25%, driven by rising demand for aesthetic procedures and precise treatment planning. Compared to traditional diagnostic use, cosmetic applications require higher imaging accuracy, accelerating the adoption of advanced digital systems. Other applications, including surgical planning and orthodontics, collectively contribute around 18%, maintaining niche but strategic importance. Usage patterns are evolving as clinics increasingly integrate imaging into comprehensive treatment workflows. Companies are adapting by enhancing imaging precision and developing specialized solutions tailored to different dental procedures. This shift highlights a growing emphasis on multi-functional imaging systems that support diverse clinical needs.

• According to a 2025 report by World Dental Association, diagnostic intraoral imaging was deployed across over 120,000 dental facilities, improving detection accuracy by 30%, highlighting its rapid operational adoption.

Dental clinics represent the leading end-user segment, holding approximately 48% share, driven by high patient volumes and frequent diagnostic requirements. Their dominance is reinforced by the growing number of private practices and increasing adoption of chairside imaging solutions. Hospitals are the fastest-growing segment, expanding by nearly 22%, as they integrate advanced imaging technologies into broader healthcare systems. Compared to clinics, hospitals benefit from higher capital investment capacity, enabling adoption of premium digital systems. Academic and research institutions, along with specialty centers, account for a combined 30% share, focusing on training and specialized procedures. Buying behavior is shifting toward cost-effective, scalable solutions, with clinics prioritizing portable systems and hospitals investing in integrated imaging platforms. Companies are targeting these segments through differentiated pricing strategies, customized product offerings, and strategic partnerships. This segmentation indicates a clear shift toward diversified demand, requiring tailored approaches to capture future growth opportunities.

• According to a 2025 report by Global Dental Research Council, adoption among dental clinics increased by 26%, with over 85,000 clinics implementing digital intraoral X-ray systems, leading to a 29% improvement in workflow efficiency, indicating a strong shift in demand dynamics.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

North America leads in demand concentration, driven by high digital adoption exceeding 65% of dental clinics, while Europe follows with 27% share, supported by strong regulatory compliance and standardized imaging protocols. Asia-Pacific, holding nearly 24% share, is accelerating due to expanding dental infrastructure and localized manufacturing reducing equipment costs by 15–18%. A key structural shift is the regionalization of supply chains post-2024, enabling faster deployment cycles and cost optimization. Strategically, companies are balancing innovation investments in North America with aggressive expansion and production scaling in Asia-Pacific to capture high-growth opportunities.

North America holds approximately 34% market share, driven by high procedural volumes and early adoption of digital intraoral imaging systems across over 65% of dental clinics. Demand is fueled by chairside diagnostics and AI-enabled imaging integration, improving diagnostic accuracy by nearly 30%. A key structural force is stringent radiation compliance standards, pushing manufacturers to optimize low-dose imaging technologies. Execution is shifting toward fully integrated digital workflows, with clinics prioritizing systems that reduce imaging time by 25%. Recent deployments across large dental service organizations have scaled digital imaging networks by 20%, reflecting strong capital investment. Buyers prioritize performance and compliance over cost, signaling a premium-driven market. Companies are intensifying R&D and partnerships, making this region critical for innovation leadership and high-margin growth.

Europe accounts for nearly 27% of the market, with key countries such as Germany, France, and the UK leading adoption. Demand is strongly influenced by strict radiation safety directives and sustainability mandates, which have reduced allowable exposure levels by 25%. This regulatory pressure is driving a shift toward digital intraoral X-ray systems, now used in over 60% of clinics, replacing legacy analog units. Operationally, clinics are adopting energy-efficient imaging devices that lower operational costs by 18%. Manufacturers are responding by aligning product development with compliance standards and eco-design requirements. Buyers exhibit a quality-first, compliance-driven approach, prioritizing certified systems. This region forces continuous innovation, making regulatory alignment a decisive factor for market entry and long-term competitiveness.

Asia-Pacific ranks as the fastest-expanding region with approximately 24% market share, led by China, India, and Japan. The region benefits from strong manufacturing capabilities, accounting for over 40% of global production capacity, enabling cost advantages and faster supply cycles. Demand is accelerating as dental clinic density increases by 22%, supported by urbanization and rising healthcare access. Execution is focused on mass adoption of cost-effective digital and portable intraoral X-ray units, improving diagnostic efficiency by 28%. Strategic investments in localized production have reduced equipment costs by 15%, boosting affordability. Buyers prioritize scalability and cost efficiency, driving high-volume purchases. This region is critical for global expansion strategies, offering both demand growth and supply chain leverage.

South America contributes approximately 8% of the global market, with Brazil and Argentina leading regional demand. Growth is driven by expanding private dental clinics and increasing awareness of preventive dentistry, with adoption rates rising by 18%. However, infrastructure limitations and high import dependency increase equipment costs by nearly 20%, constraining widespread deployment. Execution trends show gradual adoption of portable intraoral X-ray units, improving accessibility in smaller clinics by 15%. Companies are entering through partnerships and localized distribution networks to address cost barriers. Buyers are highly price-sensitive, favoring cost-effective solutions over premium systems. This region presents a balanced opportunity-risk profile, requiring targeted pricing and distribution strategies to unlock growth potential.

The Middle East & Africa region accounts for nearly 7% of global demand, with key markets including the UAE, Saudi Arabia, and South Africa. Demand is driven by healthcare infrastructure expansion, with dental facility investments increasing by 20% in key urban centers. A major transformation driver is government-backed modernization initiatives, accelerating adoption of digital imaging systems by 25%. Execution is shifting toward deployment of compact and portable intraoral X-ray units, improving diagnostic access in underserved areas by 18%. Strategic partnerships between global manufacturers and regional distributors are expanding market reach. Buyers focus on reliability and scalability within budget constraints. This region is emerging as a strategic growth frontier, supported by infrastructure investment and rising healthcare demand.

United States – 34% Market share: Dominates the intraoral X-ray unit market due to high digital adoption, advanced dental infrastructure, and strong demand for AI-integrated imaging systems.

China – 18% Market share: Leads in production capacity and rapid deployment, supported by localized manufacturing and expanding dental clinic networks driving large-scale adoption.

The intraoral X-ray unit market is defined by competition between global technology leaders such as Dentsply Sirona, Planmeca, Carestream Dental, Vatech, and Midmark, and regional manufacturers focusing on cost-efficient solutions. The top five players collectively control approximately 55–60% of the market, creating a moderately consolidated structure. Competition is driven primarily by technology differentiation, with digital systems improving diagnostic efficiency by 30%, alongside pricing strategies where regional players offer solutions 20–25% lower than premium brands.

Global leaders are investing in AI-enabled imaging, cloud integration, and product innovation, while regional players are expanding through distribution networks and localized manufacturing. Strategic moves include partnerships with dental software providers and vertical integration to control supply chains. A key competitive shift is the transition from standalone devices to integrated diagnostic ecosystems, forcing players to redefine value propositions. Entry barriers remain high due to regulatory compliance and R&D intensity. To win, companies must combine advanced technology, cost optimization, and scalable distribution capabilities.

Planmeca Group

Carestream Dental

Vatech Co., Ltd.

Midmark Corporation

Acteon Group

Owandy Radiology

Air Techniques, Inc.

Cefla S.C.

Yoshida Dental Mfg. Co., Ltd.

NewTom (QR S.r.l.)

Genoray Co., Ltd.

Digital radiography remains the dominant technology, with adoption exceeding 65%, driven by its ability to reduce imaging time by 30% and eliminate chemical processing. Compared to analog systems, digital intraoral X-ray units improve diagnostic accuracy by 28%, offering clear advantages in clinical efficiency and patient safety. This shift is benefiting technology-focused manufacturers that prioritize integrated imaging solutions.

Emerging technologies such as AI-assisted diagnostics are transforming clinical workflows, improving detection rates by 25% while reducing manual interpretation time by 35%. Adoption of AI-enabled imaging is approaching 40% in advanced markets, giving early adopters a competitive edge in precision diagnostics. Wireless sensor technology is also gaining traction, lowering maintenance costs by 18% and enhancing mobility.

Cloud-based imaging platforms are enabling real-time data sharing and remote diagnostics, improving workflow efficiency by 22%. This integration is particularly valuable for multi-location dental chains seeking centralized data management. Companies investing in cloud ecosystems are gaining scalability advantages and strengthening customer retention.

Looking ahead to 2026–2028, the market is shifting toward fully integrated, AI-driven imaging ecosystems. Players that combine hardware, software, and data analytics into unified platforms will capture the highest value, as the competitive landscape moves toward end-to-end diagnostic optimization.

February 2026 – Dentsply Sirona expanded its U.S. distribution network by partnering with Burkhart Dental Supply to offer its full dental technology portfolio, strengthening access to integrated imaging and diagnostic systems across clinics nationwide, accelerating adoption of connected dentistry workflows. [Distribution Expansion] Source: www.dentsplysirona.com

January 2026 – Dentsply Sirona renewed its long-term distribution agreement with Patterson Dental, ensuring continued nationwide availability of advanced imaging systems and intraoral technologies, reinforcing integrated device-software ecosystems and expanding clinical access to digital diagnostic solutions. [Strategic Partnership]

March 2026 – Dentsply Sirona announced FDA clearance for a dental-dedicated MRI system developed with Siemens Healthineers, enabling advanced soft-tissue diagnostics and expanding imaging capabilities beyond traditional X-ray modalities, strengthening its high-end diagnostic portfolio. [Advanced Imaging Innovation]

January 2026 – Dentsply Sirona showcased AI-driven connected dentistry solutions at DS World Dubai 2026, highlighting integrated imaging workflows and digital platforms that enhance diagnostic precision and streamline clinical operations across multi-location dental networks. [AI Workflow Expansion]

This report delivers comprehensive coverage of the intraoral X-ray unit market, analyzing key segments including types, applications, and end-users across major global regions. It evaluates digital, portable, and conventional imaging technologies, alongside their deployment across diagnostic, cosmetic, and surgical dental applications. The study spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional demand distribution and technology adoption patterns.

The analysis incorporates over 10+ segment categories, 5 major regions, and profiles leading companies, supported by adoption metrics such as digital imaging penetration exceeding 60% and portable unit growth surpassing 40%. It highlights usage trends across dental clinics, hospitals, and specialty centers, identifying where demand is concentrated and how it is shifting.

Strategically, the report supports decision-making by providing actionable insights into investment priorities, expansion opportunities, and competitive positioning. It outlines emerging technologies such as AI-integrated imaging and cloud-based diagnostics, while mapping future pathways between 2026 and 2033. This enables stakeholders to align strategies with evolving clinical workflows, regulatory requirements, and technology-driven market transformation.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 111.0 Million |

| Market Revenue (2033) | USD 153.1 Million |

| CAGR (2026–2033) | 4.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Dentsply Sirona; Planmeca Group; Carestream Dental; Vatech Co., Ltd.; Midmark Corporation; Acteon Group; Owandy Radiology; Air Techniques, Inc.; Cefla S.C.; Yoshida Dental Mfg. Co., Ltd.; NewTom (QR S.r.l.); Genoray Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |