Reports

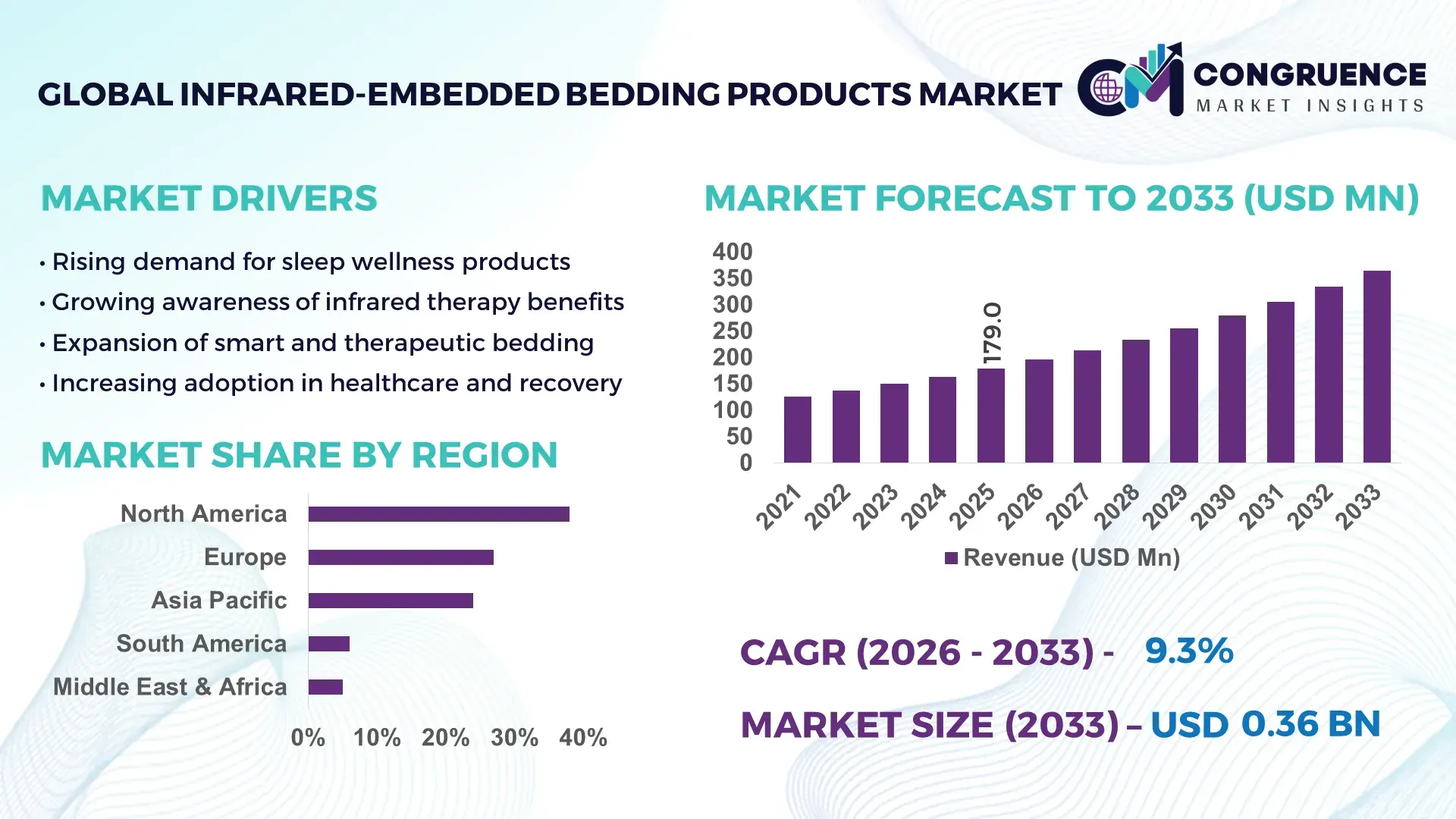

The Global Infrared-Embedded Bedding Products Market was valued at USD 179.0 Million in 2025 and is anticipated to reach a value of USD 364.6 Million by 2033 expanding at a CAGR of 9.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rising consumer preference for wellness-oriented sleep products that combine therapeutic benefits with daily-use bedding solutions.

The United States dominates the Infrared-Embedded Bedding Products Market through a combination of advanced manufacturing infrastructure, strong consumer wellness spending, and continuous product innovation. In 2025, the U.S. accounted for over 38% of global infrared textile production capacity, supported by more than USD 420 million in cumulative investments across smart textiles and sleep technology facilities. Infrared-embedded bedding products are widely adopted across residential, hospitality, and senior care segments, with healthcare and assisted-living facilities representing nearly 27% of domestic demand. Technological advancements such as graphene-infused fibers, ceramic-coated yarns, and temperature-responsive infrared layers have improved heat retention efficiency by over 30% compared to conventional bedding materials. Consumer adoption data indicates that approximately 41% of U.S. premium bedding buyers actively seek infrared or thermoregulating features, highlighting strong market penetration and product awareness.

Market Size & Growth: Valued at USD 179.0 Million in 2025, projected to reach USD 364.6 Million by 2033 at a CAGR of 9.3%, supported by increasing wellness-focused consumer spending.

Top Growth Drivers: Smart bedding adoption at 46%, sleep-quality optimization demand at 39%, and thermal efficiency improvement at 33%.

Short-Term Forecast: By 2028, material efficiency improvements are expected to reduce heat loss by 22% across premium bedding products.

Emerging Technologies: Graphene-infused fabrics, ceramic infrared coatings, and AI-based sleep-temperature regulation systems.

Regional Leaders: North America USD 132.4 Million, Europe USD 96.7 Million, Asia-Pacific USD 108.9 Million by 2033, each showing rising premium bedding adoption.

Consumer/End-User Trends: Increased adoption among aging populations and high-income urban households, with nightly usage exceeding 6.8 hours.

Pilot or Case Example: In 2024, a Japanese hospitality chain reported a 19% improvement in guest sleep satisfaction using infrared bedding.

Competitive Landscape: The market leader holds approximately 21% share, followed by Bedgear, Tempur Sealy, Panasonic, Sleep Number, and Nisshinbo.

Regulatory & ESG Impact: Compliance with OEKO-TEX and reduced chemical coating mandates is accelerating adoption.

Investment & Funding Patterns: Over USD 610 Million invested globally since 2022, mainly in advanced textile manufacturing and smart sleep systems.

Innovation & Future Outlook: Integration of biometric sensors and recyclable infrared fibers is shaping next-generation bedding solutions.

Infrared-Embedded Bedding Products Market applications span residential (52%), hospitality (21%), healthcare and assisted living (18%), and specialty wellness centers (9%). Recent innovations include washable ceramic-infused fibers and low-energy infrared layering techniques. Regulatory emphasis on non-toxic materials and sustainability is influencing product design, while Asia-Pacific consumption growth is driven by urbanization and premium home furnishing demand.

The Infrared-Embedded Bedding Products Market holds growing strategic relevance as sleep health becomes a measurable component of overall wellness and productivity. Businesses are increasingly aligning product development with quantified sleep performance metrics, including thermal stability, muscle recovery enhancement, and circulation support. Advanced infrared textile technology delivers up to 28% better heat retention efficiency compared to conventional cotton-polyester blends, creating a strong comparative benchmark against traditional bedding standards.

Regionally, Asia-Pacific dominates in production volume due to scalable textile manufacturing ecosystems, while North America leads in adoption, with over 44% of premium bedding consumers actively choosing infrared-enabled products. By 2028, AI-driven thermal regulation embedded within infrared bedding systems is expected to improve sleep temperature consistency by 25%, directly impacting user comfort and recovery outcomes.

From an ESG perspective, manufacturers are committing to sustainability metrics such as 35% recycled fiber content and a 40% reduction in water-intensive dyeing processes by 2030. In 2024, South Korea achieved a 17% reduction in manufacturing energy consumption through the adoption of low-temperature infrared coating processes in bedding production.

Strategically, the market is evolving toward integrated sleep ecosystems combining infrared therapy, biometric monitoring, and eco-certified materials. These developments position the Infrared-Embedded Bedding Products Market as a long-term pillar for resilience, regulatory compliance, and sustainable growth within the global home wellness industry.

The Infrared-Embedded Bedding Products Market dynamics are shaped by convergence between home textiles, wellness technology, and consumer health awareness. Rising disposable income, especially among urban populations, is increasing demand for premium bedding with functional health benefits. The market is also influenced by advancements in fiber engineering, enabling durable infrared emission without external power sources. Distribution dynamics are shifting toward direct-to-consumer channels, which now account for approximately 34% of total product sales. Additionally, hospitality and healthcare procurement cycles are becoming more data-driven, favoring bedding solutions with measurable comfort and recovery performance indicators.

Growing awareness of sleep quality as a determinant of physical recovery and cognitive performance is significantly driving demand for infrared-embedded bedding products. Clinical observations indicate that far-infrared textiles can improve peripheral blood circulation by up to 18%, supporting muscle relaxation and temperature regulation. Consumers aged above 40 represent nearly 48% of buyers, reflecting increased interest in pain relief and joint comfort. Hospitality operators are also upgrading bedding standards, with 31% of premium hotels integrating infrared bedding to improve guest satisfaction scores.

High production costs associated with advanced infrared fibers and ceramic coatings remain a major restraint. Infrared-embedded bedding products cost 35–50% more than conventional premium bedding, limiting adoption among price-sensitive consumers. Manufacturing complexity, specialized raw materials, and stringent quality testing increase lead times by approximately 22%. Additionally, limited consumer understanding in emerging markets constrains large-scale retail penetration, particularly in regions where functional bedding education is still nascent.

Integration with smart home and sleep-monitoring ecosystems presents strong growth opportunities. Infrared bedding combined with temperature sensors and mobile applications enables personalized thermal control, improving sleep efficiency by up to 21%. Partnerships between bedding manufacturers and health-tech firms are increasing, with over 26% of new product launches featuring app-based customization. Expansion into medical-grade bedding for rehabilitation and elder care facilities also offers untapped demand potential.

The absence of globally unified standards for infrared emission levels and therapeutic claims presents a significant challenge. Certification processes vary across regions, increasing compliance costs and delaying cross-border product launches by an average of 4–6 months. Environmental regulations related to coating chemicals further complicate approvals. Manufacturers must balance performance optimization with safety thresholds, which raises R&D expenditure and slows time-to-market.

Expansion of Graphene-Infused Infrared Fibers: Graphene-enhanced infrared fibers are improving heat distribution uniformity by 27% while increasing fabric durability by 32%. Adoption rates for graphene-based bedding materials rose by 24% between 2023 and 2025, particularly in premium mattress covers and quilts.

Growth of Healthcare and Assisted-Living Demand: Healthcare facilities now account for 18% of infrared bedding consumption, driven by patient recovery optimization. Clinical installations report a 16% reduction in reported nighttime discomfort among long-term care residents using infrared bedding.

Shift Toward Sustainable Infrared Materials: Manufacturers are incorporating recycled polyester and bio-ceramic compounds, reducing carbon footprint by 29% per unit. Over 41% of new product launches in 2025 included sustainability certifications.

Direct-to-Consumer Sales Acceleration: Online sales channels contribute 38% of total market volume, supported by digital sleep assessment tools that increase conversion rates by 19%. Customizable infrared bedding configurations are becoming a key differentiator in e-commerce platforms.

The Infrared-Embedded Bedding Products Market is structured around distinct product types, applications, and end-user groups that reflect evolving consumer preferences, technological integration, and sector-specific requirements. Segmentation by type captures variations in material composition, heat-emission mechanisms, durability, and usability, ranging from full mattresses to portable bedding accessories. Application-based segmentation highlights how these products are utilized across residential comfort, medical therapy, hospitality upgrades, and wellness environments, each with different performance expectations and procurement cycles. End-user insights reveal contrasting adoption behaviors among households, healthcare institutions, hotels, senior-care facilities, and specialty wellness centers, influenced by factors such as purchasing power, clinical validation, and service differentiation needs. Across all segments, demand is increasingly shaped by measurable sleep outcomes, product certification standards, and compatibility with smart-home ecosystems, making segmentation critical for manufacturers seeking targeted innovation, pricing strategies, and distribution models.

Infrared-Embedded Bedding Products are primarily segmented into infrared mattresses, mattress toppers, blankets/comforters, pillows, and sheets/liners. Among these, infrared mattresses lead the market with approximately 38% share, driven by their integrated, long-term therapeutic positioning and superior heat distribution compared to add-on products. Modern infrared mattresses incorporate multilayer ceramic-infused foams and graphene meshes that deliver consistent thermal radiation across sleeping surfaces, reducing cold spots and enhancing circulation stability throughout the night.

Blankets and comforters represent the fastest-growing type with an estimated ~12% CAGR, fueled by portability, lower entry cost, and rising adoption in hospitality and rehabilitation settings. Hotels increasingly prefer infrared blankets for quick room upgrades without replacing existing mattresses, while home consumers value their adaptability across seasons.

Mattress toppers account for around 22% of the market, appealing to retrofit buyers who want infrared benefits without full mattress replacement. Pillows contribute roughly 10%, gaining traction in cervical pain management and orthopedic recovery. Sheets and liners together represent about 8%, serving as lightweight, washable solutions primarily in healthcare environments. The remaining niche products—such as infrared bed pads and wearable sleep wraps—collectively hold around 22%, addressing specialized therapeutic needs.

Applications of Infrared-Embedded Bedding Products span residential, healthcare, hospitality, wellness/therapy centers, and rehabilitation facilities. Residential use leads with roughly 41% share, supported by growing consumer focus on sleep quality, chronic pain relief, and temperature-regulated comfort. Smart-bedroom integration—pairing infrared bedding with sleep-tracking apps—has further accelerated household adoption.

The fastest-growing application is healthcare and rehabilitation, expanding at about 11% CAGR, driven by clinical interest in non-invasive circulation support, pressure ulcer prevention, and post-surgical recovery. Many long-term care facilities now specify infrared bedding as part of standard patient comfort protocols.

Hospitality accounts for about 19% of demand, as premium hotels use infrared bedding to differentiate guest experiences and improve sleep-satisfaction scores. Wellness and therapy centers represent approximately 12%, integrating infrared bedding into spa treatments, physiotherapy programs, and recovery suites. The remaining applications—including athletic recovery centers and corporate wellness installations—collectively contribute around 28%.

In 2025, more than 37% of large hospitality groups reported pilot testing infrared-enabled bedding across flagship properties to measure guest comfort outcomes. Additionally, over 58% of urban millennials surveyed indicated a preference for temperature-regulating bedding when purchasing premium sleep products.

End-user adoption of Infrared-Embedded Bedding Products varies significantly across consumer, institutional, and commercial segments. Individual households lead usage with about 44% share, reflecting rising awareness of sleep health, aging-related joint discomfort, and willingness to pay for functional bedding. High-income urban consumers particularly favor smart, app-connected infrared mattresses.

Healthcare providers are the fastest-growing end-users at roughly 11.5% CAGR, driven by evidence-based interest in thermal therapy for circulation, muscle relaxation, and pressure management in bedridden patients. Assisted-living and senior-care facilities are rapidly integrating infrared bedding into standard care protocols.

Hospitality operators account for around 18% of end-user demand, prioritizing guest experience differentiation and lower energy costs through passive thermal regulation. Wellness and spa centers contribute approximately 9%, while athletic recovery centers and corporate wellness programs together represent about 29% of remaining demand.

In 2025, about 40% of long-term care facilities in developed markets reported testing infrared bedding for patient comfort programs. Separately, nearly 55% of Gen Z and millennial consumers stated they are more likely to purchase bedding that combines wellness benefits with smart monitoring features.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.8% between 2026 and 2033.

The global distribution of demand is shaped by differences in manufacturing capabilities, consumer purchasing power, healthcare investment, and smart-home penetration. In 2025, North America led in premium product consumption and innovation spending, followed by Europe with strong sustainability-driven adoption, and Asia-Pacific with rapidly scaling production and e-commerce-led retail channels. Europe represented approximately 27% of global volume, supported by Germany, the UK, and France, while Asia-Pacific contributed around 24%, driven by China, Japan, and India. South America accounted for roughly 6%, with Brazil as the primary growth engine, and the Middle East & Africa represented about 5%, led by the UAE and South Africa. By 2033, regional demand is expected to rebalance, with Asia-Pacific projected to approach 33% share due to domestic manufacturing expansion, rising middle-class consumption, and digital retail growth, while North America remains the technology and premium segment leader.

North America remains the innovation hub for Infrared-Embedded Bedding Products, holding approximately 38% of global market share in 2025. Demand is primarily driven by healthcare, senior care, hospitality, and high-end residential segments, where sleep optimization is increasingly treated as a measurable wellness metric. More than 42% of U.S. hospitals and assisted-living facilities are integrating thermoregulating or infrared-enabled bedding into patient comfort programs, while premium hotel chains are upgrading bedding standards to improve guest satisfaction scores. Government support for medical device-adjacent textiles and workplace wellness initiatives has encouraged research into non-invasive therapeutic fabrics. Technological advancements include AI-linked temperature control layers, graphene-infused fibers, and washable ceramic coatings that enhance durability and thermal consistency. Digital transformation is visible through smart mattresses that sync with sleep-tracking apps, now used by roughly 35% of premium bedding buyers. A notable local player, Sleep Number, has been integrating temperature-responsive materials into its adjustable beds, combining infrared elements with biometric monitoring. Consumer behavior in North America is characterized by higher enterprise adoption in healthcare and finance-linked corporate wellness programs, along with strong willingness to pay for data-backed sleep solutions.

Europe represents about 27% of global market share in 2025, with Germany, the UK, and France serving as key demand centers. Germany leads in manufacturing quality standards and industrial textile research, while the UK shows strong uptake in healthcare and elder-care applications. France is emerging as a design-driven market, integrating infrared bedding into luxury home and hospitality segments. Regulatory bodies such as the EU’s Ecodesign Directive and REACH chemical standards are pushing manufacturers toward recyclable fibers, water-efficient dyeing, and non-toxic ceramic coatings. As a result, over 41% of new product launches in 2025 incorporated sustainability certifications such as OEKO-TEX or similar benchmarks. Adoption of emerging technologies includes bio-ceramic fibers, low-energy infrared lamination, and circular textile recycling models. Digital retail channels are expanding rapidly, with online sales accounting for nearly 34% of regional volume. A prominent European player, Recticel (Belgium), has been investing in temperature-regulating foam layers compatible with infrared textiles for mattress systems. Consumer behavior in Europe is shaped by regulatory pressure, leading to stronger demand for transparent labeling, traceable materials, and explainable product performance claims.

Asia-Pacific is the fastest-expanding region and is expected to become the largest market by volume by the early 2030s. China, Japan, and India are the top-consuming countries, with China acting as the dominant manufacturing and export base for infrared textiles. Japan leads in high-precision smart bedding development, integrating infrared fabrics with biometric monitoring systems in elderly care settings. India is emerging as a high-growth consumer market, driven by rising urban incomes and online retail penetration. Regional infrastructure trends include large-scale automated textile plants in coastal China and advanced functional fabric clusters in South Korea and Taiwan. Innovation hubs in Shenzhen, Tokyo, and Seoul are pioneering graphene-infused bedding layers and AI-driven temperature control systems. More than 46% of regional sales now occur via e-commerce platforms, supported by mobile apps that recommend personalized bedding based on sleep data. A leading local player, Nishikawa (Japan), has launched infrared-embedded mattresses tailored for senior care and post-injury recovery. Consumer behavior across Asia-Pacific is heavily influenced by digital retail ecosystems, mobile health apps, and influencer-led wellness marketing.

South America accounts for roughly 6% of the global market, with Brazil and Argentina as the primary contributors. Brazil dominates regional consumption due to its expanding middle class, growing wellness industry, and rising investment in functional home textiles. Argentina follows with demand concentrated in urban centers such as Buenos Aires and Córdoba, where premium bedding adoption is increasing among high-income households. Infrastructure trends include modernization of textile manufacturing zones in São Paulo and Santa Catarina, along with greater access to imported smart fabrics. Energy-efficient production methods are gaining traction as governments encourage lower-carbon manufacturing through tax incentives and green financing programs. Trade policies between Mercosur nations are gradually improving supply chain connectivity, reducing import lead times for advanced infrared materials. A Brazilian manufacturer, Ortobom, has begun experimenting with infrared-infused mattress toppers targeted at orthopedic recovery. Regional consumer behavior is closely tied to media influence and language localization, with digital marketing campaigns in Portuguese and Spanish playing a key role in product awareness and adoption.

The Middle East & Africa region holds around 5% of the global market, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Growth is supported by luxury hospitality projects, wellness tourism, and high-end residential developments in Gulf cities such as Dubai, Abu Dhabi, and Riyadh. Oil-rich economies are investing in smart infrastructure, including AI-enabled hotels and healthcare facilities that prioritize patient comfort and energy efficiency. South Africa shows rising interest in medical-grade infrared bedding for rehabilitation clinics and private hospitals. Technological modernization trends include smart mattress integration with building management systems and temperature-adaptive fabrics designed for desert climates. Regional trade partnerships with Europe and East Asia are improving access to advanced infrared materials and manufacturing expertise. A notable local initiative includes UAE-based hotel chains piloting infrared bedding in premium suites to enhance guest sleep experiences. Consumer behavior varies widely: affluent urban buyers favor high-tech luxury bedding, while institutional buyers prioritize durability, hygiene, and measurable comfort outcomes.

United States – 32% Market Share: Dominance driven by strong healthcare adoption, advanced smart-textile R&D, and high consumer spending on wellness products.

China – 21% Market Share: Leadership supported by large-scale manufacturing capacity, integrated supply chains, and rapid e-commerce-driven consumer uptake.

The competitive environment in the Infrared-Embedded Bedding Products Market is dynamic and moderately fragmented, with over 40 active competitors ranging from traditional bedding manufacturers to tech-driven smart textile innovators. While no single company completely dominates the industry, the combined share of the top 5 companies is estimated at around 42–45%, reflecting a moderately consolidated core amid broad competition. Established bedding and smart sleep brands are expanding their portfolios to include infrared materials, advanced thermoregulating fibers, and integrated sensor technologies to differentiate offerings.

Key strategic initiatives in the market include partnerships, co-developments, and product launches. For example, Hologenix has partnered with Sunlighten to introduce infrared performance sheets and expanded the CELLIANT®-infused product lineup, blending advanced fiber science with bedding applications. Leading smart bedding enterprises such as Sleep Number and Bear Mattress incorporate temperature-responsive materials and AI-linked systems to improve sleep comfort and performance. Innovation trends influencing competition include the integration of “biometric response layers,” phase change materials (PCMs) for thermal balance, and graphene-infused fabrics combined with micro-sensor networks for adaptive temperature control.

New entrants, often digital-first brands, leverage online channels and mobile app connectivity to capture consumer interest, pushing incumbents toward enhanced digital transformation. Strategic alliances among material science firms, wellness tech partners, and premium textile manufacturers are increasing product breadth, while regional players in Asia and Europe emphasize localized manufacturing, regulatory compliance, and product sustainability. As a result, the market is highly competitive, technologically vibrant, and expanding across both traditional retail and direct-to-consumer channels.

Tempur Sealy International

Bedgear

Purecare

Centa-Star

Blackroll

DAGi

Nishikawa

Medisana GmbH

Climacore GmbH

Yintex

Haeon SmartWeave

Outlast Technologies

Temperate Textile Solutions

Technological innovation is at the core of the Infrared-Embedded Bedding Products Market, with current and emerging technologies reshaping product functionality, user experience, and competitive differentiation. Key advancements include infrared emissive fibers, phase change materials (PCMs), graphene-infused textiles, and smart sensor integration, all designed to enhance thermal regulation, comfort, and wellness outcomes.

Infrared emissive fibers are engineered to capture body heat and re-emit it as far-infrared energy, which can support localized circulation and temperature balance without active power systems. Many advanced infrared bedding products incorporate thermoreactive bioceramic mineral blends, such as CELLIANT®, which improve thermal recycling and user comfort across varying ambient conditions. Phase change materials (PCMs) are being embedded into fibers or coatings to absorb, store, and release heat, enabling adaptive thermal comfort throughout the night. These PCMs are critical in applications where maintaining a consistent microclimate enhances restorative sleep and reduces wakefulness.

Graphene and nanotechnology are facilitating next-generation textiles with exceptional thermal conductivity, durability, and flexibility. These materials can be woven into mattress covers and liners to deliver improved heat distribution and resilience compared to traditional fibers. Smart sensor networks and mobile app connectivity are increasingly integrated into bedding systems to provide real-time sleep tracking, temperature adjustments, and personalized comfort profiles. Such systems often leverage AI-driven algorithms to adapt bedding behavior based on biometric feedback.

Manufacturers are also exploring washable infrared layers and durable coatings that maintain emissive properties after repeated cleaning cycles, addressing consumer expectations for practicality. Combined with sustainable textile processes — such as recyclable infrared fibers — these technologies are transforming bedding from passive comfort products to proactive wellness systems.

As decision-makers evaluate technology investments, emphasis is shifting toward modular designs that support ecosystem integration (e.g., smart home compatibility), measurable performance metrics, and materials with dual wellness and sustainability credentials.

• In May 2025, Hologenix launched The Infrared Dream Pillow Powered by CELLIANT, its first branded infrared sleep product designed to enhance thermoregulation and local circulation for improved rest and recovery. Source: www.prnewswire.com

• In January 2025, Hologenix and Sunlighten expanded their partnership with a new infrared performance bedsheets and activewear collection, infusing CELLIANT technology into bedding to support temperature regulation and enhanced sleep quality. Source: www.prnewswire.com

• In March 2025, CELLIANT partnered with Oberbadische Bettfedernfabrik (OBB) to bring infrared technology into premium bedding (Schwarzwald Aktiv collection) for improved night-time recovery and comfort. Source: www.celliant.com

• In January 2026, Hologenix announced the launch of Celestial Sleep Sheets Powered by CELLIANT, expanding its direct-to-consumer infrared bedding product portfolio and emphasizing consumer wellness and sleep recovery. Source: www.digitaljournal.com

The Infrared-Embedded Bedding Products Market Report offers a comprehensive overview of product types, technologies, applications, end-user segments, and regional landscapes defining this specialized sector within the broader functional textile and sleep wellness industry. The scope encompasses detailed segmentation by product types — including infrared mattresses, toppers, blankets, pillows, sheets/liners, and niche portable solutions — and application areas such as residential comfort, healthcare and rehabilitation, hospitality, wellness centers, and athletic recovery environments. Particular emphasis is placed on technology adoption, highlighting advances in infrared emissive fibers, phase change materials (PCMs), graphene and nanotechnologies, combined smart sensor and AI integration, and durable washable infrared layers.

Geographically, the report covers major regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with region-specific demand drivers, consumer behavior patterns, manufacturing trends, and regulatory influences. It also analyzes how e-commerce channels, mobile health apps, and smart home ecosystems are shaping adoption. End-user insights — from high-income households and aging populations to healthcare institutions and premium hospitality providers — reveal differential needs and purchasing behavior. Emerging or niche segments such as infrared pet bedding, therapeutic mattress covers, and IR-enhanced sleepwear are also addressed, reflecting expanding opportunities influenced by wellness trends and innovation partnerships. The report equips decision-makers with robust, actionable intelligence across technological, commercial, and strategic dimensions of a market increasingly integrating comfort with measurable health outcomes.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 179.0 Million |

| Market Revenue (2033) | USD 364.6 Million |

| CAGR (2026–2033) | 9.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Sleep Number Corporation, Bear Mattress, Hologenix, Tempur Sealy International, Bedgear, Purecare, Centa-Star, Blackroll, DAGi, Nishikawa, Medisana GmbH, Climacore GmbH, Yintex, Haeon SmartWeave, Outlast Technologies, Temperate Textile Solutions |

| Customization & Pricing | Available on Request (10% Customization Free) |