Reports

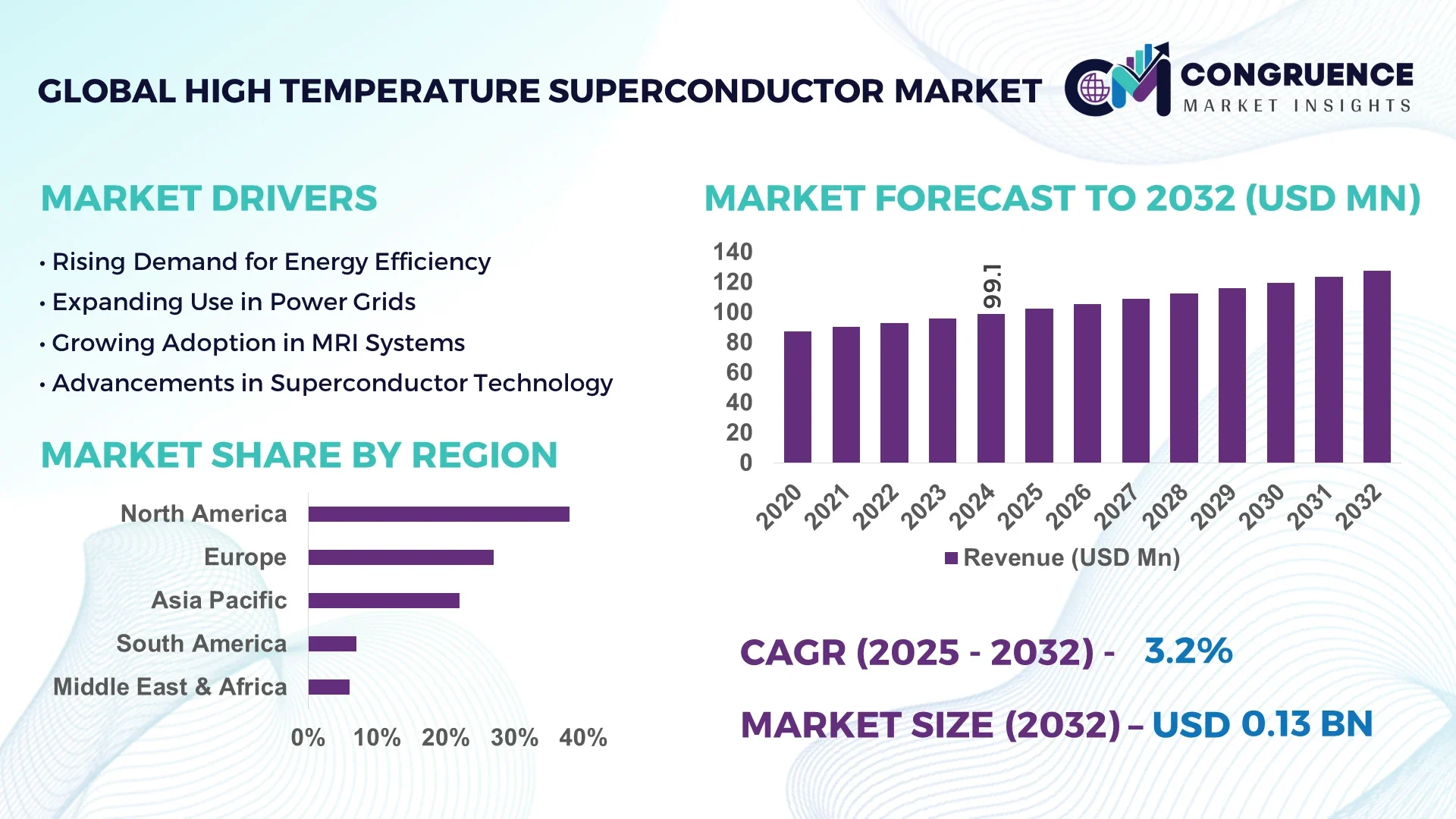

The Global High Temperature Superconductor Market was valued at USD 99.07 Million in 2024 and is anticipated to reach a value of USD 127.46 Million by 2032 expanding at a CAGR of 3.2% between 2025 and 2032.

Japan leads the High Temperature Superconductor Market with unparalleled production capacity in superconducting tapes and cables, substantial investment levels in scalable HTS wire manufacturing lines, prominent deployment in advanced applications such as fault current limiters and grid infrastructure, and cutting-edge materials development through industrial-academic collaborations focused on enhancing critical current density and mechanical flexibility.

Key industry sectors driving the High Temperature Superconductor Market include energy transmission, medical imaging, particle acceleration, energy storage systems, and electric motors. Power cable applications are forecast to grow from approximately USD 0.75 billion in 2024 to USD 1.5 billion by 2032, reflecting rising demand for high-efficiency transmission solutions. MRI systems within the healthcare segment are expected to expand from USD 0.55 billion to USD 1.1 billion over the same period, propelled by technological innovation and aging populations. Particle accelerators, energy storage, and electric motor applications each show significant upward trends, with respective growth to around USD 1.0 billion, USD 0.85 billion, and USD 0.55 billion by 2032. Regulatory drivers include government funding for grid modernization, renewable integration, and sustainability mandates, while economic factors such as rising energy costs and investments in efficient infrastructure further incentivize HTS adoption. Regionally, growth is pronounced in areas with dense urban energy demand and strong R&D ecosystems. Emerging trends feature advances in tape fabrication, flexible HTS wires, and superconducting compounds lowering cost barriers—all expanding market potential and enabling strategic decision-making for industry professionals.

Artificial intelligence is revolutionizing the High Temperature Superconductor Market by drastically enhancing material discovery and process optimization in a way that boosts efficiency and operational performance for industry stakeholders. Machine-learning algorithms now serve as powerful tools to predict superconducting critical temperatures and guide experimental synthesis more effectively, enabling decision-makers to concentrate resources on the most promising candidates. Deep-learning frameworks—including inverse design platforms—have surfaced; for example, an AI engine identified 74 previously unknown materials with predicted superconducting critical temperatures (Tₖ) above 15 K, significantly accelerating exploratory timelines and cutting trial-and-error costs. Another AI-accelerated workflow reduced a candidate pool of 1.3 million materials to just 741 with DFT-confirmed superconductivity above 5 K, delivering 87% precision and identifying viable materials for experimental validation. These AI tools streamline the HTS discovery pipeline, enabling higher throughput screening, more accurate property prediction, and faster advancement from theoretical models to lab-tested materials.

On the manufacturing and operational side, AI-driven models now inform fabrication processes by optimizing parameters based on historical synthesis data, improving consistency and yield across production lines for superconducting tapes. In deployed systems—such as superconducting cables or grid components—AI-based predictive maintenance and performance analytics are emerging, helping utilities anticipate failure modes and enhance reliability. The integration of AI also reduces the reliance on expensive low-temperature testing cycles by enabling precise virtual screening before committing to physical prototypes. Collectively, AI’s role in the High Temperature Superconductor Market spans accelerating discovery, boosting production efficiency, and strengthening deployed system performance—all without speculative revenue forecasts, focusing instead on measurable improvements that appeal directly to industry and R&D leaders.

“InvDesFlow, an AI search engine developed in 2024, uncovered 74 dynamically stable new high-Tₖ superconducting materials (Tₖ ≥ 15 K) not previously catalogued, enabling more targeted and efficient material discovery.”

The High Temperature Superconductor Market is characterized by a combination of technological advancement, infrastructure modernization, and growing demand for energy-efficient solutions. Trends indicate an increasing shift toward applications in power transmission, medical imaging, and advanced industrial systems, driven by their superior performance compared to conventional conductors. Key influences include government-backed research programs, advances in tape and wire fabrication technologies, and the expansion of renewable energy integration into national grids. The market also benefits from increasing adoption in compact, high-capacity electrical systems and the proliferation of smart grid projects in developed economies. Industry insights reveal that advancements in material composition, manufacturing scalability, and performance stability are enabling broader deployment across sectors that require high current density, reduced energy loss, and enhanced operational reliability.

The rapid modernization of global power grid infrastructure is a significant driver for the High Temperature Superconductor Market, as utilities seek to reduce transmission losses and improve efficiency. HTS cables offer up to 50% lower power losses compared to conventional copper conductors and can carry more than three times the electrical capacity within the same cross-sectional area. Major cities with dense urban demand are adopting superconducting cables for underground transmission, mitigating space constraints and environmental impact. For example, pilot projects in Asia and Europe have demonstrated the ability of HTS lines to deliver high-capacity, low-loss power across distances exceeding 10 km without the need for costly voltage conversion. This efficiency, combined with reduced maintenance requirements and resilience against overloads, positions HTS as a key enabler of sustainable and reliable power infrastructure expansion.

Despite performance advantages, the High Temperature Superconductor Market faces a major restraint in the form of high production and installation costs. Manufacturing HTS wires requires precise control of material purity, crystallographic alignment, and multilayer deposition, resulting in elevated production expenses. In addition, the need for cryogenic cooling systems—often liquid nitrogen-based—adds both initial and operational costs to HTS deployment. For many regions, particularly in developing economies, these cost barriers hinder widespread adoption despite potential long-term savings. Field data shows that installation costs for HTS cables can be two to three times higher than conventional alternatives, creating budgetary constraints for utilities and industrial operators. The lack of large-scale, standardized manufacturing facilities further prevents cost optimization, delaying mass-market penetration.

Technological innovation in second-generation (2G) HTS wire manufacturing presents a significant opportunity for the High Temperature Superconductor Market. New deposition techniques such as metal-organic chemical vapor deposition (MOCVD) and ion beam-assisted deposition (IBAD) are improving production speed and reducing material waste. These advancements enhance the critical current density and mechanical flexibility of HTS wires, making them more suitable for diverse applications, from offshore wind farm connections to compact urban substations. With some pilot production lines achieving lengths exceeding 1,000 meters without performance degradation, 2G HTS wires are moving toward industrial-scale adoption. Furthermore, the increasing availability of low-cost, high-quality substrates is expected to drive down per-meter costs, making HTS solutions competitive with high-grade copper in specialized high-demand environments.

One of the key challenges in the High Temperature Superconductor Market is the dependency on efficient cryogenic cooling systems to maintain operational superconductivity. While HTS materials can operate at higher temperatures than low-temperature superconductors, they still require cooling to 20–77 K, typically achieved with liquid nitrogen systems. The design, installation, and maintenance of this infrastructure remain technically demanding and costly. In remote or underdeveloped regions, the lack of reliable cryogen supply chains further complicates deployment. Additionally, operational risks such as cooling system failure can cause immediate loss of superconducting properties, leading to downtime and costly repairs. Efforts to integrate more compact, energy-efficient cryocoolers are ongoing, but scaling these technologies for large infrastructure projects remains an industry hurdle.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated conductor systems is transforming deployment methods in the High Temperature Superconductor Market. Pre-bent and precision-cut HTS elements are manufactured off-site using advanced automated machinery, significantly reducing labor requirements and accelerating installation timelines. This approach is particularly gaining momentum in Europe and North America, where urban space constraints and the need for rapid infrastructure upgrades make efficient construction critical. The trend also improves quality control, as components are produced in controlled environments before integration into power transmission projects.

• Breakthroughs in Critical Current Density Enhancement: Advancements in HTS tape engineering are delivering measurable increases in critical current density, with performance improvements exceeding 20% compared to previous-generation conductors. These gains are achieved through methods such as nano-engineered pinning centers and optimized deposition techniques, enabling higher current capacity without increasing conductor dimensions. Such improvements are particularly valuable for applications in high-energy research facilities, medical imaging systems, and urban transmission networks where space is limited but power demand is high.

• Growth in Superconducting Magnetic Energy Storage (SMES): SMES systems are becoming more prominent in the High Temperature Superconductor Market due to their exceptional round-trip efficiency, often exceeding 95%, and near-instantaneous power delivery. Modern SMES installations are increasingly used for grid stabilization, industrial power quality improvement, and renewable energy integration. Newer systems are capable of delivering multi-megawatt outputs in under 50 milliseconds, addressing the need for rapid response solutions in power networks facing variable loads and intermittent generation sources.

• Expansion into Quantum Computing and Advanced Electronics: The integration of HTS materials into quantum computing and advanced electronics is expanding rapidly. These materials enable ultra-low-resistance connections, stable high-frequency performance, and reduced power consumption in critical computing components. Developments in hybrid superconducting-semiconducting devices are showing improved switching speeds and energy efficiency over traditional semiconductor technologies. This trend is reinforcing HTS as a foundational material for next-generation computing architectures and high-performance defense and communication systems.

The High Temperature Superconductor Market is segmented by type, application, and end-user, each addressing specific operational requirements and technological demands. Product types include ceramic-based superconductors such as YBCO and Bismuth compounds, iron-based superconductors, organic superconductors, and magnesium diboride (MgB₂). Applications span energy transmission, medical imaging, quantum computing, magnetic energy storage, and research instrumentation. End-user segments range from energy utilities and healthcare providers to electronics manufacturers, transportation sectors, and defense agencies. This structured segmentation enables industry participants to align product innovation, manufacturing capabilities, and deployment strategies with sector-specific priorities.

The High Temperature Superconductor Market consists of ceramic superconductors (YBCO and Bismuth-based), iron-based superconductors, organic superconductors, and magnesium diboride (MgB₂). Ceramic superconductors dominate due to their high operating temperature capability, excellent critical current density, and proven reliability in demanding environments, making them ideal for power grid and industrial applications. The fastest-growing type is MgB₂, favored for its cost-effectiveness, simpler manufacturing processes, and suitability for cryogen-free cooling systems, which reduces operational complexity. Iron-based superconductors offer strong magnetic field tolerance, making them relevant for high-field magnet applications, while organic superconductors cater to niche uses in flexible and lightweight devices. The diversity within this segment ensures solutions are available for both mainstream and specialized market needs.

The leading application in the High Temperature Superconductor Market is power transmission and distribution, driven by the need for high-capacity, low-loss cables and fault current limiters that improve grid reliability. The fastest-growing application is in quantum computing and advanced electronics, where HTS materials enable faster processing, higher stability, and minimal power dissipation in critical systems. Medical imaging, particularly MRI technology, continues to be a significant application area, benefiting from HTS coils that provide stronger magnetic fields and enhanced imaging clarity. Additional applications include particle accelerators, superconducting magnetic energy storage units, and precision measurement instruments, all of which leverage the efficiency and performance advantages of HTS technologies.

Energy and power utilities are the primary end-users of high temperature superconductors, utilizing HTS cables, transformers, and fault limiters to modernize electrical networks and integrate renewable power sources. The fastest-growing end-user segment is the electronics and quantum technology industry, where the demand for superconducting components in computing, sensing, and high-speed communication systems is accelerating. Healthcare institutions represent another important user group, particularly in adopting HTS-enabled MRI systems that deliver improved diagnostic performance. Other contributing end-users include transportation sectors developing maglev train systems, research laboratories advancing high-field experiments, and defense organizations deploying HTS technology in radar, communications, and advanced weapon systems. This varied end-user base underscores the versatility and adaptability of HTS materials across industries.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.4% between 2025 and 2032.

The dominance of North America is driven by strong adoption of HTS technology in energy, healthcare, and research sectors, along with extensive investments in upgrading power grids. Meanwhile, Asia-Pacific’s rapid expansion is supported by large-scale infrastructure projects, growing manufacturing bases, and increasing government-backed innovation programs. Europe follows closely with advanced R&D capabilities and sustainability-focused deployment strategies, while other regions, including South America and the Middle East & Africa, are emerging with niche applications in industrial modernization and high-capacity transmission networks.

Advanced Grid Modernization and Medical Technology Integration Driving Demand

North America held a 38% share of the High Temperature Superconductor Market in 2024, driven by extensive investments in smart grid modernization, medical imaging, and superconducting energy storage projects. Key industries such as power utilities, healthcare, and advanced research facilities are leading demand. Regulatory frameworks promoting renewable integration and grid efficiency are accelerating adoption, supported by funding for innovative pilot projects. Technological advancements in cryogen-free cooling and higher-current HTS cables are improving cost-effectiveness and operational efficiency. The region’s mature infrastructure and strong private-public collaboration make it a critical hub for ongoing HTS innovation.

Innovative Energy Transition Strategies Accelerating Superconductor Adoption

Europe accounted for 27% of the High Temperature Superconductor Market in 2024, with Germany, the UK, and France leading installations in energy and healthcare sectors. The market is supported by strong policy frameworks under EU energy efficiency and sustainability directives, encouraging the deployment of low-loss transmission lines and superconducting fault current limiters. Advancements in HTS-based MRI technology and large-scale renewable integration projects are fueling demand. Regulatory bodies are actively promoting carbon reduction goals, making superconductors a strategic technology in achieving energy transition targets. The region also benefits from coordinated research networks and well-funded pilot projects across member states.

Expanding Infrastructure and Manufacturing Ecosystems Powering Growth

Asia-Pacific represented 22% of the High Temperature Superconductor Market in 2024, with China, Japan, and India being the largest consumers. The region’s growth is driven by rapid urbanization, industrial expansion, and massive investments in energy transmission infrastructure. China leads with large-scale HTS cable installations, while Japan focuses on precision medical imaging and maglev transportation. India is emerging as a strong market with initiatives to strengthen power reliability and renewable integration. Technology hubs in Japan and China are developing advanced conductor manufacturing capabilities, improving supply chain resilience and reducing production costs across the region.

Energy Sector Modernization Boosting High-Efficiency Transmission Adoption

South America accounted for 7% of the High Temperature Superconductor Market in 2024, led by Brazil and Argentina. Brazil’s demand is driven by upgrades in long-distance power transmission networks and renewable integration, while Argentina focuses on energy storage and industrial applications. The region is benefiting from targeted government incentives promoting grid efficiency and the adoption of advanced materials. Infrastructure development projects in both urban and remote areas are increasingly specifying HTS-based solutions to reduce energy losses and improve operational reliability. Regional universities and research centers are also contributing to localized innovation in conductor manufacturing.

Industrial Diversification and Advanced Infrastructure Projects Creating Demand

The Middle East & Africa held a 6% share of the High Temperature Superconductor Market in 2024, with the UAE and South Africa leading adoption. In the Middle East, HTS deployment is linked to high-capacity power distribution for mega infrastructure projects and oil & gas sector modernization. In Africa, South Africa’s investments in grid resilience and medical imaging technology are expanding market potential. Technological modernization, including the use of superconductors in desalination plant power systems and large-scale renewable projects, is gaining momentum. Strategic trade partnerships and local regulatory frameworks are improving access to HTS technology across the region.

United States – 28%

Strong dominance due to extensive HTS deployment in smart grid upgrades, large-scale R&D facilities, and advanced medical imaging systems.

China – 21%

Leadership driven by rapid industrial adoption, large-scale HTS cable projects, and strong domestic manufacturing capacity for advanced conductors.

The High Temperature Superconductor market is characterized by a moderately concentrated competitive environment, with approximately 25 to 30 active global and regional players driving innovation and market expansion. Leading companies hold strong positions through extensive R&D capabilities, diversified product portfolios, and robust supply chain integration. Strategic partnerships between technology providers and end-user industries are becoming increasingly common, aimed at accelerating commercialization and expanding application areas such as power transmission, medical imaging, and transportation systems. Mergers and acquisitions are reshaping the competitive structure, enabling companies to access advanced manufacturing processes and enhance production efficiency. Product innovation is a key differentiator, with a growing emphasis on developing cost-effective HTS cables, fault current limiters, and superconducting magnets that meet evolving performance and sustainability requirements. Competitors are also focusing on localization strategies, setting up regional manufacturing hubs to improve supply chain resilience and reduce lead times. The market is further influenced by advancements in cryogen-free cooling systems, enabling broader adoption across industries previously limited by infrastructure and operational constraints. Overall, the competitive dynamics favor firms with strong technological capabilities, global outreach, and the agility to adapt to rapid shifts in industrial demand.

American Superconductor Corporation

Bruker Energy & Supercon Technologies Inc.

Sumitomo Electric Industries Ltd.

Furukawa Electric Co. Ltd.

SuperPower Inc.

Fujikura Ltd.

Theva Dünnschichttechnik GmbH

Shanghai Superconductor Technology Co. Ltd.

SuperOx Group

Oxford Instruments plc

The High Temperature Superconductor market is being significantly shaped by a host of current and emerging technologies that are enhancing performance and expanding applicability. Innovations in conductor fabrication are at the forefront, with improvements such as nanometer-scale inclusions of insulating materials—like barium zirconate—being integrated into superconducting tapes. These enhancements enable record-setting critical current densities without increasing manufacturing complexity, making HTS cables more compact and efficient. Advances in material science are also pushing the boundaries of operating conditions. Researchers have stabilized novel HTS compounds that remain superconducting at room pressure, a breakthrough that opens doors to deployment in practical urban and industrial settings where high-pressure environments are infeasible. This shift represents a significant step toward mainstream, scalable HTS systems for power grids and quantum infrastructure.

In parallel, the fusion energy sector is leveraging HTS technology to build more compact and efficient tokamak reactors. Recent deployments—such as the HH70 tokamak—use exclusively high-temperature superconductors for magnet systems, reducing cooling requirements and operational complexities. Another innovation trajectory lies in accelerator and photon-source technologies. High-temperature superconducting undulators and fast-cycling HTS accelerator magnets are offering superior ramping rates and low AC losses, meeting the demanding operational parameters of next-generation particle research facilities. Additionally, HTS applications are broadening into smart electrical systems. Superconducting devices—including fault current limiters, power transformers, and lightweight motors—are being developed for grid modernization and sustainable transport. These systems benefit from HTS’s low thermal loss and compact form, making them attractive in urban and energy-constrained environments.

Collectively, these technology trends—enhanced conductor performance, ambient-pressure materials, fusion and accelerator integration, and smart infrastructure components—are driving the evolution of HTS from niche research to real-world deployment, offering powerful tools for decision-makers navigating the energy transition and advanced industrial landscapes.

• In June 2024, a Chinese fusion program completed the HH70 tokamak, the first device to use exclusively high-temperature superconductors in its magnet system, achieving its first plasma and marking a milestone in compact fusion demonstrators.

• In early 2024, researchers unveiled a novel method to twist and manipulate cuprate superconductors, enabling the creation of previously unattainable superconducting forms and offering new pathways for material engineering.

• In a 2023 breakthrough, MIT and Commonwealth Fusion Systems demonstrated that their high-temperature superconducting magnets meet the performance requirements needed for cost-effective, compact fusion power plants, confirming fusion readiness.

• In mid-2023, laboratories achieved a room-pressure high-temperature superconducting material, bringing the prospect of practical, lossless power transmission and advanced quantum device integration closer to realization.

This High Temperature Superconductor Market Report encompasses extensive coverage of technology types, application domains, regional markets, and industry verticals, providing decision-makers with a comprehensive strategic framework.

The report assesses both 1G and 2G HTS products, exploring conductor forms such as coated tapes, round wires, and bulk elements designed for varied service conditions. It examines applications including power transmission lines, fault current limiters, transformers, magnetic energy storage systems, MRI and NMR imaging systems, fusion-based power generation, high-field accelerator magnets, quantum computing interconnects, and superconducting motors and generators.

Geographically, the analysis spans developed and emerging markets across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Within each region, the report evaluates infrastructure development, R&D ecosystems, manufacturing capabilities, and deployment patterns in energy, healthcare, transportation, and defense sectors.

Additionally, it highlights emerging and niche segments such as cryogen-free HTS systems, ambient-pressure superconducting materials, integration in sustainable aviation and smart grid applications, and specialized components for photon-source facilities.

The report also profiles strategic market elements—competitive players, innovation trends, technology adoption rates, regulatory drivers, and supply-chain dynamics—structured to support corporate planning, investment decisions, and technology adoption strategies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 99.07 Million |

|

Market Revenue in 2032 |

USD 127.46 Million |

|

CAGR (2025 - 2032) |

3.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

American Superconductor Corporation, Bruker Energy & Supercon Technologies Inc., Sumitomo Electric Industries Ltd., Furukawa Electric Co. Ltd., SuperPower Inc., Fujikura Ltd., Theva Dünnschichttechnik GmbH, Shanghai Superconductor Technology Co. Ltd., SuperOx Group, Oxford Instruments plc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |