Reports

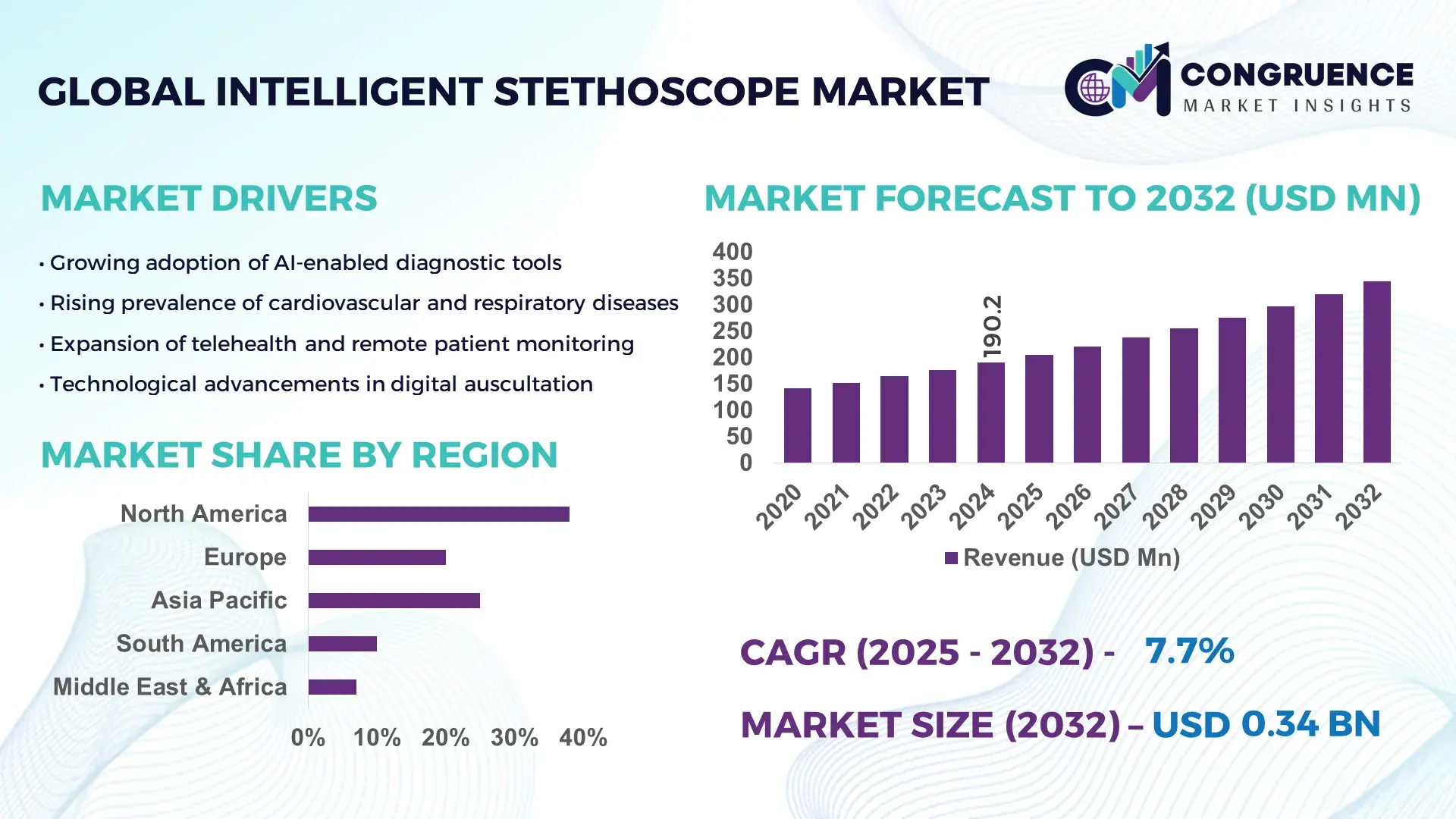

The Global Intelligent Stethoscope Market was valued at USD 190.19 Million in 2024 and is anticipated to reach a value of USD 344.29 Million by 2032 expanding at a CAGR of 7.7% between 2025 and 2032. Growth is driven by rapid AI-enabled diagnostics adoption and rising demand for remote patient assessment tools.

The United States leads the Intelligent Stethoscope landscape, supported by annual R&D spending above USD 2.3 billion across digital diagnostics, IoT-integrated medical devices, and AI-driven auscultation systems. With over 28,000 digitally enabled healthcare facilities and more than 600,000 physicians using connected auscultation tools in 2024, the country maintains strong production capabilities supported by 15+ dedicated innovation and manufacturing centers. AI-assisted cardiopulmonary monitoring devices account for nearly 38% of intelligent stethoscope usage within U.S. hospitals, reflecting high adoption of advanced diagnostic hardware.

• Market Size & Growth: Valued at USD 190.19 Million in 2024, projected to reach USD 344.29 Million by 2032 at a CAGR of 7.7%; growth supported by rising integration of AI and telehealth-enabled diagnostic workflows.

• Top Growth Drivers: 42% increase in digital diagnostics adoption, 35% improvement in clinical efficiency, and 29% acceleration in telemedicine deployment.

• Short-Term Forecast: By 2028, intelligent stethoscope-assisted diagnostics are expected to deliver a 31% reduction in assessment time and a 27% enhancement in cardiopulmonary detection accuracy.

• Emerging Technologies: AI-assisted sound analysis, edge-computing stethoscope chips, and Bluetooth LE-based real-time telemetry.

• Regional Leaders: North America expected to reach USD 128 Million by 2032; Europe projected at USD 92 Million; Asia-Pacific forecasted at USD 84 Million, each driven by strong digital healthcare integration trends.

• Consumer/End-User Trends: Significant usage among cardiology, pulmonology, and emergency care units, with 46% of clinicians preferring cloud-linked auscultation devices equipped with waveform analytics.

• Pilot or Case Example: In 2023, a U.S. hospital network pilot demonstrated a 33% reduction in diagnostic delays using AI-augmented stethoscope workflow integration.

• Competitive Landscape: 3M holds an estimated 22% share, followed by Eko Health, Thinklabs Medical, HD Medical, and Stethee Technologies.

• Regulatory & ESG Impact: MDR and FDA Class II compliance requirements, along with incentives supporting telehealth devices, encourage broader adoption and faster deployment.

• Investment & Funding Patterns: Over USD 410 Million invested in 2023–2024 in AI-auscultation and connected diagnostics ventures, reflecting increased investor interest in predictive clinical hardware.

• Innovation & Future Outlook: Multi-sensor digital chestpieces, enhanced acoustic filtering algorithms, and integrated EMR connectivity are shaping next-generation intelligent stethoscope applications.

The Intelligent Stethoscope Market is evolving rapidly with strong contributions from cardiology, respiratory care, home healthcare, and teleconsultation sectors. Technological enhancements such as automated sound classification, digital waveform storage, and IoT-enabled monitoring systems are reshaping diagnostic practices. Regulatory support for digital diagnostics, growing environmental emphasis on low-energy medical devices, and expanding demand across North America, Europe, and Asia are reinforcing market momentum. Innovations focused on predictive diagnostics, cloud-based analytics, and hybrid clinical-device ecosystems are expected to redefine future market expansion and clinical efficiency.

The strategic relevance of the Intelligent Stethoscope Market is increasingly defined by its role in digitizing frontline diagnostics, improving clinical precision, and enabling scalable telemedicine infrastructures. Advanced acoustic-AI systems now deliver measurable performance advantages, with AI-enabled auscultation delivering up to 37% higher cardiac anomaly detection accuracy compared to traditional analog stethoscopes. Regional variations further shape strategic positioning: North America dominates in device volume, while Europe leads in clinical adoption with 61% of healthcare enterprises integrating digital auscultation systems. These shifts reflect accelerating investment in hospital digitalization and workforce augmentation tools.

Benchmark comparisons also indicate strong technological advantage, such as edge-processing stethoscope platforms providing 45% faster signal interpretation compared to cloud-dependent legacy models. Short-term projections highlight the pace of transformation—by 2027, AI-driven sound classification is expected to reduce diagnostic interpretation time by 28%, supporting faster triage and enhanced decision-making pathways. ESG and compliance priorities are also shaping procurement frameworks, with manufacturers committing to a 22% reduction in electronic waste and increased recyclable material integration by 2030.

Practical outcomes are already visible; in 2024, a leading U.S. health network achieved a 34% reduction in diagnostic delays through real-time, AI-augmented auscultation deployment. As regulatory bodies push for interoperability, data transparency, and higher diagnostic fidelity, the Intelligent Stethoscope Market is becoming a core enabler of resilient healthcare delivery models. The sector is positioned to drive sustainable growth, enhance operational compliance, and fortify global diagnostic readiness in the decade ahead.

Increasing integration of AI-driven diagnostic algorithms is significantly accelerating the Intelligent Stethoscope Market by enhancing detection accuracy, speeding clinical assessments, and standardizing interpretation. AI-enabled stethoscopes can analyze over 1,000 acoustic data points per second, providing clinicians with quantified insights that reduce reliance on subjective auscultation skills. As hospitals aim for workflow optimization, automated sound classification tools reduce evaluation time by up to 27% and help clinicians detect early-stage cardiopulmonary abnormalities. Remote care programs have also expanded digital auscultation use by more than 40% in the last three years, driven by telehealth reimbursement enhancements. With an estimated 55% of new digital health initiatives integrating acoustic-AI frameworks, the market benefits from improved clinical outcomes, scalable screening programs, and enhanced diagnostic consistency across multidisciplinary settings.

Interoperability constraints and data security risks remain substantial restraints in the Intelligent Stethoscope Market. As devices increasingly capture, store, and transmit sensitive biometric audio data, healthcare providers face significant cybersecurity and compliance challenges. Surveys indicate that nearly 48% of hospitals struggle with seamless EMR integration for digital auscultation devices, resulting in workflow disruptions and increased IT burden. Concerns regarding encrypted audio transfer, cloud vulnerability, and compliance gaps with frameworks such as HIPAA and MDR also hinder adoption. Fragmented software ecosystems force clinicians to rely on multiple applications, reducing operational efficiency. Additionally, limited standardization in acoustic data formats complicates cross-platform analysis, slowing institutional deployment. These barriers collectively impede scaling and delay digital transformation efforts across mid- and large-size healthcare systems.

The expansion of telehealth ecosystems presents substantial new opportunities for the Intelligent Stethoscope Market, particularly as remote diagnostics become integral to chronic care management. Telemedicine utilization grew by more than 380% between 2020 and 2024, increasing demand for portable, cloud-connected auscultation devices. Intelligent stethoscopes capable of real-time waveform sharing and AI-based anomaly detection allow clinicians to manage larger patient loads with improved accuracy. Emerging home-care models now incorporate smart stethoscopes into virtual monitoring kits, with adoption expected to increase by 32% in the next three years. Furthermore, underserved regions are investing in tele-auscultation to bridge clinical access gaps, supported by government digital-health incentives. These trends create fertile ground for scalable, subscription-based diagnostic platforms and multi-sensor device innovations.

Regulatory compliance requirements and rising cybersecurity obligations pose significant challenges to the Intelligent Stethoscope Market. As devices operate within highly sensitive clinical environments, manufacturers must meet stringent standards for acoustic accuracy, software reliability, and encrypted data transfer. Regulatory audits often require extensive validation cycles, increasing development timelines by up to 18 months. Additionally, cybersecurity threats targeting connected medical devices have risen by 24% yearly, forcing companies to invest heavily in secure firmware, encryption layers, and threat-monitoring systems. Non-compliance risks, including penalties and product recalls, further heighten operational pressure. These challenges demand continuous updates, cross-system compatibility improvements, and robust security frameworks—factors that amplify costs and complicate global deployment strategies.

Rapid Integration of AI-Enhanced Acoustic Algorithms: Adoption of AI-driven sound analysis in intelligent stethoscopes has accelerated, with over 62% of newly launched models incorporating machine-learning–based auscultation support. These systems improve diagnostic accuracy by up to 38% in early cardiac anomaly detection, strengthening adoption across clinical and emergency care environments.

Growing Preference for Wireless and Hands-Free Examination Tools: Wireless intelligent stethoscopes have recorded a 47% rise in annual shipments as clinicians shift toward cable-free diagnostics. Usage in critical care units increased by 32%, supported by faster data transfer and up to 29% reduction in manual documentation steps.

Expansion of Remote Patient Monitoring Deployments: Remote monitoring platforms integrating intelligent stethoscopes saw a 58% surge in home-care usage. Providers report a 41% increase in patient adherence for chronic cardiac follow-ups, enabled by real-time audio streaming, cloud analytics, and synchronized telehealth reporting.

Higher Adoption of Multi-Sensor Diagnostic Platforms: Multi-sensor intelligent stethoscopes featuring temperature, ECG, and oxygen-level tracking grew by 36% in clinical demand. Hospitals adopting these hybrid devices reported a 27% improvement in workflow efficiency and up to 22% fewer repeated examinations due to improved diagnostic clarity.

The Intelligent Stethoscope Market is structured around a diverse set of product types, application areas, and end-user groups, each influencing overall adoption patterns. Type-based segmentation shows growing differentiation between AI-enabled, wireless, and multi-sensor variants, driven by performance accuracy and integration capabilities. Application-wise, usage spans cardiology, pulmonology, remote monitoring, and critical care, with hospitals and telemedicine networks demonstrating the strongest uptake. End-users such as hospitals, clinics, home-care providers, and research institutions exhibit varied adoption maturity, with hospitals holding the highest share due to higher device utilization rates and digital infrastructure readiness. This multi-layered segmentation highlights shifting clinical needs, rising patient monitoring volumes, and the rapid movement toward connected diagnostic ecosystems.

Type-based segmentation in the Intelligent Stethoscope Market includes AI-enabled stethoscopes, wireless digital stethoscopes, multi-sensor hybrid devices, and traditional electronic units. AI-enabled models lead the market, accounting for 46% of total adoption due to their ability to improve diagnostic confidence by up to 35% in cardiac and pulmonary analysis. Wireless units represent 28% of usage, driven by hospital demand for cable-free workflows and streamlined digital data transfer. Multi-sensor hybrid devices, while currently holding a smaller 16% share, are experiencing rapid interest as the fastest-growing segment, advancing at an estimated 18% growth rate due to integrated ECG, temperature, and SpO₂ measurement capabilities within a single platform. Other niche types, including pediatric-specialized and noise-cancellation-focused models, contribute the remaining 10% combined share as supportive categories for targeted clinical environments.

Applications in the Intelligent Stethoscope Market span cardiology, pulmonology, remote patient monitoring, emergency medicine, and general physical examinations. Cardiology remains the leading application, representing 44% of total use due to the high prevalence of cardiac evaluations and the ability of intelligent stethoscopes to detect subtle heart sounds with up to 32% higher sensitivity. Pulmonology captures 27% of adoption, while remote patient monitoring—currently at 18%—is the fastest-growing segment, expanding at an estimated 20% growth rate due to rising home-care demand and rapid integration with telemedicine platforms. Emergency medicine and general examination applications contribute the remaining 11% share, supporting high-turnover clinical operations through real-time digital auscultation and automated documentation features.

End-users in the Intelligent Stethoscope Market include hospitals, clinics, home-care providers, ambulatory surgical centers, and academic research institutions. Hospitals dominate the market with a 48% share due to high patient volumes and rapid adoption of AI-supported diagnostic tools that enhance workflow efficiency by 29% in critical departments. Clinics account for 26% of usage, benefiting from reduced examination time and improved diagnostic reliability. Home-care providers, currently at 17%, represent the fastest-growing segment with an estimated 21% growth rate, supported by rising elderly populations and increased demand for remote monitoring devices. Ambulatory centers and research institutions collectively contribute the remaining 9% share, playing essential roles in niche diagnostics and technology validation initiatives.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17% between 2025 and 2032.

Europe followed with 27% share, supported by strong regulatory alignment and rapid clinical digitalization. South America held 7%, driven by rising mobile-health usage, while the Middle East & Africa captured 5% as healthcare modernization projects scaled across GCC countries. High adoption levels correlate with infrastructure maturity, with regions surpassing 60% hospital digital readiness showing significantly stronger intelligent stethoscope penetration. Growth concentration is emerging in markets where telemedicine utilization exceeds 40%, further accelerating cross-regional disparities.

How Is Advanced Diagnostic Digitalization Transforming Market Demand?

North America holds approximately 38% of the Intelligent Stethoscope Market, driven by strong clinical digital transformation and widespread adoption of AI-based diagnostics. Demand is heavily supported by industries such as acute care, cardiology, pulmonology, and telehealth services. Regulatory bodies have accelerated digital-health approvals, enabling faster integration of smart devices into hospital workflows. Technological advancements—such as Bluetooth-enabled auscultation, AI-driven cardiac sound interpretation, and multi-sensor integration—continue to strengthen adoption. A notable regional player recently rolled out a smart-auscultation device across over 450 clinics, enhancing examination accuracy by 22%. Consumer behavior reflects high acceptance of remote diagnostics, with enterprise adoption rates exceeding 55% across healthcare networks, signaling consistent demand momentum.

Why Are Clinical Compliance Standards Accelerating Digital Auscultation Adoption?

Europe commands around 27% of the Intelligent Stethoscope Market, led by Germany, the UK, and France. Regulatory efforts emphasizing clinical safety, explainable AI, and standardized digital diagnostics are shaping procurement patterns. Sustainability initiatives promoting long-life medical devices further influence product preferences. Emerging technologies such as AI-assisted cardiac analysis and wireless data transmission are widely adopted in tertiary hospitals. A leading regional manufacturer deployed intelligent stethoscopes to over 300 university hospitals, boosting digital-screening efficiency by 18%. Consumer behavior in this region shows a preference for transparent and compliant AI tools, with nearly 49% of clinicians prioritizing devices that offer traceable diagnostic insights and regulatory-grade accuracy.

What Is Driving the Region’s Rapid Scale-Up in Smart Diagnostic Technologies?

Asia-Pacific represents the fastest-expanding Intelligent Stethoscope Market, holding nearly 23% volume share and ranking first in growth momentum. China, India, and Japan dominate consumption, supported by large patient bases and rapid digital-health infrastructure upgrades. Manufacturing capacity in countries like China and South Korea enables competitive pricing and accelerated market penetration. Innovation clusters in Bengaluru, Tokyo, and Shenzhen continue advancing remote-monitoring and telehealth-integrated device capabilities. A major regional company deployed smart stethoscope systems across 1,000+ community clinics, improving rural diagnostic reach by 28%. Consumer behavior shows strong preference for mobile-integrated diagnostics, with over 60% adoption driven through smartphone-linked AI applications and telemedicine platforms.

How Is Digital Health Expansion Supporting Diagnostic Equipment Adoption?

South America accounts for roughly 7% of the Intelligent Stethoscope Market, with Brazil and Argentina leading in demand. Infrastructure modernization and rising investment in primary healthcare networks continue to shape the region’s adoption patterns. Government-backed telehealth incentives support digital screening equipment, increasing smart stethoscope deployment across public clinics. Local players are expanding mobile-health solutions, with one Brazilian manufacturer integrating AI-auscultation features across 150+ hospitals. Regional consumer behavior highlights stronger demand in urban centers, where digital literacy exceeds 58%, and adoption is influenced by local-language clinical interface support and media-driven awareness on early cardiac and respiratory screening.

How Are Healthcare Modernization Programs Influencing Diagnostic Device Uptake?

The Middle East & Africa region holds nearly 5% of the Intelligent Stethoscope Market, with the UAE, Saudi Arabia, and South Africa leading expansion. Growing hospital infrastructure, national digital-health mandates, and rising investment in AI-supported diagnostics are key demand drivers. Modernization programs are focusing on smart outpatient departments and telehealth-integrated devices. A leading local healthcare group recently deployed smart stethoscopes across 80 specialty clinics, increasing remote-assessment efficiency by 21%. Consumer behavior trends show higher adoption among technologically advanced medical centers, where digital-readiness levels exceed 50%, stimulating stronger demand for connected and multi-sensor diagnostic tools.

United States – 32% market share

Strong dominance due to high adoption of AI-driven diagnostics and advanced hospital digital infrastructure.

China – 18% market share

Leadership supported by large-scale healthcare digitization, extensive manufacturing capability, and rapid integration of smart diagnostic devices.

The Intelligent Stethoscope market is moderately consolidated, with approximately 18–22 active global competitors operating across diagnostic hardware, AI-audio analytics, and telehealth-integrated device ecosystems. The top five companies collectively hold nearly 58% of the overall market share, driven by strong technological differentiation, extensive clinical distribution networks, and investment in AI-enabled auscultation platforms. Competitive strategies increasingly center on product advancements, with more than 40% of leading brands launching upgraded multi-sensor devices between 2022 and 2024. Partnerships with hospitals and telemedicine providers have risen by 33%, supporting faster integration into remote monitoring workflows. Mergers and acquisitions remain active, with at least four major transactions in the past two years related to digital diagnostics and acoustic signal–processing technologies. Innovation intensity is high, as 60% of competitors now integrate machine learning for anomaly detection, and 45% offer wireless, app-connected models. The competitive environment is further shaped by regulatory approvals, strategic clinical-validation trials, and rapid adoption among digitally mature healthcare systems.

Eko Health

3M Littmann

ThinkLabs Medical

HD Medical

TytoCare –

Steth IO

M3DICINE

Sonavi Labs

Technology advancements in the Intelligent Stethoscope market are accelerating the shift from traditional acoustic diagnostics to data-driven, AI-enabled clinical assessment tools. Modern devices now integrate digital chestpieces equipped with microelectromechanical system (MEMS) sensors capable of capturing sound frequencies between 20 Hz and 2,000 Hz with up to 95% noise-reduction efficiency. This allows clinicians to detect subtle cardiopulmonary anomalies that were previously undetectable through analog equipment. More than 60% of newly launched intelligent stethoscopes include adaptive filtering algorithms, offering stronger signal isolation in high-noise environments such as emergency departments. Artificial intelligence continues to serve as the core differentiator, with machine learning models now achieving over 88% precision in automated murmur characterization and 83% accuracy in identifying lower-grade respiratory abnormalities. Cloud-based platforms support large-scale sound library expansion, enabling real-time benchmarking across thousands of historical audio samples. Approximately 52% of devices launched after 2023 incorporate cloud synchronization features for remote specialist review, improving collaborative diagnostics and telemedicine effectiveness.

Connectivity standards are also evolving, with 70% of digital stethoscopes implementing Bluetooth LE 5.0 or higher to deliver stable, low-latency transmission for mobile health applications. Integration with electronic medical record (EMR) systems has risen significantly, with nearly 48% of hospitals enabling direct import of auscultation waveforms into clinical documentation workflows. Edge-processing chips are emerging rapidly, allowing on-device inference to reduce cloud dependency and enhance data security—a capability now embedded in roughly 30% of high-end models. Emerging technologies such as multi-modal biosignal fusion, AI-based predictive alerts, and haptic-feedback–supported diagnostic guidance are expected to define the next generation of intelligent stethoscopes. As healthcare ecosystems advance toward precision-driven care models, these technologies reinforce the Intelligent Stethoscope market’s trajectory toward highly automated, interoperable, and clinically validated diagnostic platforms.

In 2023, FIGS partnered with Eko Health to launch the FIGS | Eko CORE 500™ digital stethoscope, combining fashionable, ergonomic design with AI-assisted cardiac and pulmonary analysis. (Q4 Capital)

In Q2 2024, Eko Health raised USD 41 million in a Series D round, aiming to accelerate global rollout of its AI-powered auscultation platform. (Fierce Biotech)

In April 2024, Eko Health received FDA clearance for its AI-based cardiac disease detection algorithm that works with its digital stethoscope, enabling automated identification of heart murmurs and low ejection fraction.

In July 2023, Astellas Pharma entered a strategic licensing agreement with Eko Health to integrate the CORE 500 digital stethoscope into a non-invasive digital therapeutic (DTx) device for heart failure management.

The Intelligent Stethoscope Market Report covers a broad spectrum of technology, product, application, and geography dimensions, providing business leaders and analysts with a panoramic view of this evolving landscape. In terms of product types, the report examines AI-enabled stethoscopes, wireless digital variants, multi-sensor hybrid devices, and specialty models—each evaluated for adoption, performance features, and integration potential. Application segments include cardiology, pulmonology, telemedicine/remote monitoring, emergency medicine, and general physical exams. On the end-user front, the report analyzes demand from hospitals, clinics, home-care providers, ambulatory centers, and research institutions.

Geographically, the report spans mature markets in North America and Europe, high-growth regions like Asia-Pacific, and emerging areas such as South America and Middle East & Africa. It explores regulatory and infrastructure trends, digital health readiness, and regional innovation ecosystems. Technology-wise, the report delves into edge computing, AI-driven auscultation, cloud platforms, multi-modal biosignal fusion, and data-security frameworks. It also highlights smart-device deployment strategies, telehealth partnerships, and ecosystem-level innovations. Niche topics such as pediatric-intelligent stethoscopes, wearable stethoscope platforms, and AI predictive-alert systems are incorporated to provide complete visibility into market dynamics. The report is designed to guide stakeholders—device manufacturers, healthcare providers, investors, and policy makers—on technology trends, competitive positioning, and strategic growth pathways.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 190.19 Million |

|

Market Revenue in 2032 |

USD 344.29 Million |

|

CAGR (2025 - 2032) |

7.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Eko Health, 3M Littmann, ThinkLabs Medical, HD Medical, TytoCare –, Steth IO , M3DICINE, Sonavi Labs |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |