Reports

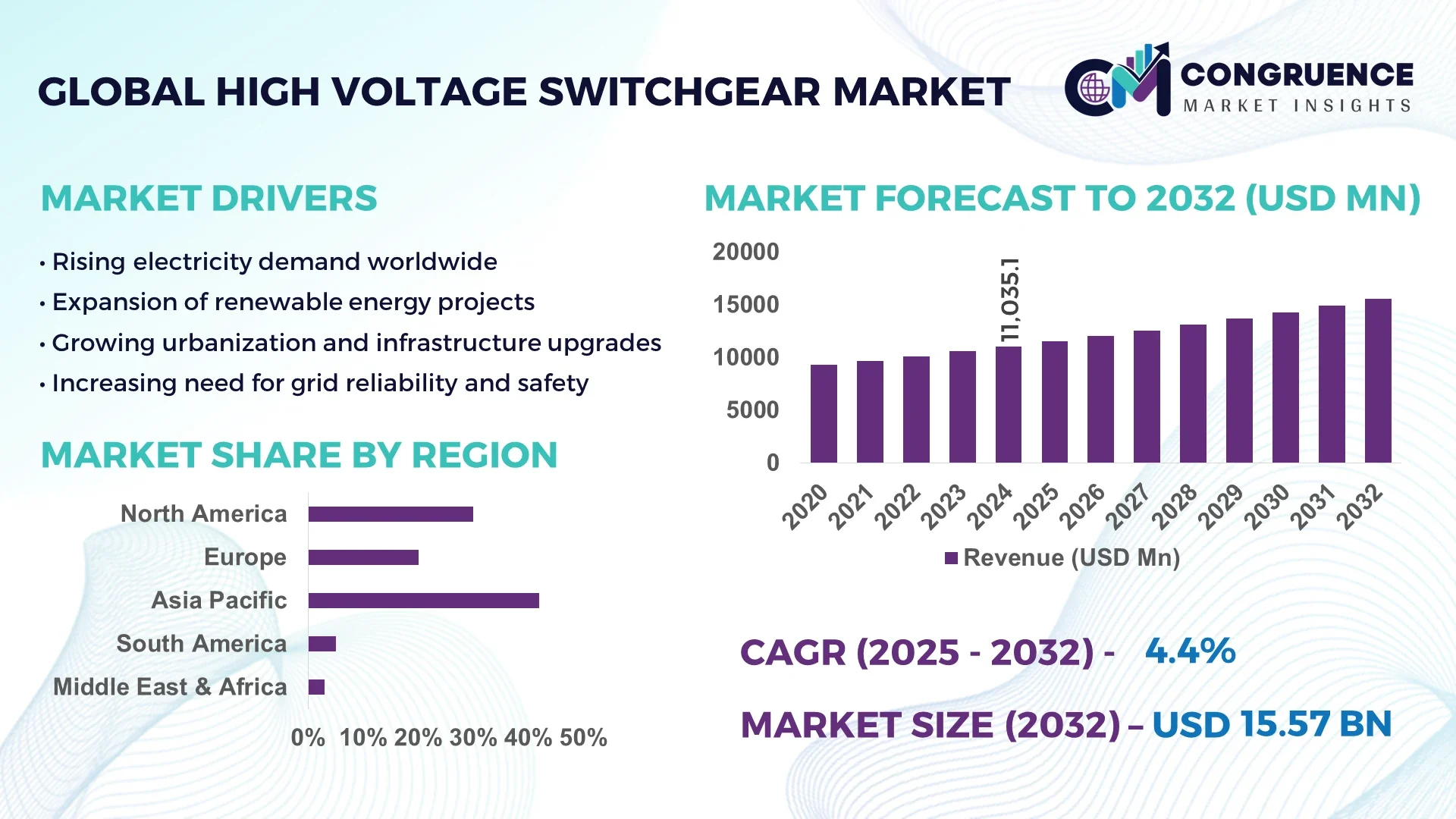

The Global High Voltage Switchgear Market was valued at USD 11035.08 Million in 2024 and is anticipated to reach a value of USD 15573.2578834306 Million by 2032 expanding at a CAGR of 4.4% between 2025 and 2032.

China, as the dominant country in the global High Voltage Switchgear Market, boasts extensive production capacity with multiple large-scale manufacturing facilities operating across its eastern industrial hubs. Investment levels are substantial, with both state-owned and private companies channeling billions into advanced gas-insulated switchgear production lines. Key industry applications include power transmission networks, ultra-high voltage grids, and renewable energy substations, where technological advancements such as compact modular designs and SF₆-alternative insulating materials are increasingly implemented to enhance system reliability and reduce environmental impact.

The High Voltage Switchgear Market serves critical industry sectors including utilities, oil & gas, mining, manufacturing, and renewable energy infrastructure. Utilities drive substantial demand through grid modernization projects and smart substations, while the oil & gas and mining sectors rely on robust switchgear for heavy-duty distribution needs. Recent technological and product innovations include gas-insulated switchgear (GIS) favored for space-constrained environments, SF₆-free alternatives to address environmental regulations, and digital switchgear featuring IoT-based sensors and real-time monitoring. Regulatory, environmental, and economic drivers include mandates to reduce greenhouse gas emissions, rising investments in renewable energy and electrification, and urbanization trends boosting electricity demand. Regional consumption patterns vary: North America and Europe focus on smart grid and clean energy integration, while Asia-Pacific emphasizes rapid infrastructure expansion and utility upgrades. Emerging trends reveal a shift toward digital substations, predictive diagnostics, compact modular designs, and environmentally friendly insulation technologies. Future outlook indicates sustained growth driven by grid resilience requirements, electrification of industries, and environmental compliance.

AI transformation is markedly enhancing the High Voltage Switchgear Market by driving operational efficiency, reliability, and proactive asset management. Artificial intelligence systems now enable predictive maintenance protocols, analyzing real-time sensor data—such as voltage, temperature, and vibration—to forecast equipment degradation, which significantly reduces unplanned outages and maintenance costs. Smart diagnostics powered by AI detect anomalies like voltage dips or potential short circuits, enabling rapid fault identification and automated isolation of affected components, thus minimizing downtime and improving grid stability. Load balancing and energy optimization are also achieved through AI-driven analytics, dynamically adjusting distribution to prevent system overloads, lowering energy waste and operational costs.

The convergence of AI with digital and IoT-enabled switchgear creates a transformative shift in high-voltage applications. Embedded sensors, cloud analytics, and machine learning allow remote monitoring and control, enhancing grid resilience and supporting integration of intermittent renewables and increasing electric vehicle loads. Predictive maintenance through AI forecasts failures, dramatically cutting repair time and improving availability. Self-healing systems, enabled by AI, automatically detect and isolate faults to reroute power—ensuring uninterrupted service. AI-oriented asset management optimizes lifecycle planning and extends operational longevity, while remote diagnostics reduce on-site inspection needs, improving safety and efficiency. These intelligent capabilities position AI-integrated switchgear as essential for modern power networks, helping decision-makers achieve more sustainable, resilient, and cost-effective infrastructure without speculative projections.

“In 2025, a U.S. smart grid pilot deployed AI-enabled high-voltage switchgear integrating embedded sensors and real-time analytics to reduce equipment downtime by over 25 %, while improving fault detection accuracy by 35 %.”

The High Voltage Switchgear Market is influenced by evolving energy infrastructure needs, technological advancements, and sustainability priorities. Global utilities and industrial sectors are adopting advanced switchgear solutions to improve grid stability and efficiency, particularly with the rising integration of renewable power sources. Environmental regulations are shaping the shift toward SF₆-free insulation technologies, while digitalization trends are accelerating adoption of smart switchgear equipped with IoT sensors and AI-driven analytics. Expanding electricity consumption in urban centers and industrial clusters further strengthens market demand, while modernization programs in aging transmission networks create consistent replacement needs. These dynamics collectively position the High Voltage Switchgear Market as a cornerstone of global energy transition.

Growing global investments in grid modernization projects and renewable energy integration are a significant driver for the High Voltage Switchgear Market. Nations across Asia, Europe, and North America are allocating billions of dollars toward strengthening transmission infrastructure to handle increasing electricity demand and renewable penetration. For instance, renewable power now contributes more than one-third of global electricity generation, creating demand for robust and flexible high-voltage equipment. Advanced switchgear technologies, such as gas-insulated systems and digital substations, ensure efficient distribution while accommodating fluctuating loads from solar and wind resources. This trend not only enhances grid reliability but also supports decarbonization initiatives, making switchgear solutions integral to long-term energy strategies.

One of the primary restraints impacting the High Voltage Switchgear Market is the regulatory pressure surrounding the use of sulfur hexafluoride (SF₆), a potent greenhouse gas traditionally used for insulation. With a global warming potential thousands of times higher than CO₂, SF₆ has been subject to increasing restrictions across Europe and other regions. Manufacturers face rising compliance costs as they transition toward alternative insulating materials, such as vacuum or fluoronitrile blends. This transition, while environmentally necessary, can slow deployment and raise product costs. Additionally, utilities operating legacy SF₆-based systems must manage complex retrofitting processes, creating both financial and technical barriers that restrain faster adoption of next-generation switchgear.

The integration of digital technologies and AI-enabled analytics presents a transformative opportunity in the High Voltage Switchgear Market. Utilities and industries are increasingly deploying intelligent switchgear that combines IoT sensors, cloud connectivity, and predictive analytics to monitor real-time performance. This technology enables condition-based maintenance, early fault detection, and enhanced energy optimization, reducing operational risks and maintenance costs. Forecasts indicate that digital switchgear adoption could increase at double-digit annual rates, driven by smart grid rollouts and rising energy storage integration. Moreover, the ability to remotely manage assets enhances safety in high-risk environments, creating additional opportunities for adoption in sectors such as mining, offshore energy, and heavy industries.

Despite strong growth prospects, the High Voltage Switchgear Market faces challenges associated with high capital expenditure and deployment complexity. Large-scale installations often require significant upfront investment in equipment, infrastructure upgrades, and skilled labor. For example, gas-insulated switchgear demands specialized handling and site preparation, which can delay project timelines and increase costs. Developing regions with constrained budgets may struggle to adopt advanced solutions, leading to slower modernization. Furthermore, the complexity of integrating new switchgear with aging transmission networks adds to technical challenges, requiring careful planning and advanced engineering expertise. These factors collectively act as hurdles for rapid adoption, especially in cost-sensitive markets.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction is creating strong demand for advanced solutions in the High Voltage Switchgear Market. Pre-engineered switchgear components manufactured off-site enhance precision and consistency, while reducing labor costs and installation timelines. Automated cutting and bending processes ensure higher efficiency, with Europe and North America witnessing increased adoption to meet strict deadlines in infrastructure and industrial projects. This trend is reshaping procurement strategies, as project developers prioritize suppliers offering prefabricated systems that improve scalability and reduce downtime.

• Shift Toward SF₆-Free Insulation Technologies: Environmental regulations targeting greenhouse gas emissions are accelerating the replacement of traditional SF₆-based switchgear with sustainable alternatives. Vacuum and fluoronitrile-based insulation technologies are gaining traction as utilities and industries aim to reduce their carbon footprint. Recent projects in Europe and Asia have successfully deployed SF₆-free solutions in high-voltage substations, demonstrating technical reliability and compliance with global climate commitments. This shift is expected to significantly expand across large-scale grid projects and renewable integration zones.

• Digital Switchgear and IoT Integration: The market is experiencing a surge in demand for digital switchgear equipped with IoT sensors and cloud-based monitoring. Utilities are leveraging real-time data analytics to improve asset health monitoring and predictive maintenance strategies. Deployment of AI-enabled systems allows remote diagnostics, minimizing field visits and reducing operational risks in hazardous environments. Growth in smart grid investments and urban electrification is fueling large-scale adoption of IoT-enabled high-voltage solutions, particularly in Asia-Pacific and North America.

• Growing Investments in Renewable Energy Infrastructure: Rising investments in solar, wind, and hydro power projects are directly boosting the High Voltage Switchgear Market. Renewable installations require reliable and flexible high-voltage connections to manage variable energy output and grid stability. In 2024, over 50% of new renewable capacity additions were paired with advanced switchgear systems, highlighting their central role in energy transition. The trend is particularly strong in developing economies focusing on electrification and clean energy adoption, driving long-term market growth.

The High Voltage Switchgear Market is segmented by type, application, and end-user, reflecting diverse adoption patterns across industries. By type, gas-insulated switchgear remains widely used for space-constrained environments, while air-insulated designs cater to cost-sensitive installations and hybrid variants bridge performance gaps. Applications span power generation, transmission, and distribution, with transmission substations leading demand due to grid expansion projects. End-users include utilities, industries, and commercial establishments, each driving distinct demand dynamics. Utilities dominate owing to grid modernization, while industrial sectors, particularly oil & gas and mining, are rapidly adopting advanced switchgear for operational resilience. Emerging opportunities lie in renewable energy and urban infrastructure projects, where technological innovation and environmental compliance are shaping adoption trends.

The High Voltage Switchgear Market features gas-insulated switchgear, air-insulated switchgear, and hybrid switchgear types, each serving specific operational needs. Gas-insulated switchgear (GIS) is the leading type due to its compact footprint, high reliability, and suitability for urban and space-limited installations. GIS is widely deployed in large cities, underground substations, and offshore platforms where space optimization is critical. Air-insulated switchgear (AIS), while less compact, remains significant for cost-efficient applications in rural and semi-urban transmission networks. The fastest-growing type is hybrid switchgear, combining the strengths of both GIS and AIS to deliver efficiency, modularity, and lower maintenance requirements. Hybrid designs are increasingly favored for grid modernization projects where scalability and reduced lifecycle costs are priorities. Other niche types, such as vacuum switchgear, are gaining attention in environmentally focused projects due to their SF₆-free insulation and growing compliance with global climate regulations. Together, these types ensure broad adaptability across infrastructure and industrial requirements.

Applications of High Voltage Switchgear span power generation, transmission, distribution, and industrial use. The leading application is transmission, driven by ongoing grid expansion and the need for reliable interconnections between renewable energy sources and national grids. Transmission substations heavily rely on high-voltage switchgear to ensure load stability and reduce losses over long distances. The fastest-growing application is renewable energy integration, where wind farms, solar plants, and hydroelectric projects require advanced switchgear to manage fluctuating generation patterns. Power generation facilities also contribute significantly, particularly in thermal and nuclear plants, where robust switchgear is critical for safe operations. Distribution networks represent another important segment, supporting urban expansion and rising electricity demand in residential and commercial areas. Industrial applications, including mining, oil & gas, and manufacturing, utilize high-voltage switchgear for energy-intensive operations, further strengthening the market base. Each application highlights the versatility of switchgear across diverse operational landscapes.

End-user segments in the High Voltage Switchgear Market include utilities, industrial enterprises, and commercial users. Utilities remain the leading end-user segment, with widespread deployment in power transmission and distribution networks. Large-scale investments in smart grids, urban electrification, and renewable integration projects make utilities the backbone of market demand. The fastest-growing end-user segment is the industrial sector, particularly in oil & gas, mining, and heavy manufacturing, where uninterrupted high-voltage supply is critical for operational efficiency. Industrial adoption is rising due to increasing automation, safety requirements, and demand for reliable power under harsh conditions. Commercial end-users, including large infrastructure projects, metro systems, and data centers, are also contributing significantly, with demand for compact, modular, and digitalized switchgear solutions. Growing electrification in transport and urban development further expands opportunities in this segment. Together, these end-user groups reflect a balanced yet evolving market landscape where utilities dominate, but industrial and commercial demand continues to accelerate.

Asia-Pacific accounted for the largest market share at 42% in 2024 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

The Asia-Pacific High Voltage Switchgear Market has benefited from rapid industrialization, urbanization, and large-scale grid expansion projects, especially in China and India, which dominate consumption patterns. Meanwhile, Middle East & Africa is witnessing accelerated investments in utility upgrades, renewable integration, and oil & gas infrastructure, which is fueling the demand for modern, digitalized switchgear systems. These dynamics underline the evolving regional balance in global market growth.

Smart Grid Integration Driving Technological Evolution

North America accounted for nearly 21% of the global High Voltage Switchgear Market in 2024, supported by investments in smart grid infrastructure and renewable energy projects. The region’s utilities and data center industries are major drivers of demand, with advanced switchgear ensuring reliable and efficient power distribution. Regulatory frameworks, such as mandates for SF₆ reduction and decarbonization targets, are pushing manufacturers toward sustainable insulation technologies. Digital transformation is also strong, with IoT-enabled switchgear and AI-driven monitoring systems increasingly deployed across power networks. Federal and state-level support for clean energy transitions further strengthens the region’s long-term outlook.

Sustainability Regulations Accelerating Market Adoption

Europe held approximately 24% of the High Voltage Switchgear Market share in 2024, driven by strong adoption in Germany, the UK, and France. The region’s sustainability initiatives, including directives to phase out SF₆, are significantly shaping product innovation. Regulatory bodies emphasize eco-friendly technologies, pushing utilities to adopt vacuum and alternative gas-insulated solutions. Emerging technologies such as modular switchgear and digital substations are being widely deployed to modernize aging infrastructure. Investment in offshore wind and cross-border interconnection projects further reinforces demand, making Europe a hub for environmentally advanced high-voltage systems.

Industrial Expansion and Urban Electrification Fueling Demand

Asia-Pacific dominated the global High Voltage Switchgear Market with 42% share in 2024, led by massive consumption in China, India, and Japan. China continues to lead with large-scale power grid upgrades and investments in ultra-high voltage transmission systems, while India accelerates renewable energy adoption and urban electrification. Japan’s technology-driven utilities focus on compact and modular switchgear for efficient space utilization. Rapid industrialization, expanding urban infrastructure, and manufacturing growth across Southeast Asia further drive switchgear demand. The region is also an innovation hub, with manufacturers developing SF₆-free and digital switchgear to meet both regulatory and efficiency standards.

Infrastructure Expansion Strengthening Power Distribution Systems

South America contributed nearly 7% of the global High Voltage Switchgear Market in 2024, with Brazil and Argentina being the primary consumers. Brazil’s expanding renewable energy sector, particularly wind and hydropower, drives steady demand for advanced switchgear installations. Argentina focuses on modernizing outdated transmission networks to reduce losses and improve reliability. Regional governments provide incentives for infrastructure expansion, including tax benefits for energy efficiency projects. Trade policies encouraging equipment imports have also increased access to digitalized and modular switchgear solutions, making the region an emerging growth area for global suppliers.

Energy Diversification and Infrastructure Modernization Shaping Growth

The Middle East & Africa accounted for 6% of the High Voltage Switchgear Market in 2024 and is forecast to grow at the fastest pace by 2032. Countries such as UAE, Saudi Arabia, and South Africa are driving adoption, supported by large-scale oil & gas projects, industrial expansion, and smart city initiatives. Demand is particularly strong for high-capacity and digital switchgear to support modern power distribution systems. Governments are actively diversifying energy portfolios, increasing investment in solar and wind, which requires reliable grid integration supported by advanced switchgear. Regional trade partnerships and regulatory reforms are further enhancing market opportunities.

China: 28% market share | Dominance attributed to large-scale production capacity and extensive investments in ultra-high voltage transmission projects.

Germany: 12% market share | Leadership driven by strong renewable energy integration and strict regulatory push for SF₆-free switchgear solutions.

The High Voltage Switchgear Market is characterized by a highly competitive environment with more than 50 active global and regional players offering diversified portfolios of air-insulated, gas-insulated, hybrid, and digitalized switchgear solutions. Competition is intense among established multinational corporations and emerging regional manufacturers, with players focusing heavily on innovation and sustainability. Strategic initiatives such as partnerships with utilities, technology collaborations, and mergers & acquisitions are shaping competitive positioning, particularly in Asia-Pacific and Europe. Product launches in SF₆-free switchgear and AI-enabled monitoring systems have gained strong momentum, as environmental compliance and digital transformation are increasingly prioritized by utilities and industries. Companies are investing in modular and compact switchgear designs to address urbanization challenges, while also strengthening local manufacturing capabilities to meet region-specific regulations. Furthermore, competitive intensity is heightened by the push for localized supply chains, technological differentiation, and customer-centric services such as predictive maintenance platforms and lifecycle support, which are becoming decisive factors in market leadership.

ABB Ltd

Siemens Energy AG

General Electric Company

Schneider Electric SE

Mitsubishi Electric Corporation

Toshiba Corporation

Eaton Corporation plc

Hyundai Electric & Energy Systems Co Ltd

Powell Industries Inc

Fuji Electric Co Ltd

The High Voltage Switchgear Market is undergoing a technological transformation driven by sustainability mandates, digitalization, and the integration of intelligent monitoring systems. One of the most significant advancements is the shift from SF₆-based insulation to eco-friendly alternatives such as vacuum, fluoronitrile blends, and CO₂-based technologies. These next-generation insulation systems address stringent environmental regulations while maintaining high performance under demanding operational conditions. For example, several utilities in Europe and Asia have successfully deployed SF₆-free high-voltage switchgear in projects above 145 kV, demonstrating both reliability and scalability for large transmission networks.

Digitalization is another key technological driver, with IoT-enabled switchgear gaining widespread adoption. Embedded sensors and real-time analytics provide predictive maintenance capabilities, reducing operational downtime and extending equipment lifespan. AI and cloud integration enable advanced asset management, remote monitoring, and fault detection, significantly improving grid resilience. The rise of digital substations that integrate high-voltage switchgear with communication technologies ensures better load management, particularly in regions integrating high levels of renewable energy.

Compact modular designs are also emerging as critical innovations, offering flexible installation options in space-constrained urban areas. These modular switchgear units simplify maintenance, reduce project timelines, and lower total lifecycle costs. Combined with the development of advanced arc-resistant switchgear and smart diagnostics, these technologies are redefining industry standards for safety, sustainability, and efficiency in power distribution.

• In February 2023, Siemens Energy launched its 420 kV Blue high-voltage switchgear using clean air insulation technology, eliminating the need for SF₆ and reducing greenhouse gas emissions in large-scale transmission projects.

• In July 2023, ABB introduced a new generation of digital switchgear integrated with real-time monitoring and predictive analytics, enabling utilities to improve asset performance and reduce unplanned outages by over 20%.

• In March 2024, Schneider Electric unveiled its SF₆-free air-insulated high-voltage switchgear designed for substations above 145 kV, enhancing sustainability compliance while maintaining operational reliability in densely populated regions.

• In May 2024, Mitsubishi Electric Corporation commissioned its 245 kV vacuum circuit breaker-based high-voltage switchgear in Japan, marking one of the largest deployments of SF₆-free technology for national grid operations.

The scope of the High Voltage Switchgear Market Report encompasses a detailed evaluation of technologies, applications, end-user industries, and geographic regions shaping global demand. The report highlights key product categories including gas-insulated, air-insulated, and hybrid switchgear, each serving diverse operational requirements across industrial, utility, and commercial installations. Advanced technologies such as digital switchgear, IoT-based monitoring systems, and SF₆-free insulation are also covered, reflecting the industry’s transition toward smarter and more sustainable solutions.

From an application standpoint, the scope spans power generation, transmission, and distribution networks, with particular emphasis on renewable integration, urban infrastructure expansion, and industrial electrification. Geographic coverage includes Asia-Pacific, Europe, North America, South America, and Middle East & Africa, each evaluated for market share, consumption patterns, and growth dynamics. Asia-Pacific dominates consumption due to large-scale grid expansion, while Europe and North America lead in adopting environmentally advanced and digitalized solutions.

The report further analyzes demand across key end-user segments such as utilities, heavy industries, and commercial sectors, outlining how modernization programs, regulatory pressures, and technological innovation drive adoption. Additionally, the scope extends to niche opportunities such as smart cities, offshore energy projects, and emerging economies investing in infrastructure upgrades. By providing comprehensive insights into both established and emerging segments, the report equips decision-makers with actionable intelligence to navigate the evolving High Voltage Switchgear Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 11035.08 Million |

|

Market Revenue in 2032 |

USD 15573.2578834306 Million |

|

CAGR (2025 - 2032) |

4.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ABB Ltd, Siemens Energy AG, General Electric Company, Schneider Electric SE, Mitsubishi Electric Corporation, Toshiba Corporation, Eaton Corporation plc, Hyundai Electric & Energy Systems Co Ltd, Powell Industries Inc, Fuji Electric Co Ltd |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |