Reports

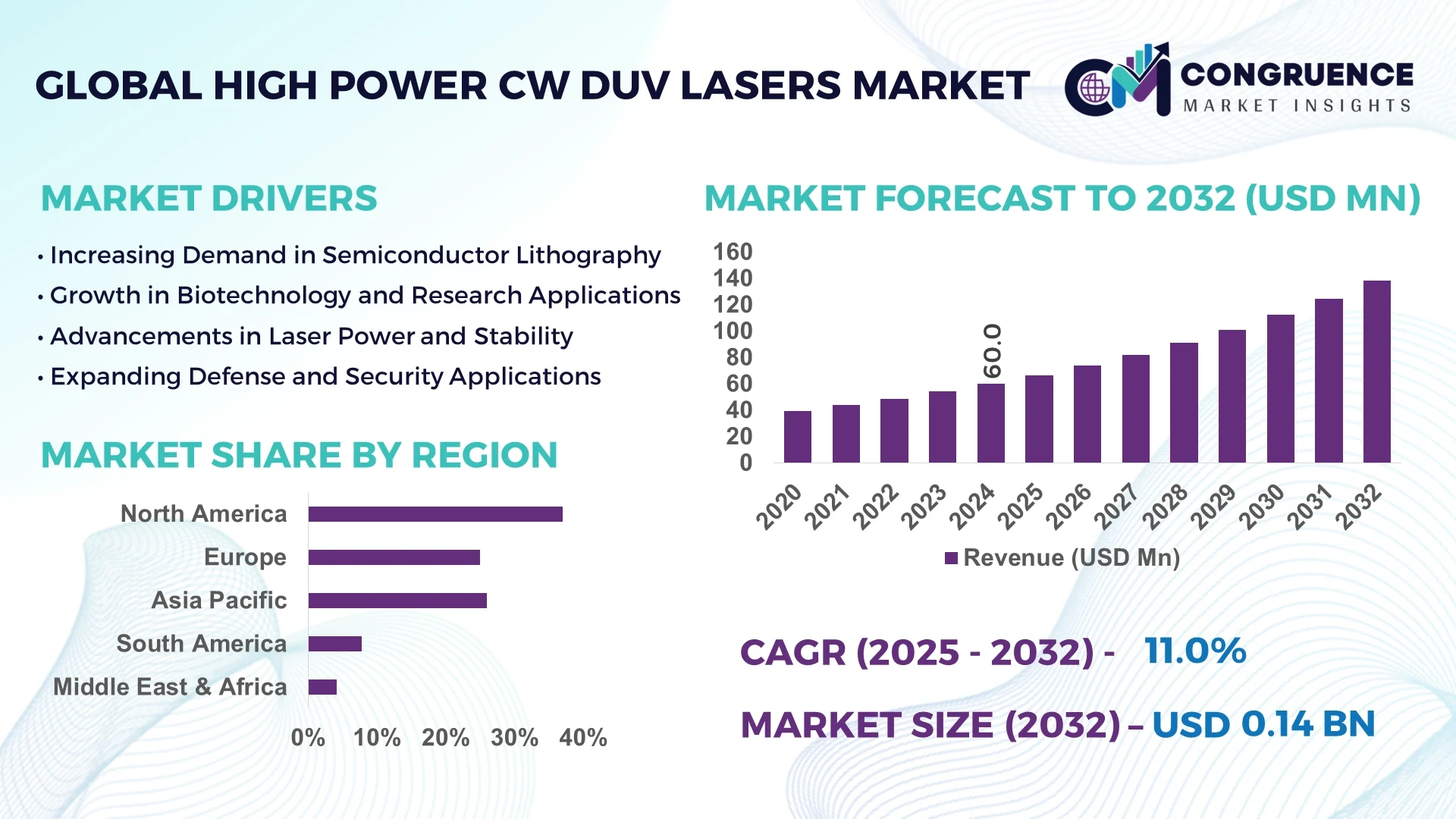

The Global High-Power CW DUV Lasers Market was valued at USD 60 Million in 2024 and is anticipated to reach a value of USD 138.3 Million by 2032 expanding at a CAGR of 11% between 2025 and 2032.

The United States plays a pivotal role in shaping the industry through its advanced production facilities, strong government-backed R&D programs, and extensive adoption of DUV lasers across semiconductor lithography, medical diagnostics, and defense-related optical technologies. The country’s significant investment in scaling production capacity and continuous innovations in ultraviolet laser sources strengthens its position as a global leader.

The High-Power CW DUV Lasers Market is characterized by its strong integration across critical industries including semiconductors, biotechnology, pharmaceuticals, and materials science. Semiconductor manufacturing continues to hold the largest share, driven by the need for precision lithography and advanced microelectronics. In biotechnology, these lasers are increasingly applied in high-resolution imaging and genomic sequencing, contributing to significant advancements in life sciences research. Recent innovations include enhanced beam stability, longer operational lifetimes, and the introduction of AI-driven calibration tools improving system performance. Regulatory support for cleanroom manufacturing standards and stringent environmental regulations in laser production have further shaped the market landscape. Regionally, Asia Pacific is emerging as a key consumer due to rapid electronics manufacturing growth, while North America leads in technological breakthroughs. Looking ahead, the market is expected to benefit from increasing demand in advanced nanofabrication, medical imaging, and photonics-based security solutions, highlighting a future of sustained expansion and continuous innovation.

Artificial Intelligence (AI) is fundamentally reshaping the High-Power CW DUV Lasers Market by driving efficiency, precision, and optimization across production and application workflows. In semiconductor manufacturing, AI-powered monitoring systems enhance beam alignment accuracy, leading to defect reduction rates of over 30% in advanced lithography processes. This not only improves yield but also extends equipment life cycles by predicting maintenance requirements before failures occur. In biotechnology applications, AI-driven image processing integrated with DUV laser platforms has improved cellular imaging clarity, allowing laboratories to achieve data acquisition speeds nearly 40% faster compared to traditional methods. Additionally, AI algorithms are being deployed for process automation, enabling continuous performance optimization in laser wavelength stabilization, thermal management, and energy efficiency.

The integration of AI into laser system design has also reduced operational variability, providing consistent performance in critical industries such as aerospace and defense. Predictive analytics further supports manufacturers in minimizing downtime, optimizing energy consumption, and enhancing throughput. As the High-Power CW DUV Lasers Market advances, AI-driven tools are expected to play an even larger role in precision nanofabrication and next-generation photonics. By combining machine learning models with real-time laser diagnostics, stakeholders across industries are gaining measurable productivity improvements and cost reductions, positioning AI as a transformative force in this sector.

“In 2025, a leading U.S.-based semiconductor equipment manufacturer integrated AI-powered real-time beam stabilization into its High-Power CW DUV Lasers, achieving a 25% improvement in lithography throughput while reducing alignment errors by 18%.”

The High-Power CW DUV Lasers Market is shaped by dynamic factors including evolving technology, stringent regulatory standards, and sector-specific demands. Continuous improvements in laser design are enabling longer lifetimes, greater stability, and superior beam quality, making them indispensable in semiconductor lithography and life sciences. Industry trends also point toward growing adoption in nanotechnology research, where high-precision ultraviolet light is critical for advanced material characterization. The market is influenced by global investments in photonics research and national initiatives supporting semiconductor independence. Environmental compliance requirements around laser manufacturing and energy efficiency also drive innovation, while increasing demand from biotechnology and healthcare is broadening the scope of applications.

The increasing complexity of semiconductor architectures is driving greater reliance on high-precision laser systems, making the High-Power CW DUV Lasers Market a cornerstone of the chip-making industry. Advanced lithography nodes below 5 nm demand highly stable and powerful DUV sources to ensure defect-free patterning. In 2024, semiconductor fabrication facilities in Taiwan and South Korea reported enhanced yields using continuous-wave DUV laser platforms, enabling tighter process control and reduced wafer wastage. The deployment of these lasers has also allowed manufacturers to increase throughput without expanding physical production lines, directly addressing cost-efficiency concerns.

Despite technological progress, the High-Power CW DUV Lasers Market faces challenges due to high system acquisition and maintenance costs. Continuous-wave DUV lasers require sophisticated cooling, alignment, and stabilization systems, often raising operational expenditures for manufacturers. For example, advanced lithography systems incorporating these lasers can demand annual service contracts costing several million dollars, limiting adoption among smaller enterprises. Moreover, maintaining consistent output under demanding cleanroom conditions requires specialized personnel and infrastructure, creating further barriers. These factors collectively restrict broader market penetration despite proven performance benefits.

The High-Power CW DUV Lasers Market is finding new opportunities in biotechnology and genomic research where ultra-precise imaging and sequencing are required. In 2025, advanced DUV laser platforms enabled higher throughput in single-cell analysis, allowing laboratories to process 20% more samples per hour compared to conventional methods. As precision medicine grows in importance, demand for accurate, non-invasive diagnostic tools powered by DUV lasers is increasing. Additionally, ongoing research into photonics-assisted drug discovery highlights untapped applications for continuous-wave DUV systems, creating fertile ground for investment and innovation in the biotechnology sector.

One of the persistent challenges in the High-Power CW DUV Lasers Market is managing energy consumption and heat dissipation. Continuous-wave lasers generate substantial thermal loads, which can compromise beam stability and reduce equipment lifespan. Manufacturers are investing in advanced cooling technologies, but these add to both system complexity and cost. In 2024, several production facilities reported efficiency losses exceeding 12% due to inadequate thermal management strategies. Addressing these issues remains critical to ensuring reliability and scalability in high-volume industrial applications, making energy efficiency a central challenge for future growth.

Integration of Advanced Cooling Systems: Thermal management is becoming a focal point for the High-Power CW DUV Lasers Market. Manufacturers are introducing closed-loop liquid cooling modules that reduce energy losses by up to 15% while maintaining stable output power. This trend is especially relevant for semiconductor fabs that require continuous, uninterrupted operation.

Automation in Laser Calibration: Automated AI-enabled calibration tools are gaining traction, reducing manual intervention and minimizing errors. In 2025, several European facilities reported achieving alignment times 40% faster, improving both productivity and system uptime. This reflects a broader move toward fully automated laser ecosystems.

Expansion into Photonics Security Applications: The High-Power CW DUV Lasers Market is witnessing growing adoption in security and defense, particularly in anti-counterfeiting and photonic encryption. High-resolution ultraviolet lasers are being deployed to create tamper-proof identifiers for sensitive documents and defense-grade components, broadening the scope of applications.

Sustainability and Energy-Efficient Designs: Eco-friendly product design is emerging as a significant trend, with manufacturers adopting recyclable materials and energy-efficient laser diodes. Facilities adopting these designs have reported a 10% reduction in overall operational carbon footprints, aligning with global sustainability goals while maintaining competitive performance.

The High-Power CW DUV Lasers Market is segmented by type, application, and end-user, each reflecting distinct patterns of demand and adoption across global industries. By type, the market covers excimer lasers, solid-state DUV lasers, and other niche variants that provide specialized performance benefits. Applications span semiconductor lithography, biotechnology research, materials processing, and defense-related photonics, highlighting the versatile role of DUV lasers in precision-driven fields. End-users range from semiconductor manufacturers and research institutions to healthcare providers and defense organizations, with each category exhibiting unique demand characteristics. Collectively, these segments demonstrate how evolving technological requirements and industry-specific needs are shaping market growth, investment priorities, and innovation strategies.

Excimer lasers represent the leading type in the High-Power CW DUV Lasers Market, largely due to their established role in advanced semiconductor lithography. Their ability to deliver high-power ultraviolet output with exceptional beam uniformity makes them essential for producing microchips at sub-10 nm nodes, driving their sustained dominance. Solid-state DUV lasers, while historically a smaller category, are emerging as the fastest-growing segment. Improvements in efficiency, compact design, and extended operational lifetimes are making them increasingly attractive for biotechnology, nanofabrication, and research applications, particularly in laboratories where reduced maintenance and smaller footprints are valued. Other types, such as hybrid and tunable DUV laser systems, serve niche needs in defense optics and specialized material sciences. While their overall contribution is smaller, their relevance lies in highly technical projects requiring tailored beam characteristics. The combination of excimer dominance and the rapid rise of solid-state technologies underscores a shifting balance within the type segmentation landscape.

Semiconductor lithography remains the leading application in the High-Power CW DUV Lasers Market, driven by continuous advancements in chip architectures and the requirement for extreme precision in patterning. These lasers enable reliable and consistent production of integrated circuits with minimal defects, supporting the growing global demand for high-performance computing and consumer electronics. Biotechnology applications are emerging as the fastest-growing area, fueled by innovations in genomic sequencing, advanced microscopy, and single-cell analysis that increasingly rely on DUV laser technology. Materials processing, including photonic surface structuring and thin-film deposition, represents another important application, with steady demand from industries focused on high-performance materials. Defense and security applications, such as high-resolution imaging and anti-counterfeiting measures, are also gaining momentum, though they currently occupy a more specialized role. Together, these application segments illustrate both the dominance of semiconductors and the rising importance of life sciences and defense in shaping future demand.

Semiconductor manufacturers are the leading end-users of the High-Power CW DUV Lasers Market, as their reliance on these systems for advanced lithography and wafer inspection remains unmatched. The push toward smaller, more powerful chips across consumer electronics, automotive electronics, and data centers ensures consistent demand. Research institutions and laboratories represent the fastest-growing end-user segment, supported by significant funding in life sciences, nanotechnology, and photonics. These organizations are adopting DUV lasers to achieve breakthroughs in genomic research, material analysis, and quantum optics. Healthcare providers, particularly in advanced diagnostic imaging and non-invasive treatment systems, also contribute steadily to market expansion. Defense and aerospace organizations, while smaller in share, are increasing their use of DUV lasers in security, surveillance, and strategic optical technologies. Collectively, this segmentation highlights a strong industrial backbone with semiconductors at the forefront, complemented by rapid uptake in research and growing contributions from healthcare and defense.

North America accounted for the largest market share at 37% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12% between 2025 and 2032.

The global High-Power CW DUV Lasers Market exhibits strong regional variation, with North America leading due to its established semiconductor fabrication hubs and early adoption of cutting-edge photonics. Europe maintains steady growth, supported by advanced research institutions and sustainability-driven regulations. Asia-Pacific is witnessing rapid expansion with China, Japan, and South Korea emerging as manufacturing powerhouses, while India is strengthening its research and industrial base. South America and the Middle East & Africa, though smaller in market size, are experiencing rising adoption in healthcare, materials processing, and energy sectors, supported by government initiatives and infrastructure modernization.

North America holds a commanding 37% share of the High-Power CW DUV Lasers Market, supported by its robust semiconductor and biotechnology industries. The United States leads the region with extensive investments in advanced lithography equipment and defense photonics. Regulatory bodies have introduced favorable frameworks to encourage domestic semiconductor production, including subsidies for fabrication plants. Technological innovation is accelerating adoption, with AI-driven calibration systems and advanced cooling technologies improving operational reliability. Canada contributes through growing research in photonics and medical imaging, while Mexico’s expanding electronics manufacturing base adds further demand. Collectively, these factors sustain North America’s leadership in the market.

Europe represents around 28% of the High-Power CW DUV Lasers Market, with Germany, the UK, and France serving as the primary contributors. Germany leads with its strong semiconductor equipment manufacturing base and advanced R&D facilities. The UK is investing heavily in biotechnology applications, while France drives adoption in defense and aerospace photonics. Regulatory emphasis from the European Commission on sustainable manufacturing practices and clean energy compliance is shaping procurement and product design. The adoption of emerging technologies such as photonic encryption and AI-integrated diagnostics is also accelerating growth. Europe’s commitment to green technology and precision manufacturing ensures steady market expansion.

Asia-Pacific accounts for approximately 25% of the High-Power CW DUV Lasers Market and is the fastest-growing regional segment. China dominates consumption due to its vast semiconductor and electronics industries, while Japan remains a leader in high-precision photonics research and advanced nanofabrication. South Korea continues to expand its semiconductor manufacturing capacity, further driving demand for high-power ultraviolet systems. India is emerging as a promising hub with investments in photonics R&D and biotechnology infrastructure. The region benefits from government-backed initiatives to strengthen domestic technology ecosystems and the presence of innovation clusters focusing on AI-driven manufacturing and next-generation semiconductor production.

South America contributes about 6% to the global High-Power CW DUV Lasers Market, with Brazil and Argentina being the primary markets. Brazil is advancing adoption in medical imaging, research laboratories, and materials processing, supported by an expanding healthcare infrastructure. Argentina shows potential in renewable energy-related photonics applications and academic research in nanotechnology. Regional governments are offering incentives to attract international photonics manufacturers, while trade policies aim to strengthen cross-border technology transfer. Despite smaller scale compared to North America and Asia, South America is steadily carving its role in research-focused and energy-driven applications of DUV lasers.

The Middle East & Africa region represents about 4% of the High-Power CW DUV Lasers Market, with the UAE and South Africa emerging as the leading contributors. The UAE is investing in defense optics, advanced construction materials, and smart city infrastructure powered by photonics. South Africa is expanding adoption in research institutions and mining-related material analysis. Regional demand is also influenced by oil and gas sectors adopting DUV-based inspection technologies. Local regulations encouraging modernization of industrial equipment and trade partnerships with Europe and Asia are facilitating technology transfer. Although in an early stage, the region shows strong potential for diversified growth.

United States – 25% Market Share

Dominance driven by advanced semiconductor fabrication capacity and strong defense-sector adoption of photonics.

China – 20% Market Share

Leadership supported by large-scale electronics manufacturing and continuous investment in photonics research and industrial applications.

The High-Power CW DUV Lasers Market is characterized by an increasingly competitive environment with over 25 globally active companies engaged in production, R&D, and system integration. Competition is primarily shaped by technological leadership, product reliability, and application-specific customization. Leading players maintain their market position by investing heavily in innovation, particularly in enhancing beam stability, extending operational lifetimes, and integrating AI-driven calibration tools. Strategic initiatives such as cross-border partnerships, joint ventures with semiconductor manufacturers, and collaborative research with biotechnology firms are becoming common, enabling companies to align closely with industry demand.

Mergers and acquisitions have been a defining feature of recent years, allowing firms to expand their geographical presence and diversify their product portfolios. Competitors are also increasingly adopting sustainability-focused initiatives, such as energy-efficient designs and recyclable laser modules, to comply with evolving environmental regulations. Continuous product launches highlight the industry’s commitment to meeting demand for advanced photonics in sectors such as semiconductors, biotechnology, and defense. This competitive intensity fosters rapid innovation cycles and compels companies to differentiate through both technical excellence and service-oriented strategies.

Coherent Corp.

Gigaphoton Inc.

Cymer (an ASML company)

Hamamatsu Photonics K.K.

Ushio Inc.

NTT Advanced Technology Corporation

TRUMPF GmbH + Co. KG

Nikon Corporation

Jenoptik AG

KLA Corporation

Technological advancements are redefining the High-Power CW DUV Lasers Market, with innovations aimed at improving performance, energy efficiency, and adaptability across critical industries. Excimer laser technology remains the cornerstone of semiconductor lithography, offering high-power ultraviolet output essential for advanced sub-10 nm node production. Solid-state DUV lasers are increasingly favored for their compact size, longer lifespans, and reduced maintenance requirements, making them particularly suitable for biotechnology research and high-precision imaging applications.

Recent developments include AI-enhanced beam stabilization systems that reduce alignment errors by up to 20%, ensuring consistent performance in semiconductor fabs and research labs. Thermal management technologies are also advancing, with closed-loop liquid cooling systems lowering energy consumption by approximately 15% while maintaining high output stability. Hybrid and tunable DUV laser systems are gaining traction in specialized areas such as defense optics and nanotechnology research, where customized beam properties are critical.

Emerging trends highlight the integration of lasers with digital twins and IoT-based monitoring platforms, allowing predictive maintenance and real-time performance optimization. In addition, sustainability is becoming a core driver, with manufacturers increasingly adopting recyclable components and energy-efficient designs to reduce environmental impact. These technological innovations collectively strengthen the strategic importance of DUV lasers across semiconductors, life sciences, defense, and advanced materials sectors, underscoring their pivotal role in future photonics applications.

In February 2023, Coherent Corp. expanded its excimer laser production capacity at its U.S. facility, adding 20% more output to support increasing semiconductor lithography demand and shorten delivery lead times for global customers.

In September 2023, Gigaphoton Inc. introduced an advanced DUV laser system featuring AI-powered monitoring, achieving a 15% improvement in operational uptime and reducing lithography defect rates in semiconductor manufacturing.

In April 2024, Hamamatsu Photonics unveiled a next-generation solid-state DUV laser optimized for biomedical imaging, enabling researchers to conduct high-resolution cellular analysis with 25% greater efficiency compared to earlier models.

In July 2024, Ushio Inc. launched a compact CW DUV laser system designed for nanofabrication, delivering improved beam uniformity and cutting system footprint by nearly 30%, enhancing suitability for smaller research labs.

The scope of the High-Power CW DUV Lasers Market Report covers an in-depth analysis of global industry dynamics, segmentation, regional developments, and technological trends influencing adoption. The report examines market segmentation by type, including excimer lasers, solid-state DUV lasers, hybrid variants, and tunable systems, each serving distinct roles across industrial and research applications. Application-based coverage highlights semiconductor lithography, biotechnology, materials processing, defense, and emerging sectors such as photonic security and nanotechnology.

Regional insights extend to North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with a focus on consumption patterns, industrial ecosystems, and government-led initiatives supporting adoption. The report also evaluates end-user segments such as semiconductor manufacturers, research institutions, healthcare providers, and defense organizations, identifying evolving demand characteristics.

Additionally, the report addresses critical technological insights, highlighting innovations in beam stability, cooling systems, digital integration, and sustainability-focused designs. It also reviews the competitive landscape, profiling leading companies and their strategic initiatives including partnerships, acquisitions, and product innovations. By covering established applications and emerging niches alike, the report provides decision-makers with a holistic understanding of the market’s present and future, enabling informed investment and strategic planning across multiple industries and geographies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 60 Million |

| Market Revenue (2032) | USD 138.3 Million |

| CAGR (2025–2032) | 11% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Coherent Corp., Gigaphoton Inc., Cymer (an ASML company), Hamamatsu Photonics K.K., Ushio Inc., NTT Advanced Technology Corporation, TRUMPF GmbH + Co. KG, Nikon Corporation, Jenoptik AG, KLA Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |