Reports

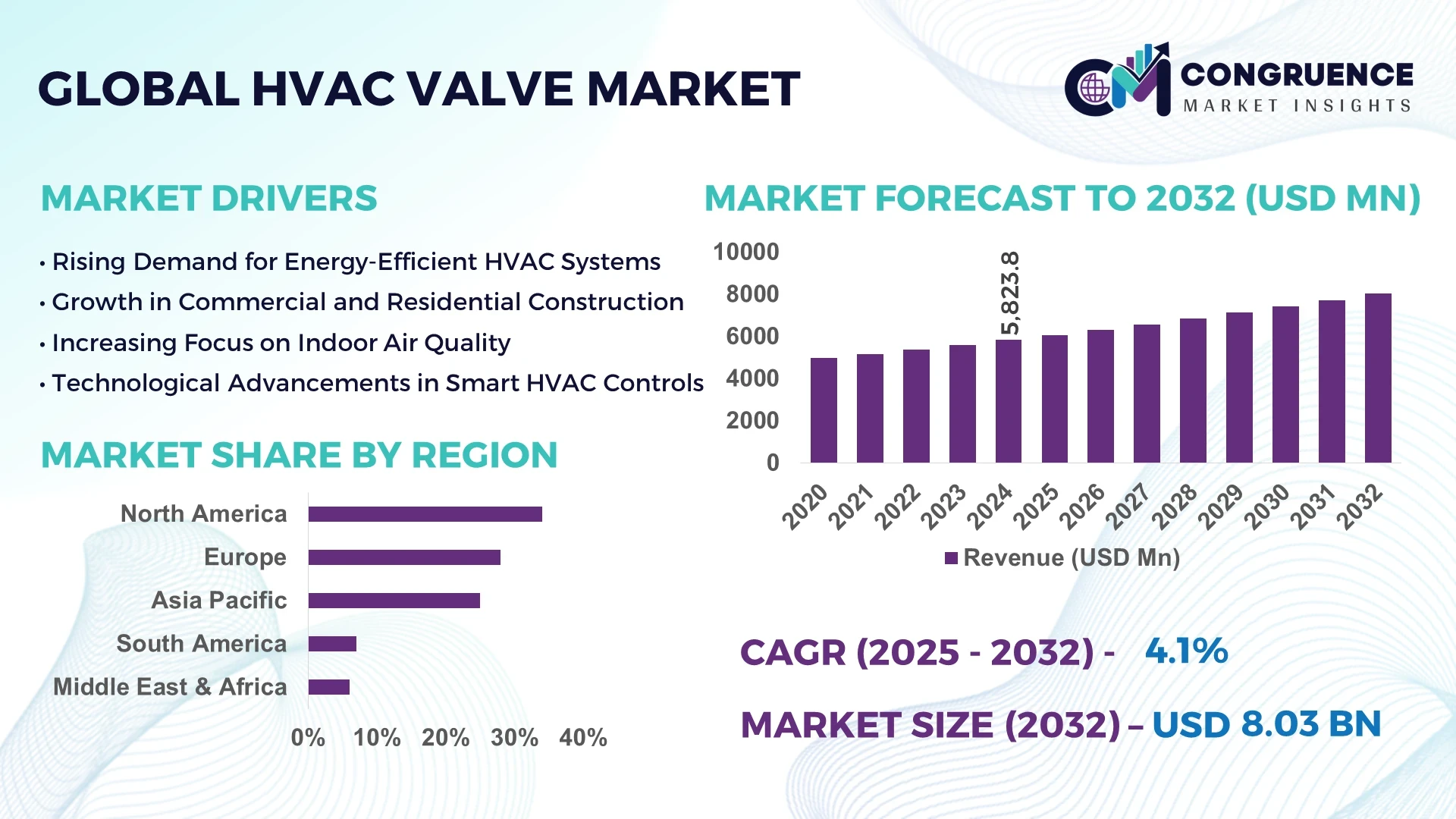

The Global HVAC Valve Market was valued at USD 5823.77 Million in 2024 and is anticipated to reach a value of USD 8031.74 Million by 2032 expanding at a CAGR of 4.1%% between 2025 and 2032.

China operates the largest integrated manufacturing footprint for HVAC control and isolation valves, supported by sustained multi-billion-dollar investments in automated machining, robotic assembly, and testing facilities; producers serve district-energy networks, transport hubs, and heavy industrial campuses, while advancing high-torque actuators, low-leakage seats, smart positioners, and digital calibration tools.

In the wider HVAC Valve market, commercial buildings (offices, healthcare, education, data centers, and mixed-use) account for an estimated 60–65% of unit demand, followed by industrial facilities at roughly 20–25% and residential hydronic systems at 10–15%. Advancements include pressure-independent control valves (PICVs), ultra-low-power electric actuators, and IoT-ready devices that expose telemetry for analytics and remote diagnostics. Environmental and regulatory drivers—particularly energy-efficiency codes, refrigerant transitions, and green-building certifications—are accelerating replacement of legacy manual valves with precise, electronically actuated alternatives. Regionally, APAC shows robust consumption growth tied to urbanization and new construction, while North America and Europe emphasize retrofits, demand-responsive control, and building-automation integration. Emerging trends include digital twins for hydronic loops, modular manifold architectures, cybersecurity-hardened communications (BACnet/IP, MQTT), and factory-calibrated PICVs that stabilize delta-T and reduce pump energy in scalable, high-performance systems.

AI is redefining performance baselines across the HVAC Valve Market through data-driven optimization, predictive maintenance, and autonomous control. Machine-learning models ingest valve position, differential pressure, coil temperatures, and pump signals to continuously tune valve authority, stabilizing loop control and reducing “hunting” by 40–60% in balanced circuits. Pressure-independent, AI-supervised strategies have demonstrated 8–15% reductions in hydronic pumping energy by maintaining optimal differential pressure and improving delta-T by roughly 1.5–3.0 °C in chilled-water systems. Computer-vision or analytics-based commissioning automates stroke verification and leakage checks, cutting commissioning time by 25–35% for large commercial projects. Predictive health models flag rising actuator torque, seat wear, or abnormal hysteresis, lowering unplanned valve replacements by 10–20% and enabling just-in-time maintenance windows that minimize downtime.

Digital-twin workflows simulate valve dynamics under load variability, helping engineers validate control sequences, right-size PICVs, and shorten project handover. In continuous operation, reinforcement-learning controllers coordinate valve positions with air-side and plant-side setpoints, yielding 5–12% whole-building HVAC energy savings in steady-state operations while keeping comfort KPIs (zone temperature, humidity) within tight bands. For portfolio owners, AI-enabled valves expose standardized telemetry via secure APIs, allowing centralized benchmarking and remote diagnostics—an operational advantage that reduces truck rolls, enhances service SLAs, and positions suppliers in the HVAC Valve Market as providers of intelligent, lifecycle-optimized components rather than commodity hardware.

“In June 2024, a major global building-automation vendor introduced an AI upgrade that optimized hydronic valve positions in a large international airport, reporting an 18% reduction in HVAC energy use and a 10% peak-demand cut across more than 1 million m², with documented improvements in delta-T stability and automated fault detection for valve actuators.”

The HVAC Valve Market is influenced by evolving building efficiency standards, advancements in automation, and the global shift toward smart infrastructure. Demand is driven by the increasing integration of valves into intelligent HVAC systems for enhanced performance, energy savings, and predictive maintenance capabilities. Urbanization and commercial construction growth, particularly in Asia-Pacific, continue to fuel product adoption, while industrial retrofits in North America and Europe boost replacement demand for advanced electronically actuated valves. The market is also shaped by environmental compliance regulations and the rapid adoption of IoT-enabled monitoring systems, which improve operational efficiency and extend asset lifespans. Additionally, the push for sustainable HVAC solutions is leading to innovations in low-power actuators, modular valve assemblies, and pressure-independent designs that optimize hydronic system performance.

The proliferation of smart building initiatives is significantly boosting demand within the HVAC Valve Market. Intelligent control systems, paired with connected HVAC valves, enable precise monitoring and real-time optimization of heating and cooling performance. According to recent industry data, smart commercial buildings equipped with advanced HVAC components can achieve 15–20% reductions in energy use through automated valve control. As more enterprises pursue green building certifications and compliance with energy codes, adoption of BACnet/IP-compatible and cloud-integrated valves is expanding. This driver is further strengthened by corporate ESG commitments, encouraging investment in equipment that supports energy transparency, predictive maintenance, and lifecycle efficiency improvements.

Despite the benefits, the integration of advanced control valves into existing HVAC infrastructure presents significant challenges for market expansion. Retrofitting legacy systems with IoT-enabled or AI-supervised valves can involve high capital costs, extensive rewiring, and compatibility issues with older building management systems. For instance, installing motorized PICVs in outdated hydronic loops often requires redesigning piping layouts and recalibrating pumps to match pressure requirements. Additionally, skilled labor shortages in HVAC commissioning can extend project timelines and increase expenses. These factors can deter smaller facility owners from upgrading, limiting penetration rates for advanced valve technologies in cost-sensitive market segments.

The global expansion of district cooling and heating networks is creating substantial opportunities for the HVAC Valve Market. Large infrastructure projects—such as smart cities, airport terminals, and urban residential complexes—require extensive networks of high-capacity control valves to manage thermal energy distribution efficiently. District energy systems equipped with modern hydronic control valves can improve load balancing, reduce thermal losses, and enable centralized monitoring, leading to 8–12% operational energy savings. The rapid urban development in regions such as the Middle East, Southeast Asia, and parts of Africa presents a significant untapped customer base for manufacturers offering robust, scalable valve solutions optimized for long-term, heavy-duty applications.

Increasingly stringent environmental regulations present a complex challenge for stakeholders in the HVAC Valve Market. Manufacturers must adapt to evolving building energy codes, refrigerant transition mandates, and efficiency benchmarks that often vary between regions. For example, valves designed for certain refrigerants may require re-engineering to comply with new low-GWP refrigerant standards, impacting design cycles and supply chains. Compliance testing, certification processes, and lifecycle assessments can add months to product development timelines, delaying market entry for new solutions. Additionally, global manufacturers must navigate multiple regulatory frameworks simultaneously, raising operational complexity and increasing the cost of maintaining compliance while staying competitive.

Rise in Modular and Prefabricated Construction: The growth of modular and prefabricated construction is influencing procurement patterns in the HVAC Valve Market. Preassembled HVAC valve assemblies and prefabricated hydronic modules allow contractors to reduce on-site labor by up to 40% and shorten installation timelines by 25–30%. These modules are manufactured in controlled environments using precision CNC cutting and automated welding, ensuring dimensional accuracy and leak-free performance. The trend is particularly notable in Europe and North America, where labor shortages and compressed project schedules make prefabricated solutions a competitive advantage.

Integration of IoT and Digital Twin Capabilities: Advanced HVAC valves are increasingly equipped with IoT connectivity and digital twin compatibility. IoT-enabled valves transmit real-time performance data such as flow rate, differential pressure, and actuator position, enabling remote diagnostics and automated adjustments. Digital twin technology allows engineers to simulate hydronic system performance before deployment, identifying optimization strategies that can improve energy efficiency by 8–12% and extend equipment lifespan. This integration is transforming valve management from reactive to predictive.

Adoption of Pressure-Independent Control Valves (PICVs): PICVs are gaining rapid traction due to their ability to maintain consistent flow regardless of pressure fluctuations, improving system stability and reducing pump energy consumption by 10–15%. These valves are particularly favored in large-scale commercial buildings and healthcare facilities where precise temperature control is critical. The growing emphasis on energy savings and indoor comfort is accelerating PICV adoption across both new construction and retrofit projects.

Sustainability-Driven Material Innovations: Manufacturers are adopting advanced materials such as lead-free brass, stainless steel, and composite polymers to meet stricter environmental regulations. These materials not only improve corrosion resistance and valve longevity but also comply with potable water safety standards. Additionally, lightweight composite-bodied valves reduce shipping weight by 15–20%, lowering transportation emissions and total project costs. This material shift aligns with broader green building initiatives and corporate sustainability commitments.

The HVAC Valve Market is segmented by type, application, and end-user, each representing distinct demand drivers and adoption patterns. Type segmentation covers manual, motorized, pressure-independent, and zone control valves, with varying degrees of technological integration. Application segmentation spans heating, cooling, and ventilation systems in diverse environments ranging from commercial high-rises to industrial facilities. End-user segmentation highlights usage across commercial, residential, and industrial sectors, each influenced by regional infrastructure investment trends, technological readiness, and regulatory landscapes. Understanding these segments provides insight into where innovation, investment, and competitive positioning can deliver the greatest impact.

Motorized control valves lead the HVAC Valve Market, driven by their precision, automation compatibility, and suitability for integration with building management systems (BMS). Their ability to modulate flow dynamically enhances energy efficiency and comfort, making them the preferred choice in modern commercial and industrial projects. The fastest-growing segment is pressure-independent control valves (PICVs), propelled by demand for stable hydronic system performance and reduced commissioning times. PICVs eliminate the need for separate balancing valves, cutting installation complexity and lowering operating costs. Manual valves, while representing a mature segment, remain relevant in cost-sensitive applications and smaller-scale installations due to their low initial investment and simplicity. Zone control valves, used for managing specific building areas, hold a niche position in residential and light-commercial systems, where zoning flexibility is valued. The diversity of valve types reflects the balance between cost, complexity, and performance requirements across different market environments.

Cooling applications dominate the HVAC Valve Market, supported by the extensive use of chilled-water systems in commercial buildings, healthcare facilities, and data centers. These environments demand precise temperature regulation to protect equipment and ensure occupant comfort. Heating applications are experiencing strong growth, particularly in colder climates and in district heating systems where hydronic valves play a critical role in efficiency optimization. Ventilation-related applications, though smaller in volume, are benefiting from the integration of air-handling units with hydronic heating and cooling coils, requiring reliable valve control to manage airflow temperature effectively. The fastest-growing application is in mixed-use developments, where integrated HVAC systems must support diverse heating, cooling, and ventilation needs within the same infrastructure. This multi-application demand is pushing the development of versatile valve solutions that can adapt to variable operational requirements while maintaining efficiency.

Commercial end-users represent the largest share of the HVAC Valve Market, with adoption driven by large-scale construction, retrofitting of existing infrastructure, and stringent energy performance requirements. Office complexes, shopping malls, educational institutions, and hospitals all rely on precise valve control for optimal environmental management. The fastest-growing end-user category is the industrial sector, particularly manufacturing plants, pharmaceuticals, and food processing facilities that require exact temperature and humidity control for process stability. Residential applications, while smaller in overall market share, are evolving with the uptake of smart home systems and zoned climate control, where compact, connected valves enhance comfort and efficiency. Additionally, government and public infrastructure projects, including airports and transit hubs, contribute to demand through large-scale, centralized HVAC systems requiring durable, high-capacity valve installations. This varied end-user landscape underscores the importance of tailoring valve design and performance to specific operational and regulatory contexts.

North America accounted for the largest market share at 34% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

Regional performance is influenced by infrastructure expansion, regulatory frameworks, and adoption of smart building technologies. Mature markets like North America and Europe continue to prioritize energy efficiency retrofits, while emerging economies in Asia-Pacific and the Middle East invest heavily in new commercial and industrial projects. Latin America shows steady adoption in metropolitan hubs, driven by infrastructure upgrades. Across all regions, IoT integration, pressure-independent solutions, and sustainability-driven innovations are becoming standard market differentiators.

Advanced Infrastructure Modernization Driving Smart HVAC Adoption

Holding approximately 34% of the global volume, this region is driven by demand from commercial real estate, healthcare, and large-scale industrial facilities. Government-backed energy efficiency programs and state-level building codes have accelerated the shift to smart, electronically actuated valves. Industries such as pharmaceuticals, data centers, and retail chains are investing in integrated HVAC control systems for operational optimization. Technological advancements, including AI-driven predictive maintenance and digital twin deployment, are enabling greater system reliability and cost savings, aligning with the region’s broader digital transformation agenda.

Sustainability Regulations Accelerating Green Valve Solutions

Representing around 28% of the global market volume, this region’s demand is concentrated in Germany, the UK, and France. The European Commission’s energy performance directives and national building codes mandate high-efficiency HVAC solutions, spurring widespread adoption of pressure-independent and IoT-enabled valves. Sustainability initiatives such as BREEAM and LEED certification have increased demand for eco-friendly materials and low-leakage designs. Emerging technologies, including AI-enhanced control systems and cybersecurity-ready valve communication protocols, are gaining traction across both new and retrofit projects.

Rapid Urbanization Fueling High-Volume HVAC Installations

Accounting for roughly 25% of global market volume, this region is led by China, India, and Japan as top consumers. Rapid construction of smart cities, large-scale manufacturing hubs, and commercial complexes is driving demand for advanced HVAC valve systems. The region is experiencing increased localization of manufacturing, supported by automation-focused industrial parks. Innovation hubs in China and Japan are developing next-generation IoT-integrated valves for real-time monitoring, while India’s infrastructure boom creates significant opportunities for scalable, modular valve solutions.

Infrastructure Revitalization and Energy Efficiency Mandates Driving Growth

With an estimated 7% share of the global market, key countries such as Brazil and Argentina are spearheading regional demand. Large-scale infrastructure upgrades, coupled with energy sector investments, are prompting adoption of modern hydronic control systems. Government incentives for energy-efficient equipment, alongside trade policies facilitating imports of advanced HVAC components, are expanding product accessibility. Industrial and commercial developments in metropolitan areas are pushing demand for durable, low-maintenance valve solutions.

Construction Boom and Industrial Expansion Elevating HVAC Valve Demand

Representing about 6% of the global market, demand is driven by high-value sectors such as oil & gas, commercial real estate, and hospitality. Countries like the UAE and South Africa are adopting smart building standards, encouraging integration of BMS-compatible control valves. Technological modernization in large-scale infrastructure projects, such as airports and mixed-use developments, is boosting uptake of advanced valve systems. Local regulatory frameworks are promoting efficiency standards, while trade partnerships with global HVAC suppliers are improving product availability and quality.

United States – 22%: Strong demand from commercial real estate, healthcare facilities, and industrial manufacturing, supported by advanced building automation adoption.

China – 18%: High production capacity combined with rapid deployment in urban infrastructure and large-scale industrial projects.

The HVAC Valve Market features a moderately consolidated competitive environment, with over 40 active global and regional players engaged in product manufacturing, distribution, and system integration. Industry leaders hold strong positions through advanced product portfolios, widespread distribution networks, and a focus on high-performance, energy-efficient solutions. Competitive strategies increasingly center on technological innovation, with key players investing in IoT-enabled smart valves, AI-driven control systems, and pressure-independent designs to meet evolving efficiency standards. Partnerships with building automation companies and collaborations with construction firms are becoming common to enhance market penetration in commercial and industrial projects. Product launches incorporating advanced materials such as lead-free brass and corrosion-resistant alloys are gaining traction due to environmental regulations. Mergers and acquisitions remain an important avenue for expanding regional presence and gaining access to specialized technologies. Competition is also intensifying in the aftermarket service space, with companies offering predictive maintenance platforms and performance analytics to differentiate their offerings in a market that prioritizes reliability, lifecycle cost savings, and regulatory compliance.

Belimo Holding AG

Danfoss Group

Honeywell International Inc.

Johnson Controls International plc

Siemens AG

Schneider Electric SE

AVK Holding A/S

NIBCO Inc.

Crane Co.

Bray International, Inc.

The HVAC Valve Market is undergoing significant technological transformation driven by advancements in automation, connectivity, and energy optimization. Smart valve technologies are increasingly embedded with IoT sensors capable of monitoring parameters such as flow rate, differential pressure, and temperature in real time, enabling predictive maintenance and reducing operational downtime by up to 25%. Pressure-independent control valves (PICVs) have emerged as a key innovation, maintaining consistent flow despite pressure fluctuations, which can lower pumping energy consumption by 10–15% in large hydronic systems. Integration with Building Management Systems (BMS) via BACnet/IP, Modbus, and MQTT protocols is now standard in premium solutions, allowing centralized control and system-wide efficiency optimization.

Material innovation is also reshaping the market, with manufacturers adopting lead-free brass, stainless steel, and high-strength composite polymers to meet regulatory requirements while extending service life in demanding environments. Digital twin applications are enabling engineers to model valve performance before installation, reducing commissioning times and improving system reliability. In parallel, AI-enhanced control algorithms are enabling adaptive valve responses to changing load conditions, improving comfort levels and operational efficiency. The integration of cybersecurity features into communication modules ensures secure data exchange in connected systems. Collectively, these technological advancements are redefining HVAC valve performance benchmarks and creating opportunities for manufacturers to deliver differentiated, high-value solutions.

In March 2024, Belimo launched a new generation of pressure-independent control valves designed for large-scale hydronic systems, capable of reducing pump energy consumption by up to 15% while maintaining precise flow control across variable load conditions.

In August 2024, Danfoss introduced its AI-enabled digital valve controller, integrating machine-learning algorithms to dynamically optimize flow regulation, resulting in a 12% improvement in thermal efficiency in commercial building HVAC systems.

In November 2023, Siemens unveiled an IoT-ready motorized valve series with integrated cloud connectivity, enabling remote diagnostics and predictive maintenance, which reduced maintenance interventions by 20% during field trials.

In May 2023, Johnson Controls expanded its range of lead-free brass control valves, designed to meet stricter environmental regulations while offering 30% higher corrosion resistance compared to conventional brass alloys.

The HVAC Valve Market Report provides an extensive analysis of the industry’s structure, technological landscape, and competitive positioning across multiple dimensions. It covers product segmentation by type, including motorized control valves, manual valves, pressure-independent control valves, and zone control valves, highlighting their respective adoption patterns and performance attributes. The report examines application-based segmentation across heating, cooling, and ventilation systems, assessing demand drivers in both new construction and retrofit projects.

Geographically, the report evaluates the market across five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—detailing regional infrastructure trends, regulatory landscapes, and technological adoption rates. The scope extends to key end-user categories, including commercial, residential, and industrial sectors, with additional focus on niche segments such as district energy systems, data centers, and healthcare facilities that require high-precision thermal management.

From a technological perspective, the report explores emerging innovations, including IoT integration, AI-based control optimization, advanced materials, and cybersecurity-enabled communication protocols. It also addresses sustainability trends influencing material selection, manufacturing processes, and lifecycle management. By encompassing both mature and emerging markets, the report offers decision-makers a comprehensive understanding of where strategic investments, product innovations, and partnerships can yield competitive advantages in a rapidly evolving HVAC valve industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 5823.77 Million |

|

Market Revenue in 2032 |

USD 8031.74 Million |

|

CAGR (2025 - 2032) |

4.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Belimo Holding AG, Danfoss Group, Honeywell International Inc., Johnson Controls International plc, Siemens AG, Schneider Electric SE, AVK Holding A/S, NIBCO Inc., Crane Co., Bray International, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |