Reports

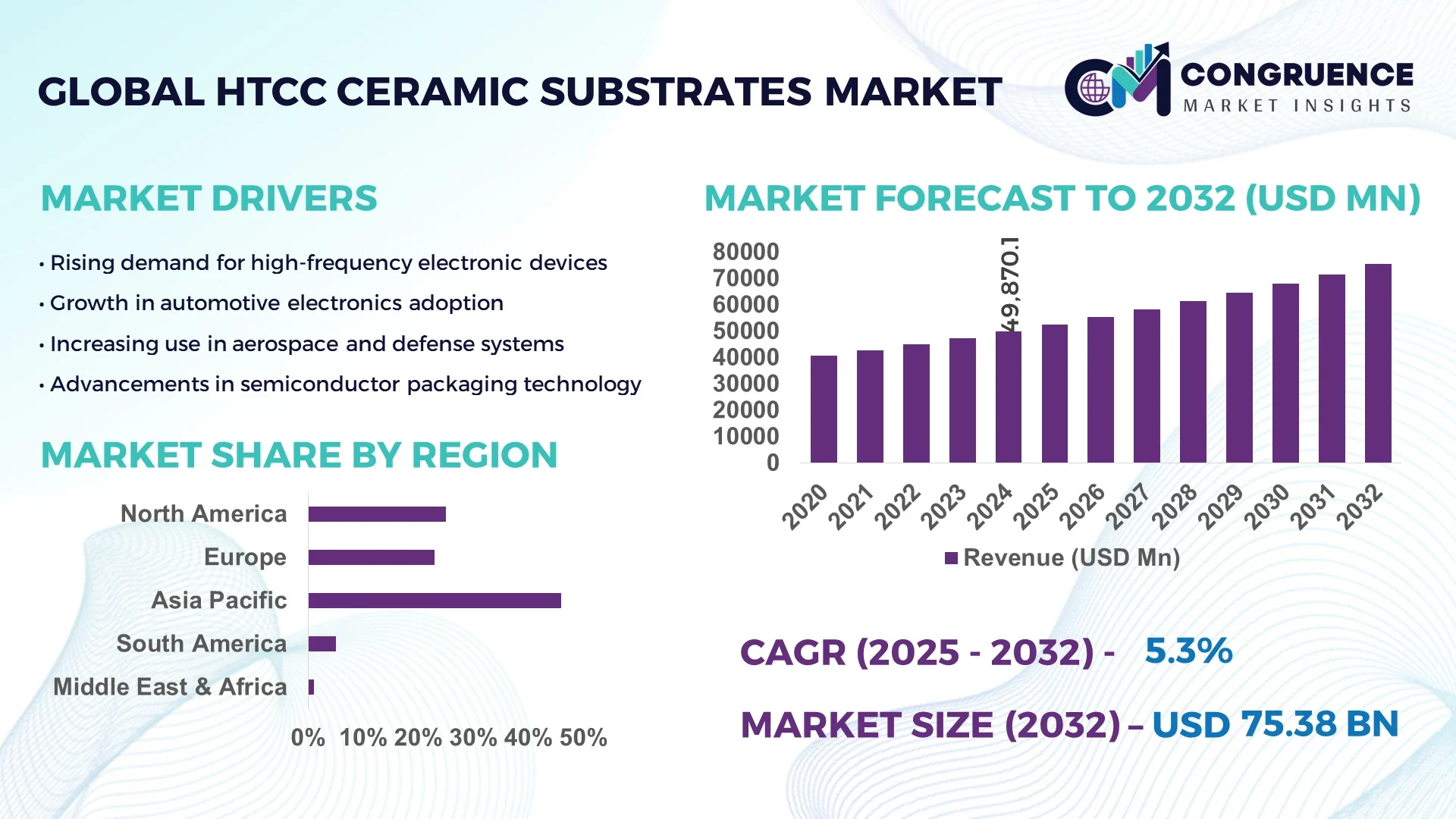

The Global HTCC Ceramic Substrates Market was valued at USD 1381.45 Million in 2024 and is anticipated to reach a value of USD 2519.34 Million by 2032 expanding at a CAGR of 7.8%% between 2025 and 2032.

In Japan, the country leading the HTCC Ceramic Substrates market, production capacity is supported by extensive, advanced manufacturing infrastructure dedicated to high-temperature co-fired ceramics. Investment levels have consistently focused on scaling multilayer sintering lines and modernizing automation equipment to support applications across automotive radar, 5G modules, high-reliability industrial devices, and aerospace-grade electronic packaging. Technological advancements include new multilayer HTCC lines tailored for extreme environments, such as high-temperature engine sensors and compact hermetic packages, enhancing both product durability and performance.

The HTCC Ceramic Substrates Market serves critical sectors including consumer electronics, automotive electronics, telecommunications, aerospace, and industrial automation. Consumer electronics remain a major contributor, with demand driven by thermal management in compact high-performance devices. Automotive electronics—particularly in EVs and ADAS—are rapidly growing, benefiting from HTCC's superior heat dissipation and reliability in power modules and sensor assemblies. Telecommunications and 5G infrastructure require HTCC substrates with high dielectric stability for high-frequency RF components. In aerospace and defense, HTCC's hermetic sealing and thermal stability enable resilient avionics and satellite components under extreme conditions. Recently, companies have introduced innovations such as ultrathin multilayer HTCC optimized for LiDAR and radar applications, while emerging hybrid packaging combining HTCC with organic or metal-organic frameworks enhances thermal efficiency and miniaturization. Regulatory and environmental drivers include stringent emissions and energy-efficiency standards, further propelled by the global shift toward sustainable manufacturing. Regionally, Asia-Pacific consumption dominates, powered by electronics manufacturing hubs in China, Japan, South Korea, and Taiwan, while North America and Europe grow through aerospace and industrial automation demand. Emerging trends include eco-friendly HTCC formulations, sustainability-focused production, and integration into smart and IoT-enabled systems—pointing toward robust growth and future innovation in high-performance electronic packaging.

Artificial intelligence is increasingly revolutionizing the HTCC Ceramic Substrates Market by streamlining manufacturing processes and elevating operational efficiency—transforming how high-performance ceramic components are designed, produced, and maintained. In production facilities, AI-driven process control systems optimize critical variables such as firing temperature, humidity, and heating rates across complex co-firing cycles. In similar ceramic industries, these systems have reduced energy use by over 20% and improved yield by more than 10%, offering strong potential in HTCC fabrication lines through comparable adaptive, real-time adjustments. Predictive maintenance systems powered by AI analyze sensor data—vibrations, temperatures, equipment metrics—to forecast kiln or press maintenance needs, minimizing unplanned downtime and extending asset longevity. These implementations have seen downtime reductions of up to 68%, directly enhancing throughput and cost efficiency.

Throughput optimization through AI-enabled bottleneck analysis and production scheduling unlocks hidden capacity. In practice, reshaping workflow using AI has increased effective output by over 20%, delivering performance gains without requiring additional capital investment. Integrating AI-based digital twins—virtual models that mirror real-time factory operations—supports rapid scenario testing and dynamic process tuning, enabling continuous improvements in yield and quality within HTCC manufacturing workflows. Moreover, AI-powered design automation is emerging in HTCC substrate development. AI streamlines complex multilayer layout designs and optimizes circuit routing for thermal and dielectric performance, greatly reducing prototyping cycles. This trend aligns with broader advances in AI-enabled layout generation and hybrid packaging strategies across LTCC and HTCC sectors.

AI is fundamentally reshaping the HTCC Ceramic Substrates Market by enhancing production efficiency, reducing operational costs, accelerating design iterations, and enabling predictive insights—empowering decision-makers and industry professionals to scale high-performance ceramic solutions with precision and agility.

“In February 2025, a manufacturer of HTCC ceramic component enclosures implemented an AI-enabled co-firing control system that optimized temperature ramp rates dynamically for each batch, improving first-pass yield from 85 % to 93 % while reducing kiln energy use by 18 %.”

The HTCC Ceramic Substrates Market is shaped by a combination of technological innovations, sector-specific demand, and evolving global industry priorities. The market is strongly influenced by the increasing miniaturization of electronic devices, the growth of high-frequency communication systems, and the rising adoption of advanced driver-assistance systems in automotive industries. Regulatory shifts toward sustainability and stricter emissions requirements are also fueling the need for high-performance substrates with efficient thermal management. Additionally, regional expansion in Asia-Pacific continues to accelerate production capacity, while Europe and North America are leveraging aerospace and defense applications. Together, these factors are creating a dynamic environment where innovation and demand for robust, high-reliability substrates drive steady advancements.

The HTCC Ceramic Substrates Market is experiencing significant growth due to the rising need for high-frequency and high-power electronic components across diverse industries. With the expansion of 5G networks, base stations, and advanced RF modules, HTCC substrates are gaining prominence for their ability to deliver excellent dielectric performance, stability, and reliability under high-temperature operating conditions. In the automotive sector, the electrification of vehicles and the deployment of advanced driver-assistance systems are generating strong demand for high-power modules that require superior thermal conductivity. Industrial automation and aerospace applications are also adopting HTCC substrates for their durability and resistance to harsh environments. As the complexity of electronic packaging continues to rise, HTCC’s ability to meet stringent performance requirements is emerging as a central driver of sustained market adoption.

Despite strong growth potential, the HTCC Ceramic Substrates Market faces constraints due to high manufacturing costs and the technical complexity of production. The co-firing process requires precise temperature control, advanced materials, and multilayer alignment that demand heavy investment in equipment and skilled labor. Production yields can be impacted by even minor deviations in process parameters, adding to overall costs. Additionally, raw materials such as alumina and tungsten used in HTCC are subject to fluctuating supply chain dynamics, creating uncertainty in procurement expenses. Smaller manufacturers often find it challenging to compete with established players that benefit from economies of scale. These financial and technical barriers limit widespread adoption, especially among emerging economies and price-sensitive applications, thereby acting as a key restraint on market expansion.

The growing adoption of IoT-enabled and smart devices is creating significant opportunities for the HTCC Ceramic Substrates Market. As consumer electronics evolve toward higher integration and lower power consumption, HTCC substrates are being utilized in miniaturized sensors, wireless communication modules, and compact power systems. The demand for devices capable of seamless connectivity in healthcare, smart homes, and industrial IoT applications is driving the need for substrates with reliable thermal and electrical performance. Furthermore, innovations in hybrid packaging, combining HTCC with organic substrates or advanced coatings, are enabling next-generation modules tailored for compact and multifunctional designs. The expanding global ecosystem of IoT devices, projected to surpass tens of billions of connected units in the next decade, positions HTCC substrates as a critical enabler of high-reliability and scalable solutions, offering a major growth avenue for manufacturers.

One of the major challenges for the HTCC Ceramic Substrates Market lies in supply chain vulnerabilities and geopolitical dependencies. The production of HTCC substrates relies heavily on raw materials such as high-purity alumina, tungsten, and molybdenum, much of which is concentrated in specific regions. Any disruptions, whether from trade restrictions, geopolitical tensions, or export regulations, directly impact availability and pricing. Additionally, global transportation bottlenecks and logistics delays can hinder timely deliveries, affecting downstream industries like automotive, aerospace, and telecommunications. Manufacturers are under pressure to diversify sourcing strategies and establish resilient supply networks, but this often entails higher costs and longer lead times. These structural challenges, coupled with ongoing geopolitical uncertainties, present a significant hurdle to maintaining consistent production and ensuring competitive market performance.

• Miniaturization Driving Demand for Ultra-Thin Substrates: The HTCC Ceramic Substrates market is witnessing a clear trend toward miniaturization, with manufacturers increasingly developing ultra-thin multilayer substrates below 100 microns. These designs are critical for next-generation consumer electronics, including compact smartphones, wearables, and advanced medical sensors, where space efficiency and high thermal conductivity are essential. This demand has accelerated R&D investments in thin-layer stacking and precision printing technologies to improve density without compromising strength.

• Expansion in Electric Vehicle Electronics: Electric vehicles are reshaping demand dynamics in the HTCC Ceramic Substrates market, particularly for power modules and battery management systems. The substrates’ ability to withstand high voltages and extreme operating temperatures makes them indispensable in traction inverters and onboard charging systems. Recent industry data highlights a sharp increase in the adoption of HTCC in high-reliability automotive electronics, with manufacturers introducing tailored designs that balance power density and durability.

• Integration in 5G and Advanced Telecommunications Infrastructure: Telecommunications is emerging as one of the fastest-growing areas of HTCC application, driven by the global rollout of 5G networks and high-frequency base stations. Substrates with superior dielectric stability are increasingly deployed in millimeter-wave modules and RF power amplifiers. Industry players are expanding production lines dedicated to telecommunications-grade HTCC, with new designs enabling greater frequency precision and energy efficiency in compact packaging formats.

• Eco-Friendly and Sustainable Manufacturing Innovations: Sustainability has become a defining trend in the HTCC Ceramic Substrates market, with manufacturers prioritizing energy-efficient sintering processes and low-impact materials. Green production technologies that cut energy consumption by up to 25% are gaining traction, particularly in Asia-Pacific. Additionally, research into recyclable ceramic composites and waste reduction strategies during high-temperature co-firing has positioned sustainability as both a regulatory necessity and a competitive advantage for manufacturers expanding into global markets.

The HTCC Ceramic Substrates market segmentation is defined by product type, application, and end-user categories, each reflecting unique adoption trends and industry demands. By type, substrates vary from alumina-based to zirconia and other specialized composites, with distinctions in performance characteristics for thermal and electrical management. Applications span across power modules, RF devices, sensors, and aerospace-grade packaging, with each domain contributing differently to growth dynamics. From an end-user perspective, sectors such as consumer electronics and automotive are driving consistent demand, while aerospace and defense contribute to high-value niche markets. Industrial automation and healthcare are also gaining momentum, creating a diverse adoption landscape. This segmentation highlights how specific needs in performance, durability, and miniaturization are shaping adoption trends and influencing manufacturing strategies worldwide.

HTCC Ceramic Substrates are primarily categorized into alumina-based substrates, zirconia-based substrates, and other composite materials. Alumina-based HTCC substrates hold the leading position, favored for their high thermal conductivity, mechanical strength, and cost-effectiveness, making them the standard in consumer electronics and automotive modules. Zirconia-based HTCC substrates, though less common, are growing in relevance due to superior mechanical resilience and toughness, particularly in aerospace and defense-grade applications where reliability under mechanical stress is critical. Among these, alumina remains dominant due to its well-established production processes and widespread application versatility. The fastest-growing type is hybrid HTCC substrates, which integrate ceramic with advanced composites or thin-film coatings to enhance electrical insulation and minimize energy loss. These are particularly suitable for next-generation RF modules and compact power electronics. Other niche variants, including specialized formulations for extreme high-frequency components, are gaining attention but remain limited to specific advanced applications. Collectively, the expansion of types reflects ongoing innovation aimed at meeting stringent requirements across emerging technologies.

Applications of HTCC Ceramic Substrates span across power modules, RF devices, sensors, and aerospace-grade electronics. Power modules represent the leading application segment, driven by demand for efficient thermal management in electric vehicles, renewable energy systems, and industrial automation. The ability of HTCC substrates to withstand high voltages and sustain thermal loads makes them indispensable in this area. The fastest-growing application is RF devices, particularly with the global expansion of 5G and beyond-5G infrastructure. HTCC substrates offer superior dielectric stability, making them critical in millimeter-wave antennas, RF filters, and base station components. This demand is further accelerated by increased investment in telecommunications infrastructure worldwide. Other applications, such as sensors for automotive ADAS, biomedical devices, and aerospace navigation systems, are steadily gaining adoption. These domains value HTCC’s hermetic sealing, durability, and ability to perform reliably under extreme environmental conditions. The diversity of applications demonstrates how HTCC substrates are integral to multiple technology sectors, each fueling broader market adoption.

End-users of HTCC Ceramic Substrates include consumer electronics, automotive, aerospace and defense, industrial automation, and healthcare. The consumer electronics sector leads the market, driven by demand for compact, high-performance devices requiring efficient heat dissipation and miniaturized packaging. Smartphones, wearables, and portable computing devices continue to incorporate HTCC to ensure reliability and longevity under high-performance conditions. The fastest-growing end-user is the automotive industry, fueled by electric vehicle adoption and advanced driver-assistance systems. HTCC substrates are increasingly integrated into EV powertrains, inverters, and high-frequency radar modules, highlighting their crucial role in enabling safe, reliable, and efficient automotive electronics. Aerospace and defense represent another significant end-user segment, where reliability under extreme conditions is critical. HTCC’s thermal stability and hermetic sealing make it ideal for avionics and satellite communication systems. Industrial automation and healthcare are emerging end-user groups, adopting HTCC substrates for robotics, medical sensors, and diagnostic devices. Collectively, these end-users demonstrate the widespread applicability of HTCC substrates across industries where performance, reliability, and miniaturization are essential.

Asia-Pacific accounted for the largest market share at 46% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

Asia-Pacific leads due to its concentration of electronics manufacturing hubs, advanced infrastructure, and sustained investments in high-temperature co-fired ceramic technologies. Meanwhile, North America benefits from surging demand in electric vehicles, aerospace, and industrial automation, supported by strong R&D activity and favorable regulatory frameworks. Europe maintains a stable position, largely due to sustainability-driven initiatives and advanced telecommunications networks, while South America and the Middle East & Africa are emerging through targeted infrastructure projects and government incentives, creating promising long-term opportunities.

High-Performance Substrates Powering Technological Growth

North America held approximately 21% of the global HTCC Ceramic Substrates market share in 2024, reflecting strong demand across automotive, aerospace, and advanced defense systems. Industries such as electric vehicles and industrial automation are particularly influential, leveraging HTCC substrates for reliable performance in high-voltage and thermal-intense environments. Government support in the form of tax credits for EV adoption and initiatives to strengthen domestic semiconductor production has bolstered growth prospects. Technological advancements include the use of AI-enabled design automation and digital twins for substrate manufacturing optimization, driving efficiency and consistency in production. The rapid integration of smart manufacturing technologies continues to position the region as a hub for innovation and advanced adoption.

Innovation-Driven Substrates Supporting Sustainable Electronics

Europe represented around 18% of the HTCC Ceramic Substrates market share in 2024, with Germany, the UK, and France being leading adopters. The region benefits from a strong industrial base in automotive, telecommunications, and aerospace, all of which increasingly require high-performance substrates. European Union regulatory bodies have enforced stricter environmental and sustainability standards, prompting manufacturers to implement greener production technologies and improve energy efficiency. Emerging technology adoption, such as the deployment of 5G networks and advanced radar systems, is accelerating HTCC integration in the region. With a strong emphasis on eco-friendly manufacturing, Europe continues to invest in sustainable innovations that align with long-term growth strategies.

Electronics Manufacturing Hubs Driving Regional Leadership

Asia-Pacific dominated the global HTCC Ceramic Substrates market in 2024 with 46% share, supported by large-scale consumption in China, Japan, South Korea, and India. China leads as the primary hub for mass electronics manufacturing, while Japan maintains a reputation for advanced R&D in high-performance ceramics. South Korea is rapidly expanding HTCC adoption in semiconductors and 5G infrastructure, and India is emerging with increasing investment in EVs and industrial automation. Regional innovation hubs are focusing on hybrid ceramic technologies and sustainable production processes, supported by robust infrastructure and government-led manufacturing initiatives. This collective ecosystem cements Asia-Pacific as the global leader in HTCC substrate consumption and production.

Emerging Applications Across Automotive and Energy Sectors

South America accounted for nearly 6% of the global HTCC Ceramic Substrates market share in 2024, led primarily by Brazil and Argentina. The growing focus on renewable energy systems and electric mobility is creating new demand opportunities, particularly in power modules and high-reliability industrial electronics. Infrastructure modernization projects are increasing the use of HTCC substrates in telecommunications and automation applications. Government incentives supporting clean energy adoption and regional trade policies are encouraging local industries to expand investments in advanced electronics manufacturing. While still in its growth phase, the region shows promising momentum in adopting HTCC solutions for next-generation energy and mobility projects.

Advanced Materials Adoption in Energy and Infrastructure

The Middle East & Africa represented around 9% of the global HTCC Ceramic Substrates market share in 2024, driven by adoption in oil and gas exploration equipment, construction automation, and telecommunications. Countries such as the UAE and South Africa are emerging as growth hotspots, investing heavily in technological modernization and smart infrastructure. Regional regulations supporting digital transformation and trade partnerships are encouraging industries to integrate advanced materials like HTCC for durable, high-performance applications. Investments in aerospace, satellite communication, and defense electronics are further broadening demand, positioning the region as a steadily advancing player in the global market landscape.

China – 29% Market Share: China leads the HTCC Ceramic Substrates market due to its massive electronics manufacturing ecosystem and large-scale investments in high-performance ceramic technologies.

Japan – 17% Market Share: Japan dominates with advanced R&D capabilities and strong applications in automotive, aerospace, and telecommunications requiring reliable and durable HTCC substrates.

The HTCC Ceramic Substrates market is characterized by a moderately consolidated competitive environment with over 25 active global and regional manufacturers engaged in advanced ceramic substrate production. Leading players focus on innovation in multilayer structures, ultra-thin substrate development, and hybrid material integration to differentiate their product portfolios. Strategic initiatives such as cross-industry partnerships with semiconductor companies, collaborations with automotive OEMs, and joint ventures in 5G infrastructure are increasingly shaping the market’s competitive dynamics. Several players are also investing in green manufacturing technologies, including low-energy sintering and recyclable ceramic composites, to align with sustainability-driven regulations and consumer expectations. Product launches targeting high-frequency RF devices, compact radar modules, and advanced EV power systems are reinforcing market positioning. Competitive intensity is further heightened by regional expansion strategies, particularly in Asia-Pacific, where localized production hubs are supporting large-scale demand. The interplay of innovation, partnerships, and strategic expansion is defining the trajectory of competition, ensuring the HTCC Ceramic Substrates market remains highly dynamic and innovation-led.

Kyocera Corporation

Maruwa Co. Ltd.

Murata Manufacturing Co. Ltd.

NGK Spark Plug Co. Ltd.

NIKKO Company

KOA Corporation

Yokowo Co. Ltd.

Chaozhou Three-Circle Group (CCTC)

Guangdong Fenghua Advanced Technology Holding Co. Ltd.

Hebei Sinopower Ceramic Electronics Co. Ltd.

Technological advancements in the HTCC Ceramic Substrates market are reshaping the performance, design flexibility, and application potential of high-temperature co-fired ceramics. Current innovations focus on enhancing multilayer integration, dielectric performance, and thermal conductivity to meet the increasing complexity of modern electronics. Advanced multilayer HTCC structures now support over 40 layers of circuitry with embedded vias, enabling higher density packaging for compact devices. These capabilities are critical for industries such as 5G telecommunications, aerospace, and automotive electronics, where high power density and reliability are essential.

One emerging trend is the adoption of ultra-thin HTCC substrates, with thicknesses reduced to under 100 microns without compromising mechanical stability. These developments are accelerating applications in wearables, medical implants, and miniaturized sensors. Hybrid technologies combining HTCC with LTCC or organic substrates are gaining traction, optimizing both cost and performance for specific applications. Meanwhile, advancements in metallization techniques, including copper-molybdenum composites and silver alloys, are enhancing electrical conductivity and heat dissipation efficiency.

Sustainability has become a parallel driver of technology adoption, with energy-efficient co-firing methods capable of reducing power consumption by up to 20%. Additionally, research into recyclable ceramic composites and advanced sintering additives aims to reduce environmental impact while improving yield rates. Digital transformation is also entering the HTCC manufacturing ecosystem, with AI-powered design automation and predictive quality control reducing error margins and cycle times. Collectively, these technological innovations are positioning HTCC substrates as a cornerstone material for next-generation electronics requiring high precision, durability, and reliability.

• In February 2023, Kyocera expanded its ceramic substrate production in Kagoshima, Japan, adding a new manufacturing line designed for automotive and 5G-related modules. The facility aims to increase annual output by 25%, supporting the rising demand for high-performance substrates in next-generation communication and mobility solutions.

• In July 2023, Maruwa introduced an advanced ultra-thin HTCC multilayer substrate designed for radar and LiDAR systems in electric vehicles. The product delivers improved dielectric stability and heat dissipation, reducing module size by 18% compared to conventional solutions and enabling higher efficiency in compact automotive electronics.

• In March 2024, Murata Manufacturing launched a new generation of HTCC-based RF components specifically for 5G base stations. These substrates feature enhanced frequency precision, with performance tested up to 40 GHz, ensuring robust operation in high-frequency communication modules. This innovation is expected to accelerate adoption in telecom infrastructure.

• In October 2024, NGK Spark Plug Co. announced the development of hermetic HTCC packages for aerospace navigation systems. The new product line offers improved sealing and resistance to extreme temperature fluctuations, targeting avionics and satellite communications where durability and reliability are mission-critical.

The scope of the HTCC Ceramic Substrates Market Report encompasses a comprehensive evaluation of product types, applications, end-user sectors, geographic regions, and emerging technologies that define market evolution. The report covers alumina-based substrates, zirconia substrates, and hybrid composites, analyzing their roles in addressing specific industry requirements for thermal management, dielectric performance, and mechanical stability. In terms of applications, the report provides detailed insights into power modules, RF devices, sensors, and aerospace-grade electronics, reflecting the diverse range of technologies supported by HTCC substrates. End-user industries including consumer electronics, automotive, aerospace and defense, industrial automation, and healthcare are assessed, highlighting how each sector contributes to demand dynamics and product innovation.

Regionally, the report evaluates Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, presenting insights into regional consumption patterns, production hubs, and strategic growth opportunities. Asia-Pacific’s dominance through electronics manufacturing, North America’s focus on automotive and aerospace, and Europe’s emphasis on sustainability initiatives are clearly detailed to guide regional strategies. The scope also includes technological trends such as multilayer miniaturization, hybrid HTCC integration, AI-assisted design, and sustainable production practices, identifying their impact on competitiveness and future product development. Emerging niche segments, including IoT-enabled sensors and medical device substrates, are analyzed for their growth potential. Overall, the report provides a structured, data-driven perspective tailored for decision-makers, ensuring clarity on market breadth, evolving opportunities, and strategic areas of investment.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1381.45 Million |

|

Market Revenue in 2032 |

USD 2519.34 Million |

|

CAGR (2025 - 2032) |

7.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Kyocera Corporation, Maruwa Co. Ltd., Murata Manufacturing Co. Ltd., NGK Spark Plug Co. Ltd., NIKKO Company, KOA Corporation, Yokowo Co. Ltd., Chaozhou Three-Circle Group (CCTC), Guangdong Fenghua Advanced Technology Holding Co. Ltd., Hebei Sinopower Ceramic Electronics Co. Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |