Reports

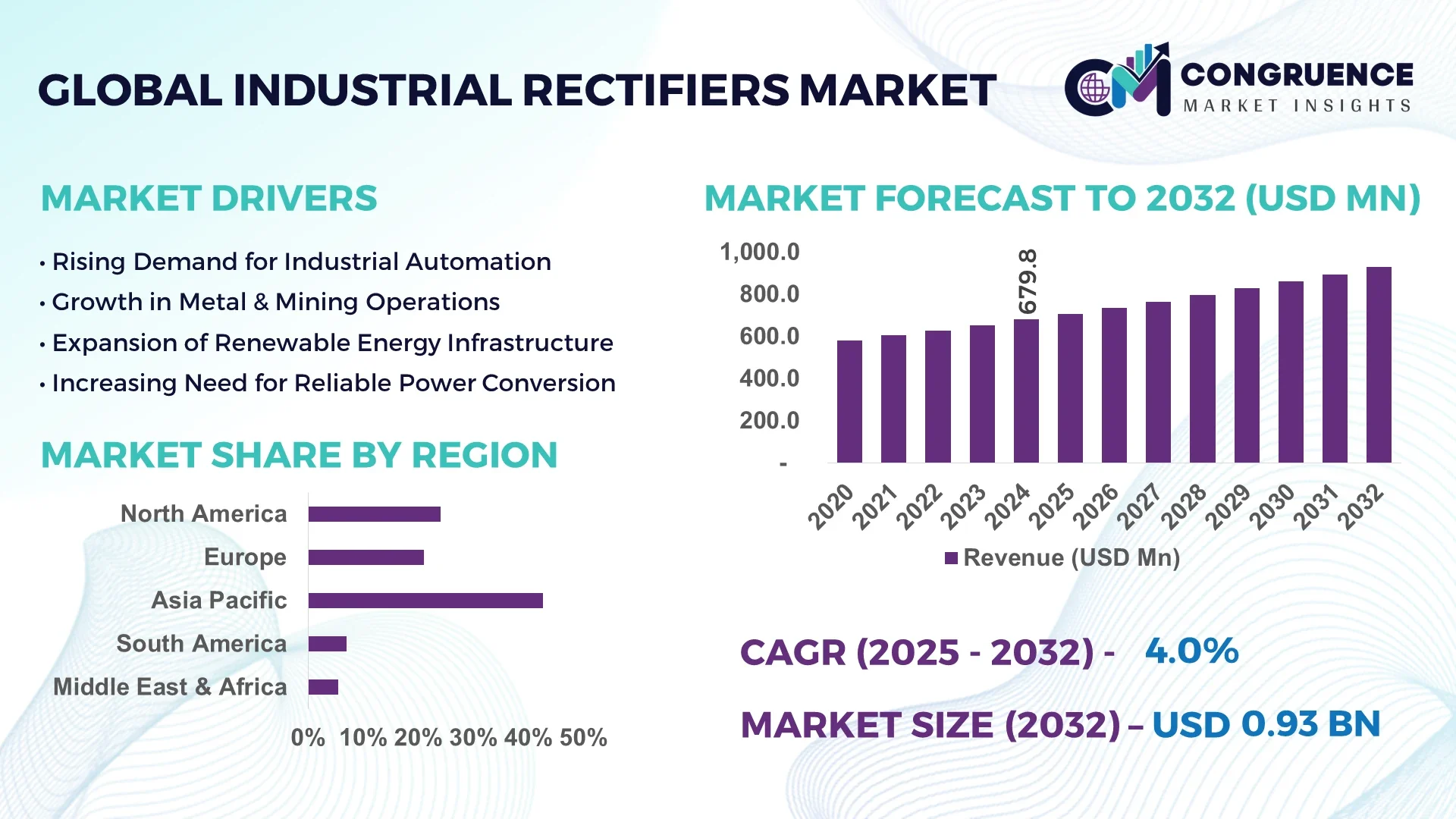

The Global Industrial Rectifiers Market was valued at USD 679.8 Million in 2024 and is anticipated to reach a value of USD 930.4 Million by 2032, expanding at a CAGR of 4.0% between 2025 and 2032.

Asia-Pacific, particularly China, dominates the global industrial rectifiers market, accounting for over 40% of the market share. China’s rapid industrialization, expanding manufacturing base, and significant investments in infrastructure and renewable energy have fueled demand for advanced rectification technologies. Additionally, its emphasis on electric vehicle manufacturing and modernization of electrical grids continues to generate robust demand for reliable rectifier systems.

Industrial rectifiers are crucial for converting AC to DC power in processes such as electroplating, welding, smelting, and power supply systems. These devices play an indispensable role in industries requiring constant and precise voltage outputs. As automation and digitization continue to expand across industrial sectors, the need for advanced power conversion equipment becomes increasingly vital. Moreover, energy efficiency regulations and carbon emission mandates are compelling industries to adopt newer rectifier technologies that minimize power loss and improve sustainability across operations.

Artificial Intelligence (AI) is driving a major transformation in the industrial rectifiers market. AI technologies are being increasingly integrated into power electronics systems to enable real-time monitoring, predictive maintenance, and system optimization. Machine learning algorithms process large volumes of operational data collected from embedded sensors to predict failures before they happen, significantly reducing downtime and maintenance costs.

AI also enhances control systems by enabling real-time adjustments based on load conditions, improving energy efficiency and output quality. Industrial rectifiers with AI capabilities can self-diagnose faults and adapt operating parameters dynamically, making them more resilient and cost-effective over time. This capability is particularly beneficial in high-load sectors such as metal processing, mining, and transportation, where even minor equipment failure can lead to substantial operational disruptions.

In smart grid environments, AI-powered rectifiers contribute to efficient energy management by helping balance supply and demand, regulating voltage levels, and preventing grid instability. These systems can also seamlessly integrate renewable energy sources by ensuring clean and stable power delivery to industrial operations. As industries accelerate digital transformation initiatives, the adoption of AI in industrial rectifiers is expected to become a defining factor for operational competitiveness and sustainability.

“In May 2024, a study titled 'Artificial Intelligence Approaches for Predictive Maintenance in the Steel Industry: A Survey' highlighted the application of AI in predictive maintenance for industrial equipment, including rectifiers. The research emphasized the use of AI methods to analyze data from industrial sensors, enabling early detection of potential failures and optimizing maintenance schedules, thereby enhancing operational efficiency in the steel industry.”

The increasing complexity of industrial operations necessitates stable and uninterrupted power sources. Industrial rectifiers are critical for converting AC to DC, ensuring smooth functionality in sectors like mining, automotive, manufacturing, and power generation. As automated production lines and electric-powered industrial tools become more prevalent, the demand for precision voltage control and uninterrupted DC power grows substantially. Additionally, the integration of renewable energy systems into traditional grids requires advanced rectification for efficient power distribution and energy stability across industrial facilities.

Industrial rectifiers involve considerable upfront costs due to their complexity, installation requirements, and custom configurations for specific industries. Beyond the capital expenditure, the maintenance of high-capacity rectifiers demands skilled technical staff and regular inspection, increasing operational expenses. For small and mid-sized enterprises, these financial barriers may delay the adoption of modern rectifier systems. Moreover, the need for continuous upgrades to stay in line with evolving power standards and safety regulations further escalates lifecycle costs.

As energy systems transition toward sustainability, industrial rectifiers serve as key enablers in bridging traditional and renewable power sources. Their ability to stabilize fluctuating inputs from solar and wind makes them integral in supporting smart grid development. Industries are increasingly adopting rectifiers that can communicate with grid systems to optimize load management and energy flow. This transition opens new avenues for companies to develop smart rectification solutions compatible with evolving grid infrastructures and environmental compliance frameworks.

The fast-paced advancement of power electronics and control systems poses a significant challenge to market players. As new technologies emerge, older rectifier models quickly become outdated, compelling businesses to invest in frequent upgrades. This not only increases R&D costs but also requires additional training for staff to operate and maintain newer models. For companies lacking sufficient resources, keeping up with technological change can become a major hindrance, affecting both productivity and market competitiveness.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping the demand dynamics in the industrial rectifiers market. Prefabricated power systems that include rectifiers are increasingly being assembled off-site, streamlining installation processes and reducing project timelines. These systems are particularly valuable in remote industrial locations or emergency setups where speed and reliability are essential. The growing emphasis on construction efficiency is expected to drive demand for compact, integrated rectifier solutions.

Advancements in Semiconductor Materials: The industrial rectifiers market is witnessing a transition from traditional silicon-based designs to more advanced materials such as silicon carbide (SiC) and gallium nitride (GaN). These materials offer superior performance in high-voltage and high-temperature environments, leading to smaller, more efficient rectifiers. With better thermal management and lower switching losses, these advanced rectifiers are becoming increasingly popular across industries demanding consistent performance and energy savings.

Emphasis on Energy Efficiency and Sustainability: Industrial facilities are under growing pressure to reduce energy consumption and carbon emissions. As a result, rectifier systems are being designed with features that minimize energy loss and support environmental compliance. These include regenerative systems that recover and reuse energy, and intelligent control modules that adjust power delivery in real-time. Such features not only support sustainability goals but also reduce operational costs over time.

Integration with Industrial Internet of Things (IIoT): Smart rectifiers embedded with sensors and connectivity features are facilitating the next generation of industrial automation. These systems enable remote diagnostics, real-time energy usage tracking, and predictive alerts, improving equipment uptime and reducing manual intervention. With the growing adoption of IIoT platforms, rectifiers are evolving from simple power converters into intelligent systems that support data-driven decision-making and factory-wide optimization strategies.

The global industrial rectifiers market is segmented based on type, application, and end-user industry. This segmentation provides deeper insight into market dynamics, enabling stakeholders to identify key growth areas and tailor their strategies accordingly. Rectifier types vary widely based on voltage ratings and phase configurations, with different formats suiting specific industrial operations. Applications range from electrochemical processes to welding and motor drives, each with unique performance requirements. Furthermore, the market serves a broad spectrum of end-users, including metal and mining, chemical processing, oil & gas, and power utilities, each contributing differently to overall market demand. A clear understanding of these segments reveals the market's structural complexity and its evolving focus areas as industries undergo digital and energy transformations.

The industrial rectifiers market comprises several key types: single-phase rectifiers, three-phase rectifiers, and multi-pulse rectifiers such as 6-pulse and 12-pulse variants. Among these, three-phase rectifiers currently dominate the market due to their superior performance in heavy-duty industrial applications. These rectifiers are widely used in sectors requiring high power output and stable DC supply, such as metal smelting and electroplating. Their ability to reduce harmonic distortion and improve power quality makes them ideal for large-scale operations.

Multi-pulse rectifiers, particularly the 12-pulse configuration, are witnessing the fastest growth in demand. This is driven by the need for energy-efficient solutions that comply with power quality standards in advanced manufacturing environments. These rectifiers help minimize Total Harmonic Distortion (THD) and are preferred in industries with strict compliance mandates and sensitive electrical infrastructure. Single-phase rectifiers continue to hold relevance in light and medium-duty applications but face slower growth due to limited scalability. The market trend reflects a clear shift towards high-efficiency and low-harmonic rectification technologies.

The primary applications of industrial rectifiers include electroplating, welding, smelting, motor drives, and power supply systems. Among these, electroplating accounts for the largest share of the market due to its extensive usage across automotive, electronics, and metal finishing industries. Consistent voltage supply and precise current control are critical in these processes, making rectifiers indispensable. The stable and reliable power delivery enabled by rectifiers directly impacts coating quality and process efficiency.

Meanwhile, smelting is emerging as the fastest-growing application segment. The global push for sustainable metallurgy and increased metal production in Asia-Pacific and Latin America has amplified demand for high-capacity rectifiers in smelting operations. These rectifiers must withstand extreme conditions and deliver high current outputs, which modern designs can increasingly support.

Applications in motor drives and power supply systems remain steady, particularly in automated manufacturing units and data centers, where reliable DC power is critical. Welding applications also continue to rely on rectifiers but face slower growth due to the adoption of alternative technologies like inverters in smaller setups.

The industrial rectifiers market caters to a broad range of end-users, including metal & mining, chemical processing, power utilities, oil & gas, and automotive & transportation. Metal and mining hold the leading share, largely due to the sector’s reliance on high-capacity electrochemical and smelting processes. Rectifiers are vital in metal extraction and purification, where consistent DC output ensures higher operational yield and efficiency.

Power utilities represent the fastest-growing end-user segment, fueled by global electrification efforts and the increasing integration of renewable energy sources. As these utilities modernize and expand grid infrastructure, the need for advanced rectification solutions to stabilize and convert power becomes critical. The deployment of smart grids and renewable power systems further enhances demand for intelligent rectifier systems with high energy efficiency and remote monitoring features.

The chemical processing industry also significantly contributes to market demand, especially in applications involving electrolysis and corrosion prevention. Oil & gas and automotive sectors show moderate but steady growth, with evolving electrification trends and investment in automation supporting rectifier adoption. The convergence of industrial electrification and digitalization is expected to reshape demand across all end-user segments.

Asia-Pacific accounted for the largest market share at 42.6% in 2024; however, the Middle East & Africa region is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2025 and 2032.

The dominance of Asia-Pacific stems from rapid industrialization, substantial investments in metal processing industries, and the presence of major manufacturing hubs, especially in China, India, and Japan. High-capacity demand from industries such as mining, automotive, and electronics fuels the adoption of advanced rectification technologies across this region. In contrast, the Middle East & Africa are experiencing surging demand driven by industrial diversification efforts, ongoing electrification projects, and infrastructure expansion in nations like Saudi Arabia, UAE, and South Africa. Rising energy consumption and increasing adoption of smart grid systems are accelerating the demand for efficient rectifiers, positioning the region as a high-growth frontier for global suppliers.

Emphasis on Automation and Industrial Modernization

North America’s industrial rectifiers market remains strong, supported by the widespread modernization of industrial facilities and robust demand from automotive and aerospace manufacturing sectors. The United States leads regional demand, driven by investments in electric vehicle infrastructure and next-generation manufacturing plants that rely on precise power control systems. The growing focus on renewable energy integration, especially solar and wind, has fueled demand for high-efficiency rectifiers capable of converting variable inputs into stable outputs. Additionally, smart manufacturing initiatives supported by government and private sector funding are pushing the adoption of rectifiers integrated with AI and IIoT capabilities, enabling predictive maintenance and real-time monitoring.

Sustainability Mandates Drive Energy-Efficient Rectifier Adoption

Europe's industrial rectifiers market is primarily driven by stringent environmental regulations and a strong commitment to energy efficiency. Germany, the UK, and France account for the majority of demand, particularly in applications such as electroplating, electric transport infrastructure, and industrial automation. As the EU prioritizes carbon neutrality goals, there is a strong push for adopting rectifiers that reduce energy loss and improve power conversion efficiency. The presence of well-established metal processing and automotive sectors further boosts the demand for advanced rectifier technologies. Moreover, retrofitting older manufacturing units with smart and sustainable electrical equipment is a major trend across Europe.

Rapid Industrial Growth and Grid Expansion Fuel Market Expansion

Asia-Pacific is the most dominant region in the global industrial rectifiers market, with China holding the largest share due to its massive industrial base, aggressive infrastructure development, and leadership in metal production. India follows with rising demand from sectors like chemicals, mining, and renewable energy. The region’s growing focus on electric mobility and high-speed railway electrification has significantly contributed to the growth of rectifier usage. Countries such as Japan and South Korea are adopting compact, high-efficiency rectifiers in smart factories, helping to drive the technological evolution of the market. Continued industrialization and government-backed energy projects will sustain long-term growth.

Growing Investments in Mining and Energy Infrastructure

South America’s industrial rectifiers market is driven by the expansion of mining and energy sectors, particularly in Brazil, Chile, and Peru. These countries have vast mineral resources and are investing heavily in advanced processing equipment, creating a steady demand for robust rectifier systems. In Brazil, industrial electrification and refinery upgrades are major contributors to market growth. The growing presence of multinational industrial firms is also boosting the adoption of modern rectification technologies. Furthermore, ongoing improvements in regional power infrastructure and electrification of rural and remote industrial sites are expected to enhance market potential over the next decade.

Diversified Economic Expansion and Smart Grid Projects Lead Growth

The Middle East & Africa region is poised for the fastest growth in the industrial rectifiers market, supported by government-led industrial diversification strategies and energy infrastructure development. Countries like Saudi Arabia and the UAE are investing in non-oil industrial projects, including metal processing, renewable energy integration, and water treatment—all of which require efficient rectification systems. Meanwhile, South Africa leads the continent in adopting modern manufacturing technologies, contributing to increased rectifier demand. The rollout of smart grids and urban electrification projects in the Gulf and Sub-Saharan regions is further elevating demand for high-performance and AI-integrated rectifier units.

China: USD 165.2 Million – Driven by large-scale industrialization, leading manufacturing capacity, and dominance in metal processing.

United States: USD 93.4 Million – Supported by widespread modernization of industrial infrastructure and investments in clean energy systems.

The global industrial rectifiers market is marked by intense competition. Numerous key players are investing in technological innovations, strategic alliances, and geographic expansion to strengthen their market positions. The demand for high-efficiency rectifiers in sectors like power utilities, manufacturing, and transportation is pushing manufacturers to enhance product performance and durability. Notably, the use of advanced semiconductor materials such as silicon carbide (SiC) and gallium nitride (GaN) is improving energy efficiency and thermal resistance, enabling the deployment of rectifiers in extreme industrial environments.

Leading players are emphasizing compact, modular designs, digital control integration, and environmentally friendly technologies to meet global sustainability standards. Additionally, emerging markets across Asia-Pacific and Latin America offer significant growth potential due to rapid industrialization and infrastructure development. The market remains fragmented, encouraging continuous innovation and collaborations to meet diverse end-user demands while differentiating offerings in a competitive landscape.

ABB Ltd.

Siemens AG

AEG Power Solutions

Fuji Electric Co., Ltd.

Diodes Incorporated

Raychem RPG Pvt. Ltd.

Dawonsys

Powercon

Spang Power Electronics

Neeltran

General Electric Company

Schneider Electric SE

Mitsubishi Electric Corporation

Eaton Corporation PLC

Rockwell Automation, Inc.

Delta Electronics, Inc.

Infineon Technologies AG

Toshiba Corporation

Emerson Electric Co.

Vishay Intertechnology, Inc.

Danfoss A/S

The industrial rectifiers market is undergoing rapid technological transformation driven by increasing demand for high-performance, energy-efficient power conversion systems. Wide-bandgap semiconductors such as silicon carbide (SiC) and gallium nitride (GaN) are revolutionizing rectifier designs. These materials allow devices to operate at higher voltages, frequencies, and temperatures, significantly improving efficiency and reducing energy losses.

Smart rectifiers integrated with IoT capabilities are becoming prevalent, offering remote monitoring, predictive maintenance, and performance analytics. These features are crucial for industrial environments requiring high uptime and operational stability. Furthermore, digital control systems are replacing analog configurations, offering precise output regulation, load management, and fault diagnostics.

Power factor correction and harmonic reduction technologies are being embedded in new rectifier systems to support compliance with global power quality standards. The shift towards miniaturization has also led to compact rectifier units suitable for constrained environments without compromising power output.

As industries transition to automation, electrification, and renewable integration, demand is growing for adaptive rectifiers that can work seamlessly with variable loads and smart grid infrastructure. Technology providers are investing in R&D to cater to evolving requirements, including durability in harsh operating conditions and customization for niche applications like electric vehicles and robotics.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In January 2024, AEG Power Solutions launched a new range of UPS systems optimized for industrial operations. The systems feature flexible phase configurations and are designed to deliver higher efficiency under variable load conditions.

In June 2023, Siemens AG rolled out IoT-enabled industrial safety solutions, incorporating digital diagnostics and centralized monitoring. These systems are tailored for environments requiring continuous power supply and real-time fault detection.

In January 2023, Fuji Electric expanded its engineering infrastructure by setting up a dedicated Plant Systems Center aimed at enhancing its capabilities in delivering custom-built rectifier systems for large-scale energy and manufacturing applications.

The Industrial Rectifiers Market Report presents a holistic analysis of global trends, market dynamics, key developments, and growth opportunities across various segments. It evaluates the market based on type, application, end-user industries, and regions, offering a granular understanding of evolving demand patterns.

By type, the market is segmented into silicon-controlled rectifiers, bridge rectifiers, and others, each serving unique use cases ranging from light-duty applications to high-voltage industrial systems. Applications such as electroplating, welding, battery charging, and power supplies represent significant demand areas due to their reliance on stable and efficient DC power conversion.

The report explores end-user industries like metals & mining, chemical processing, automotive, oil & gas, utilities, and electronics manufacturing, identifying key demand drivers and emerging use cases. Regional insights provide a comparative overview of market maturity and investment trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

Additionally, the report analyzes technological trends such as the adoption of smart rectifiers, SiC/GaN-based components, and remote monitoring systems. It also addresses the regulatory and environmental landscape influencing product innovation and design. By providing actionable insights, the report helps stakeholders identify growth strategies, investment opportunities, and competitive advantages in a rapidly evolving market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Industrial Rectifiers Market |

| Market Revenue (2024) | USD 679.8 Million |

| Market Revenue (2032) | USD 930.4 Million |

| CAGR (2025–2032) | 4.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | ABB Ltd., Siemens AG, AEG Power Solutions, Fuji Electric Co., Ltd., Diodes Incorporated, Raychem RPG Pvt. Ltd., Dawonsys, Powercon, Spang Power Electronics, Neeltran, General Electric Company, Schneider Electric SE, Mitsubishi Electric Corporation, Eaton Corporation PLC, Rockwell Automation, Inc., Delta Electronics, Inc., Infineon Technologies AG, Toshiba Corporation, Emerson Electric Co., Vishay Intertechnology, Inc., Danfoss A/S |

| Customization & Pricing | Available on Request (10% Customization is Free) |