Reports

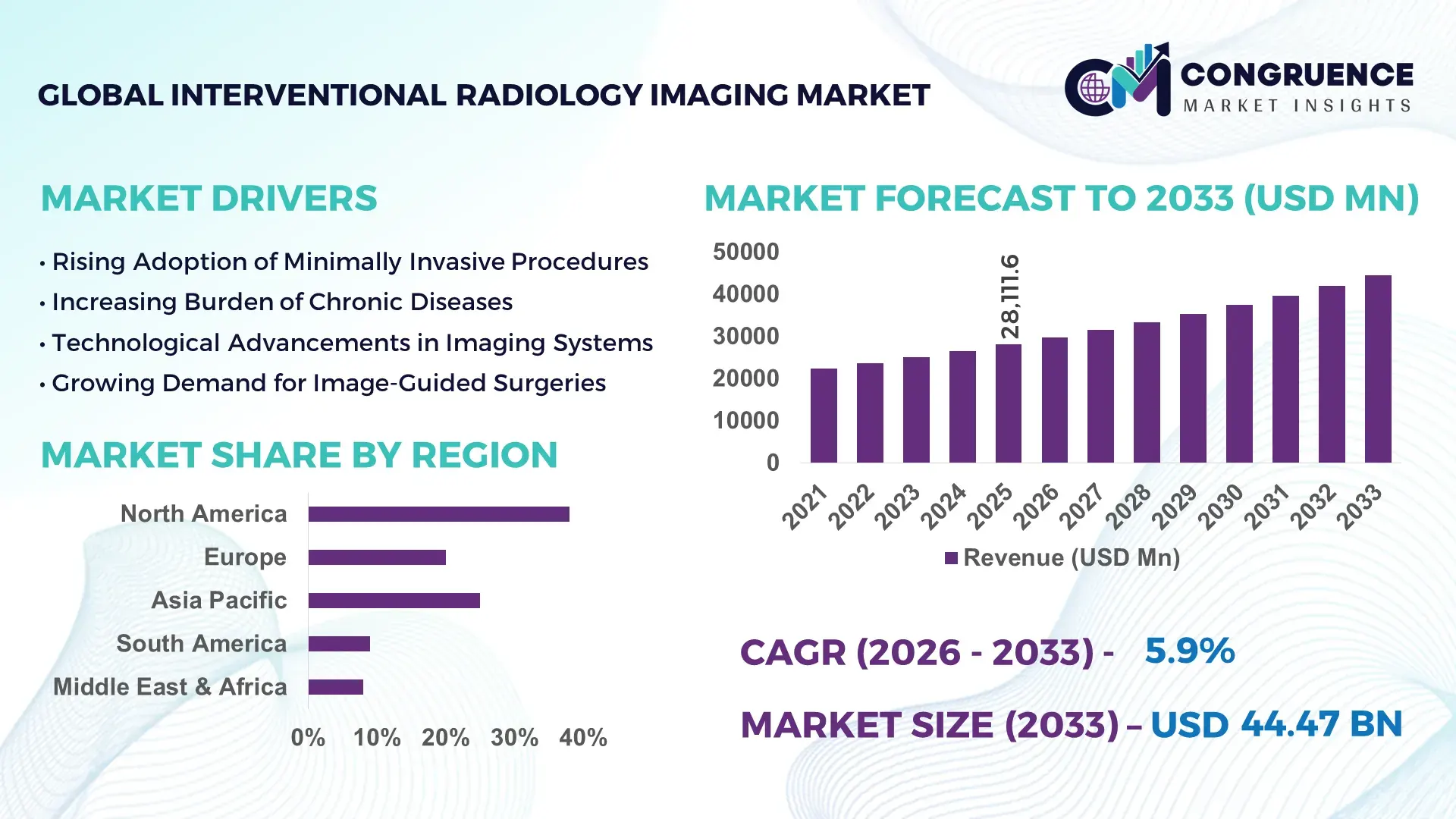

The Global Interventional Radiology Imaging Market was valued at USD 28111.63 Million in 2025 and is anticipated to reach a value of USD 44468.63 Million by 2033 expanding at a CAGR of 5.9% between 2026 and 2033. This growth is primarily driven by the increasing adoption of minimally invasive diagnostic and therapeutic procedures across global healthcare systems.

The United States continues to lead the interventional radiology imaging market with advanced healthcare infrastructure and substantial investments in imaging technologies. The country performs over 3 million interventional radiology procedures annually, supported by more than 1,200 specialized imaging centers equipped with advanced fluoroscopy and angiography systems. Investment in AI-powered imaging solutions has exceeded USD 2 billion annually, enhancing diagnostic precision and procedural efficiency. Interventional radiology is widely applied in oncology, cardiology, and neurology, with nearly 65% of hospitals integrating hybrid operating rooms that support real-time imaging-guided procedures. Additionally, over 70% of healthcare providers have adopted digital imaging platforms, ensuring seamless integration with electronic health records and improving workflow efficiency.

Market Size & Growth: USD 28111.63 Million in 2025 to USD 44468.63 Million by 2033 at 5.9% CAGR, driven by rising demand for minimally invasive procedures.

Top Growth Drivers: 45% increase in minimally invasive surgeries, 38% improvement in imaging accuracy, 32% rise in chronic disease prevalence.

Short-Term Forecast: By 2028, AI-assisted imaging is expected to improve diagnostic efficiency by 28% and reduce procedural time by 22%.

Emerging Technologies: AI-based image reconstruction, 3D imaging systems, and robotic-assisted interventional platforms.

Regional Leaders: North America projected at USD 16 Billion by 2033 with high adoption of hybrid ORs; Europe at USD 12 Billion with strong regulatory compliance; Asia-Pacific at USD 10 Billion driven by expanding healthcare infrastructure.

Consumer/End-User Trends: Hospitals account for over 60% usage, followed by ambulatory surgical centers adopting portable imaging solutions.

Pilot or Case Example: In 2024, a leading healthcare network improved procedural accuracy by 30% using AI-integrated angiography systems.

Competitive Landscape: Market leader holds approximately 22% share, followed by major competitors with strong portfolios in imaging systems and software.

Regulatory & ESG Impact: Regulatory bodies are mandating radiation dose reduction by up to 25% and promoting eco-friendly imaging equipment.

Investment & Funding Patterns: Over USD 5 Billion invested globally in imaging innovation, with increasing venture funding in AI-driven diagnostics.

Innovation & Future Outlook: Integration of cloud-based imaging platforms and real-time analytics is shaping next-generation interventional radiology workflows.

The interventional radiology imaging market is characterized by strong contributions from oncology, cardiology, and vascular surgery segments, collectively accounting for over 70% of procedural demand. Technological advancements such as AI-enabled imaging analytics and low-dose radiation systems are transforming clinical outcomes and patient safety standards. Regulatory frameworks are increasingly emphasizing radiation safety and digital integration, while economic drivers include rising healthcare expenditures and demand for cost-effective treatment alternatives. Regionally, Asia-Pacific is witnessing rapid growth due to infrastructure expansion and increasing patient awareness, while developed regions continue to focus on precision imaging and workflow automation. Emerging trends such as remote imaging diagnostics, robotic-assisted procedures, and integrated imaging platforms are expected to further enhance procedural efficiency and clinical accuracy.

The interventional radiology imaging market holds significant strategic importance as healthcare systems shift toward minimally invasive, cost-efficient treatment models. Advanced imaging technologies are central to improving clinical outcomes, reducing hospital stays, and enhancing procedural accuracy. AI-powered imaging systems deliver up to 35% improvement in diagnostic precision compared to conventional imaging standards, enabling faster and more reliable decision-making.

North America dominates in procedural volume due to its established healthcare infrastructure, while Asia-Pacific leads in adoption growth with over 40% of healthcare facilities integrating advanced imaging technologies. The increasing prevalence of chronic diseases, including cardiovascular disorders and cancer, is driving demand for real-time imaging solutions that support targeted interventions. By 2028, AI-driven imaging analytics is expected to reduce procedural complications by 25% and improve workflow efficiency by 30%, significantly enhancing operational performance in hospitals and diagnostic centers. Firms are committing to ESG goals, including reducing radiation exposure by 20% and adopting energy-efficient imaging systems by 2030.

In 2024, a European healthcare provider achieved a 27% reduction in procedure time through the implementation of robotic-assisted imaging systems integrated with real-time analytics. This demonstrates the measurable impact of advanced technologies on operational efficiency and patient outcomes. The future pathway of the interventional radiology imaging market lies in the integration of AI, robotics, and cloud-based platforms, positioning it as a critical pillar for healthcare resilience, regulatory compliance, and sustainable growth.

The growing preference for minimally invasive procedures is a primary driver of the interventional radiology imaging market. These procedures reduce hospital stays by up to 50% and lower complication rates by nearly 30%, making them highly attractive to both patients and healthcare providers. Interventional radiology techniques are increasingly used in oncology, cardiology, and neurology, with over 60% of cancer treatments now incorporating image-guided interventions. Advanced imaging systems enable real-time visualization, improving procedural accuracy by approximately 35%. Furthermore, the aging global population, with individuals aged 65 and above expected to exceed 1 billion by 2030, is contributing to higher demand for minimally invasive diagnostic and therapeutic solutions. Hospitals are investing heavily in hybrid operating rooms equipped with advanced imaging systems, further accelerating market growth.

High capital investment requirements for advanced imaging systems pose a significant restraint to market growth. The cost of installing a single interventional radiology imaging suite can exceed USD 1 million, including equipment, software integration, and facility modifications. Maintenance and operational costs add an additional 10–15% annually, creating financial challenges for smaller healthcare providers. Moreover, the need for specialized infrastructure such as radiation-shielded rooms and trained personnel further increases the overall investment burden. In developing regions, limited healthcare budgets and lack of reimbursement frameworks hinder the adoption of advanced imaging technologies. Additionally, the shortage of skilled interventional radiologists, estimated at a global deficit of over 20%, restricts the effective utilization of available imaging systems, further impacting market expansion.

Technological advancements present significant opportunities for the interventional radiology imaging market, particularly through the integration of AI, machine learning, and robotics. AI-based imaging solutions can reduce diagnostic errors by up to 40% and enhance image processing speed by 50%, enabling faster clinical decision-making. The development of portable and compact imaging systems is expanding access to interventional radiology in remote and underserved regions. Additionally, the adoption of cloud-based imaging platforms allows for real-time data sharing and remote diagnostics, improving collaboration among healthcare professionals. The increasing focus on personalized medicine is also driving demand for advanced imaging technologies that enable targeted treatment planning. Emerging markets, particularly in Asia-Pacific and Latin America, offer substantial growth potential due to rising healthcare investments and expanding patient populations.

Regulatory complexities and radiation safety concerns present significant challenges for the interventional radiology imaging market. Stringent regulations require compliance with safety standards that limit radiation exposure, often necessitating costly upgrades to existing equipment. Healthcare providers must adhere to guidelines that mandate dose reduction by up to 25%, requiring continuous investment in advanced imaging technologies. Additionally, obtaining regulatory approvals for new imaging systems can take several years, delaying product launches and innovation cycles. Concerns regarding cumulative radiation exposure among patients and healthcare workers have led to increased scrutiny and demand for safer imaging solutions. Training requirements for personnel to operate advanced systems further add to operational challenges, while compliance with data security and privacy regulations complicates the integration of digital imaging platforms.

• Accelerated Adoption of AI-Driven Imaging Analytics: AI-enabled interventional radiology imaging systems are witnessing rapid integration, with over 48% of hospitals globally deploying AI-assisted imaging workflows to enhance diagnostic accuracy. These systems improve lesion detection rates by nearly 35% and reduce image processing time by 40%, enabling faster decision-making in complex procedures. Additionally, AI-guided navigation tools have demonstrated a 28% reduction in procedural errors, significantly improving patient outcomes. The increasing availability of cloud-based AI platforms has further supported scalability, with adoption expected to exceed 60% across tertiary care centers within the next few years.

• Expansion of Hybrid Operating Rooms and Advanced Imaging Suites: The demand for hybrid operating rooms equipped with integrated imaging technologies has increased by 42% over the past five years. These facilities combine surgical and imaging capabilities, enabling real-time guidance during minimally invasive procedures. Approximately 65% of large hospitals in developed regions have already implemented hybrid ORs, leading to a 30% improvement in procedural efficiency and a 25% reduction in patient recovery time. The integration of multi-modality imaging systems such as CT, MRI, and fluoroscopy within a single environment is enhancing workflow optimization and clinical precision.

• Rising Demand for Low-Dose Radiation Imaging Technologies: Radiation safety has become a critical focus, with over 55% of healthcare providers adopting low-dose imaging systems to minimize patient exposure. Advanced imaging technologies now offer up to 50% reduction in radiation dose while maintaining high image quality. Regulatory mandates are pushing for stricter compliance, resulting in a 20% increase in investments toward safer imaging solutions. These systems are particularly crucial in pediatric and oncology applications, where repeated imaging procedures necessitate stringent dose control measures.

• Growth in Portable and Point-of-Care Imaging Solutions: Portable interventional radiology imaging systems are gaining traction, with adoption increasing by 37% in ambulatory and emergency care settings. These systems enable real-time imaging at the point of care, reducing patient transfer time by up to 45% and improving treatment response rates by 30%. Compact imaging devices equipped with wireless connectivity and battery-powered operations are expanding access to advanced imaging in remote and underserved areas. The trend is further supported by a 25% increase in outpatient procedures, driving demand for flexible and mobile imaging solutions.

The interventional radiology imaging market is segmented based on type, application, and end-user, each contributing uniquely to overall industry dynamics. Imaging modalities such as fluoroscopy, CT, MRI, and ultrasound form the core product categories, with varying adoption rates depending on procedural requirements and clinical settings. Applications span across oncology, cardiology, neurology, and vascular interventions, with oncology accounting for a substantial proportion of imaging-guided procedures due to increasing cancer prevalence. End-users include hospitals, ambulatory surgical centers, and specialized diagnostic clinics, with hospitals leading in adoption due to advanced infrastructure and higher patient volumes. Technological advancements, including AI integration and low-dose imaging systems, are influencing segmentation trends by enhancing precision and expanding application scope. Additionally, emerging markets are showing increased adoption across all segments, driven by healthcare infrastructure development and rising demand for minimally invasive treatments.

Interventional radiology imaging systems are categorized into fluoroscopy, computed tomography (CT), magnetic resonance imaging (MRI), ultrasound imaging, and others. Fluoroscopy-based systems currently dominate the market, accounting for approximately 40% of total adoption due to their real-time imaging capabilities and widespread use in vascular and cardiac procedures. CT imaging follows with around 28% adoption, offering high-resolution cross-sectional imaging essential for complex interventions. MRI-based systems, although representing nearly 15% of adoption, are gaining traction due to their superior soft tissue contrast and absence of ionizing radiation. Ultrasound imaging is the fastest-growing segment, expanding at an estimated CAGR of 7.8%, driven by its portability, cost-effectiveness, and increasing use in point-of-care applications. Other imaging modalities collectively contribute around 17% of the market, serving niche applications such as hybrid imaging and advanced diagnostic procedures.

The application landscape of the interventional radiology imaging market includes oncology, cardiology, neurology, vascular interventions, and others. Oncology leads the segment with approximately 38% share, driven by the increasing use of image-guided biopsies, tumor ablation, and targeted therapies. Cardiology accounts for nearly 27% of applications, with interventional imaging playing a crucial role in procedures such as angioplasty and stent placement. Neurology holds around 14%, supported by advancements in stroke management and neurovascular interventions. Vascular interventions represent the fastest-growing application segment, expanding at an estimated CAGR of 8.2%, fueled by the rising incidence of peripheral artery diseases and the growing adoption of minimally invasive treatment options. Other applications collectively contribute about 21%, addressing specialized procedures across multiple clinical domains.

The end-user segmentation of the interventional radiology imaging market includes hospitals, ambulatory surgical centers, diagnostic imaging centers, and others. Hospitals dominate the segment, accounting for approximately 62% of total adoption due to their comprehensive infrastructure, high patient inflow, and availability of advanced imaging technologies. Ambulatory surgical centers represent around 18%, benefiting from the growing preference for outpatient procedures and cost-effective treatment models. Diagnostic imaging centers contribute nearly 12%, focusing on specialized imaging services and diagnostic support. Ambulatory surgical centers are the fastest-growing end-user segment, expanding at an estimated CAGR of 7.5%, driven by the increasing shift toward minimally invasive outpatient procedures and reduced hospitalization costs. Other end-users collectively account for about 8%, including research institutions and specialty clinics.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America leads due to the presence of over 6,000 hospitals equipped with advanced imaging infrastructure and more than 70% adoption of hybrid operating rooms. Europe follows with approximately 27% share, supported by over 3,500 specialized diagnostic imaging centers and strong regulatory frameworks emphasizing radiation safety. Asia-Pacific holds nearly 24% share, with more than 40% of new hospital infrastructure projects incorporating interventional imaging systems. South America contributes around 6%, driven by expanding healthcare investments in Brazil and Argentina, while the Middle East & Africa region accounts for nearly 5%, supported by increasing modernization of healthcare facilities in the UAE and South Africa. Globally, more than 65% of interventional procedures are now guided by advanced imaging technologies, reflecting strong regional demand variations and infrastructure development.

How is advanced healthcare infrastructure accelerating imaging-guided interventions adoption?

North America holds approximately 38% of the global interventional radiology imaging market, supported by a highly developed healthcare ecosystem and strong adoption of advanced imaging technologies. The region performs over 3.5 million interventional procedures annually, with oncology and cardiology accounting for nearly 60% of total demand. Government initiatives promoting value-based care and reduced hospital stays have accelerated the adoption of minimally invasive imaging-guided treatments. Regulatory frameworks emphasize radiation dose reduction, leading to a 25% increase in the adoption of low-dose imaging systems. Technological advancements such as AI-integrated imaging platforms and robotic-assisted procedures are widely implemented, with over 55% of hospitals utilizing digital imaging solutions. A leading regional player has expanded its portfolio of AI-powered angiography systems, improving diagnostic precision by 30% and reducing procedure time by 20%. Consumer behavior reflects a preference for advanced, minimally invasive procedures, with over 68% of patients opting for outpatient imaging-guided treatments, highlighting strong demand for efficient and patient-centric healthcare solutions.

Why are stringent safety standards and digital innovation reshaping imaging adoption trends?

Europe accounts for approximately 27% of the interventional radiology imaging market, with key countries such as Germany, the United Kingdom, and France leading in adoption. The region operates over 3,000 specialized imaging centers and has achieved nearly 60% integration of digital imaging systems across healthcare facilities. Regulatory bodies have mandated radiation exposure reductions of up to 20%, driving the adoption of low-dose and high-precision imaging technologies. Sustainability initiatives are also influencing market dynamics, with healthcare providers targeting a 15% reduction in energy consumption through the use of energy-efficient imaging equipment. Emerging technologies such as AI-based diagnostic tools and 3D imaging systems are increasingly adopted, with nearly 45% of hospitals integrating these solutions. A prominent regional manufacturer has introduced advanced MRI-guided interventional systems, enhancing imaging accuracy by 28%. Consumer behavior in the region is shaped by strong regulatory oversight, leading to increased demand for transparent, safe, and explainable imaging solutions.

What factors are accelerating large-scale adoption of imaging technologies across healthcare systems?

Asia-Pacific represents approximately 24% of the global interventional radiology imaging market and is ranked as the fastest-growing region in terms of adoption and infrastructure expansion. Countries such as China, India, and Japan collectively account for over 65% of regional demand, supported by rapid urbanization and increasing healthcare investments. More than 2,500 new hospitals are under development, with over 45% integrating advanced imaging systems for interventional procedures. Manufacturing capabilities in the region are expanding, with local production of imaging equipment increasing by nearly 30%, reducing dependency on imports. Technological innovation hubs in countries like Japan and South Korea are driving advancements in AI-enabled imaging and robotic-assisted interventions, with adoption rates exceeding 40% in tertiary care centers. A regional player has launched portable imaging systems that have improved accessibility in rural areas by 35%. Consumer behavior is influenced by rising healthcare awareness and mobile-based diagnostic solutions, leading to a 50% increase in outpatient imaging procedures.

How are healthcare investments and policy reforms shaping imaging-driven care delivery?

South America holds approximately 6% of the global interventional radiology imaging market, with Brazil and Argentina being the primary contributors. The region has seen a 20% increase in healthcare infrastructure investments, resulting in the establishment of over 500 new diagnostic centers equipped with modern imaging technologies. Government incentives aimed at improving healthcare access have supported the adoption of interventional radiology procedures, particularly in urban areas. Trade policies facilitating the import of advanced medical equipment have contributed to a 15% rise in imaging system installations. A regional healthcare provider has implemented digital imaging platforms across its network, improving diagnostic efficiency by 25% and reducing patient wait times by 18%. Consumer behavior reflects growing demand for affordable and accessible healthcare services, with nearly 55% of patients preferring minimally invasive procedures due to shorter recovery periods and lower treatment costs.

What role do modernization initiatives and strategic partnerships play in advancing imaging capabilities?

The Middle East & Africa region accounts for approximately 5% of the global interventional radiology imaging market, with significant growth observed in countries such as the UAE and South Africa. Healthcare modernization initiatives have led to a 35% increase in the adoption of advanced imaging systems across major hospitals. Investments in healthcare infrastructure, particularly in the Gulf region, have resulted in the development of over 200 new medical facilities equipped with state-of-the-art imaging technologies. Technological trends include the integration of AI-driven diagnostic tools and cloud-based imaging platforms, with adoption rates reaching 30% in leading hospitals. Strategic trade partnerships have facilitated access to advanced imaging equipment, contributing to a 20% increase in system installations. A regional healthcare group has implemented integrated imaging solutions, improving procedural accuracy by 27%. Consumer behavior is characterized by increasing demand for high-quality healthcare services, with a 40% rise in patients seeking advanced imaging-guided treatments.

United States – 34% share in the Interventional Radiology Imaging market, driven by advanced healthcare infrastructure and high adoption of AI-integrated imaging technologies.

China – 18% share in the Interventional Radiology Imaging market, supported by large-scale healthcare infrastructure expansion and increasing domestic production of imaging systems.

The interventional radiology imaging market is moderately consolidated, with the top five companies accounting for approximately 55% of the global market share. Over 40 active competitors operate across various segments, including imaging equipment manufacturing, software development, and integrated healthcare solutions. Market leaders are focusing on innovation-driven strategies, with more than 60% of new product launches incorporating AI and machine learning capabilities to enhance imaging precision and workflow efficiency.

Strategic partnerships and collaborations have increased by nearly 35% over the past three years, enabling companies to expand their technological capabilities and geographic presence. Mergers and acquisitions remain a key growth strategy, with over 25 major deals recorded recently, aimed at strengthening product portfolios and accessing emerging markets. Companies are also investing heavily in research and development, with R&D spending accounting for nearly 12% of total operational budgets. The competitive landscape is characterized by rapid technological advancements, including the development of low-dose imaging systems and robotic-assisted interventional platforms. Additionally, companies are focusing on digital transformation, with over 50% of players offering cloud-based imaging solutions. The market environment remains highly dynamic, with continuous innovation and strategic initiatives shaping competitive positioning and long-term growth.

Siemens Healthineers

GE HealthCare

Philips Healthcare

Canon Medical Systems Corporation

Fujifilm Holdings Corporation

Hitachi Medical Systems

Carestream Health

Hologic Inc.

Shimadzu Corporation

Samsung Medison

Agfa-Gevaert Group

Esaote S.p.A.

Technological advancements are fundamentally transforming the interventional radiology imaging market, with a strong focus on precision, automation, and patient safety. Artificial intelligence integration has reached significant maturity, with over 50% of advanced imaging systems now incorporating AI-based image reconstruction and diagnostic support tools. These technologies enhance lesion detection accuracy by up to 35% and reduce image processing time by nearly 40%, enabling faster and more reliable clinical decisions. Machine learning algorithms are also being used for predictive analytics, assisting clinicians in identifying procedural risks and optimizing treatment pathways.

Robotic-assisted interventional systems are gaining momentum, with adoption increasing by approximately 30% across tertiary care hospitals. These systems improve procedural precision by nearly 25% and reduce operator fatigue, particularly in complex vascular and neurological interventions. In parallel, 3D and 4D imaging technologies are enabling real-time visualization of anatomical structures, improving navigation accuracy during minimally invasive procedures by over 20%. Low-dose radiation imaging technologies are another critical innovation, with new-generation systems achieving up to 50% reduction in radiation exposure while maintaining high-resolution imaging quality. This is particularly important in oncology and pediatric applications, where repeated imaging is required. Additionally, cloud-based imaging platforms are being adopted by nearly 45% of healthcare providers, allowing seamless data sharing, remote diagnostics, and integration with electronic health records.

Portable and point-of-care imaging devices are also expanding access to interventional radiology, with usage increasing by 35% in outpatient and emergency settings. These systems offer wireless connectivity and compact designs, enabling faster deployment and improved patient throughput. Collectively, these technological advancements are driving operational efficiency, enhancing clinical outcomes, and redefining the future of image-guided interventions.

• In March 2025, Siemens Healthineers announced enhancements to its ARTIS icono angiography platform, introducing AI-supported image optimization and advanced 3D imaging capabilities. The upgrade improved procedural visualization accuracy by over 30% and reduced radiation exposure during complex interventional procedures. Source: www.siemens-healthineers.com

• In January 2025, GE HealthCare launched an upgraded Allia IGS Pulse system with automated workflow integration and real-time imaging analytics. The system demonstrated a 25% reduction in procedure time and improved clinical efficiency in interventional cardiology and radiology applications. Source: www.gehealthcare.com

• In September 2024, Philips Healthcare expanded its Azurion image-guided therapy platform with enhanced cloud connectivity and AI-driven decision support tools. The upgrade enabled seamless data integration across hospital systems and improved interventional workflow efficiency by approximately 20%. Source: www.philips.com

• In November 2024, Canon Medical Systems introduced a next-generation Alphenix angiography system featuring advanced low-dose imaging technology and improved detector sensitivity. The system achieved up to 40% reduction in radiation dose while maintaining high image clarity for complex vascular procedures. Source: www.canonmedical.com

The Interventional Radiology Imaging Market Report provides a comprehensive analysis of key industry segments, technologies, and regional dynamics shaping the global market landscape. The report covers a wide range of imaging modalities, including fluoroscopy, computed tomography (CT), magnetic resonance imaging (MRI), and ultrasound systems, which collectively account for over 90% of interventional imaging procedures. It also examines emerging technologies such as AI-driven imaging analytics, robotic-assisted intervention systems, and cloud-based imaging platforms, which are increasingly influencing clinical workflows and operational efficiency.

From an application perspective, the report encompasses critical areas such as oncology, cardiology, neurology, and vascular interventions, with oncology and cardiology together contributing more than 60% of total imaging-guided procedures. The analysis further extends to end-user segments, including hospitals, ambulatory surgical centers, and diagnostic imaging facilities, where hospitals represent over 60% of total system adoption due to their advanced infrastructure and higher patient volumes. Geographically, the report provides detailed insights into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, collectively accounting for 100% of the global market distribution. It highlights regional variations in technology adoption, infrastructure development, and healthcare investment patterns, with over 65% of advanced imaging installations concentrated in developed regions.

Additionally, the report explores niche and emerging segments such as portable imaging systems and hybrid operating rooms, which have witnessed adoption increases of 30% and 40% respectively. It also addresses regulatory frameworks, safety standards, and environmental considerations influencing market growth. This structured analysis enables stakeholders to identify strategic opportunities, assess competitive positioning, and make informed investment decisions within the evolving interventional radiology imaging ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens Healthineers, GE HealthCare, Philips Healthcare, Canon Medical Systems Corporation, Fujifilm Holdings Corporation, Hitachi Medical Systems, Carestream Health, Hologic Inc., Shimadzu Corporation, Samsung Medison, Agfa-Gevaert Group, Esaote S.p.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |