Reports

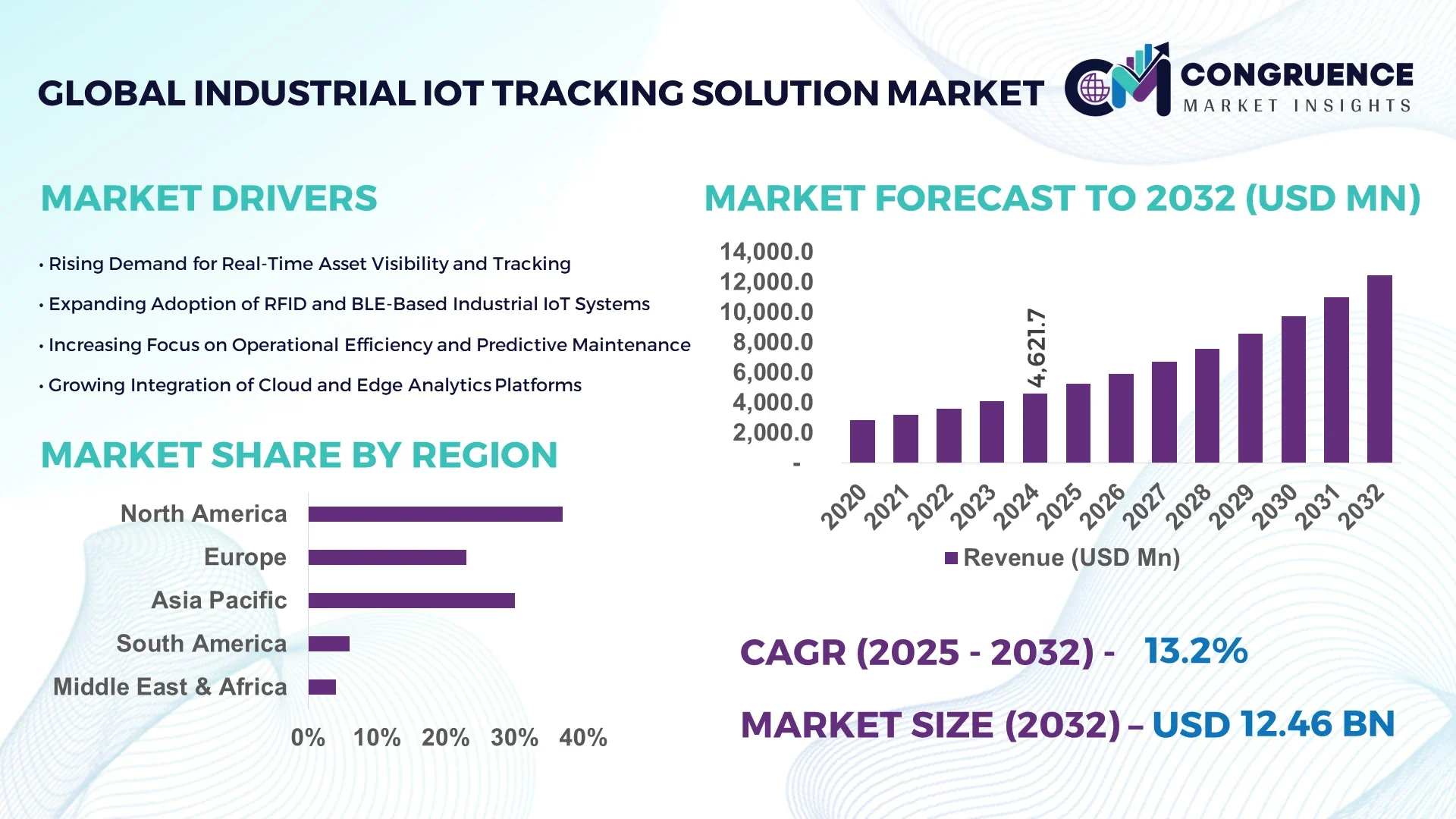

The Global Industrial IoT Tracking Solution Market was valued at USD 4,621.7 Million in 2024 and is anticipated to reach a value of USD 12,461.6 Million by 2032 expanding at a CAGR of 13.2% between 2025 and 2032. This rise is driven by accelerating demand for real-time asset visibility across production and supply chains.

In China, manufacturers have scaled deployment of tracking sensors and cloud platforms with significant investment: industrial clusters in Guangdong and Jiangsu added over 200,000 IoT tracking nodes in 2024, and local governments allocated more than RMB 3.8 billion in smart factory funds. China’s major semiconductor fabs and auto plants integrate tracking solutions in warehousing, assembly, and logistics, with over 65% of leading electronics firms deploying end-to-end IoT tracking across 10+ sites by 2025.

Market Size & Growth: Current market value USD 4,621.7 M; projected to USD 12,461.6 M; CAGR ~13.2 %; growth fueled by demand for predictive maintenance and supply chain transparency.

Top Growth Drivers: Real-time visibility adoption (45 %), reduction in unplanned downtime (32 %), operational efficiency gains (28 %).

Short-Term Forecast: By 2028, enterprises expect up to 20 % reduction in asset idle time and 15 % improvement in throughput using tracking systems.

Emerging Technologies: Ultra-wideband (UWB) tracking, AI-enabled predictive routing, low-power BLE mesh networks.

Regional Leaders: Asia-Pacific projected USD 4,200 M by 2032 (strong industrial base); North America USD 3,600 M (early adopters); Europe USD 2,800 M (focus on standards and regulations).

Consumer/End-User Trends: Leading adopters include manufacturing, logistics, energy; trend toward “track-and-trace as service” subscriptions.

Pilot or Case Example: In 2025, a large automotive Tier-1 supplier reduced tooling misplacement incidents by 37 % via an IoT tracking pilot across 8 plants.

Competitive Landscape: Market leader holds ~18 % share; other major competitors include global automation firms, IoT platform players, RFID specialists.

Regulatory & ESG Impact: Industry mandates for traceability in critical sectors, tax incentives for IoT modernization, ESG pressure for waste reduction.

Investment & Funding Patterns: Over USD 520 M raised in IoT tracking / asset visibility startups in 2024; growing use of project finance and SaaS leasing models.

Innovation & Future Outlook: Integration with digital twin systems, convergence with blockchain-based provenance, plug-and-play sensor modules shaping new deployments.

Industrial IoT tracking solutions now target smart manufacturing, oil & gas, cold chain logistics, and utilities. Recent product innovations include self-powered wireless tags, hybrid RFID-BLE trackers, and AI routing engines. Economic drivers include rising energy costs, supply chain disruptions, and regulatory compliance. Regionally, consumption is highest in Asia and North America, with emerging growth in Latin America and MEA. Future outlook sees trends toward autonomous tracking, edge analytics, and integration with Industry 5.0 innovation.

Industrial IoT tracking solutions serve as strategic enablers of operational resilience and supply-chain agility. Enterprises deploy tracking to reduce losses, improve turnaround, and monitor compliance. For example, UWB-based tracking delivers ~25 % improvement in location accuracy compared to legacy RFID systems. Asia-Pacific dominates in volume deployment across discrete manufacturing, while North America leads in adoption depth—over 60 % of large manufacturers deploy full asset tracking networks. In the short term, by 2027, AI-driven routing and sensor fusion are expected to improve utilization rate by 18 %. Firms are committing to carbon intensity reductions—some pledge 12 % cut by 2030—by optimizing asset movements. In 2025, a semiconductor firm in Taiwan achieved 22 % reduction in material transfer delays using dynamic tracking with AI inference. The Industrial IoT Tracking Solution Market is evolving as a foundational pillar for resilient, compliant operations and sustainable growth in the digital industrial era.

Demand for precise end-to-end asset visibility, along with rising pressure on inventories and supply chain disruptions, is fueling adoption of industrial IoT tracking systems. Integration of sensors, connectivity, cloud platforms, and analytics enables real-time monitoring, predictive maintenance, and location-based services for assets across factories and logistics networks. Advances in low-power communication protocols and miniaturized tags lower barriers. Regulatory emphasis on traceability (e.g., in pharmaceuticals, food, defense) further drives adoption. Meanwhile, evolving interoperability standards and platform consolidation are reshaping vendor relationships. Market entrants focus on modular, scalable tracking offerings that integrate easily with ERP and MES systems. Demand is particularly strong in capital-intensive sectors such as automotive, aerospace, chemicals, and energy.

Industrial IoT tracking enables firms to monitor equipment, vehicles, and inventory continuously. This real-time visibility reduces asset misplacement and inventory inefficiencies; companies report up to 30 % fewer losses in pilot deployments. High-cost industries such as electronics and aerospace use tracking to reduce downtime and avoid process bottlenecks. Asset visibility also supports just-in-time operations, reduces buffer stocks, and improves logistics coordination. With transparently tracked assets, companies can detect anomalies, anticipate maintenance, and enable tighter process control—all of which strengthen ROI and justify more deployments.

Many tracking solutions use proprietary protocols, and systems from different vendors often lack seamless integration. Enterprises face expensive middleware development and data normalization costs. Legacy industrial systems may resist upgrades. Further, complex environments (e.g. harsh factories, underground mines) can degrade signal performance, raising technical integration risks. Limited battery life in tags and security concerns around connectivity also slow deployment. These technical and integration hurdles create reluctance, particularly in smaller operations with limited IT budgets.

Cold chain logistics, pharmaceutical transport, and vaccine delivery demand fine-grained location and condition monitoring. These sectors require temperature, humidity, and movement tracking in real time—creating high-value opportunities for advanced industrial IoT trackers. Ultra-low-power sensor tags and smart analytics can yield combined insights on location and condition. Vendors can differentiate by offering regulatory compliance tracking (e.g., chain-of-custody records). Emerging markets in South America, Southeast Asia, and Africa present untapped demand for cold-chain visibility in food and medical logistics—where tracking adoption remains low but critical.

Initial capital cost for tag hardware, network infrastructure, and software integration is significant. Operational costs including tag replacement, maintenance, and connectivity (SIM, LPWA) add to TCO. In many industries with tight margins, getting favorable ROI is challenging. For smaller firms, managing and scaling tracking systems adds complexity. Additionally, shifting from CAPEX to OPEX models (leasing, pay-as-you-go) is still emerging and limited. Regulatory compliance and data privacy requirements (e.g. GDPR) also impose overhead and integration burdens, slowing adoption in sensitive sectors.

• Surge in Hybrid Connectivity Integration: Adopters are combining UWB, BLE, LPWAN, and 5G to optimize coverage and power usage. Over 40 % of new tracking deployments in 2025 integrate dual-mode tags for indoor and outdoor movement. Hybrid connectivity also supports fallback switching and better reliability across phases of transport.

• AI-Powered Predictive Routing: Systems are embedding AI inference at the edge to dynamically direct asset flows. Early adopters report 12 % reduction in transit delays by rerouting based on live conditions. Predictive routing is becoming standard in high-throughput logistics plants and smart factories.

• Sensor Fusion with Environmental Monitoring: Integration of temperature, vibration, pressure, and gas sensors into location tags is gaining traction—nearly 25 % of new tracker models sold in 2025 offer multi-modal sensing. This fusion supports complex applications like pharmaceutical cold chain and chemical tanker tracking.

• Plug-and-Play, Self-Configuring Tags: Vendors are launching tags that auto-configure network parameters and self-heal topology. Adoption of self-organizing tags reached 30 % in recent pilot series. These trends reduce deployment time, training overhead, and support costs.

Market segmentation for industrial IoT tracking solutions spans type, application, and end-user classifications. Types include RFID tags, BLE trackers, UWB modules, LPWAN trackers, and hybrid sensor modules. Applications cover asset tracking, inventory control, condition monitoring, cold chain logistics, tool tracking, and vehicle fleet monitoring. End-users range from manufacturing, logistics & warehousing, energy & utilities, chemicals & petrochemicals, healthcare, and transportation. Decision-makers evaluate tradeoffs—power, range, accuracy, cost—between types and applications. For example, UWB is preferred for high accuracy in factory floors, while LPWAN suits outdoor logistics. In end-users, discrete manufacturing and logistics dominate adoption, with energy & utilities and healthcare showing growth potential as regulatory tracking requirements increase globally.

Leading type is RFID and hybrid sensor modules, currently accounting for roughly 38 % share of deployments due to cost-effectiveness and maturity. The fastest-growing type is UWB tracking modules, expanding rapidly as enterprises demand centimeter-level precision—its adoption growth outpacing others at double-digit annual rates. Other types include BLE trackers (about 22 %), LPWAN trackers (around 18 %), and multi-mode hybrid sensor modules making up the remaining share (~7 %).

In a 2024 industry report, a global electronics manufacturer used UWB tracking modules to streamline tool movement across assembly lines, reducing misplacement incidents by 28 % within six months.

The leading application is asset tracking, capturing around 34 % share, as most enterprises first address visibility of high-value assets. The fastest-growing application is cold chain & condition monitoring, supported by stricter regulatory demands and integration of sensor fusion capabilities. Other applications include inventory control, tool tracking, vehicle fleet monitoring, and tool usage analytics, contributing a combined ~30 %. In 2024, over 38 % of enterprises globally reported piloting tracking systems for logistics optimization.

In 2023, a global pharmaceutical logistics provider deployed an IoT tracking and temperature monitoring solution across its vaccine distribution, improving spoilage detection in over 120,000 shipments.

The leading end-user segment is manufacturing, accounting for ~36 % share, as factories need internal visibility on assembly assets and internal logistics. Fastest growth is in logistics & warehousing—this end-user sees rapid deployment due to e-commerce expansion and demand for last-mile visibility. Other users include energy & utilities, healthcare, transportation, and chemicals—together making up ~28 % share. In 2024, more than 38 % of large enterprises globally were actively piloting IoT tracking across logistics.

According to a 2024 Gartner report, uptake of tracking in warehouse operations rose by 22 % among top 100 logistics firms, enabling over 500 warehouses to reduce misplaced inventory incidents.

North America accounted for the largest market share at ~37% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of ~26% between 2025 and 2032.

In 2024 North America saw over 38% of IoT tracking/asset visibility device shipments, led by demand from manufacturing, logistics, and healthcare sectors. Asia-Pacific accounted for close to 26% of the total Industrial IoT Tracking Solution deployments by device-volume in 2024, with China and India contributing more than 55% of regional installations. Europe held about 24% share in device-based tracking unit adoption. Latin America and Middle East & Africa together accounted for under 10% of global device installations but showed double-digit year-on-year growth in construction and energy infrastructure investment.

How is precision tracking transforming supply chains?

North America held approximately 37% market share of global Industrial IoT Tracking Solution deployments in 2024. Key industries driving demand include manufacturing (especially automotive and aerospace), healthcare (hospital asset management), logistics & warehousing, and oil & gas. Notable regulatory changes include stricter safety and data privacy norms (e.g. more rigorous FDA tracking requirements in healthcare, SEC/OTC oversight for supply chain disclosures), and government incentives for smart manufacturing programs. Technological advancements include deployment of ultra-wideband (UWB) tags, edge-AI for latency reduction, integration of 5G-enabled connectivity and cloud-native tracking dashboards. A prominent local player is Zebra Technologies, which expanded its UWB/localization product line in 2024 to incorporate sensor fusion for tool tracking in automotive plants. There is higher enterprise adoption in healthcare & finance sectors with institutions moving to track equipment and operational assets to improve utilization and meet compliance requirements.

Why is accuracy and compliance driving innovation in tracking solutions?

Europe accounted for about 24% of global Industrial IoT Tracking Solution device deployments in 2024. Key markets include Germany (strong in automotive and machinery), United Kingdom (logistics, pharmaceuticals), and France (aerospace, energy). Regulatory bodies such as the EU’s GDPR, the European Medicines Agency, and national industrial policy (Germany’s Industrie 4.0 strategy) enforce traceability and data protection, pushing demand for explainable tracking and encrypted tagging. Emerging technologies like BLE mesh networks, UWB localization indoors, and Blockchain-backed provenance systems are being adopted. A local player, STMicroelectronics, introduced low-power tracking chipsets optimized for EU energy efficiency standards in late 2024, with 20% improvement in power consumption. Consumer behavior in Europe shows high preference for vendors offering transparent data handling, on-premises tracking options, and GDPR-compliant device firmware.

How is mass manufacturing reshaping tracking deployments?

Asia-Pacific ranked first in terms of volume of Industrial IoT Tracking Solution devices in 2024 among all regions. Top consuming countries are China, India, and Japan, which together cover over 60% of all device installations in the region. Infrastructure trends include expansion of smart factories, growth in logistics hubs, and large-scale investments in port automation. Innovation hubs in Shenzhen, Bangalore, and Tokyo are pushing locally developed hybrid trackers combining RFID, BLE, and UWB functionality. A local player, Hikvision, extended its IoT tracking offering in 2024 to include environmental sensors in cold chain logistics, implementing tracking tags that log temperature/humidity plus location for over 500,000 shipments. Consumer behavior shows strong demand tied to e-commerce, mobile AI apps, and integrated digital payment & tracking bundles; enterprises often prefer scalable cloud-based solutions.

What growth is spurred by resource sectors and digital policy?

In South America, key countries like Brazil and Argentina are beginning to adopt Industrial IoT Tracking Solutions more broadly, especially in mining, agriculture, and oil & gas. The regional market share in terms of device units is estimated at around 5-7% globally in 2024. Infrastructure trends include expansion of energy pipelines, rural cold chain corridors for food, and smart port logistics. Government incentives in Brazil include tax breaks for hardware imports and digitalization funds for agribusiness. A local firm, TOTVS, has piloted tracking-enabled logistic platforms combining GPS, BLE and condition sensors for refrigerated goods. Consumer behavior varies: enterprises in urban centers demand high accuracy and cloud dashboards; rural and remote operations focus more on durability, battery life, and offline capabilities.

How do oil & gas and infrastructure drive demand in remote regions?

Oil & gas, construction, and utilities are major demand drivers in Middle East & Africa. Countries such as UAE, Saudi Arabia, South Africa lead adoption of Industrial IoT Tracking Solutions in 2024. Technological modernization includes deployment of satellite-assisted tracking, LPWAN connectivity across deserts, and ruggedized tags for high temperature zones. Local regulations and trade partnerships (e.g., GCC standards) push for traceability in oil pipelines and urban infrastructure projects. A regionally headquartered company, DarkMatter, integrated tracking modules into logistics of energy projects. Consumer behavior shows preference for robust devices, long-life power sources, and minimal upkeep; enterprises often prioritize hardware resilience over software richness.

United States: ~38% share; dominance due to mature infrastructure, strong regulatory push, and high end-user demand in manufacturing and logistics.

China: ~25% share; strong production capacity, large scale manufacturing, and aggressive deployment of tracking solutions in both industrial and consumer sectors.

The competitive environment in the Industrial IoT Tracking Solution market is moderately fragmented, with over 40 active competitors globally offering specialized hardware, firmware, platforms, and services. The top 5 companies together hold approximately 55-60% of the global market share in terms of device deployment and enterprise contracts. Strategic initiatives include product launches of UWB and hybrid trackers, partnerships between platform providers and cloud vendors, expansion of edge-AI capabilities, and mergers among sensor manufacturers and software firms. One competitor introduced over 15 new tag designs in 2024 alone, another began global rollout of a plug-and-play asset tracing system for healthcare logistics. M&A activity is increasing: several companies acquired smaller start-ups developing niche tracking technologies to fill their solution gaps. Market positioning distinguishes players by precision (cm-level), connectivity options (BLE, LPWAN, 5G), and service models (hardware + SaaS, pay-per-asset, subscription).

Siemens

Bosch

Zebra Technologies Corporation

Siemens AG

Honeywell International Inc.

PTC Inc.

Cisco Systems, Inc.

Qualcomm Technologies, Inc.

IBM Corporation

Rockwell Automation, Inc.

Trimble Inc.

Huawei Technologies Co., Ltd.

GE Digital (General Electric Company)

Edge computing is becoming pervasive in Industrial IoT Tracking Solutions to reduce latency and enable real-time decision-making; about 45% of new systems in 2024 incorporate edge-AI modules for local filtering and anomaly detection. Ultra-wideband (UWB) technology is pushing tracking precision to centimeters indoors, especially in automotive and electronics plants where precise tool and component tracking matters. Low-power wireless protocols like BLE-Mesh, LoRaWAN, NB-IoT are gaining favor in outdoor and remote asset tracking; about 30-35% of new tags in 2024 offer LPWAN or dual-mode connectivity. Sensor fusion of environmental sensors (temperature, humidity, vibration) is becoming standard in cold chain and chemical sector tracking: nearly 25-30% of trackers shipped in 2024 included condition-monitoring sensors. Digital twin integration is rising: companies now embed tracking data into digital twin models for equipment lifecycle prediction and virtual simulations. Blockchain and distributed ledger technology are used in traceability and provenance applications, notably in pharmaceuticals and critical components manufacturing. Also, power harvesting and battery-less tag innovation is showing early pilots achieving >80% uptime in harsh outdoor environments.

• In December 2023, Qualcomm and Silicon Labs released Wi-Fi 6 modules reducing power consumption by up to 88% for IoT tracking and sensors applications. Source: www.iot-analytics.com

• In Q3 2024, Bosch partnered with AWS to deliver cloud-based analytics for industrial IoT platform users in manufacturing and logistics sectors. Source: www.bosch.com

• In August 2024, Siemens and SAP jointly launched an IIoT platform combining shop-floor data with enterprise resource planning to streamline operations in multiple factories. Source: www.siemens.com

• In Q2 2024, Tulip raised USD 50 million in Series C funding to scale its industrial IoT software platform and expand into new global customer segments. Source: tulip.co

This report covers product types (RFID tags, UWB modules, BLE trackers, LPWAN and hybrid sensor modules), applications (asset tracking, cold chain monitoring, tool tracking, inventory control, fleet monitoring, condition monitoring), and end-users (manufacturing, logistics & warehousing, healthcare, energy & utilities, transportation, chemicals). Geographic scope includes North America, Europe, Asia-Pacific, South America, Middle East & Africa. It identifies both established and emerging technologies, such as ultra-wideband localization, edge analytics, sensor fusion, cloud-native dashboards, digital twins, blockchain provenance, and low-power hybrid connectivity. The report addresses regulatory / compliance drivers including traceability obligations, data privacy, environmental regulations, and incentives for smart manufacturing. It also maps recent investment funding, pilot case studies, and emerging market segments such as cold chain, precision tools tracking, wearable operator safety, and rural infrastructure deployments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4,621.7 Million |

|

Market Revenue in 2032 |

USD 12,461.6 Million |

|

CAGR (2025 - 2032) |

13.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Zebra Technologies, STMicroelectronics, Hikvision, Siemens, Bosch, Zebra Technologies Corporation, Siemens AG, Honeywell International Inc., PTC Inc., Cisco Systems, Inc., Qualcomm Technologies, Inc., IBM Corporation, Rockwell Automation, Inc., Trimble Inc., Huawei Technologies Co., Ltd., GE Digital (General Electric Company) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |