Reports

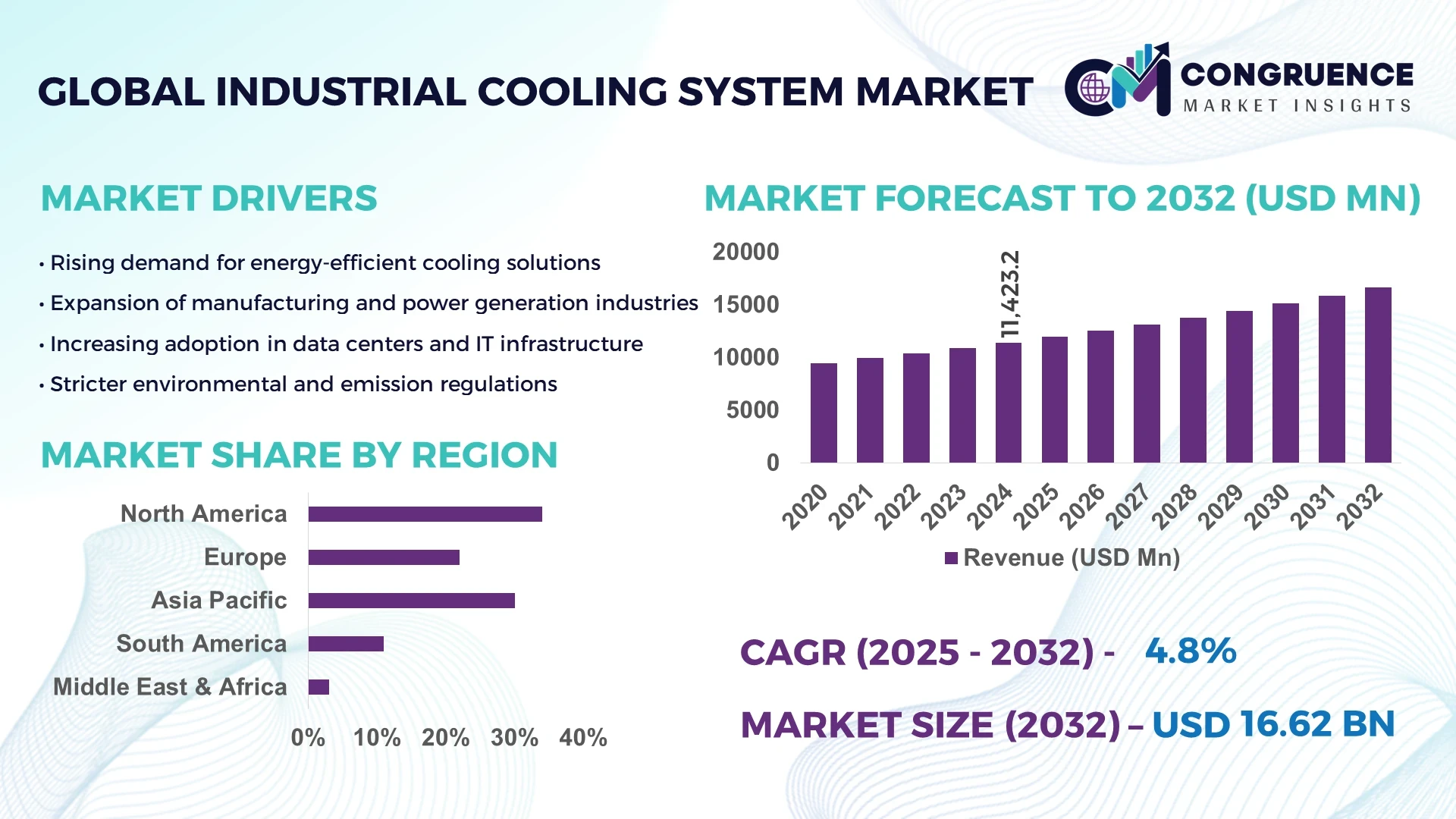

The Global Industrial Cooling System Market was valued at USD 11423.2 Million in 2024 and is anticipated to reach a value of USD 16621.79 Million by 2032 expanding at a CAGR of 4.8% between 2025 and 2032.

Germany has established itself as a powerhouse in industrial cooling solutions, boasting expansive production capacity in advanced cooling towers and chillers. The nation continually escalates capital investment in high-efficiency industrial thermal systems, deploying its technology across automotive manufacturing, chemical processing, and heavy engineering. German firms emphasize cutting-edge control automation, modular system designs, and eco-friendly refrigerants to support stringent performance standards and environmental compliance.

Industrial Cooling System Market dynamics revolve around key sectors such as utility and power generation, pharmaceuticals, chemical processing, and data center cooling. Utility and power applications demand extensive water-cooled systems to manage continuous high-load thermal dissipation, while pharmaceuticals emphasize precision and temperature stability. Recent innovations include hybrid and liquid cooling, waste-heat recovery integration, IoT-enabled remote monitoring, variable speed drives enhancing COP, and low-GWP refrigerant adoption. Regulatory pressures and environmental mandates are steering manufacturers toward sustainable, energy-efficient cooling architectures. Regionally, North America maintains substantial consumption, buoyed by data-center and digital infrastructure, while Asia Pacific exhibits the fastest expansion thanks to rapid industrialization and diverse manufacturing sectors. Emerging trends such as immersion and modular direct-to-chip cooling, AI-enabled adaptive systems, and heat-reuse frameworks indicate a future where tailored, intelligent cooling solutions become the norm for industrial decision-makers and engineering professionals.

The Industrial Cooling System Market is increasingly shaped by artificial intelligence, redefining performance benchmarks for reliability and operational efficiency. AI-enabled systems now interpret real-time operational data streams using deep learning algorithms—such as LSTM models—to dynamically regulate thermal parameters and avert overheating, thus substantially improving energy usage. AI-driven diagnostics and predictive maintenance have become integral; systems now anticipate component degradation, optimizing service schedules and minimizing downtime. The U.S. market is pivoting toward IoT-enabled, AI-driven cooling systems, enabling precise thermal control, reduced latency in monitoring, and tangible cost savings across manufacturing facilities and smart factories.

Data center operators, confronting surging computational loads, adopt AI cooling frameworks to manage dense, high-heat environments. AI and automation deliver enhanced thermal management in hyperscale facilities, aligning cooling response with fluctuating rack-level demands, and yielding sustainable outcomes. AI-ready reference architectures co-developed by infrastructure leaders now support server racks drawing over 130 kW, achieving up to 20% reduction in cooling energy consumption while accelerating project timelines by nearly one-third. Offline reinforcement learning systems, applied in real-world large-scale operations, demonstrate energy reductions between 14% and 21% without compromising safety or operational constraints. Together, these advances position AI not as a luxury but as a critical, strategic driver of efficiency and resilience within today’s Industrial Cooling System Market.

“2025: In production data-center environments, a physics-informed offline reinforcement learning framework delivering closed-loop control of air-cooling units achieved 14–21% energy savings over 2000 operational hours, maintaining safety and operational constraints.”

The Industrial Cooling System Market is characterized by continuous technological advancements, evolving regulatory frameworks, and increasing demand across diverse sectors such as power generation, chemicals, pharmaceuticals, and data centers. Heightened industrialization in emerging economies has accelerated adoption, particularly for high-capacity cooling towers and advanced chillers designed to optimize thermal efficiency. Sustainability is becoming a central theme, with industries investing in low-emission refrigerants, closed-loop cooling solutions, and energy-efficient systems to comply with environmental standards. Rising heat loads from hyperscale data centers and the rapid growth of electric vehicle battery manufacturing facilities are further influencing the trajectory of the market. As global industries prioritize efficiency, reliability, and environmental compliance, the Industrial Cooling System Market is expected to transform into a more technology-driven and adaptive sector in the coming years.

Growing emphasis on energy efficiency is a pivotal driver in the Industrial Cooling System Market, as industries aim to reduce operational costs while meeting strict environmental regulations. Industrial facilities are increasingly deploying advanced cooling systems equipped with variable speed drives, high-efficiency motors, and smart controls that deliver measurable reductions in energy consumption. For instance, advanced hybrid cooling towers and liquid cooling technologies are achieving energy savings of up to 20% in large-scale applications. In power plants, efficient closed-loop cooling designs help mitigate water consumption, while in data centers, AI-integrated systems optimize cooling loads dynamically. This push for sustainability and cost control positions energy-efficient cooling technologies as central to the market’s future expansion.

The Industrial Cooling System Market faces restraints due to the significant upfront capital required for installation and modernization of large-scale cooling infrastructure. Cooling towers, chillers, and advanced liquid cooling units demand substantial financial outlays, particularly when integrating smart monitoring technologies and low-GWP refrigerants. Smaller manufacturers and mid-sized facilities often delay adoption, preferring to extend the life of existing systems to manage costs. Additionally, high installation and maintenance expenses in sectors such as petrochemicals and steel manufacturing limit widespread implementation. This financial barrier can slow the pace of innovation adoption, creating disparities between regions with strong capital resources and those constrained by limited budgets.

The rapid global expansion of hyperscale data centers presents a significant opportunity for the Industrial Cooling System Market. Increasing reliance on cloud computing, AI applications, and 5G networks has led to exponential growth in data traffic, demanding advanced cooling solutions to manage high-density heat loads. Immersion cooling, direct-to-chip liquid cooling, and modular cooling units are being rapidly deployed to meet the evolving requirements of digital infrastructure. By 2025, data centers worldwide are projected to consume nearly one-fifth of total electricity in some regions, amplifying the need for highly efficient cooling systems. Manufacturers focusing on sustainable, high-performance cooling solutions are well-positioned to capitalize on this opportunity, especially in Asia Pacific and North America.

Stringent environmental standards and compliance requirements pose an ongoing challenge to the Industrial Cooling System Market. Regulatory bodies worldwide are enforcing restrictions on high-GWP refrigerants, water-intensive cooling methods, and emissions from cooling towers. Manufacturers must invest heavily in research and development to transition toward environmentally friendly refrigerants and closed-loop water-saving systems. Compliance costs increase significantly for companies operating in multiple jurisdictions, where differing environmental laws demand system customization. In addition, industries must ensure ongoing monitoring and reporting to remain compliant, which increases operational complexity. These challenges create pressure on both established players and new entrants, forcing continuous adaptation in technology and business models.

• Rise in Modular and Prefabricated Construction: Modular and prefabricated construction is reshaping the Industrial Cooling System Market, as industries increasingly adopt off-site manufacturing of cooling units and components. Prefabricated cooling towers, chiller modules, and piping assemblies reduce project installation timelines by nearly 30% while minimizing on-site labor dependency. Europe and North America are at the forefront, where demand for precision-built cooling units aligns with strict regulatory and energy-efficiency requirements. This trend supports scalability, as modular systems can be easily expanded to meet industrial growth without extensive downtime.

• Adoption of Low-GWP Refrigerants: Environmental regulations are driving the transition toward low global warming potential (GWP) refrigerants, influencing industrial cooling manufacturers to redesign equipment. By 2024, a majority of new chiller installations in advanced economies shifted to R-32 and other eco-friendly refrigerants, achieving emissions reductions of up to 70% compared to legacy systems. This shift reflects both environmental compliance and growing corporate sustainability commitments. Industries such as chemicals and pharmaceuticals are particularly active in upgrading their systems to maintain regulatory alignment while lowering operational risks tied to outdated refrigerants.

• Integration of IoT and Remote Monitoring: The integration of IoT-enabled sensors and real-time monitoring platforms has become a defining trend in the Industrial Cooling System Market. Intelligent cooling systems equipped with remote diagnostics are achieving 15–20% reductions in unplanned downtime by predicting failures before they occur. Operators can now monitor energy consumption, water usage, and temperature fluctuations remotely, enabling data-driven decision-making. Industrial plants, data centers, and utilities are particularly investing in these systems, as the ability to automate cooling responses directly enhances efficiency and operational reliability.

• Expansion of Immersion and Liquid Cooling in Data Centers: The accelerating growth of data centers has boosted adoption of immersion and liquid cooling solutions. With rack densities surpassing 100 kW in hyperscale facilities, traditional air-cooling methods are no longer sufficient. Immersion cooling reduces energy usage by nearly 40% compared to conventional techniques while extending hardware lifespans. This trend is expanding rapidly in Asia Pacific and North America, where rising demand for cloud computing and AI workloads is fueling investments in advanced cooling technologies. Manufacturers are responding with customizable liquid cooling systems tailored to the unique thermal loads of next-generation IT infrastructure.

The Industrial Cooling System Market is segmented by type, application, and end-user, each reflecting unique growth patterns and industrial requirements. By type, the market spans cooling towers, chillers, air cooling, and liquid cooling systems, with certain categories dominating due to their efficiency and scalability. By application, industries such as power generation, chemical processing, pharmaceuticals, and data centers are key drivers, each requiring tailored cooling strategies to manage thermal loads. By end-user, sectors including manufacturing, utilities, and IT infrastructure represent the major demand clusters, with data centers emerging as a significant high-growth segment. This segmentation highlights the diversity of industrial requirements and demonstrates how technological innovation and regulatory factors shape adoption across industries.

Cooling towers continue to lead the Industrial Cooling System Market, primarily due to their widespread use in power plants, petrochemical complexes, and large-scale manufacturing facilities. Their capacity to handle extensive heat loads while ensuring operational stability has made them the most dominant type across industrial settings. Chillers, on the other hand, represent the fastest-growing segment, fueled by rising demand in pharmaceuticals, food and beverage industries, and high-tech manufacturing. The adoption of energy-efficient chillers with advanced control systems is further accelerating their growth. Air cooling systems hold relevance in smaller facilities where cost-effectiveness and simplicity are valued, although their adoption is limited in heavy industries. Liquid cooling systems, particularly for data centers, are gaining traction as they support high-density heat loads with significant efficiency. Each type fulfills a unique role, but the ongoing shift toward sustainable and energy-efficient technologies is ensuring strong momentum for chillers and liquid cooling solutions in the coming years.

Power generation remains the leading application area within the Industrial Cooling System Market, driven by the constant need for large-scale thermal management in thermal, nuclear, and renewable plants. Cooling systems ensure consistent operational safety, efficiency, and compliance with regulatory frameworks governing emissions and water use. Data centers are the fastest-growing application segment, as hyperscale facilities expand globally to support cloud computing and AI-driven workloads. Their demand for precision cooling technologies, including liquid and immersion cooling, continues to accelerate investments in advanced systems. Chemical processing industries rely heavily on cooling for stability in reaction processes, while pharmaceuticals prioritize highly controlled environments for production and storage. Food and beverage industries also employ cooling systems to maintain quality and safety standards. Collectively, applications are diversifying, but the surge in digital infrastructure has shifted market momentum toward advanced, intelligent cooling technologies.

Manufacturing industries represent the leading end-user segment in the Industrial Cooling System Market, supported by widespread demand across automotive, steel, and chemical sectors. Their reliance on large-capacity cooling towers and chillers positions them as the primary users of industrial cooling technologies. Data centers, however, are emerging as the fastest-growing end-user, driven by exponential growth in digitalization, AI-driven processes, and cloud computing. With increasing rack densities and energy demands, they require highly efficient cooling solutions to maintain operational integrity and sustainability. Utilities and power plants also contribute significantly, deploying cooling systems to maintain efficiency in electricity generation. Pharmaceutical and food sectors adopt more specialized cooling systems to ensure compliance with strict safety standards. Together, these end-users illustrate a dynamic landscape where traditional heavy industries maintain consistent demand, while digital infrastructure accelerates transformative growth in advanced cooling solutions.

North America accounted for the largest market share at 34% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

Regional dynamics are shaped by a combination of industrial expansion, digital infrastructure development, and stringent environmental regulations. While mature markets such as North America and Europe continue to lead with advanced technologies and sustainability mandates, Asia-Pacific is witnessing accelerated growth supported by large-scale industrialization in China, India, and Southeast Asia. South America and the Middle East & Africa present niche opportunities tied to energy, mining, and construction projects, supported by regional government incentives. Each geography demonstrates distinct demand patterns, with innovation and modernization playing central roles in shaping the Industrial Cooling System Market outlook globally.

Advancing Energy-Efficient Thermal Infrastructure

North America held nearly 34% of the Industrial Cooling System Market share in 2024, driven by robust demand from industries such as power generation, oil & gas, and rapidly expanding data centers. The region benefits from strong regulatory frameworks, with agencies enforcing strict energy efficiency and emissions standards that accelerate the adoption of sustainable cooling technologies. The U.S. is at the forefront, deploying AI-integrated, IoT-enabled systems across hyperscale data centers and industrial plants to optimize thermal performance. Canada’s energy-efficient infrastructure projects further reinforce regional demand. Technological transformation, including the shift toward modular cooling systems and low-GWP refrigerants, highlights North America’s leadership in advanced industrial cooling.

Driving Sustainability with Smart Cooling Solutions

Europe accounted for approximately 28% of the Industrial Cooling System Market in 2024, led by key economies such as Germany, France, and the UK. The region emphasizes stringent sustainability mandates under initiatives like the European Green Deal, which compel industries to adopt low-emission, energy-efficient cooling systems. Germany stands out with high demand from its automotive and chemical industries, while France and the UK focus on digital infrastructure expansion, spurring investments in advanced cooling for data centers. European manufacturers are integrating digital monitoring tools, hybrid cooling solutions, and eco-friendly refrigerants to align with regulatory compliance. This trend positions the region as a hub for sustainable innovation in industrial cooling technologies.

Expanding Industrial Capacity with Next-Generation Cooling Systems

Asia-Pacific represented 25% of the Industrial Cooling System Market volume in 2024, ranking as the fastest-growing region due to rapid industrialization in China, India, and Southeast Asia. China leads consumption with extensive application in power plants, steel, and electronics manufacturing, while India is witnessing accelerated adoption driven by growth in pharmaceuticals and data centers. Japan’s innovation hubs focus on liquid and immersion cooling systems for high-tech industries. Massive infrastructure development, combined with the digital transformation of manufacturing sectors, fuels demand for scalable and energy-efficient cooling solutions. The region’s emphasis on cost-effective yet technologically advanced systems positions Asia-Pacific as a strategic growth engine for global manufacturers.

Strengthening Infrastructure and Energy Sector Integration

South America captured around 7% of the Industrial Cooling System Market in 2024, with Brazil and Argentina emerging as the leading contributors. Brazil’s expanding power generation and petrochemical industries drive substantial demand for large-scale cooling towers, while Argentina supports growth through modernization of its energy and manufacturing sectors. Government incentives for infrastructure development, coupled with trade policies favoring industrial upgrades, are stimulating adoption of advanced cooling technologies. Mining and food processing industries also contribute significantly, requiring reliable systems for operational safety and efficiency. South America’s rising demand illustrates a transition toward more sustainable, cost-efficient cooling frameworks.

Transforming Energy and Construction with Advanced Cooling Technologies

The Middle East & Africa accounted for nearly 6% of the Industrial Cooling System Market in 2024, with strong demand driven by oil & gas, petrochemicals, and large-scale construction projects. Countries such as the UAE are investing heavily in high-efficiency cooling infrastructure for industrial plants and urban development, while South Africa is witnessing increased adoption across mining and manufacturing. Modernization efforts focus on integrating IoT-enabled monitoring systems and low-water cooling solutions to address regional resource constraints. Trade partnerships and government-backed initiatives supporting sustainable technology adoption further strengthen the market outlook in this region.

United States – 22%

Strong demand from hyperscale data centers and advanced manufacturing sectors drives the U.S. dominance in the Industrial Cooling System Market.

China – 18%

High production capacity in power generation and extensive application across steel and electronics industries establish China as a leading market player.

The Industrial Cooling System Market is highly competitive, with more than 150 active global and regional players operating across multiple industry verticals. Competition is shaped by a mix of established multinational corporations and specialized regional manufacturers offering tailored solutions. Market leaders focus on product innovation, sustainable refrigerant adoption, and AI-enabled systems to maintain strategic positioning. In recent years, partnerships between cooling technology providers and data center operators have accelerated, targeting the demand for scalable, energy-efficient thermal solutions. Mergers and acquisitions are also prominent, as companies consolidate capabilities to expand product portfolios and global reach. For example, joint ventures between equipment manufacturers and engineering service providers are enhancing delivery efficiency and customer service integration. Innovation trends such as liquid cooling, immersion systems, modular construction, and IoT-driven diagnostics are intensifying competition, forcing companies to differentiate through technological advancements. As industries demand lower emissions, reduced water usage, and higher operational reliability, competitive intensity continues to rise, positioning innovation and sustainability as critical differentiators in this evolving landscape.

Johnson Controls International

SPX Cooling Technologies

EVAPCO Inc.

Baltimore Aircoil Company

Daikin Industries Ltd.

Trane Technologies plc

Mitsubishi Heavy Industries Ltd.

Alfa Laval AB

Kelvion Holding GmbH

Hamon Group

The Industrial Cooling System Market is undergoing significant transformation, driven by innovations in energy efficiency, sustainability, and digital integration. Advanced cooling towers and chillers are now designed with variable frequency drives and high-efficiency motors that can reduce power consumption by 15–20% compared to legacy systems. Hybrid cooling technologies that combine wet and dry mechanisms are gaining traction, offering water savings of up to 30% while maintaining stable performance in high-load environments. Liquid and immersion cooling technologies are emerging rapidly, particularly in data centers where rack densities exceed 100 kW, enabling up to 40% reductions in cooling energy usage while improving hardware lifespan.

The integration of IoT and AI has become a cornerstone of next-generation cooling systems, enabling real-time monitoring of parameters such as temperature, humidity, and power usage. Predictive maintenance powered by machine learning reduces downtime by identifying faults before system failures occur, enhancing operational reliability. Furthermore, advancements in eco-friendly refrigerants, such as R-32 and other low-GWP variants, are reshaping equipment design to align with global environmental regulations. Modular and prefabricated systems are also streamlining deployment, reducing installation times by up to 25% in large industrial projects. Collectively, these technological advancements underscore a shift toward sustainable, intelligent, and scalable cooling systems tailored for modern industrial needs.

• In February 2023, SPX Cooling Technologies launched its Marley NC Everest Counterflow Cooling Tower with enhanced thermal performance and 60% higher cooling capacity compared to conventional towers, designed to serve high-demand power and industrial applications.

• In September 2023, Johnson Controls introduced its YORK YLAA Air-Cooled Scroll Chiller featuring low-GWP refrigerants and integrated smart controls, achieving up to 20% greater energy efficiency for commercial and industrial facilities.

• In April 2024, Daikin Industries unveiled its next-generation inverter-driven industrial chillers with modular configurations, enabling scalable deployment while reducing installation times by 30% across manufacturing and process industries.

• In July 2024, EVAPCO Inc. expanded its product portfolio with the launch of eco-friendly dry and hybrid cooling systems, offering water savings of up to 40% and meeting stringent international environmental compliance standards.

The scope of the Industrial Cooling System Market Report encompasses an extensive analysis of technologies, applications, and regional markets shaping the industry landscape between 2024 and 2032. The report evaluates multiple product categories including cooling towers, chillers, air cooling systems, and liquid cooling technologies, providing insights into their adoption patterns, operational efficiencies, and industrial relevance. Segmentation covers diverse applications such as power generation, chemical processing, pharmaceuticals, food and beverage, and data centers, each presenting unique operational requirements and growth trajectories.

Geographically, the study spans key markets across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing regional demand drivers such as infrastructure development, regulatory frameworks, and energy efficiency initiatives. The report also highlights emerging markets where industrialization and urbanization are accelerating adoption, especially in Asia-Pacific and Latin America.

The scope further extends to technological advancements including AI-driven predictive maintenance, IoT-enabled remote monitoring, hybrid and immersion cooling, and the adoption of low-GWP refrigerants. Industry professionals will also find insights into evolving business models such as modular construction and prefabrication that are reducing project timelines. By addressing both established and emerging opportunities, the report offers decision-makers a comprehensive view of the Industrial Cooling System Market’s breadth, positioning, and future direction.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 11423.2 Million |

|

Market Revenue in 2032 |

USD 16621.79 Million |

|

CAGR (2025 - 2032) |

4.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Johnson Controls International, SPX Cooling Technologies, EVAPCO Inc., Baltimore Aircoil Company, Daikin Industries Ltd., Trane Technologies plc, Mitsubishi Heavy Industries Ltd., Alfa Laval AB, Kelvion Holding GmbH, Hamon Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |