Reports

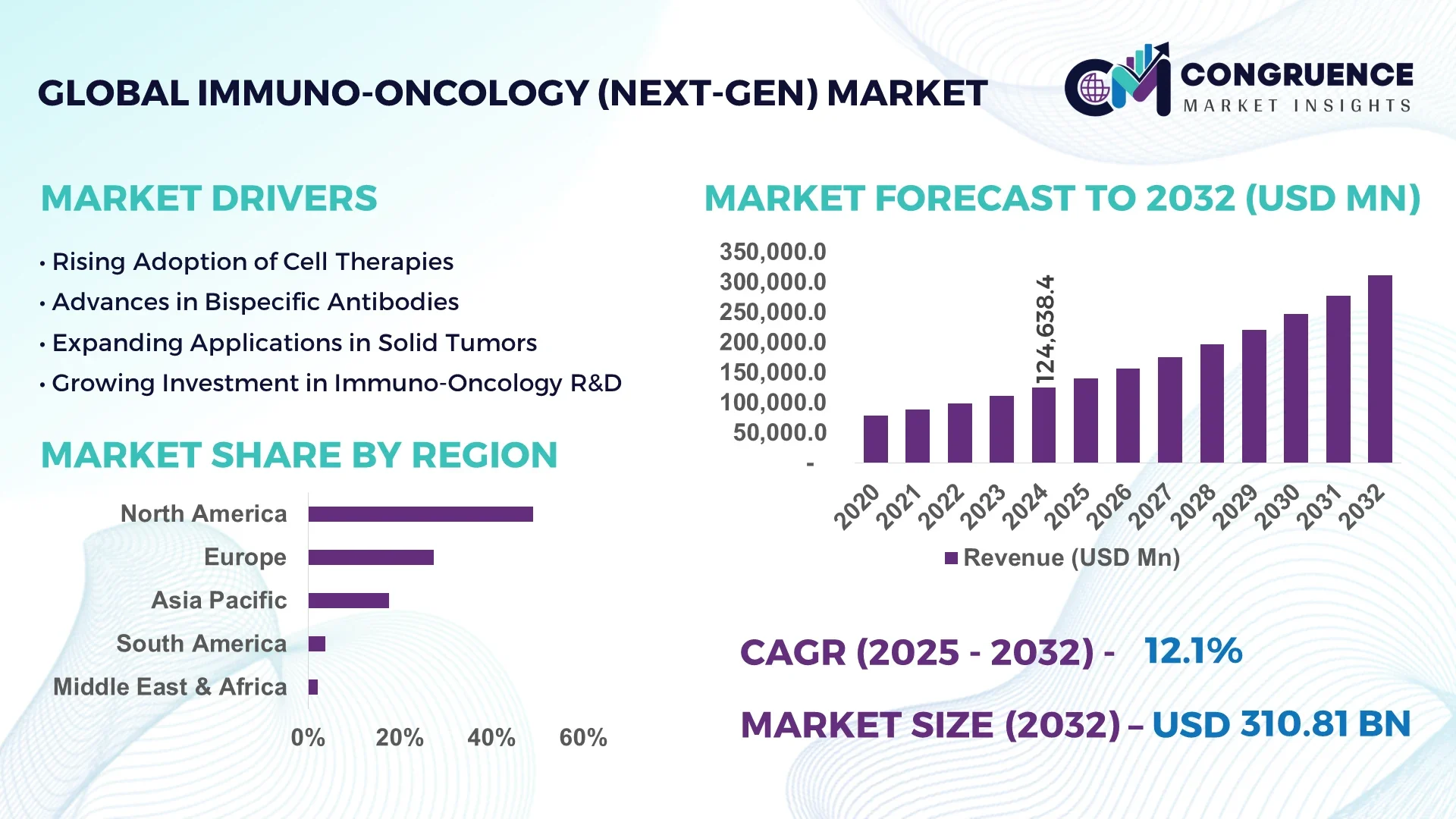

The Global Immuno-Oncology (Next-Gen) Market was valued at USD 124,638.4 Million in 2024 and is anticipated to reach a value of USD 310,811.3 Million by 2032 expanding at a CAGR of 12.1% between 2025 and 2032.

In the United States, immuno-oncology manufacturing enjoys robust production capacity with advanced cell therapy manufacturing facilities, substantial investments in CAR-T and bispecific antibody R&D, and leadership in oncology applications including hematologic and solid tumor treatments. Cutting-edge platforms for next-generation biotherapeutics, advanced CLIA labs, and centralized manufacturing supply chains support this position.

Within the broader Immuno-Oncology (Next-Gen) market, segments include cell-based therapies (CAR-T, TCR-engineered lymphocytes), bispecific antibodies, immune checkpoint modulators, and targeted cancer vaccines. Innovations such as off-the-shelf allogeneic CAR-T products, multifunctional bispecific constructs, and automated closed-system manufacturing are driving adoption. Regulatory agencies are increasingly approving next-generation biologics under expedited pathways, while healthcare systems incentivize precision immunotherapy through value-based care policies. Regionally, North America and Europe show high adoption in oncology centers, while Asia-Pacific is rapidly expanding capacity to support growing demand in China, Japan, and India. Emerging trends include modular manufacturing units for decentralized production, integration of AI-powered immunoprofiling in trial design, multi-epitope cancer vaccines, and combination platforms aiming to enhance response durability and broaden indication coverage.

AI is revolutionizing operational performance, precision, and workflow optimization within the Immuno-Oncology (Next-Gen) Market. Machine learning algorithms now enable predictive modeling of immune system responses to novel bispecific antibody constructs and cell therapy candidates, reducing screening time by over 30% and enhancing preclinical pipeline efficiency. AI-powered imaging pipelines guide manufacturing quality control by detecting subtle phenotype deviations in CAR-T cell batches, improving yield consistency and reducing batch failure rates. Natural language processing (NLP) tools are optimizing clinical trial protocols by extracting biomarker eligibility criteria from vast oncology literature, streamlining patient matching and shortening protocol development cycles. Within the market, AI-driven process analytics track real-time manufacturing data, detecting deviations in culture conditions and prompting early intervention, reducing contamination risk and ensuring regulatory compliance. Integration of AI into trial data platforms allows dynamic adaptive design, enabling real-time dose adjustments informed by immune response signatures. AI also enhances post-market surveillance through immune-related adverse event prediction models, enabling proactive risk mitigation in widespread immuno-oncology deployment. These developments collectively enhance productivity, precision, and scalability in the Immuno-Oncology (Next-Gen) Market.

“In September 2024, AstraZeneca entered an $18 million collaboration with an AI-focused biotech firm to use single-cell immune modelling for cancer drug trial optimization, improving biomarker identification and dose selection efficiency.”

The Immuno-Oncology (Next-Gen) Market is defined by rapid therapeutic innovation, regulatory adaptation, and evolving clinical adoption. Clinical demand for durable, personalized immunotherapies is driving advanced modality development—from off-the-shelf CAR-T therapies to multifunctional bispecific biologics. Regulatory pathways are adapting to accommodate next-gen modalities, including accelerated approval for therapies targeting unmet oncology needs. Providers are investing in modular, scalable manufacturing suites to decentralize production and improve access. At the same time, payers are promoting value-based reimbursement models tied to long-term survival outcomes. Academic-industry partnerships are facilitating translational pipelines for novel immunotherapeutics. Across emerging regions, government initiatives are building immunotherapy infrastructure and regulatory frameworks. This dynamic ecosystem is shaping strategic investment, innovation cycles, and market delivery in the Immuno-Oncology (Next-Gen) Market.

Next-generation advancements like allogeneic CAR-T constructs and bispecific engager platforms are accelerating clinical adoption. Clinical sites report over 10 new Phase II/III trials launched annually testing next-gen immune therapies, prompting manufacturers to scale production, streamline delivery workflows, and integrate robust quality systems to meet mounting demand.

Sophisticated production requirements—including viral vector supply, closed system bioreactors, and cryogenic logistics—inflate operational complexity. Regional treatment sites report that only about 40% of CAR-T centers manage in-house production, relying heavily on centralized facilities, which can delay treatment access and drive manufacturing bottlenecks.

Emerging models use portable, modular production units to enable on-site generation of cell therapies at hospital networks. Pilot programs indicate these setups can reduce delivery lead times by up to two weeks and expand treatment access to non-metropolitan centers, representing a scalable opportunity in Immuno-Oncology (Next-Gen) deployment.

Regions differ considerably in regulatory oversight—some require time-consuming validation for cell therapy production, while others lack established frameworks. Simultaneously, reimbursement for next-gen immunotherapies remains sparse in many markets, limiting provider ability to offer treatments despite clinical demand and slowing market penetration.

Expansion of Off-the-Shelf CAR-T Platforms: Commercial launch of allogeneic CAR-T therapies is increasing, with multiple facilities now integrating frozen, ready-to-infuse products that reduce preparation times by 50% compared to autologous models.

Surge in Multifunctional Bispecific Antibody Trials: The number of bispecific constructs entering early-stage clinical trials has doubled, with oncology centers reporting over 25 novel bispecific agents evaluated per year across solid and hematologic cancer types.

Adoption of Modular Manufacturing Pods: Hospitals and specialty centers are implementing modular, closed-system manufacturing units, enabling localized production and reducing logistic dependencies—especially in regions lacking large centralized facilities.

AI-Driven Immune Biomarker Profiling: AI-based immunoprofiling tools are now routinely used in trial design and patient stratification, identifying immune activation signatures that predict therapy response with over 85% accuracy, helping optimize candidate selection and outcomes.

The Immuno-Oncology (Next-Gen) market is segmented by type (cell therapies, bispecific antibodies, immune modulators, targeted immunotherapeutics), application (hematologic malignancies, solid tumors, adjuvant therapy, combination regimens), and end-user (academic hospitals, specialty oncology centers, commercial cell therapy providers, biopharma companies). Each segment reflects distinct infrastructure needs, therapeutic development pipelines, and adoption drivers. This segmentation provides decision-makers with clarity on strategic focus areas, deployment modalities, and investment priorities within the evolving market.

Cell therapies, including CAR-T cells and TCR-engineered products, lead the segment due to their transformative clinical efficacy and depth of pipeline. Bispecific antibodies are the fastest-growing type, powered by scalable production, off-the-shelf administration, and broader applicability in solid tumors. Immune checkpoint modulators and novel immunotherapeutics like oncolytic biologics continue to serve as foundational adjuncts, maintaining relevance in combination regimens and therapeutic expansion.

Hematologic cancers remain the primary application, led by multiple approved CAR-T and bispecific treatments showing high remission rates. The fastest-growing application is solid tumor immunotherapy, particularly for lung, breast, and GI malignancies, buoyed by bispecific and cell therapy trials. Adjuvant applications and combination strategies (e.g., with checkpoint inhibitors) are expanding as clinical evidence mounts, supporting broader therapeutic integration.

Academic hospitals are the leading end-user segment, owing to research infrastructure and early adoption of clinical trials and manufacturing systems. Specialty oncology centers and commercial cell therapy providers are the fastest-growing end-users, scaling therapy delivery through dedicated infrastructure and treatment networks. Biopharma companies remain key contributors through partnerships and licensing of next-gen therapies for commercialization.

North America accounted for the largest market share at 49.1% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13-14% between 2025 and 2032.

North America maintains its leadership with well-established immuno-oncology infrastructure, production facilities for cell therapies and bispecific antibodies, and integrated hospital-based clinical deployment. Meanwhile, Asia-Pacific—led by China, Japan, and India—is building robust manufacturing hubs, expanding reimbursement frameworks, and initiating population-scale immuno-oncology programs. Europe, South America, and the Middle East & Africa are steadily growing through targeted public health investments, emerging R&D clusters, and adoption of next-generation therapeutics. The regional landscape reflects varied maturity in infrastructure, regulatory alignment, and investment focus, all shaping the global Immuno-Oncology (Next-Gen) market outlook.

Precision Immunotherapy Ecosystem Thrives

North America commands approximately 52.1% of the global Immuno-Oncology (Next-Gen) Market. Demand is prominently driven by pharmaceutical developers, academic medical centers, and specialty oncology clinics investing heavily in CAR-T, bispecific, and immune-modulatory platforms. Regulatory bodies have streamlined approval pathways for novel immuno-oncology agents and cellular therapies, enhancing clinical adoption. Government programs also offer support such as manufacturing grants and immunotherapy access initiatives. Technological trends include adoption of closed-system manufacturing for CAR-T production, AI-enabled trial design platforms, and advanced biomarker profiling tools integrated into clinical workflows—strengthening regional leadership and innovation.

Innovative Therapeutics Transform Clinical Delivery

Europe represents around 27.4 of the Immuno-Oncology (Next-Gen) Market. Key markets include Germany, the UK, and France—each advancing national frameworks to integrate immuno-oncology therapies. Regulatory authorities and health systems are emphasizing sustainable high-tech laboratory operations and eco-efficient manufacturing. Countries are adopting immunotherapy into national cancer plans, supporting delivery via university hospitals and regional oncology centers. Emerging technologies—such as multiplex biomarker panels, AI-led patient stratification tools, and decentralized manufacturing pilot programs—are increasingly adopted in clinical settings across the region.

Rapid Surge in Therapeutic Access and Production

Asia-Pacific represents approximately 17.6% of the global market volume and ranks second in regional scale. Notable players—China, India, and Japan—are rapidly investing in immunotherapy R&D, building CAR-T and bispecific production capacity, and deploying clinical trial networks. Infrastructure trends include public-private manufacturing hubs and genomic-data platforms, particularly in metropolitan centers. Innovation clusters are leveraging AI-based bioinformatics, biomarker discovery programs, and cell therapy pilot sites to capture emerging demand and fuel regional leadership in next-generation immuno-oncology.

Emerging Therapeutic Infrastructure and Policy Support

South America accounts for roughly 3.8% of the Immuno-Oncology (Next-Gen) Market, with Brazil and Argentina as leading contributors. Brazil’s immunotherapy centers within academic hospitals are facilitating bispecific and CAR-T protocols, while Argentina is initiating precision oncology access programs. Infrastructure developments include expansion of regional manufacturing labs and diagnostic networks. Government incentives through health ministry grants and supportive import policies are encouraging clinical adoption—particularly for hematologic malignancy therapies and rare tumor immuno-regimens.

Modernizing Oncology Care through Strategic Partnerships

Middle East & Africa contribute an estimated 2.1% of the Immuno-Oncology (Next-Gen) Market, with the UAE and South Africa as growth hubs. Demand is rising in tertiary care systems focused on oncology and public health modernization. Technology adoption includes digital pathology networks, mobile health coordination, and tele-enabled clinical trial access. Governments are pursuing knowledge partnerships with global immunotherapy innovators and funding pilot production sites—laying foundations for broader regional integration of next-generation immuno-oncology.

United States – 52.1% Market Share

The United States dominates the Immuno-Oncology (Next-Gen) Market through deep R&D pipelines, integrated clinical networks, and robust regulatory pathways for advanced modalities.

China – ~15% Market Share

China is a leading Immuno-Oncology (Next-Gen) Market participant thanks to large-scale clinical trials, expanding domestic manufacturing capacity, and strong government support for immunotherapy development.

The competitive landscape of the Immuno-Oncology (Next-Gen) Market is characterized by more than 100 active global competitors, including biotechnology firms, large pharmaceutical companies, cell therapy specialists, and bioinformatics innovators. Leading players are engaging in high-value partnerships, such as co-developing bispecific antibodies or integrating AI into trial workflows. Mergers and acquisitions are reconfiguring pipelines—especially for antibody drug conjugates and next-gen cell platforms. Innovation trends include off-the-shelf allogeneic products, modular manufacturing units, and AI-powered biomarker profiling systems. Competition centers on accelerating clinical access, optimizing therapeutic durability, and expanding into underserved markets—all while balancing cost-efficiency and regulatory strategy. This dynamic environment demands strategic agility from companies targeting immuno-oncology leadership.

Bristol-Myers Squibb

Merck & Co.

Roche / Genentech

AstraZeneca

BioNTech

Novartis

Gilead Sciences / Kite Pharma

Amgen

Pfizer

Genmab

Technology continues to be a decisive factor reshaping the Immuno-Oncology (Next-Gen) Market. Advanced CAR-T and TCR-engineered cell therapies are central, supported by closed-system manufacturing platforms ensuring scalable, controlled production. Bispecific antibody constructs designed to engage dual antigens are expanding therapeutic reach across solid and hematologic tumors. Oncolytic immunotherapies and cellular payload vectors are emerging for deep tissue targeting. Precision biomarker profiling—including multiplex spatial assays and liquid-biopsy integration—supports adaptive trial design and therapy personalization. AI-driven analytics fuel immuno-phenotyping, immune-response modeling, and safety-signal detection, enhancing both preclinical screening and post-market surveillance. Decentralized manufacturing modules are enabling near-site production, reducing logistic barriers and increasing geographic access. Cloud-based bioinformatics platforms are enhancing cross-institution data analysis while preserving security standards. Together, these technologies are driving the transformation of immuno-oncology from centralized center-based care to distributed, personalized, and efficient frameworks.

In March 2024, Bristol-Myers Squibb partnered with BioNTech in an $11.1 billion collaboration to co-develop a PD-L1/VEGF-A bispecific antibody, moving three Phase III trials forward with significant funding commitments.

In June 2024, AstraZeneca’s Matterhorn trial results showed that adding Imfinzi to chemo and surgery reduced gastric cancer recurrence by 29%, potentially benefiting 40,000 patients annually across G7 nations.

In late 2023, Pfizer completed its acquisition of ADC-specialist Seagen, integrating its antibody-drug conjugate pipeline to strengthen next-generation cancer therapy capabilities.

In early 2025, AstraZeneca advanced three cancer immunotherapy candidates in late-stage development—highlighted by progression-free survival extension to over 40 months in HER2-positive breast cancer—underscoring innovative immunotherapeutic impact.

The Immuno-Oncology (Next-Gen) Market Report offers a comprehensive analysis covering global and regional performance across product types, applications, end-users, and technological trends. Product types include CAR-T and TCR cell therapies, bispecific antibodies, oncolytic immunotherapies, and immune-modulating biologics. Applications span hematologic malignancies, solid tumors, adjuvant and combination regimens. The end-user landscape is categorized into academic medical centers, specialty oncology clinics, commercial cell therapy providers, and biopharmaceutical companies. Geographic segmentation includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, each profiled for infrastructure readiness, regulatory environment, and adoption curves. Technology coverage highlights closed-system manufacturing, biomarker profiling platforms, AI-integrated drug discovery, modular production, and digital bioinformatics. The report also explores emerging niche areas such as on-site therapy pods, integrated point-of-care immuno-profiling, and population-scale immunotherapy initiatives. Tailored for industry leaders, investors, and strategists, this report provides a detailed blueprint of innovation, deployment, and competitive strategy in the evolving Immuno-Oncology (Next-Gen) Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 124638.4 Million |

|

Market Revenue in 2032 |

USD 310811.3 Million |

|

CAGR (2025 - 2032) |

12.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bristol-Myers Squibb, Merck & Co., Roche / Genentech, AstraZeneca, BioNTech, Novartis, Gilead Sciences / Kite Pharma, Amgen, Pfizer, Genmab |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |