Reports

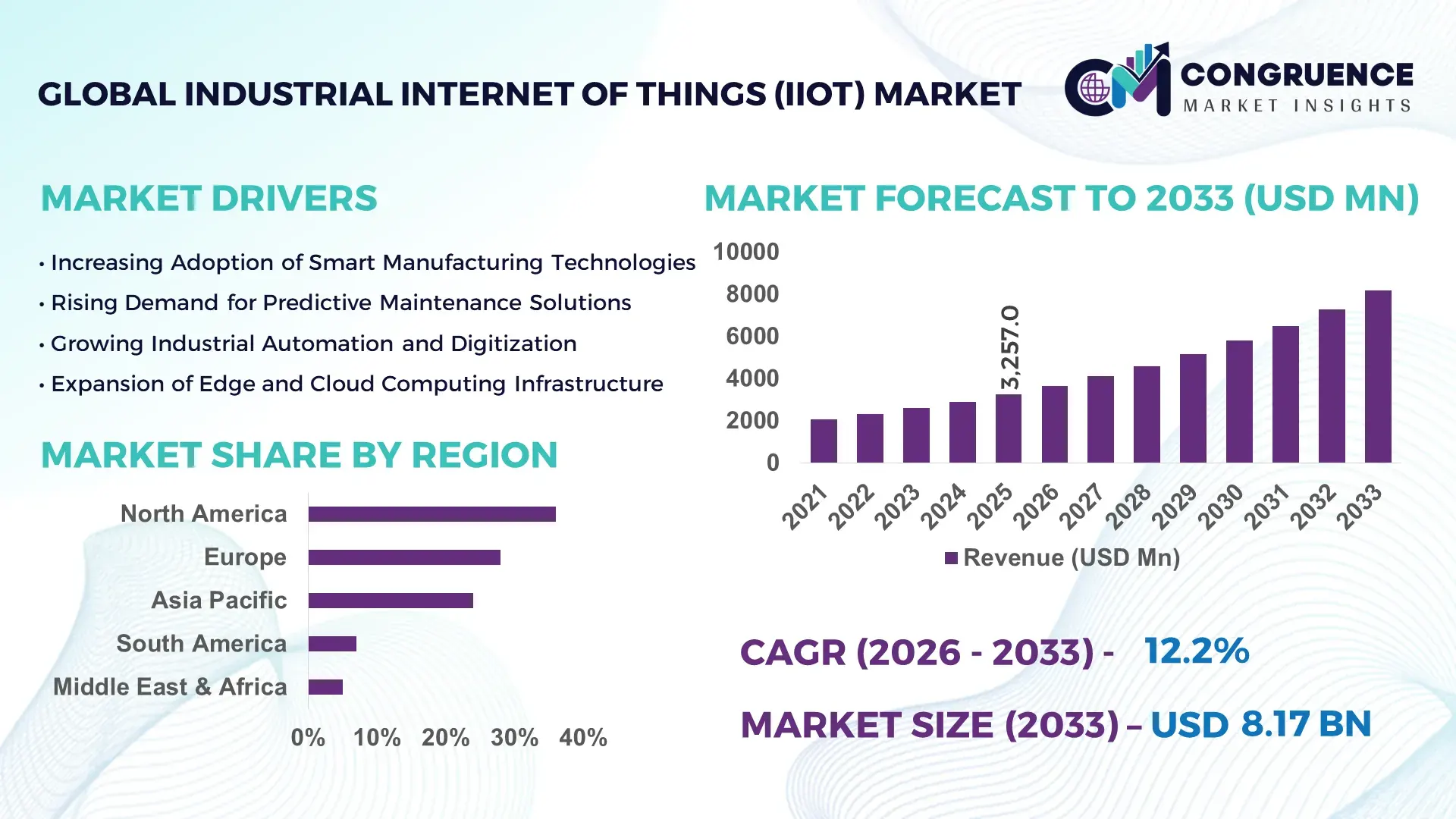

The Global Industrial Internet of Things (IIoT) Market was valued at USD 3,257.0 Million in 2025 and is anticipated to reach a value of USD 8,168.5 Million by 2033 expanding at a CAGR of 12.18% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by accelerated industrial automation, rising deployment of smart sensors across manufacturing plants, and increasing integration of AI-driven predictive maintenance systems to optimize asset utilization and reduce operational downtime.

The United States leads the Industrial Internet of Things (IIoT) Market in terms of production capacity and technology deployment. Over 72% of large manufacturing enterprises in the country have adopted connected asset monitoring systems, while more than 65% of energy and utility providers utilize real-time IIoT-enabled grid management platforms. The U.S. manufacturing sector operates over 12 million smart sensors across automotive, aerospace, and oil & gas facilities. Annual industrial automation investments exceed USD 25 billion, with significant funding directed toward edge computing, 5G-enabled factory networks, and cybersecurity frameworks. Industrial robotics density in the U.S. surpassed 285 robots per 10,000 employees in 2025, reflecting strong alignment between IIoT integration and advanced manufacturing initiatives.

Market Size & Growth: USD 3,257.0 Million in 2025, projected to reach USD 8,168.5 Million by 2033, expanding at 12.18% CAGR due to rapid digital transformation across manufacturing and energy sectors.

Top Growth Drivers: 68% predictive maintenance adoption, 52% efficiency gains from real-time analytics, 47% reduction in unplanned downtime.

Short-Term Forecast: By 2028, IIoT-based asset monitoring is expected to reduce operational costs by 22% across large-scale manufacturing facilities.

Emerging Technologies: AI-driven edge analytics, 5G-enabled industrial connectivity, digital twin modeling platforms.

Regional Leaders: North America projected above USD 2,950 Million by 2033 with strong smart factory penetration; Europe above USD 2,300 Million driven by Industry 4.0 mandates; Asia-Pacific above USD 2,100 Million fueled by high-volume electronics manufacturing.

Consumer/End-User Trends: 64% of manufacturers prioritize cloud-based IIoT dashboards; 58% energy firms deploy smart metering and grid automation.

Pilot Example: In 2025, a smart refinery project reduced maintenance-related downtime by 31% using AI-enabled IIoT sensors.

Competitive Landscape: Market leader holds ~18% share; key competitors include Siemens, ABB, Cisco, IBM, and Schneider Electric.

Regulatory & ESG Impact: 40% of industrial firms align IIoT investments with carbon reduction targets; digital monitoring supports 18% average energy savings.

Investment Patterns: Over USD 18 billion invested globally in industrial automation and smart infrastructure projects in 2025.

Innovation & Outlook: Expansion of interoperable platforms, cyber-secure edge devices, and autonomous operations shaping future scalability.

Manufacturing contributes approximately 34% of IIoT deployments, followed by energy & utilities at 22% and oil & gas at 18%. Recent innovations include AI-powered anomaly detection reducing defect rates by 27% and low-power wide-area networks improving remote asset connectivity by 35%. Regulatory emphasis on energy efficiency and emissions monitoring drives 20% higher adoption in Europe, while Asia-Pacific records 30% higher sensor installations in electronics manufacturing hubs.

The Industrial Internet of Things (IIoT) Market has become a strategic pillar for operational resilience, cost optimization, and regulatory compliance across asset-intensive industries. Organizations integrating AI-enabled predictive maintenance platforms report up to 40% reduction in unplanned downtime and 25% improvement in asset life cycles. Edge computing delivers 35% faster processing compared to traditional centralized cloud-only architectures, enabling real-time decision-making on factory floors.

North America dominates in deployment volume, while Europe leads in structured Industry 4.0 adoption with over 62% of large enterprises implementing connected production lines. By 2028, AI-powered digital twin technology is expected to improve production efficiency by 28% across automotive and aerospace facilities. Firms are committing to ESG metrics, including 30% energy consumption reduction targets by 2030 through smart metering and automated process optimization.

In 2025, Germany achieved a 26% productivity improvement in select smart factories through integrated robotics and IIoT analytics platforms. Comparatively, 5G-enabled private industrial networks deliver 45% lower latency compared to traditional Wi-Fi systems, significantly improving robotic precision and autonomous guided vehicle performance.

The Industrial Internet of Things (IIoT) Market is positioned as a long-term enabler of intelligent operations, regulatory transparency, and sustainable industrial transformation, reinforcing its role as a foundation for digital-first manufacturing ecosystems worldwide.

The Industrial Internet of Things (IIoT) Market is shaped by rapid digital transformation across manufacturing, oil & gas, power generation, transportation, and logistics. Increasing deployment of smart sensors—estimated at over 15 billion industrial endpoints globally—continues to expand the connected industrial ecosystem. Integration of AI-driven analytics platforms has improved predictive accuracy in maintenance operations by nearly 30%. Government-backed Industry 4.0 programs in Germany, China, and the United States support smart factory investments exceeding USD 50 billion collectively. Additionally, over 60% of global manufacturers prioritize operational visibility and remote monitoring solutions. Cybersecurity investments in industrial environments have grown by 20% year-on-year, reflecting increasing awareness of digital risks. These factors collectively influence supply chain modernization, energy efficiency mandates, and competitive differentiation strategies across sectors adopting IIoT solutions.

Predictive maintenance has become a central growth catalyst for the Industrial Internet of Things (IIoT) Market. Studies indicate that predictive maintenance reduces maintenance costs by 18–25% and decreases unexpected breakdowns by up to 45%. Over 70% of large-scale manufacturers now deploy sensor-based asset monitoring systems to collect vibration, temperature, and performance data in real time. In energy generation facilities, predictive analytics has extended turbine lifespan by nearly 20%. Automotive plants integrating AI-powered IIoT platforms have achieved 15% higher equipment effectiveness. These measurable operational gains encourage capital investment in smart devices, cloud-based monitoring dashboards, and edge analytics, accelerating industrial digitalization globally.

Cybersecurity remains a significant restraint within the Industrial Internet of Things (IIoT) Market. Industrial systems accounted for over 25% of reported cyberattacks targeting critical infrastructure in 2025. Approximately 40% of manufacturing firms identify data breaches and ransomware threats as primary barriers to IIoT adoption. Legacy equipment integration creates security gaps, with 30% of connected industrial devices lacking advanced encryption protocols. The average recovery time from industrial cyber incidents exceeds 20 days, disrupting production and supply chains. Regulatory compliance costs for cybersecurity upgrades have increased by nearly 15% annually. These risks compel enterprises to allocate additional budgets toward secure architectures, sometimes delaying deployment timelines.

The deployment of private 5G networks within industrial environments presents significant opportunity for the Industrial Internet of Things (IIoT) Market. 5G connectivity reduces latency by up to 45% and supports device densities exceeding 1 million devices per square kilometer. Smart factories leveraging 5G report 30% improvement in robotic coordination and 22% increase in data transmission efficiency. Asia-Pacific leads pilot implementations, with over 200 industrial 5G campuses operational in 2025. Enhanced connectivity enables scalable edge computing, augmented reality maintenance systems, and autonomous material handling solutions. These advancements create opportunities for platform providers, semiconductor firms, and industrial automation integrators.

Integration complexity remains a structural challenge for the Industrial Internet of Things (IIoT) Market. Nearly 48% of industrial facilities operate equipment older than 15 years, limiting compatibility with modern sensor networks. Retrofitting legacy systems increases implementation costs by approximately 20%. Interoperability issues across proprietary communication protocols affect 35% of integration projects. Skilled workforce shortages further complicate deployments, with 32% of firms reporting difficulty in hiring industrial data engineers. Extended deployment timelines—averaging 12–18 months for large facilities—impact ROI realization. These challenges require standardized frameworks, modular architectures, and comprehensive training programs to ensure scalable adoption.

AI-Integrated Predictive Maintenance Expansion (45% Accuracy Gain): AI-driven analytics platforms have improved equipment failure prediction accuracy by 45%, enabling proactive maintenance scheduling. Over 62% of heavy industries now use machine learning algorithms for anomaly detection, reducing maintenance response times by 28%. Integration with digital twins allows simulation-based diagnostics, increasing operational uptime by 32%.

Private 5G Network Deployment in Industrial Campuses (200+ Sites Operational): More than 200 industrial campuses globally deployed private 5G networks by 2025. These networks reduce communication latency below 10 milliseconds and enhance autonomous vehicle coordination efficiency by 30%. Smart port operations utilizing IIoT report 18% faster cargo handling times.

Edge Computing Adoption Surges (35% Faster Processing): Industrial edge devices process data 35% faster than centralized cloud models. Approximately 58% of enterprises deploy hybrid cloud-edge architectures to ensure real-time analytics and regulatory compliance. Energy utilities achieved 21% improvement in grid response times through distributed analytics.

Sustainability-Driven Digital Monitoring (20% Energy Savings): IIoT-enabled energy management systems reduce industrial power consumption by 20% on average. Over 50% of European manufacturers deploy carbon monitoring dashboards. Water treatment facilities integrating sensor-based analytics report 25% reduction in resource wastage.

The Industrial Internet of Things (IIoT) Market is structured across three primary dimensions: type, application, and end-user verticals. By type, the market includes hardware, software, and services, forming an integrated ecosystem that enables data capture, analytics, and operational execution. Hardware components account for a substantial installed base, with billions of connected sensors and edge devices deployed globally across factories, utilities, and transport networks. Software platforms are increasingly central to value realization, enabling AI-driven analytics, cybersecurity, and digital twin simulation. Services support integration, lifecycle management, and regulatory compliance.

From an application perspective, predictive maintenance and asset management remain dominant due to measurable reductions in downtime and operational disruptions. Energy management, supply chain optimization, and process automation are gaining momentum as sustainability targets intensify. End-user segmentation reveals manufacturing as the primary adopter, followed by energy & utilities, oil & gas, transportation, healthcare, and aerospace. Adoption intensity exceeds 60% among large enterprises in developed economies, reflecting strong digital transformation mandates.

Hardware represents the leading segment, accounting for approximately 44% of total adoption, supported by widespread deployment of industrial sensors, programmable logic controllers (PLCs), gateways, and edge computing devices. Software platforms contribute around 34%, while services account for the remaining 22%. While hardware leads in installed volume, software solutions are expanding faster at an estimated 14.5% CAGR, driven by AI-based analytics, cybersecurity modules, and cloud-edge orchestration platforms. Comparatively, hardware holds 44% of adoption, software 34%, and services 22%. However, software-based analytics and digital twin platforms are projected to surpass 40% adoption by 2033 due to demand for predictive intelligence and operational visualization. Services remain essential for system integration, accounting for over 60% of enterprise-level deployment contracts involving multi-site rollouts.

Predictive maintenance leads the application landscape with nearly 33% share, primarily due to its ability to reduce equipment failure rates by up to 45% and extend machinery lifespan by approximately 20%. Asset tracking and management follow at 24%, while energy management systems account for 18%. Supply chain and logistics optimization, along with quality monitoring and automation, collectively contribute 25%. While predictive maintenance accounts for 33% of adoption and asset tracking 24%, energy management is expanding fastest at 15.2% CAGR, driven by regulatory energy efficiency mandates and carbon reduction initiatives. In 2025, more than 41% of global enterprises reported piloting IIoT-enabled predictive analytics within core production operations. Additionally, 38% of manufacturers globally are integrating IIoT dashboards into enterprise resource planning systems to enhance supply chain transparency.

Manufacturing remains the dominant end-user segment with approximately 38% share, reflecting extensive adoption of smart factory systems, robotics integration, and real-time analytics. Energy & utilities follow with 21%, while oil & gas account for 17%. Transportation & logistics contribute 12%, and healthcare & pharmaceuticals collectively represent 12%. While manufacturing leads at 38% and energy & utilities at 21%, the utilities segment is expanding fastest at an estimated 13.9% CAGR, supported by smart meter rollouts and grid modernization programs. Over 60% of global oil refineries utilize IIoT-enabled remote monitoring systems, while 42% of transportation operators deploy real-time fleet telematics integrated with predictive analytics. In 2025, approximately 39% of large healthcare institutions tested connected monitoring devices linked to centralized data platforms.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.6% between 2026 and 2033.

Europe holds approximately 28% share, supported by Industry 4.0 frameworks. Asia-Pacific contributes 24%, driven by high-volume electronics and automotive production. South America accounts for 7%, while Middle East & Africa represent 5%. Over 65% of North American manufacturers deploy connected production systems, whereas Asia-Pacific hosts more than 45% of newly installed industrial robots globally.

North America holds 36% market share, driven by aerospace, automotive, and oil & gas sectors. Over 70% of large manufacturers deploy predictive maintenance systems. Federal digital infrastructure programs encourage smart grid expansion. Robotics density exceeds 285 units per 10,000 workers. A leading automation provider expanded AI-driven control systems across 200 facilities in 2025. Enterprise adoption remains highest in healthcare and financial industrial analytics integration.

Europe commands 28% share, led by Germany, the UK, and France. Over 62% of large enterprises deploy connected manufacturing platforms. Carbon neutrality mandates push 30% energy reduction commitments by 2030. Robotics density in Germany exceeds 400 per 10,000 workers. Regulatory frameworks drive explainable AI deployment across 55% of factories.

Asia-Pacific accounts for 24% share and ranks fastest in installation volume. China, Japan, and India lead adoption. Over 45% of global industrial robot installations occur in this region. Electronics manufacturing plants deploy 30% more connected sensors compared to global averages. Smart city and 5G initiatives enhance industrial connectivity.

South America represents 7% share, led by Brazil and Argentina. Mining and energy contribute over 50% of IIoT deployments regionally. Government-backed infrastructure upgrades support digital oilfield investments. Over 35% of refineries integrate smart monitoring platforms.

Middle East & Africa account for 5% share. UAE and Saudi Arabia invest heavily in smart oilfield technologies. Over 60% of upstream operations deploy remote monitoring systems. Construction digitization and smart port projects enhance regional connectivity.

United States – 34% Market Share: High industrial automation density and strong smart manufacturing adoption.

China – 22% Market Share: Large-scale electronics and automotive production with extensive sensor deployment.

The Industrial Internet of Things (IIoT) Market is moderately consolidated, with the top five players accounting for approximately 52% of total market presence. Over 150 active global competitors operate across hardware, software, and system integration segments. Market leaders focus on AI-enabled analytics platforms, private 5G solutions, and cybersecurity-enhanced industrial gateways. Strategic partnerships between telecom operators and automation providers increased by 18% in 2025. More than 40 product launches were recorded in edge computing and digital twin segments. Mergers and acquisitions activity rose by 12%, primarily targeting cloud-based analytics startups. Innovation intensity remains high, with 30% of firms investing in R&D for interoperable industrial protocols and low-power sensor networks.

ABB Ltd.

Schneider Electric SE

Cisco Systems, Inc.

IBM Corporation

Rockwell Automation, Inc.

Honeywell International Inc.

General Electric Company

Emerson Electric Co.

Bosch Rexroth AG

Mitsubishi Electric Corporation

SAP SE

Intel Corporation

The Industrial Internet of Things (IIoT) Market integrates advanced sensing, connectivity, analytics, and automation technologies. Over 15 billion industrial IoT devices are connected globally, generating petabytes of operational data daily. Edge computing nodes reduce latency below 20 milliseconds, supporting mission-critical robotics and automated guided vehicles. AI-powered anomaly detection models improve fault prediction accuracy by up to 45%. Digital twin platforms simulate production processes with 30% improved optimization efficiency. Private 5G networks support device densities exceeding 1 million per square kilometer. Blockchain-based industrial ledgers enhance supply chain transparency, reducing documentation errors by 18%. Low-power wide-area networks extend remote asset connectivity up to 15 kilometers. Cybersecurity frameworks incorporating zero-trust architectures reduce breach risks by 25%. These technological advancements collectively enhance operational intelligence and resilience.

• In February 2026, Siemens AG unveiled Digital Twin Composer, a new Industrial Metaverse platform that combines real-time IIoT data, AI, simulation, and high-fidelity 3D digital twin environments enabling manufacturers to detect up to 90% of potential manufacturing issues before physical production begins. This solution enhances design cycles, improves virtual decision-making, and integrates plant operational data into a unified digital context. Source: www.news.siemens.com

• In February 2025, Siemens Digital Industries Software announced it was named a Leader in the IDC MarketScape: Worldwide Industrial IoT Platforms and Applications 2024 vendor assessment, highlighting the strength of its Insights Hub™ IIoT platform for delivering real-time operational insights and smarter decision-making across industrial environments. Source: www.news.siemens.com

• At Automation Fair® 2025 in November, Rockwell Automation, Inc. announced over 30 new technologies, including the OptixEdge™ Advanced Edge Gateway Solution for enhanced IIoT data collection and decision-making at the machine level, plus next-generation ControlLogix® 5590 controllers and modular PointMax™ I/O systems to support digital transformation in industrial operations. Source: www.rockwellautomation.com

• In December 2025, Rockwell Automation reported being recognized across 20 Gartner® Hype Cycles for 2025 spanning manufacturing, AI, cybersecurity, and edge computing—affirming strategic relevance of its IIoT and connected enterprise technologies in multiple industrial use cases. Source: www.rockwellautomation.com

The Industrial Internet of Things (IIoT) Market Report provides comprehensive coverage of hardware, software, and services segments, encompassing sensors, gateways, analytics platforms, cybersecurity solutions, and system integration services. The report analyzes applications including predictive maintenance, asset tracking, energy management, digital twin modeling, and supply chain optimization across manufacturing, oil & gas, energy & utilities, aerospace, automotive, pharmaceuticals, mining, and transportation sectors.

Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed country-level insights for the United States, China, Germany, Japan, India, Brazil, and UAE. The study evaluates over 150 active market participants and assesses competitive positioning, strategic initiatives, and innovation trends. Technology coverage includes AI-driven analytics, private 5G connectivity, edge computing, blockchain integration, and advanced robotics interoperability. The report also examines regulatory frameworks, ESG-driven energy efficiency mandates, cybersecurity standards, and industrial digital transformation policies shaping enterprise adoption across more than 25 industrial verticals globally.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,257.0 Million |

| Market Revenue (2033) | USD 8,168.5 Million |

| CAGR (2026–2033) | 12.18% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Siemens AG; PTC Inc.; Hitachi, Ltd.; ABB Ltd.; Schneider Electric SE; Cisco Systems, Inc.; IBM Corporation; Rockwell Automation, Inc.; Honeywell International Inc.; General Electric Company; Emerson Electric Co.; Bosch Rexroth AG; Mitsubishi Electric Corporation; SAP SE; Intel Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |