Reports

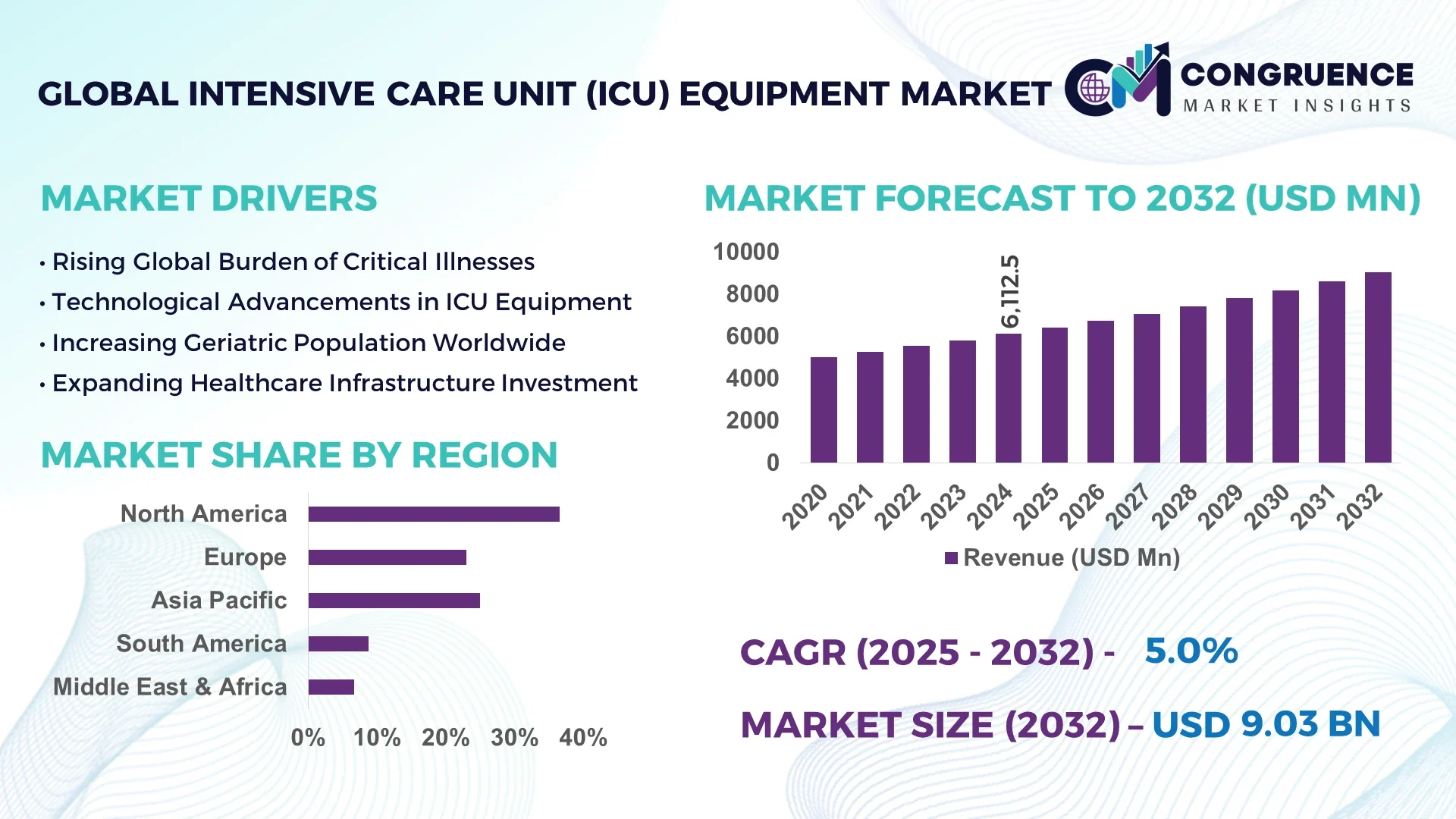

The Global Intensive Care Unit (ICU) Equipment Market was valued at USD 6112.47 Million in 2024 and is anticipated to reach a value of USD 9030.9 Million by 2032 expanding at a CAGR of 5.0% between 2025 and 2032.

The United States leads in ICU equipment manufacturing due to its robust production infrastructure, extensive hospital networks, and high investments in critical care technology, particularly in ventilator and patient monitoring systems.

The Intensive Care Unit (ICU) Equipment Market is undergoing a significant transformation driven by increasing demand for advanced life-support systems and real-time patient monitoring tools. The integration of next-generation technologies like IoT-enabled devices, high-resolution imaging systems, and precision diagnostics is revolutionizing critical care units globally. Key sectors influencing market growth include general ICUs, neonatal ICUs, and cardiac ICUs, with hospitals and specialty clinics being major end-users. Regulatory frameworks focused on patient safety and infection control are catalyzing innovation in ventilators, infusion pumps, and multi-parameter monitors. Economic factors such as increased healthcare spending and rising incidences of chronic diseases are pushing up equipment demand, especially in aging populations. Emerging economies across Asia-Pacific and Latin America are also witnessing rising adoption due to expanding hospital infrastructure and government-funded healthcare programs. Meanwhile, global supply chains are becoming more resilient, ensuring consistent availability of critical ICU equipment even in high-demand regions.

Artificial Intelligence is revolutionizing the Intensive Care Unit (ICU) Equipment Market by enabling intelligent automation, predictive analytics, and real-time clinical decision support across a wide range of critical care applications. AI-powered algorithms are being embedded into vital monitoring systems to continuously assess patient vitals, detect early signs of deterioration, and issue automated alerts—enhancing clinical accuracy and reducing human error. In ventilator systems, machine learning models adjust parameters in real-time based on dynamic patient responses, optimizing respiratory therapy and minimizing complications.

Within the Intensive Care Unit (ICU) Equipment Market, AI-driven data platforms are now capable of aggregating and analyzing large-scale patient datasets from multiple ICU devices. This allows healthcare professionals to derive actionable insights on patient trends, risk stratification, and treatment outcomes. Hospitals deploying AI-integrated ICU equipment report significant improvements in response times, workflow efficiency, and patient throughput. Additionally, AI models assist in infection control by predicting outbreak patterns and optimizing disinfection schedules for ICU environments.

AI also supports remote ICU operations, or “e-ICUs,” by enabling centralized teams to monitor and intervene in patient care across multiple sites, particularly in rural or understaffed areas. This advancement is especially vital in emerging markets, where resource allocation and skilled labor shortages challenge ICU performance. As demand for precision medicine rises, AI is becoming indispensable in enhancing the operational capabilities of intensive care systems, making the Intensive Care Unit (ICU) Equipment Market more adaptive and future-ready.

“In April 2024, a major U.S.-based medical device manufacturer integrated an AI module into its ICU ventilator line, enabling real-time respiratory pattern recognition and automated oxygen adjustment, which led to a 25% reduction in manual interventions and improved clinical outcomes in a multi-center hospital trial.”

The Intensive Care Unit (ICU) Equipment Market is evolving in response to the increasing prevalence of chronic diseases, aging global populations, and the expanding demand for high-quality critical care infrastructure. Healthcare systems worldwide are intensifying investments in advanced ICU devices such as ventilators, infusion pumps, and patient monitoring systems to enhance treatment outcomes and reduce mortality rates. This market is further influenced by the rise in surgical procedures, higher ICU admissions, and government mandates for equipping healthcare facilities with state-of-the-art critical care tools. Technological advancements, especially in wireless monitoring and AI integration, are reshaping ICU workflows and equipment capabilities. Simultaneously, market players are entering strategic collaborations and launching innovations aimed at improving accuracy, efficiency, and patient safety. However, the market’s dynamics are also shaped by cost pressures, procurement challenges, and regulatory compliance complexities in both developed and emerging regions.

The upward trend in chronic illnesses such as cardiovascular disease, diabetes, and respiratory disorders is significantly increasing ICU admissions globally. According to industry estimates, over 30% of ICU beds in the U.S. are routinely occupied by patients with comorbidities like chronic obstructive pulmonary disease (COPD) and heart failure. This scenario has amplified the demand for technologically sophisticated Intensive Care Unit (ICU) Equipment that enables continuous and accurate monitoring. The growing burden on healthcare systems is prompting hospitals to upgrade existing ICUs with multifunctional ventilators, automated infusion devices, and real-time monitoring systems. In high-density urban hospitals, smart ICU setups have become essential for handling patient surges and improving care efficiency. These developments are reinforcing long-term market growth as health systems prioritize critical care preparedness and resilience.

The procurement and ongoing maintenance of advanced Intensive Care Unit (ICU) Equipment present a substantial financial challenge for healthcare facilities, particularly in low- and middle-income countries. A single unit of a modern ICU ventilator or multifunctional monitor can cost tens of thousands of dollars, with additional expenses incurred for calibration, training, and routine servicing. Moreover, integrating such devices with hospital IT systems often requires infrastructure upgrades, raising total capital expenditures. These high costs lead many hospitals—especially in budget-constrained regions—to rely on outdated or refurbished equipment, limiting access to the latest innovations. As pricing pressure continues, market expansion in cost-sensitive territories may face delays unless scalable, affordable solutions are introduced.

The rapid adoption of tele-ICU and remote monitoring systems is creating promising new avenues for growth in the Intensive Care Unit (ICU) Equipment Market. Tele-ICUs enable centralized intensivist teams to remotely oversee and support local ICU operations, improving patient outcomes and reducing staffing burdens. In countries like India and Brazil, pilot tele-ICU programs have shown up to a 20% improvement in treatment turnaround times and enhanced mortality management. Equipment integrated with cloud connectivity, data-sharing features, and remote diagnostics are increasingly being adopted in both urban and rural healthcare settings. These developments provide a scalable solution to workforce shortages and uneven critical care access, particularly across geographically dispersed hospital networks. As digital transformation in healthcare accelerates, the demand for connected ICU devices is expected to remain on an upward trajectory.

One of the most significant challenges in the Intensive Care Unit (ICU) Equipment Market is the disparity in regulatory requirements across regions. Devices such as infusion pumps, patient monitors, and ventilators must undergo rigorous compliance assessments, which vary in scope and duration depending on the country. For instance, while the U.S. FDA emphasizes software validation and cybersecurity protocols, European regulators often prioritize environmental sustainability and material safety. These inconsistencies result in prolonged approval timelines, increased costs for multi-region compliance, and delayed product launches. Manufacturers must navigate a complex landscape of documentation, certifications, and audits, which can hinder innovation and restrict market entry, particularly for startups and SMEs. Addressing these challenges requires harmonization of standards and more efficient approval mechanisms.

• Rise in Modular and Prefabricated Construction: Modular and prefabricated hospital infrastructure is significantly altering the demand profile for ICU equipment, particularly in rapidly urbanizing regions. These pre-engineered ICUs demand compact, easily integrated, and mobile equipment solutions. In North America, hospitals are increasingly deploying modular ICUs to meet fluctuating patient loads. As a result, ICU ventilators and multi-parameter monitors designed for fast deployment and plug-and-play functionality are gaining traction. The efficiency of off-site fabrication is reducing build time by up to 50%, which directly influences procurement timelines and drives up demand for ready-to-use ICU systems.

• Growth of Smart and Wireless ICU Devices: Smart ICU equipment is becoming the new standard, especially in tertiary hospitals across the U.S., Japan, and South Korea. Devices like wireless ECG monitors, real-time telemetry systems, and Bluetooth-integrated infusion pumps are increasingly deployed to minimize wired clutter and enhance data accessibility. Hospitals report a 30% improvement in workflow efficiency when using wireless ICU systems, allowing for better coordination between care teams and faster response to critical alerts.

• Surge in AI-Based Clinical Decision Support Tools: Advanced ICU systems are now equipped with AI-based decision support modules that interpret patient data in real time. Hospitals adopting these systems experience fewer adverse events due to predictive analytics that guide medication dosing, ventilation parameters, and infection control strategies. In Germany, more than 150 hospitals have implemented AI-enhanced ICU monitors that help identify patient deterioration up to 6 hours in advance.

• Demand Shift Toward Pediatric and Neonatal ICU Equipment: Global health systems are witnessing a notable shift in ICU infrastructure investment toward pediatric and neonatal applications. Countries like India and Brazil are expanding NICU facilities in both public and private healthcare systems, leading to a sharp rise in demand for incubators, neonatal ventilators, and infant phototherapy equipment. In 2024, over 20,000 neonatal ICU units were added globally, with Asia-Pacific accounting for more than 40% of this growth.

The Intensive Care Unit (ICU) Equipment Market is segmented based on type, application, and end-user, each segment reflecting distinct trends driven by healthcare infrastructure modernization, demographic shifts, and medical advancements. The equipment types include ventilators, patient monitors, infusion pumps, and beds, among others, with ventilators holding strategic importance during respiratory emergencies. Applications span across general ICUs, neonatal ICUs, cardiac ICUs, and trauma ICUs, where neonatal and cardiac units are showing accelerated equipment uptake. End-user segmentation primarily includes hospitals, ambulatory surgical centers, and specialty clinics, with public hospitals representing the dominant category due to large-scale ICU expansions. Meanwhile, private healthcare institutions are rapidly adopting technologically advanced ICU equipment, fueling further diversification in procurement preferences across geographies.

Among ICU equipment types, ventilators dominate global utilization due to their central role in respiratory management, particularly in high-dependency and post-operative care units. These devices are crucial in treating patients with severe pulmonary conditions, driving consistent demand across hospitals and trauma centers. The fastest-growing type is patient monitoring systems, propelled by rising preferences for continuous real-time analytics, integration with hospital information systems, and wireless data transmission capabilities. These systems enhance response times and reduce adverse event occurrences. Infusion pumps remain essential in ICU drug administration and fluid management, offering high accuracy and programmable features for complex medication protocols. ICU beds with integrated sensors and ergonomic features are increasingly sought in smart ICU settings. Though niche, extracorporeal membrane oxygenation (ECMO) systems are gaining attention in advanced cardiac care units for critical life support, contributing to market diversification.

General ICUs represent the leading application area, serving a broad spectrum of critical care patients, including those with trauma, sepsis, or post-surgical complications. Their comprehensive usage drives consistent procurement of multi-functional equipment. The fastest-growing application segment is neonatal ICUs, with hospitals worldwide increasing investments in infant ventilators, incubators, and phototherapy systems due to rising preterm birth rates. Cardiac ICUs are also witnessing growth as cardiovascular diseases remain a leading cause of ICU admissions, necessitating specialized monitors and defibrillation units. Trauma ICUs are evolving in response to higher road accident-related injuries and emergency surgical procedures. Meanwhile, neurology-focused ICUs, though smaller in volume, require advanced imaging and neuro-monitoring systems, adding complexity and value to the overall market mix.

Hospitals remain the leading end-user of ICU equipment, particularly public hospitals in developed nations that benefit from government-funded critical care expansion. Large-scale procurement contracts and infrastructure development projects have made hospitals the primary consumer of advanced ICU solutions. The fastest-growing end-user segment is specialty clinics and multi-specialty centers, where focused care delivery and rising patient preference for private facilities are driving increased ICU setup investments. Ambulatory surgical centers are adopting ICU-grade equipment to manage immediate post-operative recovery for high-risk patients, enabling faster discharge cycles. Long-term acute care centers and home healthcare settings are also beginning to integrate portable ICU devices, especially in countries with aging populations and chronic care demands, contributing to new opportunities for equipment suppliers.

North America accounted for the largest market share at 36.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America's dominance in the Intensive Care Unit (ICU) Equipment Market is attributed to its advanced healthcare systems, robust ICU infrastructure, and continuous investment in AI-enabled monitoring devices and smart ventilators. Meanwhile, Asia-Pacific’s accelerating growth is fueled by healthcare infrastructure expansion across India, China, and Southeast Asia, along with increased government focus on affordable critical care accessibility.

Europe held a significant 27.4% share in 2024, driven by innovation-led ICU product launches and strict patient safety regulations. Asia-Pacific followed with 22.8%, led by rising demand for neonatal ICU solutions and domestic manufacturing surges in China. Latin America accounted for 7.1%, witnessing growth due to public hospital modernization efforts in Brazil. The Middle East & Africa captured a combined 6.2%, supported by investments in healthcare transformation in the UAE, Saudi Arabia, and South Africa. Regional trends reveal a shift toward AI-integrated ICU systems, mobile monitoring units, and cloud-based patient data management platforms. Growing cross-border collaborations, training programs, and funding support from global health institutions are accelerating ICU capacity building in emerging economies.

Adoption of Advanced ICU Technologies Supporting Market Leadership

The region secured a market share of 36.5% in 2024, reflecting sustained investments in critical care infrastructure and high per capita healthcare spending. Hospitals and tertiary care centers continue to drive demand for AI-powered ventilators, integrated monitoring systems, and next-generation infusion pumps. The healthcare sector, especially in the U.S. and Canada, is prioritizing digital transformation in ICU workflows. Regulatory frameworks, including rapid FDA approvals and CMS support for ICU telehealth programs, have created a favorable environment for technology adoption. Several hospitals have initiated full-scale upgrades to smart ICUs equipped with cloud-connected systems, voice-controlled functions, and predictive analytics tools. This shift is improving patient outcomes, clinician efficiency, and ICU resource utilization across both urban and rural medical institutions.

Regulatory-Driven Innovation Elevating Market Momentum

Holding 27.4% of the global market share in 2024, this region remains a powerhouse of medical device innovation, with Germany, France, and the UK leading in ICU equipment adoption. European Union policies promoting patient safety and data privacy, including MDR compliance, have stimulated the integration of certified smart monitoring devices across ICUs. Sustainability initiatives such as energy-efficient ventilators and recyclable device components are gaining traction. Digital twin technology and AI-backed ICU software are being piloted in several European hospitals to simulate and optimize patient care models. Increased R&D funding and public-private partnerships across the continent are accelerating the introduction of precision diagnostics, modular ICU units, and real-time alerting systems, further solidifying Europe's market position.

Infrastructure Expansion and Local Innovation Fuel Market Growth

With a market volume reaching 22.8% in 2024, the region stands out for rapid ICU infrastructure upgrades and widespread adoption of cost-effective critical care solutions. China, India, and Japan are leading demand generation through large-scale hospital expansions, health insurance coverage schemes, and rising awareness of intensive care standards. China’s surge in domestic manufacturing has increased supply of ventilators and portable ICU units, while India is scaling up neonatal ICU capacity in both public and private sectors. Japan’s focus on robotic ICU automation and elderly patient monitoring solutions further supports market advancement. Regional startups and med-tech hubs in Singapore and South Korea are actively innovating AI-integrated monitoring platforms and compact ICU workstations tailored for space-constrained hospitals.

Public Health Reforms and ICU Expansion Driving Demand

Brazil and Argentina are the key contributors in this region, which held a market share of 7.1% in 2024. Brazil’s National Health System (SUS) has allocated funding for ICU modernization across major urban centers, boosting demand for ventilators, defibrillators, and infusion pumps. Argentina is prioritizing neonatal ICU upgrades through partnerships with international health organizations. ICU device manufacturers are establishing regional warehouses and service centers to improve accessibility and reduce lead times. Trade liberalization policies and tariff exemptions for medical imports have further encouraged procurement of advanced ICU systems. The focus on building pandemic-resilient health infrastructure is pushing government agencies to adopt mobile ICU units and invest in scalable, modular care platforms.

Healthcare Digitalization Accelerating ICU Equipment Modernization

With a combined market share of 6.2% in 2024, this region is undergoing major ICU modernization, especially in the UAE, Saudi Arabia, and South Africa. Demand is driven by oil-funded infrastructure investment, rising chronic disease incidence, and growing emphasis on digital healthcare. The UAE is adopting AI-based ICU systems in its smart hospitals, while Saudi Arabia is investing in AI-integrated ventilators and predictive monitoring systems through Vision 2030 healthcare reforms. South Africa’s public sector is expanding ICU capacity through donor-backed funding and procurement programs. Regulatory frameworks are being restructured to fast-track medical device approvals and harmonize standards with global norms. Bilateral trade partnerships are also strengthening ICU equipment imports and support services.

United States – 31.2% market share

High production capacity, widespread adoption of AI-enabled ICU systems, and established critical care infrastructure contribute to dominance.

China – 15.6% market share

Rapid manufacturing scalability, expanding domestic hospital networks, and cost-efficient ICU equipment innovation fuel strong market position.

The Intensive Care Unit (ICU) Equipment market is characterized by a moderately consolidated competitive landscape, with more than 35 globally active manufacturers competing across key product segments such as ventilators, patient monitors, infusion pumps, and ICU beds. Leading players maintain strong brand portfolios and robust distribution networks, enabling them to supply both advanced and emerging healthcare markets. These companies frequently engage in strategic collaborations, technology licensing deals, and product line expansions to sustain market relevance.

In 2024, over 12 major product launches were recorded in the ICU segment, primarily focusing on AI integration, wireless connectivity, and automation enhancements. Several multinational manufacturers have invested in localized production facilities in Asia and Latin America to improve delivery timelines and reduce operational costs. Mergers and acquisitions are also shaping competition, with firms acquiring innovative startups specializing in remote monitoring and cloud-based ICU platforms.

Innovation-driven differentiation remains central, with companies racing to offer modular, mobile, and AI-optimized ICU solutions. Key competitive priorities include product scalability, regulatory compliance, and cybersecurity resilience. As hospitals and governments prioritize critical care readiness, competitors are intensifying efforts to develop predictive diagnostic tools and smart ICU ecosystems capable of integrating seamlessly with hospital information systems.

Drägerwerk AG & Co. KGaA

Medtronic plc

GE HealthCare Technologies Inc.

Nihon Kohden Corporation

Koninklijke Philips N.V.

Getinge AB

Skanray Technologies Ltd

BPL Medical Technologies

Hamilton Medical AG

Mindray Medical International Limited

The Intensive Care Unit (ICU) Equipment market is undergoing a significant transformation, driven by advancements in digital health technologies, real-time analytics, and next-generation device integration. One of the most impactful developments is the integration of artificial intelligence (AI) into patient monitoring systems. These AI-powered solutions enable predictive diagnostics, automated alerts, and real-time risk scoring, which enhances patient care precision and clinician response time. For instance, modern ICU monitors now feature embedded algorithms capable of analyzing heart rate variability and respiratory trends to predict sepsis or respiratory failure up to several hours in advance.

Tele-ICU systems are gaining traction, particularly in regions with limited access to specialized care. These platforms utilize high-definition cameras, secure data transmission, and remote analytics to allow intensivists to monitor and manage patients from centralized command centers. In 2024, more than 500 hospitals globally adopted tele-ICU frameworks to address staffing shortages and improve critical care accessibility.

Wireless and wearable ICU devices are also revolutionizing bedside care. Bluetooth-enabled infusion pumps and telemetry systems minimize wire clutter and improve patient mobility. Integration with hospital information systems (HIS) allows for synchronized data sharing across departments, enhancing overall workflow efficiency. Additionally, new ICU beds equipped with embedded sensors for pressure redistribution and patient movement detection are improving post-operative recovery outcomes. Sustainability-focused innovations, such as low-power consumption devices and recyclable components, are also gaining adoption, especially in Europe and North America.

• In February 2024, GE HealthCare launched its CARESCAPE ONE platform featuring an adaptive patient monitoring interface. The solution supports modular integration and provides real-time vital signs tracking with AI-based decision support for ICU professionals across multi-bed environments.

• In October 2023, Dräger introduced the Savina 300 NIV ventilator with upgraded turbine technology, enabling high-flow non-invasive ventilation with reduced noise levels. The model supports improved respiratory outcomes in both adult and pediatric intensive care settings.

• In May 2024, Mindray unveiled the BeneFusion i Series, a smart infusion pump system integrated with touchscreen controls and automated drug library management. The system is designed to enhance medication safety and streamline ICU workflow through cloud connectivity.

• In July 2023, Philips expanded its eICU portfolio with the IntelliVue X3 portable monitor, which enables seamless transition of critical monitoring data between departments. This lightweight device is optimized for emergency transfers and short-stay ICU units, improving data continuity and patient safety.

The Intensive Care Unit (ICU) Equipment Market Report offers a comprehensive evaluation of key segments, technologies, and regional dynamics shaping the global critical care landscape. It includes detailed analysis of essential product categories such as ventilators, infusion pumps, patient monitoring systems, defibrillators, ICU beds, and extracorporeal membrane oxygenation (ECMO) devices. Additionally, the report provides insight into specialized ICU setups, including neonatal ICUs, cardiac ICUs, and trauma ICUs, each exhibiting unique equipment demands.

Geographically, the report covers market activity across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with focus areas including technological adoption, infrastructure development, and regional policy influences. Emphasis is placed on rapidly developing healthcare ecosystems in Asia-Pacific and Latin America, where critical care capacity is expanding.

The report also explores emerging trends such as AI-based ICU solutions, tele-ICU integration, and modular ICU construction. It identifies growth opportunities in niche areas like wireless ICU systems, sensor-enabled beds, and remote monitoring devices. End-user segments such as hospitals, specialty clinics, and ambulatory surgical centers are evaluated for their procurement patterns and equipment adoption rates. This report equips stakeholders with strategic insights for product development, investment planning, and market entry initiatives within the high-impact ICU equipment domain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 6112.47 Million |

|

Market Revenue in 2032 |

USD 9030.9 Million |

|

CAGR (2025 - 2032) |

5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Drägerwerk AG & Co. KGaA, Medtronic plc, GE HealthCare Technologies Inc., Nihon Kohden Corporation, Koninklijke Philips N.V., Getinge AB, Skanray Technologies Ltd, BPL Medical Technologies, Hamilton Medical AG, Mindray Medical International Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |