Reports

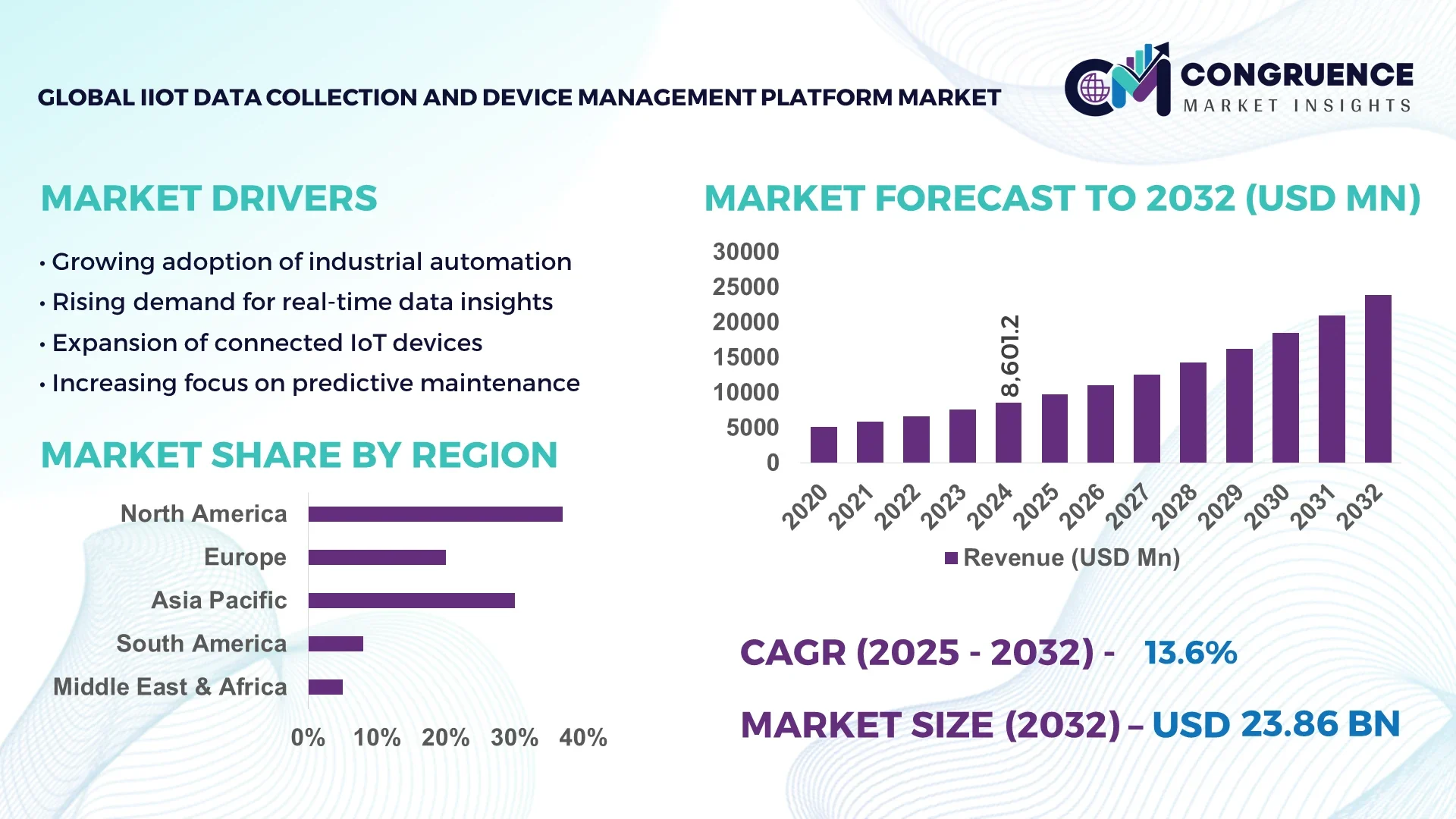

The Global IIoT Data Collection and Device Management Platform Market was valued at USD 8601.2 Million in 2024 and is anticipated to reach a value of USD 23855.4 Million by 2032 expanding at a CAGR of 13.6% between 2025 and 2032.The

United States leads global production capacity and investment levels within the IIoT Data Collection and Device Management Platform market, deploying advanced manufacturing-grade sensors and gateways across automotive, energy, and heavy industries. Significant capital influx supports large-scale deployments, R&D in edge computing integration, and deployment in smart grid and digital factory applications focused on automation, real-time monitoring, and asset lifecycle optimization.

Key sectors such as process industries (chemicals, oil & gas, pharmaceuticals) and discrete industries (automotive, electronics, aerospace) form the backbone of demand, with process industries currently dominating and discrete sectors growing swiftly. Recent technological innovations include edge-native architectures integrating on-device preprocessing, digital-twin capabilities for virtual asset monitoring, and subscription-based licensing models enhancing scalability. Policy drivers include sustainability mandates—many platforms now offer energy consumption and carbon-footprint tracking modules—and regional digital infrastructure investments, particularly across North America, Europe, and Asia-Pacific. Regulatory emphasis on cybersecurity has elevated platform adoption, and interoperability standards like OPC UA and MQTT SparkPlug™ are increasingly adopted. Future trends point toward broader AI-edge convergence, open-source tooling, and modular, pay-as-you-scale deployment strategies targeting agile digital transformation paths for industrial decision-makers.

AI is rapidly reshaping the IIoT Data Collection and Device Management Platform Market by enhancing operational performance, automating complex industrial workflows, and driving unprecedented efficiency in data ingestion and device orchestration. AI-powered edge modules now enable real-time anomaly detection and predictive insights at the device endpoint, significantly reducing unplanned downtime and enabling proactive maintenance actions. Integration of AI into data-collection pipelines has surged, with platform providers allocating a larger share of R&D resources toward generative and edge AI capabilities—boosting data throughput, reducing latency, and strengthening bandwidth efficiency in IIoT deployments. Digital-twin functionalities augmented with AI assist in simulating and monitoring millions of virtual assets, empowering decision-makers with live insights into complex systems like automotive lines and aerospace operations. AI-driven analytics also support operational optimization by automating device provisioning, bulk configuration updates, and contextual data tagging. Security-enhanced AI features, including built-in encryption and certificate-based authentication, further reinforce platform reliability. Subscription-based licensing models, streamlined with AI, allow enterprises to scale without significant capital investment. AI’s influence spans across device management, predictive maintenance, and data collection pipelines—ensuring that IIoT platforms move from passive data aggregators to intelligent, adaptive infrastructure that enables more agile, resilient industrial operations, aligned with strategic goals of efficiency, reliability, and cost optimization.

“Generative AI and edge AI integrations have risen sharply—investments into AI-enabled data-collection pipelines accounted for 25% of platform R&D budgets in Q1 2024, up from 12% in 2022.”

The IIoT Data Collection and Device Management Platform market is shaped by rapid digital transformation across industries, with demand rising for real-time analytics, predictive maintenance, and seamless device orchestration. Strong adoption is seen in manufacturing, oil and gas, utilities, and automotive sectors, where connected devices generate vast volumes of data requiring advanced collection and management solutions. Increasing regulatory focus on cybersecurity and data governance is pushing enterprises toward platforms with integrated compliance and secure communication protocols. The market is further influenced by the shift toward cloud-native and hybrid edge deployments, enabling scalable, low-latency applications. Global investment in 5G infrastructure, AI-enhanced automation, and interoperability standards continues to drive evolution, while enterprises focus on enhancing operational visibility, reducing downtime, and maximizing asset utilization.

The integration of edge and cloud architectures is a significant growth driver for the IIoT Data Collection and Device Management Platform market. Edge computing enables faster decision-making by processing data close to the source, reducing latency, and minimizing bandwidth usage. At the same time, cloud platforms provide virtually unlimited storage and advanced analytics capabilities, allowing enterprises to scale seamlessly across geographies. According to industry assessments, nearly 70% of industrial enterprises have already initiated edge-cloud integration projects to enhance system responsiveness and improve asset monitoring. This architectural convergence not only reduces operational costs but also supports high-volume device deployments, making it critical for industries such as manufacturing, energy, and logistics to maintain competitiveness in digitally transforming environments.

A key restraint in the IIoT Data Collection and Device Management Platform market is the complexity of integrating heterogeneous devices, sensors, and protocols within a unified system. Enterprises often operate legacy equipment alongside modern IoT-enabled devices, creating significant challenges in interoperability and data harmonization. Industry surveys indicate that more than 55% of IIoT implementation delays stem from integration issues and incompatibility across platforms. This complexity increases deployment timelines, requires substantial customization, and elevates the cost of implementation for large-scale projects. In addition, the lack of universal standards in device communication adds another layer of difficulty, limiting scalability and creating vendor lock-in risks that discourage adoption among risk-averse organizations.

The growing demand for predictive maintenance presents a substantial opportunity within the IIoT Data Collection and Device Management Platform market. Predictive maintenance powered by advanced analytics and machine learning enables organizations to forecast equipment failures before they occur, thereby avoiding costly downtime. Industry studies show that predictive maintenance can reduce maintenance costs by up to 30% and equipment breakdowns by nearly 70%. Adoption is accelerating across energy, transportation, and heavy manufacturing sectors, where unplanned outages result in significant productivity losses. Platforms equipped with AI-driven predictive modules are increasingly favored as enterprises seek to extend asset lifespan, optimize maintenance cycles, and ensure greater reliability in mission-critical operations. This trend is opening lucrative pathways for platform vendors offering scalable, AI-enabled solutions.

One of the most pressing challenges for the IIoT Data Collection and Device Management Platform market is the rise of cybersecurity threats targeting connected ecosystems. With billions of devices transmitting sensitive operational and performance data, industrial environments are highly vulnerable to ransomware, denial-of-service attacks, and unauthorized access. Reports suggest that cyberattacks on industrial control systems increased by over 20% in 2024, underscoring the need for resilient, secure platforms. Implementing multi-layered encryption, certificate-based authentication, and zero-trust frameworks adds significant cost and technical complexity for enterprises. Furthermore, compliance with evolving regional data protection regulations demands continuous updates and security audits, placing additional strain on platform providers and end-users alike. This ongoing challenge remains a critical factor influencing adoption decisions.

• Expansion of Edge AI Capabilities: The integration of edge AI within the IIoT Data Collection and Device Management Platform market is accelerating, with platforms embedding real-time processing capabilities directly into gateways and sensors. This minimizes latency and enables localized decision-making for critical industrial applications. In 2024, more than 45% of new deployments included edge-based analytics modules, significantly reducing dependence on centralized data centers. Industries such as automotive manufacturing and oil and gas are leveraging this advancement to optimize asset performance, reduce downtime, and enable near-instant response to anomalies.

• Growth of Device-to-Cloud Interoperability Standards: The adoption of standardized protocols such as MQTT SparkPlug™ and OPC UA is reshaping platform interoperability. In 2025, adoption rates for MQTT SparkPlug™ surged by over 30% as enterprises prioritized seamless connectivity across mixed-vendor device ecosystems. This trend is particularly impactful in energy and utilities, where hundreds of thousands of devices must be synchronized in real time. The standardization is helping businesses reduce integration costs, accelerate deployment times, and achieve greater scalability for large-scale IIoT projects.

• Focus on Cyber-Resilient Infrastructure: With cyberattacks on industrial systems rising, demand for cyber-resilient IIoT: platforms has intensified. In 2024, more than 60% of platform upgrades included advanced security features such as zero-trust frameworks and multi-layer encryption. Industries with critical infrastructure, including utilities and aerospace, are investing heavily in platforms that can secure billions of data points generated daily. This shift underscores a long-term market trend where cybersecurity is no longer an add-on but a core requirement of IIoT solutions.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the IIoT Data Collection and Device Management Platform market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor requirements and expediting timelines. High-precision connected devices and automated monitoring systems are essential for maintaining quality standards in this process. Europe and North America are witnessing increasing demand, with over 40% of new large-scale construction projects in 2024 integrating IIoT-enabled monitoring solutions to ensure efficiency, accuracy, and sustainability compliance.

The IIoT Data Collection and Device Management Platform market is segmented by type, application, and end-user, with each category reflecting distinct adoption patterns. By type, device management platforms and data collection solutions form the primary categories, where device management leads due to its role in supporting large-scale industrial connectivity, while cloud-native data collection tools are witnessing rapid adoption for predictive analytics. Applications span predictive maintenance, remote monitoring, asset optimization, and supply chain tracking, with predictive maintenance dominating as industries aim to reduce unplanned downtime. By end-user, manufacturing remains the largest segment owing to heavy automation investments, while utilities and energy sectors are rapidly scaling adoption to enhance grid stability and resource efficiency. Other industries such as transportation and healthcare are contributing by embedding IoT-driven intelligence into operational ecosystems, signaling a broadening market footprint.

In terms of type, device management platforms hold the leading position in the IIoT Data Collection and Device Management Platform market. Their ability to provision, monitor, and update millions of connected devices across global operations makes them indispensable for large-scale industrial enterprises. Adoption is particularly strong in manufacturing and utilities, where ensuring seamless communication between diverse device ecosystems is critical. The fastest-growing type is cloud-based data collection solutions, driven by their capacity to provide real-time insights, predictive capabilities, and flexible scalability across regions. Cloud-native tools are increasingly favored for enabling analytics-driven maintenance and supporting digital twins in sectors such as energy and automotive. Other types, including hybrid edge-cloud platforms and open-source integration tools, play important niche roles by catering to specific needs like reducing latency in mission-critical operations or ensuring cost efficiency for small and mid-sized enterprises. Together, these product types highlight a layered adoption strategy aligned with the varying digital maturity levels of industries.

Predictive maintenance emerges as the leading application within the IIoT Data Collection and Device Management Platform market, as industries prioritize reducing downtime and maximizing asset efficiency. This application enables organizations to cut maintenance costs significantly by predicting equipment failures before they occur, an advantage that has made it central to large-scale manufacturing, aerospace, and energy operations. The fastest-growing application is remote monitoring, fueled by the rising need for real-time visibility across geographically distributed assets and field equipment. Utilities and oil and gas industries are increasingly adopting remote monitoring solutions to ensure operational continuity and improve safety compliance. Other notable applications include asset optimization, which is gaining traction in transportation and logistics for route efficiency, and supply chain tracking, where IIoT platforms are helping businesses streamline inventory management and reduce delivery delays. Collectively, these applications illustrate the market’s pivot toward maximizing operational intelligence and enhancing enterprise-wide agility.

Manufacturing represents the leading end-user segment in the IIoT Data Collection and Device Management Platform market, driven by large-scale automation, smart factory initiatives, and adoption of digital twin technologies. Automotive and electronics manufacturers are among the earliest adopters, using IIoT platforms to enhance production line efficiency and minimize operational risks. The fastest-growing end-user segment is the utilities and energy sector, propelled by rising investments in smart grid modernization and renewable energy integration. IIoT platforms are helping utilities achieve load balancing, real-time monitoring, and predictive fault detection. Other relevant end-users include transportation, where IoT-based fleet tracking and safety compliance are becoming industry standards, and healthcare, where connected devices support patient monitoring and asset tracking within hospitals. These diverse end-user contributions highlight the expanding ecosystem of IIoT applications, underscoring the platform’s role as a central enabler of operational excellence across multiple industries.

North America accounted for the largest market share at 37% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.2% between 2025 and 2032.

The market’s regional dynamics are influenced by industrial maturity, infrastructure development, and government support for digital transformation. North America leads in early adoption due to advanced industrial automation and strong investment in edge computing, while Asia-Pacific benefits from rapid industrialization and large-scale manufacturing. Europe’s emphasis on sustainability and regulatory compliance supports market penetration, whereas South America and the Middle East & Africa show increasing potential driven by energy, construction, and smart infrastructure projects.

Strong Digital Infrastructure Driving Platform Expansion

North America held a market share of approximately 37% in 2024, with demand driven primarily by the manufacturing, aerospace, automotive, and utilities industries. Advanced digital infrastructure and widespread deployment of 5G networks have accelerated adoption across industrial applications. Government initiatives supporting smart factory transitions and enhanced cybersecurity compliance are further boosting demand. Regulatory frameworks around data protection and industrial safety have positioned the region as a leader in compliance-ready IIoT platforms. Technological advancements, such as the integration of edge AI and digital twin models, are widely implemented to optimize industrial efficiency and reduce downtime, making North America a global hub for platform innovation.

Regulatory Standards and Sustainability Shaping Market Adoption

Europe accounted for nearly 29% of the global market share in 2024, with Germany, the UK, and France being the most influential markets. Adoption is driven by stringent regulatory frameworks under organizations such as the European Commission, which enforce standards on cybersecurity, emissions, and sustainability. The EU’s digital transformation programs are accelerating platform deployment in sectors such as automotive, energy, and construction. Germany, with its Industry 4.0 initiatives, remains at the forefront of smart manufacturing adoption, while France and the UK are advancing with renewable energy integration and digital infrastructure upgrades. Emerging technologies, including blockchain-enabled device authentication and AI-enhanced asset management, are further supporting Europe’s transition toward resilient industrial ecosystems.

Industrial Growth and Smart Manufacturing Accelerating Demand

Asia-Pacific ranked second in market volume in 2024, accounting for nearly 24% of consumption, and is positioned as the fastest-growing regional market. China, India, and Japan dominate adoption, with China leading in smart factory rollouts and IoT-enabled infrastructure investments. India is experiencing rising adoption in automotive and energy sectors, driven by government-backed digitalization initiatives, while Japan leverages its advanced manufacturing base and robotics integration. Rapid infrastructure expansion and the establishment of innovation hubs across Southeast Asia further contribute to strong adoption trends. Regional focus on AI-driven predictive maintenance, low-latency edge computing, and 5G-enabled device connectivity is fueling continuous growth in this market.

Energy Modernization and Infrastructure Expansion Supporting Growth

South America represented about 6% of the global IIoT Data Collection and Device Management Platform market in 2024, with Brazil and Argentina leading adoption. Brazil’s investments in smart energy grids and industrial automation have strengthened its position, while Argentina is advancing with digital monitoring in oil and gas operations. Infrastructure modernization projects, particularly in construction and transportation, are also driving demand for connected platforms. Regional governments are providing incentives for technology adoption through tax reforms and trade partnerships that encourage industrial digitalization. These developments, combined with rising private-sector investment in connectivity and energy efficiency, are laying the foundation for sustained adoption across South America.

Oil, Gas, and Construction Driving Connected Platform Investments

The Middle East & Africa accounted for 4% of the global IIoT Data Collection and Device Management Platform market in 2024, with growth centered in the UAE, Saudi Arabia, and South Africa. Oil and gas industries are leading adopters, deploying IIoT-enabled monitoring and predictive analytics to optimize drilling and refinery operations. The construction sector is also integrating connected platforms to support megaprojects such as smart cities and large-scale infrastructure developments. Regulatory frameworks promoting industrial modernization, alongside trade partnerships encouraging technology transfer, are fueling demand. Investments in renewable energy projects and the expansion of 5G networks are further supporting platform adoption across the region.

United States – 27% market share | The country leads due to its advanced industrial automation ecosystem, widespread adoption of edge AI, and strong digital infrastructure supporting large-scale deployments.

China – 19% market share | Dominance is supported by rapid smart factory adoption, large-scale manufacturing capacity, and government-backed initiatives promoting IoT-driven industrial growth.

The IIoT Data Collection and Device Management Platform market is highly competitive, with over 80 active global and regional players shaping the landscape. The environment is characterized by continuous innovation, strategic collaborations, and product differentiation aimed at capturing industrial clients across manufacturing, utilities, energy, and transportation sectors. Leading vendors are strengthening their market positioning through cloud-native solutions, AI-powered analytics, and edge computing integration. Partnerships between platform providers and telecom operators are accelerating 5G-enabled deployments, while technology alliances with cybersecurity firms are enhancing trust in connected ecosystems. In 2024 alone, more than 30 new product launches were recorded, including modular platforms designed for scalability and cross-industry compatibility. Mergers and acquisitions remain a central strategy, with companies targeting smaller niche players specializing in interoperability or security enhancements. Innovation trends emphasize predictive maintenance, digital twins, and secure interoperability standards, setting the tone for heightened competition. This dynamic landscape is pushing both established and emerging vendors to prioritize customer-centric models, rapid deployment capabilities, and flexible subscription-based offerings to remain competitive.

Siemens AG

IBM Corporation

Microsoft Corporation

PTC Inc.

Cisco Systems Inc.

Oracle Corporation

SAP SE

ABB Ltd.

General Electric Company

Software AG

Hitachi Ltd.

Advantech Co. Ltd.

Huawei Technologies Co. Ltd.

Dell Technologies Inc.

Amazon Web Services (AWS)

The IIoT Data Collection and Device Management Platform market is being reshaped by rapid technological advancements that are enabling enterprises to manage large-scale device ecosystems with greater precision, speed, and security. Edge computing remains a transformative force, with more than 50% of industrial deployments in 2024 incorporating localized data processing to reduce latency and improve decision-making in real time. This trend is particularly significant in sectors such as energy and automotive, where milliseconds can impact system reliability and safety.

Artificial intelligence and machine learning are being increasingly integrated into platforms, offering predictive insights, anomaly detection, and advanced data classification capabilities. AI-driven device orchestration has allowed enterprises to cut downtime by nearly 40% and optimize maintenance cycles across high-value assets. Meanwhile, digital twin technology is gaining traction, enabling virtual simulations of physical equipment to test performance, identify inefficiencies, and enhance production workflows.

Cybersecurity technologies are also advancing rapidly, with multi-layer encryption, zero-trust frameworks, and blockchain-based authentication now embedded into leading solutions. Standardization efforts are improving interoperability, with adoption of protocols like OPC UA and MQTT SparkPlug™ rising by over 30% between 2023 and 2024. Cloud-native and hybrid architectures are further shaping the landscape, offering scalable deployment models and subscription-based flexibility for enterprises of all sizes. Collectively, these innovations position IIoT platforms as central enablers of industrial digital transformation.

• In March 2023, Siemens launched its Industrial Edge Management System update, enabling users to manage thousands of devices centrally with enhanced AI-based monitoring features, improving operational efficiency for large-scale manufacturing deployments.

• In July 2023, Advantech introduced its new Edge Intelligence Server series supporting AI inference capabilities at the edge, reducing data transmission needs by up to 40% while providing faster real-time analytics for critical applications.

• In February 2024, PTC expanded its ThingWorx platform with enhanced digital twin functionality, allowing enterprises to simulate complex industrial operations across multiple facilities, leading to significant improvements in asset lifecycle management.

• In June 2024, Microsoft integrated advanced security modules into Azure IoT Hub, including certificate-based authentication and zero-trust protocols, strengthening protection against rising cyberattacks on industrial device ecosystems.

The scope of the IIoT Data Collection and Device Management Platform Market Report covers a comprehensive analysis of industry drivers, challenges, opportunities, and emerging technologies shaping the sector between 2024 and 2032. It includes an in-depth segmentation by type, highlighting device management platforms, data collection solutions, and hybrid cloud-edge offerings that serve both large enterprises and small-to-medium industrial operators. Applications such as predictive maintenance, remote monitoring, asset optimization, and supply chain visibility are analyzed to reflect their unique contributions to operational efficiency and industrial automation.

Geographically, the report examines five core regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into market distribution, consumption trends, and regulatory frameworks. The analysis includes leading economies such as the United States, China, Germany, India, and Brazil, which are at the forefront of adoption.

The report also addresses key technological areas, including AI integration, edge computing, interoperability standards, and cybersecurity frameworks, alongside niche segments such as blockchain-enabled device management and sustainable IoT hardware solutions. Attention is given to end-users spanning manufacturing, utilities, energy, transportation, healthcare, and construction, with detailed insights into their adoption levels and strategic priorities. By covering these dimensions, the report provides a holistic view of the market’s current structure and long-term outlook, equipping decision-makers with actionable intelligence for strategic planning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 8601.2 Million |

|

Market Revenue in 2032 |

USD 23855.4 Million |

|

CAGR (2025 - 2032) |

13.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens AG, IBM Corporation, Microsoft Corporation, PTC Inc., Cisco Systems Inc., Oracle Corporation, SAP SE, ABB Ltd., General Electric Company, Software AG, Hitachi Ltd., Advantech Co. Ltd., Huawei Technologies Co. Ltd., Dell Technologies Inc., Amazon Web Services (AWS) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |