Global Implantable Insulin Pumps Market Report Overview

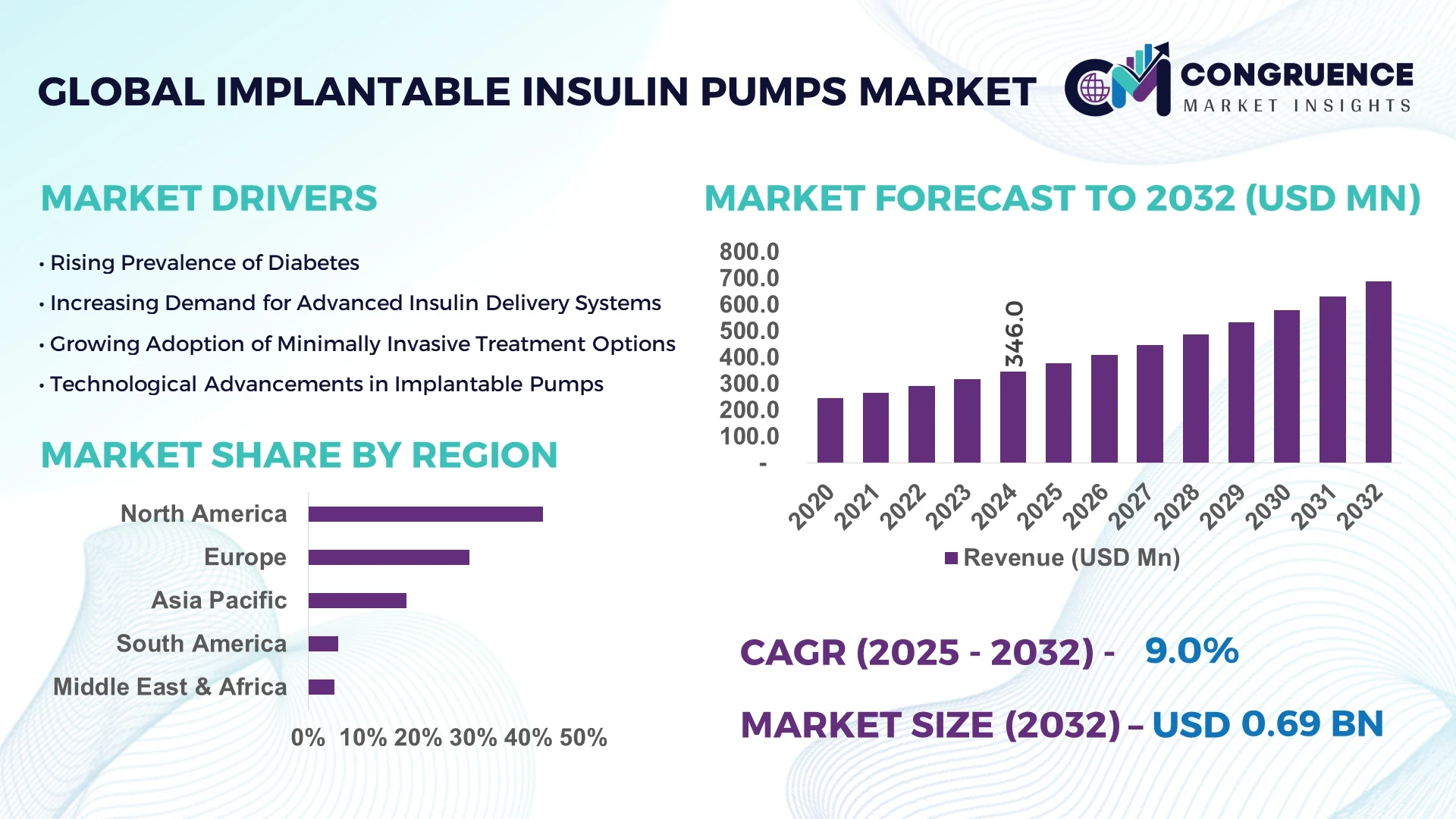

The Global Implantable Insulin Pumps Market was valued at USD 346.0 Million in 2024 and is anticipated to reach a value of USD 690.9 Million by 2032 expanding at a CAGR of 9.03% between 2025 and 2032.

The United States plays a pivotal role in the Implantable Insulin Pumps Market, with advanced R&D infrastructure, robust clinical trial networks, and consistent investment from both public and private sectors. Major medical device companies in the U.S. continue to develop cutting-edge implantable insulin delivery systems, supported by strong collaboration with top academic medical centers and federal innovation funding initiatives.

The Implantable Insulin Pumps Market has gained traction across various healthcare sectors, including endocrinology, internal medicine, and long-term diabetes management clinics. Increasing demand for continuous and automated insulin delivery systems is driving innovations that reduce patient burden and enhance glycemic control. Technological breakthroughs such as closed-loop systems, advanced biocompatible materials, and long-lasting battery life are reshaping the product landscape. Regulatory support in the form of fast-track designations and post-market surveillance is also fueling product development and commercialization. Economically, the rising global prevalence of diabetes—particularly in North America, Western Europe, and parts of Asia—has spurred consumption patterns favoring long-term, implantable solutions over traditional methods. Moreover, emerging markets are witnessing a gradual shift towards such advanced devices due to improving healthcare infrastructure. The future outlook indicates increasing focus on AI-enabled devices, patient-centric customization, and interoperable health systems integration.

How is AI Transforming Implantable Insulin Pumps Market?

Artificial intelligence (AI) is significantly transforming the Implantable Insulin Pumps Market by enhancing automation, improving glycemic prediction models, and supporting real-time insulin regulation. AI algorithms integrated into pump software now enable dynamic, predictive adjustments in insulin delivery based on biometric data, lifestyle patterns, and dietary inputs. These adaptive learning capabilities are reducing the incidence of hypoglycemic events by over 35% compared to older programmable models. Furthermore, AI enhances operational efficiency through continuous calibration and error detection, ensuring safer and more reliable delivery mechanisms.

Remote patient monitoring and AI-powered mobile applications are also influencing post-implantation care. Real-time data collected from implantable devices is analyzed using cloud-based platforms, allowing physicians to adjust treatment plans proactively. These developments minimize patient hospital visits, reduce healthcare costs, and improve adherence. AI is also being deployed in the manufacturing and testing phases, optimizing design simulations and reducing product development cycles. With AI-enabled interoperability, implantable insulin pumps are increasingly becoming integral components of comprehensive diabetes care ecosystems. The integration of voice-controlled diagnostics and AI chatbots for patient engagement further augments the market's digital shift.

"In 2025, a leading U.S.-based medtech firm introduced an AI-integrated implantable insulin pump system that demonstrated a 40% improvement in automated insulin adjustment accuracy during clinical trials. The system utilized machine learning to continuously adapt insulin delivery parameters in real time, resulting in a 25% decrease in patient-reported glycemic variability within the first three months of implantation."

Implantable Insulin Pumps Market Dynamics

The Implantable Insulin Pumps Market is witnessing rapid evolution fueled by technological advancements, increasing diabetes prevalence, and growing demand for long-term glycemic control solutions. Innovations in miniaturized device design, enhanced biocompatibility, and seamless integration with digital health platforms are reshaping clinical approaches. Patient-centric developments such as remote calibration, wireless charging, and AI-enabled feedback loops are attracting both healthcare providers and consumers. The regulatory environment has become increasingly supportive, with quicker approvals for advanced devices, especially in North America and Europe. Simultaneously, emerging economies are experiencing rising device adoption due to improving infrastructure and patient awareness. These dynamics are collectively creating an environment conducive to sustained market growth.

DRIVER:

Growing prevalence of diabetes and long-term insulin dependence

The global rise in Type 1 and Type 2 diabetes, particularly among aging populations, is significantly increasing demand for implantable insulin delivery systems. According to global health data, over 540 million people are currently living with diabetes, and this number is projected to rise sharply in the coming decade. Implantable insulin pumps offer consistent basal insulin delivery, reducing the frequency of injections and improving quality of life for chronic patients. These systems are especially beneficial for individuals with recurrent hypoglycemia or severe glycemic variability. Their ability to offer stable, long-term glycemic control has led to a surge in clinical adoption, particularly in developed regions such as North America and Western Europe. Moreover, recent advancements in patient-specific customization and real-time monitoring have increased both clinician and patient confidence in these systems.

RESTRAINT:

High initial costs and limited reimbursement coverage

One of the critical barriers affecting the growth of the Implantable Insulin Pumps Market is the high upfront cost associated with device procurement, surgical implantation, and follow-up monitoring. In many regions, especially across low- and middle-income countries, access to such advanced treatment options remains limited due to lack of reimbursement frameworks and high out-of-pocket expenditure. For example, a fully integrated implantable insulin pump system can cost up to USD 20,000 including surgical fees, which remains prohibitive for most uninsured or underinsured patients. Furthermore, uneven insurance coverage in certain markets deters patients from considering this option, particularly when alternative insulin therapies are available at lower costs. These financial constraints are slowing adoption rates, despite the long-term cost benefits of reduced hospitalizations and complications.

OPPORTUNITY:

Integration of AI and IoT for smart insulin delivery systems

The convergence of AI and Internet of Things (IoT) technologies is creating vast opportunities in the Implantable Insulin Pumps Market. AI-enabled pumps equipped with continuous glucose monitoring (CGM) sensors are now capable of learning from user behavior and adjusting insulin delivery accordingly. This development reduces manual intervention and allows for personalized diabetes management. IoT platforms allow seamless data transmission from the pump to healthcare providers, enhancing remote patient management. Several companies are investing in this space, developing systems that synchronize with mobile applications and wearable tech, offering patients comprehensive metabolic insights. In addition, remote diagnostics and predictive analytics are reducing emergency visits and enhancing treatment outcomes. This shift towards intelligent, connected care systems is expected to create long-term growth potential in both developed and developing markets.

CHALLENGE:

Complexity of regulatory approvals and device standardization

The path to regulatory approval for implantable medical devices, particularly insulin pumps, remains highly complex and time-consuming. These devices must comply with stringent safety, efficacy, and performance standards across multiple jurisdictions. Manufacturers are required to conduct extended clinical trials, biocompatibility assessments, and post-market surveillance, which can delay time-to-market by several years. Additionally, variations in standards across regions—such as the FDA in the U.S., EMA in Europe, and CDSCO in India—add to the complexity of global distribution. The lack of standardization for device interoperability and data integration further complicates development, particularly for manufacturers aiming to align with emerging AI and IoT frameworks. These regulatory and technical hurdles can be resource-intensive and discourage smaller companies from entering the market.

Implantable Insulin Pumps Market Latest Trends

-

Rise in AI-enabled personalized insulin regulation: AI-driven systems are rapidly gaining popularity in the Implantable Insulin Pumps Market for their ability to adapt insulin delivery in real time based on patient-specific data. Recent models now include machine learning algorithms that interpret glucose variability, physical activity, and dietary intake to regulate insulin levels. This personalization has improved glycemic control outcomes by over 30% in certain patient populations, especially those with brittle diabetes.

-

Advancements in wireless charging technology: Emerging innovations in wireless energy transfer are enabling next-generation implantable pumps to recharge without external leads or ports. Devices equipped with inductive and resonant charging technologies now support weekly or biweekly recharges via wearable patches. These advancements eliminate the need for surgical battery replacements and improve patient convenience, driving preference toward such systems in premium healthcare markets.

-

Expansion of minimally invasive implantation techniques: Medical technology providers are introducing new methods that allow for faster and less invasive pump implantation, including the use of robotic-assisted surgical tools and micro-incision devices. This trend is reducing procedural risk, recovery time, and associated costs, thereby improving clinician acceptance and patient adoption in outpatient and specialty care settings.

-

Integration with mobile health ecosystems: Implantable insulin pumps are increasingly being designed for seamless integration with smartphones, smartwatches, and digital health platforms. These integrations allow users and clinicians to track performance, receive alerts, and adjust settings remotely. The trend is especially pronounced in North America and Western Europe, where mobile health adoption exceeds 65% among chronic disease patients, encouraging further convergence of medical devices and digital tools.

Segmentation Analysis

The Implantable Insulin Pumps Market is segmented based on type, application, and end-user, reflecting a diverse and evolving landscape driven by technological advancement and patient-centric innovations. Product types are distinguished by delivery mechanisms and design formats, with certain models emphasizing long-term performance and others focused on adaptability. Application-wise, the market primarily serves patients with Type 1 and Type 2 diabetes, where demand is shaped by disease severity, insulin dependency, and treatment complexity. End-user segmentation spans hospitals, specialty clinics, and home care settings, with the latter gaining increasing attention due to the shift towards outpatient care and remote patient management. These segments collectively influence procurement strategies, product design, and clinical implementation, offering targeted insights for stakeholders aiming to position themselves effectively within the competitive environment.

By Type

The Implantable Insulin Pumps Market includes several product types such as fully implantable insulin pumps, semi-implantable pumps, and hybrid insulin infusion systems. Fully implantable insulin pumps represent the leading segment, primarily due to their long-term utility, reduced maintenance needs, and compatibility with closed-loop glucose monitoring systems. These devices are particularly favored in chronic Type 1 diabetes cases where sustained insulin delivery and reduced manual intervention are crucial.

The fastest-growing type is the hybrid insulin infusion system. Its rise is being propelled by advancements in AI-driven modulation, minimal surgical requirements, and the ability to operate seamlessly with external CGM devices. These systems are gaining attention among younger, tech-savvy patients seeking intelligent solutions with remote calibration features and mobile integration.

Semi-implantable pumps, while occupying a smaller share, continue to be relevant for transitional treatment plans or for patients unable to undergo full implantation. These devices often act as a stepping stone for patients considering a full implantable solution, especially in developing healthcare environments.

By Application

The primary application of implantable insulin pumps lies in the treatment of Type 1 diabetes, which accounts for the largest user base in this market. The long-term insulin dependence and complexity of glucose regulation in these patients necessitate precise and automated delivery systems. Fully implantable solutions have shown notable success in maintaining steady glycemic control, particularly in pediatric and adolescent populations where consistent insulin absorption is critical.

The fastest-growing application area is Type 2 diabetes management. This is largely driven by the global increase in obesity, sedentary lifestyles, and the shifting preference for automated insulin regulation over multiple daily injections. Moreover, patients with advanced insulin resistance or complications such as hypoglycemia unawareness are increasingly benefiting from implantable pumps.

Other applications include use in gestational diabetes cases and clinical trials for broader metabolic disorder management. While still niche, these emerging areas highlight the potential adaptability of implantable insulin delivery systems for diverse diabetic conditions and even investigational off-label uses.

By End-User Insights

Hospitals remain the leading end-user segment in the Implantable Insulin Pumps Market due to their comprehensive infrastructure, skilled personnel, and ability to handle surgical implantations and post-operative monitoring. These institutions often serve as the primary centers for device trials, initial implantation procedures, and patient training, particularly for complex cases.

The fastest-growing end-user category is home care settings. Driven by the rise of remote monitoring technologies, AI-enabled diagnostics, and patient preference for decentralized healthcare, home-based care is becoming increasingly viable. Devices with self-regulating algorithms and wireless data transmission capabilities support patient independence and ease the burden on healthcare systems. Additionally, health insurance providers are beginning to recognize the cost-effectiveness of managing chronic diabetes at home, further accelerating this trend.

Specialty diabetes clinics and outpatient surgical centers also contribute significantly to the market, providing focused expertise and convenient services for ongoing management and adjustments. These facilities are playing an increasingly important role in patient education, long-term support, and device optimization.

Region-Wise Market Insights

North America accounted for the largest market share at 42.7% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.4% between 2025 and 2032.

This regional disparity highlights the maturity of established healthcare ecosystems in North America and the rapid infrastructural and technological advancements driving growth in Asia-Pacific. While North America benefits from strong insurance coverage, high awareness, and advanced clinical practices, Asia-Pacific is gaining traction due to increasing diabetic populations, growing healthcare expenditure, and rising adoption of AI-integrated medical devices. Both regions are actively shaping the future of the Implantable Insulin Pumps Market through innovation, demand shifts, and strategic investments in digital healthcare.

North America Implantable Insulin Pumps Market

Strong Clinical Infrastructure and Technological Integration Accelerate Demand

North America held a commanding 42.7% share of the global Implantable Insulin Pumps Market in 2024, supported by well-established healthcare systems, broad access to medical technology, and favorable reimbursement frameworks. The United States continues to be the key driver within the region, with major companies developing AI-powered and remotely monitored insulin delivery systems. Hospitals and specialty diabetes centers are central to clinical adoption, while tech collaborations are accelerating innovation. Recent policy shifts allowing streamlined FDA approvals for advanced implantable devices have further opened the market. Additionally, the region's focus on personalized medicine, remote patient care, and interoperability between insulin pumps and other wearable devices has driven rapid digital transformation.

Europe Implantable Insulin Pumps Market

Advancing Through Standardization and Cross-Border Healthcare Initiatives

Europe accounted for approximately 29.3% of the Implantable Insulin Pumps Market in 2024, with Germany, the UK, and France serving as core markets. The region benefits from a highly structured regulatory environment, with the European Medicines Agency (EMA) playing a crucial role in device approvals and safety monitoring. Sustainability in healthcare and investment in digital therapeutics are also influencing the adoption of implantable insulin solutions. Initiatives under the EU Digital Health Strategy are accelerating device integration into national healthcare systems. Furthermore, European hospitals are adopting closed-loop insulin pump systems at a growing pace, especially in academic and teaching institutions, reflecting a high degree of technological openness and cross-border clinical collaborations.

Asia-Pacific Implantable Insulin Pumps Market

Rapid Urbanization and Technology Penetration Drive Expansion

Asia-Pacific is rapidly emerging as the fastest-growing region in the Implantable Insulin Pumps Market, with China, India, and Japan being the major contributors. In 2024, the region accounted for 17.8% of the global market volume. This growth is driven by rising diabetes prevalence, urban lifestyle changes, and increased healthcare spending across key economies. China and Japan are investing heavily in localized manufacturing and innovation hubs, while India is witnessing a surge in demand due to growing awareness and better insurance coverage. The region is also a hotspot for med-tech startups focused on AI-driven solutions, enabling broader access to smart insulin delivery systems in both metro and tier-2 cities. Government support for domestic manufacturing and public-private health initiatives further bolster market expansion.

South America Implantable Insulin Pumps Market

Public Health Investment and Private Sector Growth Enhance Adoption

South America represented 5.4% of the global Implantable Insulin Pumps Market in 2024, with Brazil and Argentina leading in terms of adoption. Brazil’s government initiatives to improve diabetes care infrastructure and subsidize implantable medical devices have played a pivotal role in market penetration. Argentina has followed with expanded access to specialty diabetes clinics in urban regions. Private hospitals across major South American cities are adopting newer implantable technologies, driven by rising middle-class health awareness. Additionally, telemedicine growth across the region is supporting follow-up care and remote device management. However, disparities in public healthcare funding between rural and urban areas still pose a challenge to uniform growth.

Middle East & Africa Implantable Insulin Pumps Market

Targeted Innovation and Trade Expansion Fuel Progress

Middle East & Africa accounted for 4.8% of the global Implantable Insulin Pumps Market in 2024, with UAE and South Africa at the forefront. These nations are leading due to strategic public-private healthcare partnerships and growing investments in medical technology modernization. In the UAE, the increasing prevalence of diabetes and a focus on smart hospital infrastructure have made the country an innovation hub. South Africa, on the other hand, is expanding access through regional trade incentives and healthcare digitalization. Additionally, regulatory reforms aimed at fast-tracking high-tech device approvals and enhanced trade partnerships with North American and European suppliers are facilitating growth in this geographically diverse region.

Top Countries Leading the Implantable Insulin Pumps Market

-

United States – 38.6% Market Share

Strong end-user demand, advanced manufacturing, and integration of AI in insulin delivery systems.

-

Germany – 14.2% Market Share

High production capacity, centralized healthcare policy, and proactive regulatory framework.

Market Competition Landscape

The Implantable Insulin Pumps Market features a moderately consolidated competitive landscape with approximately 20–25 active global and regional players. Leading manufacturers are focused on expanding their technology portfolios through strategic product launches, acquisitions, and cross-industry collaborations. Innovation is a key competitive factor, with firms heavily investing in AI-driven delivery algorithms, wireless recharging, and biocompatible materials that extend device longevity and reliability. Many companies are also building strategic partnerships with healthcare providers and tech platforms to integrate real-time data analytics and telemedicine features.

Mergers and acquisitions have intensified since 2023, especially among medical device companies seeking to gain foothold in high-growth markets across Asia-Pacific and Europe. Several firms are prioritizing user-friendly product interfaces and mobile compatibility to appeal to a broader patient base. Market competition is further influenced by regulatory approvals, patent portfolios, and pricing strategies tailored for both developed and emerging regions. The shift toward value-based care models and increased reimbursement support are also shaping how companies position themselves competitively across key geographies.

Companies Profiled in the Implantable Insulin Pumps Market Report

- Sooil Development Co., Ltd.

- Tandem Diabetes Care, Inc.

Technology Insights for the Implantable Insulin Pumps Market

The Implantable Insulin Pumps Market is undergoing a significant technological transformation marked by integration of AI, IoT, and advanced biosensor technologies. One of the most impactful developments is the incorporation of closed-loop insulin delivery systems, which utilize continuous glucose monitoring (CGM) sensors to automatically adjust insulin levels based on real-time data. These systems enhance glycemic control while reducing patient intervention and clinical follow-up frequency.

Wireless energy transfer technology is becoming a standard in premium devices, eliminating the need for invasive battery replacements. Current-generation devices can be charged weekly through skin-contact inductive pads, improving patient compliance and comfort. Furthermore, biocompatible polymers and nanomaterials are being introduced to enhance device durability, minimize rejection rates, and improve long-term functionality.

AI algorithms now enable predictive insulin delivery, using machine learning to analyze historical glucose trends, meal patterns, and physical activity. These adaptive systems are reducing hypoglycemia incidents and optimizing basal insulin delivery, especially in high-risk patients. Integration with mobile platforms, smartwatches, and health monitoring ecosystems has created a seamless user experience, allowing remote monitoring by healthcare professionals. The rise of telehealth has further boosted the demand for such connected systems, particularly in home care environments. These technological trends are driving greater personalization, lower operational risk, and broader clinical adoption.

Recent Developments in the Global Implantable Insulin Pumps Market

• In February 2024, Tandem Diabetes Care introduced a next-generation implantable insulin pump equipped with a wireless recharging module and AI-assisted insulin dosing. Early clinical testing showed a 32% improvement in glycemic stability among test users over three months.

• In November 2023, Medtronic unveiled a hybrid closed-loop implantable system with dual-sensor feedback, allowing real-time data syncing with smartphone apps. The new model significantly reduced manual intervention by over 40%.

• In May 2024, EOFlow announced the commercial release of its wearable and semi-implantable insulin pump in South Korea, incorporating Bluetooth-enabled CGM compatibility and enhanced battery life for weekly recharging cycles.

• In August 2023, Debiotech partnered with a European university to develop an ultra-miniaturized insulin pump system with automated self-learning algorithms, targeting pediatric diabetic patients with high insulin sensitivity variability.

Scope of Implantable Insulin Pumps Market Report

The Implantable Insulin Pumps Market Report provides a comprehensive analysis of the current and emerging dynamics across global, regional, and segment-level dimensions. The report covers product types including fully implantable pumps, semi-implantable devices, and hybrid systems, each examined for their adoption trends, functional differentiation, and clinical utility. Applications are categorized into Type 1 diabetes, Type 2 diabetes, and other niche areas such as gestational diabetes and metabolic disorder research.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting key regional developments, regulatory trends, and adoption patterns. It also profiles major end-user segments such as hospitals, specialty clinics, and home healthcare environments, providing insights into clinical workflows, procurement trends, and digital transformation initiatives.

The study further evaluates emerging technologies including AI-based dosing systems, real-time CGM integration, biocompatible materials, and wireless energy solutions. It identifies growth opportunities in personalized therapy, remote care models, and next-generation biosensor-enabled pumps. The scope also includes in-depth competitive analysis, strategic assessments, and insights into future market readiness, making it an essential resource for medical device manufacturers, healthcare providers, investors, and policy planners.

Implantable Insulin Pumps Market Report Summary