Reports

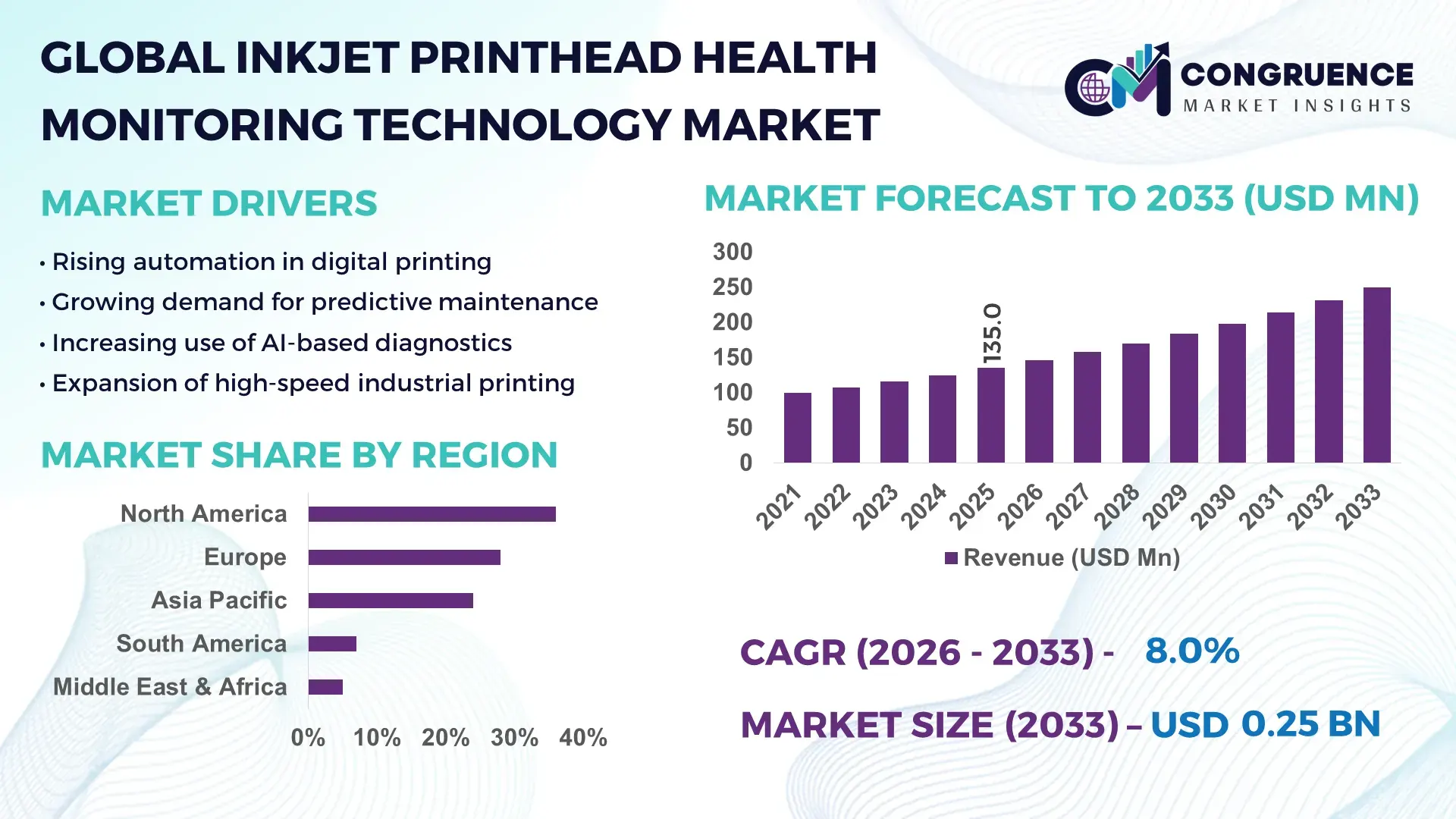

The Global Inkjet Printhead Health Monitoring Technology Market was valued at USD 135.0 Million in 2025 and is anticipated to reach a value of USD 249.9 Million by 2033, expanding at a CAGR of 8% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rising adoption of predictive maintenance, real-time nozzle diagnostics, and AI-enabled monitoring systems across industrial and commercial inkjet printing environments to reduce downtime and improve print consistency.

The United States dominates the Inkjet Printhead Health Monitoring Technology Market in terms of technological deployment and innovation intensity. The country hosts more than 35 large-scale industrial inkjet printer manufacturing and R&D facilities, particularly across electronics, packaging, and textile printing applications. Over 62% of industrial inkjet systems installed in the U.S. by 2025 are equipped with embedded health monitoring sensors for nozzle condition, ink flow stability, and thermal stress detection. Annual investments exceeding USD 420 million are directed toward smart printing infrastructure, AI-driven diagnostics, and Industry 4.0 integration. Adoption is strongest in packaging and label printing, which together account for over 48% of monitored printhead installations, followed by textile and electronics printing. Advanced firmware analytics, cloud-connected diagnostics, and edge-based fault prediction are increasingly standard across high-throughput printing lines, supporting scalable production efficiency and consistent output quality.

Market Size & Growth: Valued at USD 135.0 Million in 2025, projected to reach USD 249.9 Million by 2033 at an 8% CAGR, supported by increasing demand for predictive maintenance and zero-defect printing.

Top Growth Drivers: Predictive maintenance adoption (58%), reduction in unplanned downtime (42%), improvement in printhead lifespan (36%).

Short-Term Forecast: By 2028, automated health diagnostics are expected to reduce maintenance costs by 27% across industrial inkjet operations.

Emerging Technologies: AI-based nozzle diagnostics, MEMS-enabled ink flow sensors, cloud-connected printhead analytics platforms.

Regional Leaders: North America (USD 92.0 Million by 2033, strong industrial automation), Europe (USD 78.5 Million, sustainability-driven upgrades), Asia Pacific (USD 69.4 Million, high-volume manufacturing adoption).

Consumer/End-User Trends: Packaging, textile, and electronics manufacturers increasingly deploy continuous monitoring for high-speed production lines.

Pilot or Case Example: In 2024, a U.S. packaging printer achieved a 31% downtime reduction using AI-driven printhead health analytics.

Competitive Landscape: Market leader holds ~29% share, followed by Epson, Canon, Fujifilm Dimatix, and Ricoh.

Regulatory & ESG Impact: Energy efficiency standards and waste reduction mandates accelerate adoption of monitoring-enabled printheads.

Investment & Funding Patterns: Over USD 610 Million invested globally since 2022 in smart inkjet monitoring platforms and sensor integration.

Innovation & Future Outlook: Increased convergence of AI, IoT, and edge analytics will enable autonomous printhead optimization.

Inkjet Printhead Health Monitoring Technology Market adoption is concentrated across packaging (41%), textile printing (24%), electronics manufacturing (18%), and commercial graphics (17%). Recent innovations include self-calibrating nozzles, real-time clog detection, and ink chemistry–aware diagnostics. Regulatory pressure to reduce ink waste, combined with rising automation investments in Asia Pacific, is reshaping regional consumption patterns, while future growth is supported by cloud-integrated predictive analytics and digital twin-enabled printhead management.

The Inkjet Printhead Health Monitoring Technology Market is strategically critical to modern digital manufacturing as print quality, uptime reliability, and cost efficiency become decisive competitive factors. Health monitoring systems integrate sensors, firmware intelligence, and analytics platforms to enable real-time condition assessment of printheads, minimizing nozzle failures and ink inconsistencies. AI-enabled diagnostics deliver up to 34% improvement in fault detection accuracy compared to rule-based monitoring standards, directly supporting operational resilience.

In regional terms, Asia Pacific dominates in production volume, driven by high-throughput electronics and textile printing, while North America leads in adoption, with approximately 61% of industrial printers using advanced monitoring solutions. By 2028, AI-driven anomaly detection is expected to reduce unplanned printhead stoppages by 30%, significantly improving throughput efficiency. From an ESG perspective, firms are committing to ink waste reduction targets of 20–25% by 2030, enabled through precise nozzle health tracking and optimized ink delivery.

In 2024, a Japanese electronics manufacturer achieved a 28% improvement in yield consistency by deploying edge-based printhead diagnostics combined with machine learning algorithms. Looking forward, the Inkjet Printhead Health Monitoring Technology Market is positioned as a foundational pillar for smart manufacturing ecosystems, supporting compliance, sustainability, and long-term operational scalability.

The Inkjet Printhead Health Monitoring Technology Market is shaped by increasing digitalization of printing operations, rising cost sensitivity, and growing emphasis on predictive maintenance. Manufacturers are transitioning from reactive maintenance models to continuous monitoring frameworks that leverage sensor data and analytics. Integration with MES and cloud platforms is improving visibility across multi-site operations, while advances in MEMS sensors and AI algorithms are enhancing detection accuracy. Demand is strongest in high-speed, mission-critical printing environments where downtime directly impacts output and margins. At the same time, standardization challenges and integration complexity influence adoption patterns across regions.

Predictive maintenance is a primary driver as industrial printers increasingly rely on real-time diagnostics to prevent nozzle clogging, thermal stress, and ink flow irregularities. Facilities using health monitoring systems report up to 40% reduction in emergency maintenance events and 25–30% longer printhead lifespan. Packaging and electronics manufacturers, where print defects lead to high rejection rates, are prioritizing sensor-enabled printheads. The shift toward continuous production lines further amplifies demand for automated health monitoring to ensure uninterrupted operation and consistent quality.

Integration complexity remains a key restraint, particularly for legacy printing systems. Nearly 37% of small and mid-sized print shops report challenges integrating health monitoring software with existing hardware and workflow systems. High customization requirements, firmware compatibility issues, and the need for skilled technical personnel slow adoption. Additionally, upfront integration timelines can extend commissioning periods by 15–20%, discouraging cost-sensitive operators from immediate deployment.

The expansion of smart factories presents significant opportunities, as inkjet systems become interconnected components of digital production ecosystems. Smart manufacturing facilities deploying IIoT frameworks show over 45% higher utilization of condition monitoring tools. Integration with digital twins and centralized dashboards enables cross-line optimization and remote diagnostics. Emerging economies investing heavily in automated packaging and textile hubs are expected to adopt monitoring-enabled printheads as standard equipment, creating strong long-term demand.

As monitoring systems generate large volumes of operational data, managing, storing, and securing this information becomes challenging. Industrial printers report data handling costs rising by 18–22% after deploying advanced analytics platforms. Cybersecurity risks associated with cloud-connected diagnostics also raise concerns, particularly in regulated industries. Ensuring secure data transmission and compliance with industrial data standards adds complexity and increases deployment costs.

AI-Driven Real-Time Nozzle Diagnostics: AI-enabled monitoring platforms are increasingly deployed to detect nozzle clogging and misfiring in real time. Systems using machine learning algorithms achieve up to 35% faster fault identification and reduce print defects by 22%, supporting consistent output in high-speed production environments.

Expansion of Cloud-Connected Monitoring Platforms: Cloud-based health monitoring solutions now support multi-site visibility, with over 48% of large printing enterprises adopting centralized dashboards by 2025. These platforms enable remote diagnostics and reduce on-site maintenance interventions by 26%.

Integration of MEMS and Thermal Sensors: Advanced MEMS-based ink flow and temperature sensors are embedded in modern printheads, improving measurement accuracy by 30% compared to conventional sensing methods. Adoption is strongest in electronics and packaging printing, where precision is critical.

Shift Toward Modular Monitoring Architectures: Manufacturers are adopting modular health monitoring architectures, allowing sensor and software upgrades without full system replacement. Approximately 52% of new industrial printhead installations support modular diagnostics, reducing lifecycle upgrade costs by 20% and enhancing scalability across production lines.

The Inkjet Printhead Health Monitoring Technology Market is segmented across technology types, applications, and end-user industries, reflecting the diversity of deployment models and operational priorities in digital printing. By type, solutions range from hardware-centric sensor systems to software-driven AI analytics and cloud platforms, each addressing different levels of diagnostic sophistication and automation. Application segmentation is shaped by printing intensity, precision requirements, and tolerance for downtime, with packaging, textiles, electronics, and commercial graphics exhibiting distinct monitoring needs. End-user segmentation highlights the varying maturity of predictive maintenance adoption, with large industrial manufacturers leading deployment while smaller print service providers adopt more modular or subscription-based solutions. Across all segments, demand is increasingly influenced by integration with smart factory ecosystems, regulatory pressures on waste reduction, and the need for consistent quality in high-speed production environments.

The market is primarily divided into sensor-based monitoring systems, AI/ML analytics software, cloud-based monitoring platforms, edge firmware diagnostics, and hybrid integrated systems.

Sensor-based monitoring systems remain the leading type, accounting for 46% of total adoption, as they provide direct, real-time measurement of nozzle temperature, ink pressure, and flow stability—critical for high-volume industrial printers. Their reliability, low latency, and compatibility with legacy equipment underpin their leadership.

The fastest-growing type is AI/ML analytics software, expanding at approximately 14% CAGR, driven by the shift from reactive maintenance to predictive and prescriptive diagnostics, greater availability of labeled printhead performance data, and rising integration with MES and digital twin environments.

Cloud-based platforms enable multi-site visibility and remote troubleshooting but are typically adopted as complementary layers rather than standalone systems. Edge firmware diagnostics are gaining traction in high-speed packaging lines where millisecond-level response times are required. Hybrid integrated systems—combining embedded sensors with AI and cloud analytics—are emerging as the most advanced deployment model. Collectively, these remaining segments represent about 54% of the market, reflecting a diversified technology mix rather than single-solution dominance.

Key applications include packaging and labeling, textile printing, electronics manufacturing, commercial graphics, and industrial coding and marking.

Packaging and labeling is the leading application with roughly 44% share, as high-speed production lines require continuous monitoring to avoid costly recalls, reprints, and material waste. Tight quality standards in food, beverage, and pharmaceutical packaging further reinforce adoption.

The fastest-growing application is electronics printing, advancing at about 13% CAGR, supported by rising use of inkjet processes in printed circuit boards, semiconductor packaging, and functional inks where microscopic defects are unacceptable.

Textile printing is expanding due to digital customization and shorter production runs, while commercial graphics prioritize color consistency and brand compliance. Coding and marking applications use monitoring primarily to prevent batch traceability errors. Together, these secondary applications account for roughly 56% of usage, with varying intensity of monitoring depending on throughput and quality requirements.

Adoption trends are accelerating: in 2025, around 39% of global printing enterprises reported piloting printhead health monitoring systems for automated quality assurance, and over 57% of large packaging brands stated that they prefer suppliers using monitored digital printing lines to reduce compliance risk.

Major end-user segments include industrial manufacturers, commercial print service providers, packaging converters, textile producers, and electronics manufacturers.

Industrial manufacturers are the leading end-user group with approximately 41% share, as they operate continuous, high-throughput lines where downtime has the greatest financial impact. These firms prioritize integrated monitoring within smart factory architectures.

The fastest-growing end-user is packaging converters, expanding at about 12% CAGR, fueled by stricter traceability regulations, growth in personalized packaging, and rising automation investments.

Commercial print providers are adopting modular monitoring to balance cost and reliability, while textile producers use diagnostics to maintain color accuracy across large digital runs. Electronics manufacturers deploy the most advanced monitoring due to microscopic quality tolerances. Combined, these secondary end-users represent roughly 59% of the market, with adoption intensity varying by production scale and regulatory exposure.

In 2025, about 37% of mid-sized print enterprises reported piloting monitoring systems for customer quality dashboards, and over 55% of global packaging brands indicated greater trust in suppliers using AI-enabled print diagnostics for compliance assurance.

North America accounted for the largest market share at 36% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2026 and 2033.

North America leads with over 68% penetration of monitored industrial inkjet systems and more than 1.9 million active digital printheads deployed with diagnostic capabilities. Asia-Pacific shows accelerating momentum, driven by over 45% of new industrial printer installations occurring in China, India, and Japan combined. Europe maintains strong adoption supported by sustainability mandates, while South America and the Middle East & Africa remain emerging but technology-upgrading regions.

North America holds approximately 36% market share, driven by packaging, electronics, and commercial printing industries. Over 61% of large printing enterprises use real-time printhead diagnostics to minimize downtime. Regulatory focus on waste reduction and traceability supports adoption. AI-enabled predictive maintenance and cloud-connected monitoring are widely implemented. A major U.S.-based printer OEM reported 30% fewer emergency shutdowns after deploying sensor-integrated printheads. Enterprise users show higher adoption in packaging and regulated manufacturing segments.

Europe accounts for around 28% market share, led by Germany, the UK, and France. Strict environmental regulations and circular economy initiatives push demand for ink waste reduction and defect monitoring. Over 54% of industrial printers integrate diagnostics for compliance tracking. Adoption of explainable AI diagnostics is rising. European converters prioritize transparent monitoring systems to meet regulatory audits and sustainability benchmarks.

Asia-Pacific ranks first in volume of installations, contributing over 42% of global industrial inkjet system deployments. China, Japan, and India dominate consumption due to electronics, textile, and packaging manufacturing. Smart factory investments and local innovation hubs support rapid integration. More than 47% of new print lines include embedded monitoring. Adoption is strongly driven by e-commerce packaging and high-throughput production.

South America represents about 7% market share, led by Brazil and Argentina. Packaging and media printing drive demand as facilities modernize equipment. Government incentives for manufacturing efficiency support gradual adoption. Approximately 29% of large print facilities have begun integrating basic monitoring tools. Consumer demand is closely tied to localized content and labeling requirements.

The Middle East & Africa account for roughly 5% of global demand, with growth centered in the UAE and South Africa. Adoption is driven by packaging, construction materials printing, and industrial coding. Over 25% of new industrial printers in the GCC include diagnostic features. Technology modernization initiatives and trade partnerships support gradual uptake, with enterprise buyers prioritizing durability and uptime.

United States – 24% Market Share: High industrial automation levels and widespread adoption of predictive maintenance systems.

China – 18% Market Share: Large-scale manufacturing base and rapid deployment of smart factory printing infrastructure.

The global Inkjet Printhead Health Monitoring Technology Market exhibits a moderately fragmented competitive environment with a mix of established multinational corporations and emerging specialized technology providers. Over 25 active competitors are competing across hardware, software, and integrated diagnostic platform segments, reflecting broad participation rather than dominance by just a few players. The top 5 companies together hold around 34–38% combined share of the overall ecosystem, meaning strategic positioning and innovation are critical to gaining competitive advantage. Industry leaders such as Canon Inc., HP Inc., Epson, Ricoh, and Konica Minolta maintain strong market positions through continuous R&D investments, strategic partnerships, and product launches that emphasize AI-enabled diagnostics, IoT connectivity, and predictive analytics capabilities.

Strategic initiatives have intensified: several players have formed R&D collaborations and go-to-market alliances to co-develop high-precision printheads with enhanced health monitoring capabilities, and integration with MES and cloud platforms is becoming standard practice. Pricing strategies and modular monitoring solutions have emerged as key differentiators, particularly in textile and packaging applications where cost-performance balance drives purchasing decisions. Innovation trends show a focus on MEMS-based sensor integration, AI/ML-driven diagnostic software, and edge-to-cloud connected platforms that support real-time nozzle health assessment and continuous performance optimization. Competitive pressures continue to be shaped by technological advancement velocity, intellectual property portfolios, and the ability to support industry 4.0–aligned operational transformation.

Ricoh Company, Ltd.

Konica Minolta, Inc.

Xaar plc

Fujifilm Dimatix, Inc.

Seiko Instruments

Kyocera Corporation

SII Printek

Toshiba Tec Corporation

Brother Industries

Memjet

Lexmark

The technological landscape for the Inkjet Printhead Health Monitoring Technology Market is evolving rapidly as manufacturers seek greater precision, reduced downtime, and smarter diagnostic capabilities. A central driver is the integration of MEMS-based sensor technology directly into printhead assemblies, enabling detailed real-time monitoring of nozzle temperature, ink pressure, flow consistency, and vibration patterns. Nearly 48% of global printhead manufacturers now integrate advanced MEMS technology to enhance sensing precision while reducing energy consumption by over 20%, strengthening operational reliability and performance consistency.

AI and machine learning algorithms are increasingly embedded within monitoring platforms to interpret complex sensor signals, allowing predictive insights that anticipate nozzle wear or clogging before production impact occurs. This shift toward predictive and prescriptive analytics enhances uptime and supports intelligent maintenance scheduling across industrial lines. Edge computing integration ensures that time-critical diagnostics occur at the machine level, while cloud-based analytics give enterprise-wide visibility across geographically dispersed production facilities.

Another trend is open-platform architecture, encouraging interoperable ecosystems where third-party diagnostic modules and monitoring dashboards can seamlessly integrate with existing MES systems. This approach shortens deployment cycles and expands customization options for end users. Additionally, multi-parameter sensing arrays are being deployed to monitor environmental factors such as humidity and substrate variations that influence print quality, especially in high-precision packaging and electronics applications.

Advancements in materials science, such as the use of low-viscosity and UV-curable inks, demand more sophisticated monitoring to maintain droplet placement accuracy under varying conditions. Modular sensor kits and firmware-upgradeable diagnostic features allow legacy printheads to be retrofitted with health monitoring capabilities, increasing total addressable technology penetration. The combined impact of these technologies is elevating reliability, enabling faster troubleshooting, and reducing lifecycle maintenance costs—key performance indicators for digital printing operations.

• In January 2026, Meteor Inkjet Ltd launched its Nozzle Health Technology, the first commercially available system to provide real-time monitoring of every nozzle in an inkjet printhead, enabling manufacturers to instantly detect wetting, blockage, or air ingestion and take corrective actions before print defects occur. Source: www.meteorinkjet.com

• In October 2025, Meteor Inkjet introduced advanced DropWatcher optics, enhancing visualisation precision in inkjet development environments to better characterize droplet formation and support optimized printhead diagnostics. Source: www.meteorinkjet.com

• In June 2024, HP Inc. unveiled its latest lineup of digital printing presses with intelligent solutions designed for automation and production efficiency, promoting broader adoption of integrated diagnostics and workflow automation in inkjet systems. Source: www.hp.com

• In October 2024, Ricoh Company, Ltd. announced the establishment of Ricoh Printing Solutions Europe Limited, consolidating industrial printing functions to enhance support and accelerate development of advanced inkjet technologies including high-reliability printheads and digital production tools. Source: www.ricoh.com

The scope of the Inkjet Printhead Health Monitoring Technology Market Report encompasses a comprehensive evaluation of technologies, segments, geographic regions, and industry applications shaping the global competitive landscape. This includes detailed insights into sensor technologies, software analytics platforms, and integrated monitoring systems that support real-time diagnostics and predictive maintenance across printhead ecosystems. Coverage extends across product types such as MEMS-enabled sensors, AI/ML-based diagnostic software, edge computing modules, and hybrid diagnostics architectures that combine hardware with cloud analytics.

Geographical analysis highlights regional deployment trends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing granular evaluation of regional technology penetration, manufacturing infrastructure, and digital transformation readiness. Application domains include industrial packaging, textiles, electronics manufacturing, commercial graphics, and coding & marking, each with unique monitoring needs, performance criteria, and end-user expectations. The report also examines how technology trends such as open-platform integration, multi-parameter sensing, and real-time anomaly detection influence adoption and operational decision-making in high-throughput environments.

Industry focus areas cover how digital transformation initiatives—such as smart factory frameworks and Industry 4.0 adoption—accelerate integration of health monitoring systems into broader enterprise workflows. The scope further identifies emerging niches like additive manufacturing and IoT-connected diagnostics, along with infrastructure considerations that support cross-site monitoring and predictive analytics across distributed production facilities. Strategic competitive profiling of key players, innovation trends, and technology partnerships forms an integral part of the report, offering business leaders actionable insights to guide investment, deployment, and technology roadmap decisions.

This comprehensive perspective ensures that stakeholders—ranging from printhead OEMs and software solution providers to enterprise end users and system integrators—can assess technological readiness, segment opportunities, and strategic imperatives within the evolving landscape of inkjet printhead health monitoring.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 135.0 Million |

| Market Revenue (2033) | USD 249.9 Million |

| CAGR (2026–2033) | 8.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Canon Inc., HP Inc., Epson Corporation, Ricoh Company, Ltd., Konica Minolta, Inc., Xaar plc, Fujifilm Dimatix, Inc., Seiko Instruments, Kyocera Corporation, SII Printek, Toshiba Tec Corporation, Brother Industries, Memjet, Lexmark |

| Customization & Pricing | Available on Request (10% Customization Free) |