Reports

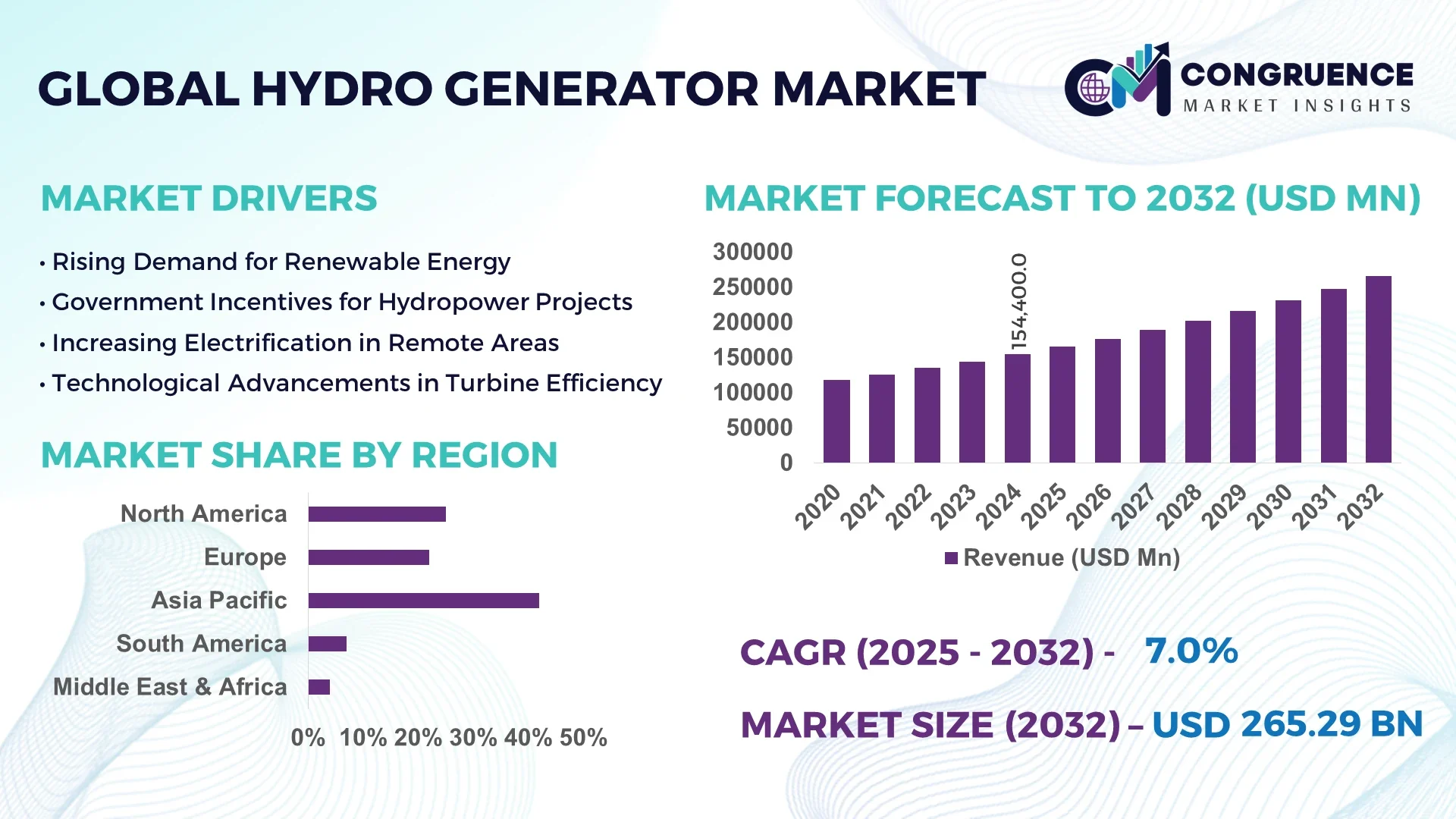

The Global Hydro Generator Market was valued at USD 154,400 Million in 2024 and is anticipated to reach a value of USD 265,287.94 Million by 2032 expanding at a CAGR of 7.0% between 2025 and 2032.

China dominates the hydro generator market globally, holding the largest installed capacity and continuously expanding its hydroelectric power projects with substantial investments in large-scale hydroelectric plants and cutting-edge generator technologies.

Globally, the hydro generator market is witnessing robust growth driven by the increasing global demand for clean and renewable energy sources. In 2024, hydroelectric power contributed approximately 16% of total global electricity generation, highlighting its importance in the energy mix. Several countries in Asia-Pacific, Europe, and North America are boosting their hydro generator capacities, with new projects often exceeding 1,000 MW in generation capacity. Modern hydro generators are achieving efficiency rates above 95%, thanks to advances in turbine blade design and materials technology. Additionally, there is growing deployment of small and micro hydro generators for off-grid and rural electrification projects, providing sustainable energy access in remote areas. Enhanced durability and lower maintenance costs of next-generation hydro generators have improved overall plant availability and operational lifespan, positively impacting the market’s expansion.

Artificial Intelligence (AI) is significantly transforming the hydro generator market by enhancing operational efficiency, predictive maintenance, and resource management. AI-powered monitoring systems collect real-time data from hydro turbines and generators, enabling early detection of mechanical anomalies such as vibration irregularities and temperature spikes, which are critical to preventing costly failures. This approach has led to reductions in unexpected downtime by over 30% in various hydroelectric facilities worldwide. AI algorithms analyze sensor data to predict maintenance needs, scheduling repairs proactively and extending the operational life of equipment.

In addition, AI supports advanced grid management by accurately forecasting electricity demand patterns and automatically adjusting hydro generator output to match consumption, improving energy distribution efficiency. Integration of AI with IoT devices in smart hydro plants allows for automatic control of turbine speed and blade pitch based on dynamic water flow and reservoir levels. Machine learning models assist in water resource management by predicting inflows and optimizing reservoir releases to balance power generation with environmental sustainability. Moreover, AI-driven drones and robotic inspection systems improve safety and precision in dam and turbine inspections, reducing manual labor risks and increasing inspection frequency. These AI applications are driving innovation, sustainability, and efficiency across the hydro generator market.

“In 2024, a major hydroelectric plant implemented AI-based predictive maintenance technology that reduced turbine downtime by 25% and improved overall energy generation efficiency by 12% within six months.”

The hydro generator market is shaped by various dynamic factors influencing its growth and technological advancements. Increasing global emphasis on renewable energy and carbon reduction targets has accelerated investments in hydroelectric power projects. Technological innovations in hydro turbines and generator efficiency are enabling higher energy outputs and extended operational lifespans. Additionally, the growing trend of decentralizing power generation is fueling demand for small and micro hydro generators, especially in rural and off-grid areas. Environmental regulations and policies promoting clean energy are also significant market drivers, while aging infrastructure and the high capital cost of new hydro plants remain critical factors affecting market expansion. Overall, the market is balancing between growth opportunities and operational challenges, fostering continuous innovation.

The rising global demand for renewable energy is a primary driver of the hydro generator market. With renewable energy accounting for more than 30% of global electricity production in 2024, hydroelectric power remains a dominant contributor due to its reliability and scalability. Governments worldwide are pushing for clean energy projects to reduce greenhouse gas emissions, driving large-scale hydro generator installations. Increasing electricity consumption in emerging economies is further stimulating investments in hydro power infrastructure. In 2024 alone, hydro generator capacity expansions exceeded 40 GW globally, underscoring the demand surge for sustainable energy generation technologies.

The high upfront costs associated with hydro generator projects act as a significant restraint in the market. Constructing large hydroelectric plants requires substantial financial resources for dam construction, turbine installation, and grid integration. These capital-intensive requirements limit the development of new hydro generator facilities, particularly in developing regions with budget constraints. Moreover, lengthy project timelines and complex regulatory approvals add to the financial and operational challenges. Existing aging infrastructure also demands expensive upgrades and maintenance, which can deter investments. These financial barriers slow market penetration and delay returns on investment for hydro power projects.

Growing demand for decentralized energy access presents a lucrative opportunity for small and micro hydro generators. These smaller-scale systems provide affordable and sustainable electricity to remote and off-grid communities, particularly in developing countries. Advances in compact turbine technology have improved efficiency and reduced installation costs, making small hydro projects more viable. In 2024, several rural electrification initiatives integrated micro hydro generators to support local energy needs. Furthermore, governments and NGOs are increasingly funding these projects to promote energy equity, which opens a significant growth avenue within the hydro generator market.

Hydro generator projects face significant challenges related to environmental impact assessments and regulatory compliance. Construction and operation of hydroelectric plants can disrupt aquatic ecosystems, affecting fish migration and water quality, which has led to stricter environmental regulations globally. Obtaining permits involves complex processes that can delay project timelines and increase costs. Additionally, climate change introduces uncertainty in water availability and reservoir levels, complicating long-term hydro power planning. These regulatory and environmental challenges require companies to invest heavily in sustainable project design and continuous monitoring, posing barriers to market expansion.

• Rise in Modular and Prefabricated Construction: The hydro generator market is increasingly embracing modular and prefabricated construction techniques. Prefabricated turbine components and generator parts are manufactured off-site with high precision, allowing for faster assembly and installation at hydroelectric project sites. This shift significantly reduces construction time and labor costs while improving quality control. Regions like Europe and North America are leading this trend, where complex hydro projects benefit from reduced environmental impact and accelerated timelines due to modular construction.

• Integration of Advanced Materials in Turbine Design: Recent advancements in material science are influencing hydro generator manufacturing, with lightweight composites and corrosion-resistant alloys being integrated into turbine components. These materials enhance durability and operational efficiency while reducing maintenance frequency. For instance, new turbine blades with improved hydrodynamic properties increase energy capture from water flows, boosting overall generator output. Such innovations are becoming more widespread, especially in markets focused on upgrading aging hydroelectric infrastructure.

• Increased Adoption of Digital Twin Technology: Digital twin technology is gaining traction within hydro generator operations. By creating real-time digital replicas of hydro turbines and generators, operators can simulate performance, predict failures, and optimize maintenance schedules. This technology leads to better asset management and prolonged equipment lifespan. Pilot projects employing digital twins report improvements in operational efficiency and reduced unplanned outages, helping operators maximize energy production.

• Growth of Small-Scale and Run-of-River Hydro Projects: The market is seeing a rising trend in the development of small-scale and run-of-river hydro generators, particularly in regions with limited large dam capacity. These projects have lower environmental impact and shorter development cycles. In 2024, several countries expanded investments in small hydro systems to increase renewable energy access in rural and off-grid areas. The demand for compact, efficient hydro generators tailored to such projects is boosting innovation and market growth worldwide.

The hydro generator market is segmented based on type, application, and end-user, each offering unique insights into market behavior and growth prospects. By type, the market includes Francis, Kaplan, Pelton, and Bulb turbines, which cater to different hydrological and project scale requirements. Applications span power generation for utilities, industrial use, and off-grid or rural electrification. End-users comprise government bodies, private power producers, and independent power producers (IPPs). Understanding these segments helps clarify demand drivers, technological preferences, and investment trends shaping the hydro generator market’s future.

The hydro generator market includes four main turbine types: Francis, Kaplan, Pelton, and Bulb turbines. Francis turbines lead the market due to their versatility in medium-head hydroelectric plants and high efficiency, accounting for over 40% of installed hydro capacity worldwide. Kaplan turbines, designed for low-head applications with adjustable blades, are the fastest-growing segment, favored for run-of-river and tidal projects, especially in Asia-Pacific. Pelton turbines are primarily used in high-head mountainous regions, representing around 25% of market share due to their reliability in steep terrains. Bulb turbines, used in small and micro hydro projects, are gaining traction as decentralized energy solutions expand. Together, these turbine types support a diverse range of hydro generator installations catering to varied geographical and operational needs.

Power generation for utility companies is the largest application segment in the hydro generator market, contributing over 70% of total market demand. This dominance is due to large-scale hydroelectric dams supplying baseload power to national grids globally. Industrial applications, including manufacturing plants and mining operations, account for about 15%, driven by increasing industrial electrification needs in developing regions. The fastest-growing application is off-grid and rural electrification, which is rapidly expanding as governments prioritize energy access for remote communities. Small hydro projects in this segment are increasing at a notable pace, facilitating local power generation and reducing reliance on fossil fuels, especially in emerging economies.

The end-user base for hydro generators primarily consists of government agencies, private independent power producers (IPPs), and industrial consumers. Government and public sector agencies hold the largest market share, as they manage most large hydroelectric projects and infrastructure development worldwide. However, private IPPs are the fastest-growing segment, propelled by deregulation and increased private sector investments in renewable energy. These producers are focusing on smaller, decentralized hydro projects that offer quicker returns and lower initial capital requirements. Industrial end-users, while smaller in market share, are increasingly adopting hydro generators for captive power generation to reduce energy costs and enhance sustainability practices.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, Africa is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

Asia-Pacific dominates due to massive hydroelectric projects in China, India, and Southeast Asia, fueling demand for advanced hydro generators. Meanwhile, Africa's growing energy infrastructure and electrification initiatives are rapidly increasing hydro generator installations, particularly in countries with untapped hydro resources. North America and Europe also hold significant shares with established hydroelectric infrastructure but slower expansion rates compared to emerging regions. South America’s investments in renewable energy diversify the market further, with countries like Brazil and Colombia playing vital roles.

"Emerging Trends in North America’s Hydro Generator Sector"

North America holds approximately 18% of the global hydro generator market share as of 2024, with the United States and Canada leading installations. The region focuses on upgrading aging hydroelectric plants with higher efficiency turbines and generators to meet stricter environmental regulations. Increased funding for small and micro hydro projects in rural areas has also contributed to market growth. The U.S. is advancing digital integration in hydro generator systems, improving monitoring and predictive maintenance. Canada continues expanding hydro capacity to support its renewable energy goals, particularly in provinces like Quebec and British Columbia, which account for a majority of hydroelectric production.

"Europe's Sustainable Hydro Generator Advancements"

Europe represents about 22% of the global hydro generator market with strong contributions from countries such as Norway, France, and Germany. The focus is on modernizing existing hydro plants by incorporating variable speed turbines and eco-friendly designs to minimize aquatic impact. The European Union’s policies encourage increased investments in small hydropower projects to support decentralized energy production. Scandinavian countries lead in integrating automation and smart grid compatibility within hydroelectric systems. Emerging Eastern European markets are also ramping up capacity expansion efforts, diversifying Europe’s hydroelectric portfolio further.

"Rapid Expansion and Innovation in Asia-Pacific Hydro Generation"

Asia-Pacific dominates the hydro generator market with a 42% share, driven primarily by China and India. Large-scale dam projects and run-of-river hydro plants are under continuous development. China remains the world’s largest producer of hydroelectric power, with multiple new installations equipped with high-efficiency Kaplan and Francis turbines. India is investing in upgrading older hydro facilities while focusing on small-scale hydro for rural electrification. Southeast Asian countries like Vietnam and Indonesia are also expanding hydroelectric capacity to meet growing energy demands and reduce fossil fuel dependence, fostering regional market growth.

"Sustainable Hydropower Growth in South America"

South America accounts for around 10% of the global hydro generator market, with Brazil and Colombia as key contributors. Brazil’s vast river systems support extensive hydroelectric infrastructure, making it a global leader in renewable power generation. Colombia is accelerating development in small and medium hydro projects to boost energy access in remote areas. Both countries emphasize improving turbine efficiency and integrating environmental safeguards. Regional trends also include hybrid hydro projects combining solar and wind power, enhancing grid stability and energy reliability in diverse geographic zones.

"Emerging Hydro Generator Opportunities in Middle East & Africa"

Middle East & Africa collectively hold around 8% of the global hydro generator market share. Despite limited large-scale hydro resources in the Middle East, countries like Turkey and Iran are developing small hydro plants to diversify their energy mix. Africa’s market is expanding swiftly due to significant untapped hydro potential in nations such as Ethiopia, Kenya, and Zambia. Investments in infrastructure modernization and cross-border hydroelectric projects are driving demand for advanced hydro generators. The region also focuses on off-grid hydro solutions to improve rural electrification and support sustainable development goals.

China (35%): Largest market share driven by massive hydroelectric dam projects and continuous capacity expansions.

Brazil (15%): Significant share due to extensive river systems supporting large-scale and small hydroelectric power generation.

The global hydro generator market features a competitive landscape characterized by the presence of numerous established multinational corporations and emerging regional players. Leading companies focus heavily on innovation, with investments in R&D to improve turbine efficiency, durability, and digital integration. Technological advancements such as smart hydro generators with real-time monitoring and predictive maintenance capabilities are becoming standard to maintain competitive advantages. Market players are also pursuing strategic partnerships and joint ventures to expand their geographical footprint and project portfolios. The trend of upgrading existing hydroelectric infrastructure with modern hydro generators is driving demand for reliable and high-capacity equipment. In 2024, companies launched several new product lines emphasizing eco-friendly designs and reduced environmental impact. Market competition is also fueled by increasing governmental support for renewable energy, which encourages manufacturers to customize solutions for small to large-scale hydro projects. This competitive environment promotes continuous innovation, enhanced product quality, and customer-centric services to secure long-term contracts and market share.

General Electric Company

Andritz AG

Voith GmbH & Co. KGaA

Siemens Energy AG

Alstom SA

Toshiba Corporation

Hyundai Heavy Industries Co., Ltd.

Bharat Heavy Electricals Limited (BHEL)

Mitsubishi Power Ltd.

Fuji Electric Co., Ltd.

The hydro generator market is witnessing significant technological advancements focused on improving efficiency, reliability, and environmental sustainability. Modern hydro generators increasingly incorporate advanced turbine designs such as Kaplan, Francis, and Pelton turbines, each optimized for different water flow and head conditions, enabling customized solutions for diverse hydroelectric sites. Innovations in materials science have led to the use of corrosion-resistant alloys and composite materials, enhancing the lifespan and durability of generator components in harsh aquatic environments. Digital transformation is playing a pivotal role, with the integration of Internet of Things (IoT) sensors and smart monitoring systems allowing real-time performance tracking and predictive maintenance. These technologies reduce downtime and operational costs by detecting anomalies before failures occur. Additionally, automation technologies enable precise control of turbine speed and power output, optimizing energy generation even under fluctuating water flow conditions.

Energy storage integration with hydro generators is another emerging trend, facilitating grid stability and better management of intermittent renewable energy sources. Small-scale and modular hydro generators are also gaining traction, designed for decentralized power generation in remote or off-grid locations.m Furthermore, eco-friendly innovations, such as fish-friendly turbines and sediment management systems, are increasingly adopted to minimize environmental impact, ensuring compliance with stringent regulatory standards worldwide. These technological developments collectively contribute to enhancing the operational efficiency and sustainability of hydro generator projects globally.

In December 2024, China approved the construction of the Medog Hydropower Station on the Yarlung Tsangpo River in Tibet. This ambitious project, with an estimated investment exceeding ¥1 trillion (approximately $137 billion), aims to become the world's largest hydropower facility upon completion in 2033. The station is projected to generate 300 billion kilowatt-hours of electricity annually, tripling the capacity of the current largest, the Three Gorges Dam.

In August 2024, the Indian government approved a financial assistance package of ₹4,136 crore for the development of 15,000 MW of hydropower projects in the Northeast region. This initiative, spanning from FY2024-25 to FY2031-32, aims to bolster renewable energy capacity and infrastructure in the northeastern states through joint ventures with Central Public Sector Undertakings.

In June 2024, the Adani Group signed a Memorandum of Understanding (MoU) with Druk Green Power Corporation for a 570 MW hydropower project in Bhutan's Chukha province. This collaboration aligns with Bhutan's infrastructure development vision and India's renewable energy goals, reflecting a growing trend of cross-border hydropower partnerships.

In September 2024, the Indian Union Cabinet approved a ₹12,461 crore outlay to support the development of 31,350 MW of hydropower projects over the next eight years. This funding aims to enhance infrastructure in remote and hilly regions, covering costs for enabling infrastructure such as transmission lines, ropeways, and communication facilities.

The scope of the Hydro Generator Market report encompasses a comprehensive analysis of the global hydroelectric power generation sector, covering technological advancements, market segmentation, and regional dynamics. The report includes detailed insights into various hydro generator types such as Francis, Kaplan, and Pelton turbines, highlighting their applications across different scales of hydropower plants—from small micro-hydro setups to large-scale dams exceeding 1,000 MW capacity. It also explores diverse applications including electricity generation for residential, commercial, and industrial users, emphasizing increasing adoption in remote and off-grid areas.

The report evaluates the market based on end-users such as utility companies, independent power producers, and government energy projects, reflecting trends in renewable energy integration and environmental sustainability. Geographic analysis covers major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, noting investment flows, policy support, and infrastructure development in each area.

Key technological trends such as digital monitoring systems, smart grid compatibility, and AI-assisted predictive maintenance are assessed, along with challenges like environmental regulations and high initial capital costs. The report also highlights emerging opportunities in developing nations focusing on rural electrification and cross-border hydroelectric projects. Overall, this report provides stakeholders with essential data and actionable insights to strategize effectively within the evolving hydro generator market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 154400 Million |

|

Market Revenue in 2032 |

USD 265287.94 Million |

|

CAGR (2025 - 2032) |

7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type:

By Application:

By End-User:

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

|

|

Customization & Pricing |

Available on Request (10% Customization is Free) |