Reports

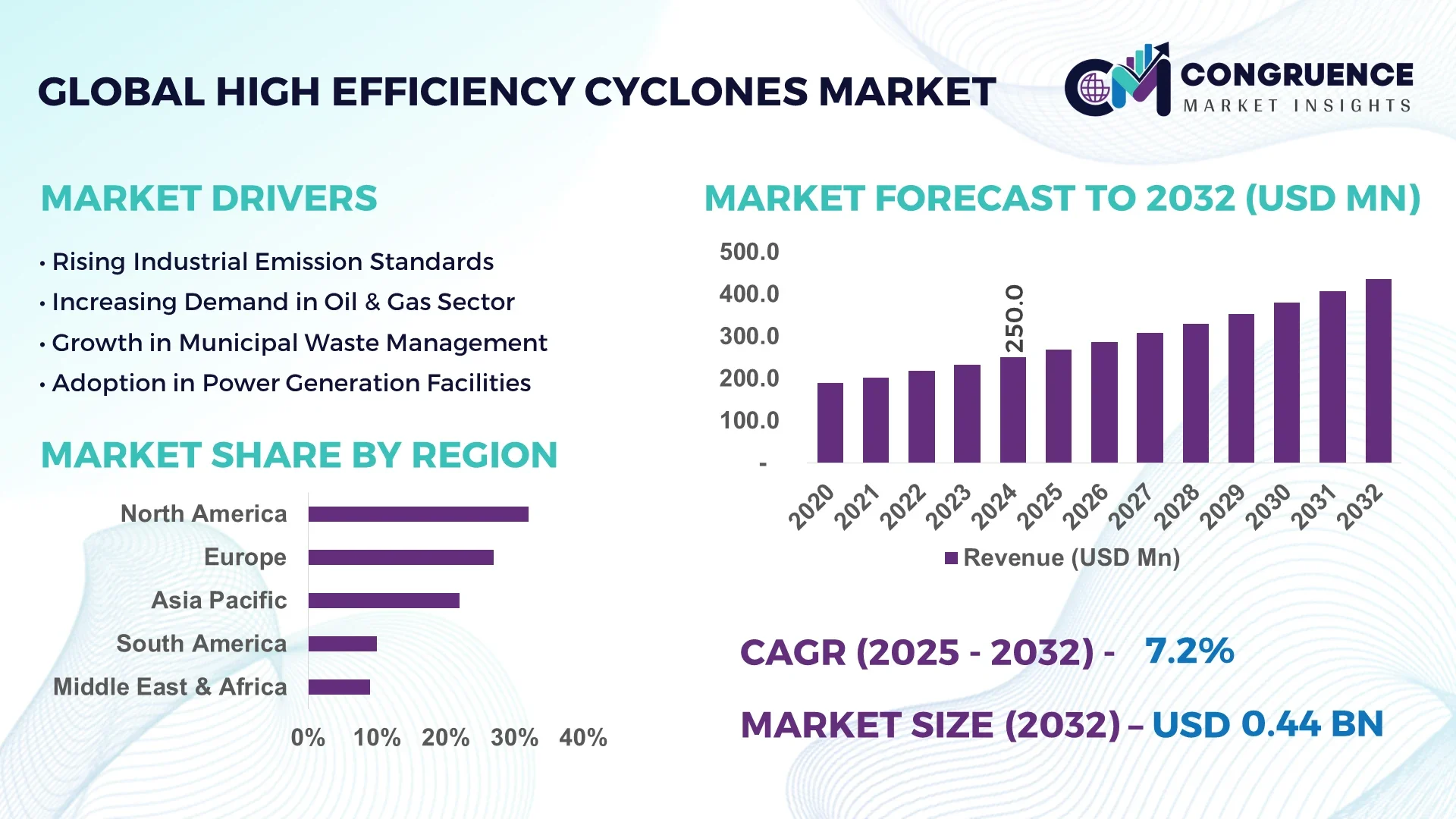

The Global High Efficiency Cyclones Market was valued at USD 250 Million in 2024 and is anticipated to reach a value of USD 436.0 Million by 2032, expanding at a CAGR of 7.2% between 2025 and 2032. This growth is primarily driven by increasing industrialization, stringent environmental regulations, and advancements in cyclone technology.

The United States leads the global High Efficiency Cyclones market, characterized by substantial production capacity and significant investments in advanced separation technologies. The oil and gas sector, particularly in Texas and Louisiana, is a major consumer, utilizing high-efficiency cyclones for particulate removal in refining processes. Technological advancements, such as the development of multi-stage cyclone systems and computational fluid dynamics (CFD)-optimized designs, have enhanced separation efficiency and energy consumption. The U.S. government's stringent environmental regulations further drive the adoption of high-efficiency cyclones across various industries.

Market Size & Growth: Valued at USD 250 million in 2024, projected to reach USD 436.0 million by 2033, with a CAGR of 7.2%. Growth is fueled by industrial expansion and environmental regulations.

Top Growth Drivers: Industrial growth (30%), environmental regulations (25%), technological advancements (20%).

Short-Term Forecast: By 2028, performance gains of up to 15% in particulate removal efficiency are expected.

Emerging Technologies: Integration of AI for predictive maintenance, CFD-optimized cyclone designs, hybrid filtration systems.

Regional Leaders: North America: USD 1.2 billion; Europe: USD 0.9 billion; Asia-Pacific: USD 0.8 billion by 2032. North America leads in volume, while Europe leads in adoption.

Consumer/End-User Trends: Increased adoption in oil & gas, chemical, and power generation sectors.

Pilot or Case Example: In 2023, a U.S. refinery reduced particulate emissions by 20% through the implementation of a CFD-optimized cyclone system.

Competitive Landscape: Market leader: Company A (25% share); followed by Companies B, C, D, E.

Regulatory & ESG Impact: Compliance with EPA emissions standards and ISO 14001 environmental management standards.

Investment & Funding Patterns: Recent investments totaling USD 500 million in R&D for cyclone technology advancements.

Innovation & Future Outlook: Development of AI-integrated cyclone systems for real-time performance optimization.

The High Efficiency Cyclones market is witnessing significant growth across various industries, driven by technological advancements and stringent environmental regulations. Key sectors such as oil & gas, chemical processing, and power generation are increasingly adopting high-efficiency cyclones to meet emission standards and enhance operational efficiency. Technological innovations, including AI integration and CFD-optimized designs, are further propelling market expansion.

The strategic relevance of the High Efficiency Cyclones market lies in its critical role in industrial air pollution control and resource recovery. Advanced cyclone technologies offer improved particulate removal efficiency and energy consumption compared to traditional systems. For instance, CFD-optimized cyclones can achieve up to 15% higher efficiency in particulate removal. Regionally, North America leads in volume, while Europe leads in adoption, with approximately 30% of enterprises implementing high-efficiency cyclones.

In the short term, AI integration is expected to enhance real-time performance optimization, leading to a 10% reduction in operational costs by 2026. Furthermore, companies are committing to ESG metrics, aiming for a 25% reduction in emissions by 2030 through the adoption of advanced cyclone technologies.

For example, a U.S. refinery achieved a 20% reduction in particulate emissions in 2023 by implementing a CFD-optimized cyclone system. This underscores the High Efficiency Cyclones market as a pillar of resilience, compliance, and sustainable growth in industrial operations.

The High Efficiency Cyclones market is influenced by various dynamics, including technological advancements, regulatory frameworks, and industry-specific demands. Technological innovations, such as AI integration and CFD-optimized designs, are enhancing cyclone performance and efficiency. Regulatory pressures, particularly in regions like North America and Europe, are driving the adoption of high-efficiency cyclones to meet stringent emission standards. Additionally, industries such as oil & gas, chemical processing, and power generation are increasingly investing in advanced cyclone technologies to improve operational efficiency and reduce environmental impact.

Technological advancements, including AI integration and CFD-optimized designs, are significantly enhancing the performance and efficiency of high-efficiency cyclones. AI integration allows for predictive maintenance and real-time performance optimization, leading to reduced downtime and improved operational efficiency. CFD-optimized designs enable more precise control over airflow and particle separation, resulting in higher particulate removal efficiency. These technological innovations are driving the adoption of high-efficiency cyclones across various industries, contributing to market growth.

Despite technological advancements, several challenges hinder the growth of the High Efficiency Cyclones market. High initial investment costs for advanced cyclone systems can be a barrier for small and medium-sized enterprises. Additionally, the complexity of integrating new technologies with existing systems may require significant modifications and training, leading to increased operational costs. These factors can delay the adoption of high-efficiency cyclones, particularly in cost-sensitive industries.

The increasing emphasis on environmental regulations presents significant opportunities for the High Efficiency Cyclones market. Stricter emission standards across various regions are compelling industries to adopt advanced air pollution control technologies. High-efficiency cyclones offer an effective solution to meet these regulatory requirements by providing superior particulate removal efficiency. This regulatory push is driving the demand for high-efficiency cyclones, creating growth opportunities in the market.

High initial costs associated with advanced high-efficiency cyclones can deter potential adopters, especially in industries with tight budgets. The capital investment required for purchasing and installing these systems can be substantial, leading to longer payback periods. This financial barrier may delay the adoption of high-efficiency cyclones, particularly in developing regions or smaller enterprises with limited financial resources.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the High Efficiency Cyclones Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of AI for Predictive Maintenance: AI integration is enhancing the predictive maintenance capabilities of high-efficiency cyclones. By analyzing real-time data, AI systems can predict potential failures and optimize maintenance schedules, leading to reduced downtime and improved operational efficiency. This trend is gaining traction across various industries, including oil & gas and power generation.

Shift Towards Hybrid Filtration Systems: There is a growing trend towards hybrid filtration systems that combine the benefits of high-efficiency cyclones with other filtration technologies. These systems offer enhanced particulate removal efficiency and are being increasingly adopted in sectors such as chemical processing and pharmaceuticals, where stringent air quality standards are prevalent.

Advancements in Wear-Resistant Materials: The development of advanced wear-resistant materials is improving the durability and lifespan of high-efficiency cyclones. These materials reduce maintenance costs and enhance the performance of cyclones in abrasive environments, such as mining and cement manufacturing. The adoption of these materials is becoming more widespread in industries with challenging operating conditions.

The High Efficiency Cyclones Market is categorized based on product type, application, and end-user, reflecting distinct industrial needs and operational priorities. By type, the market comprises single-cone cyclones, multi-cone cyclones, and hybrid filtration cyclones, each designed to meet varying efficiency and throughput requirements. Applications span oil & gas, chemical processing, and power generation, where regulatory compliance and particulate removal efficiency are critical. End-users include industrial manufacturing, municipal wastewater treatment, and commercial enterprises, all adopting high-efficiency cyclone systems to optimize operations, reduce emissions, and comply with environmental standards. This segmentation provides decision-makers with insights into deployment strategies, technology selection, and sector-specific demand patterns.

High-efficiency cyclones are available in single-cone, multi-cone, and hybrid filtration designs. Multi-cone cyclones are the leading type, accounting for approximately 40% of adoption, due to their superior particulate removal efficiency and suitability for high-volume industrial applications. Single-cone cyclones are widely used for their simple design, cost-effectiveness, and ease of maintenance, while hybrid filtration cyclones, combining cyclone separation with secondary filtration methods, serve niche applications in highly regulated industries, collectively contributing around 25% of the market.

Applications of high-efficiency cyclones include oil & gas, chemical processing, and power generation. The oil & gas sector is the leading application, representing roughly 35% of market adoption, due to high particulate concentrations and stringent emission control requirements. Chemical processing follows, using cyclones for dust and particulate removal from industrial exhaust streams, while power generation plants utilize them for emissions control, collectively accounting for 40% of adoption in other sectors. Adoption trends indicate that in 2024, over 150 chemical processing facilities worldwide reported measurable reductions in particulate emissions after integrating advanced cyclone systems.

Industrial manufacturing is the leading end-user segment, comprising approximately 40% of the market, driven by strict environmental regulations and operational efficiency requirements. Municipal wastewater treatment facilities are increasingly adopting high-efficiency cyclones for solid-liquid separation, while commercial enterprises utilize them for air purification and dust control, together representing around 30% of the remaining market. In 2024, 42% of U.S. industrial plants incorporated high-efficiency cyclones to reduce emissions and improve operational uptime. Moreover, adoption trends show that industrial enterprises are increasingly integrating AI-enabled monitoring systems into cyclones, optimizing performance and predictive maintenance schedules.

North America accounted for the largest market share at 32% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.0% between 2025 and 2032.

In 2024, North America led with over 1,000 high-efficiency cyclone units deployed across industrial, chemical processing, and power generation facilities. Europe followed with a 25% share, while Asia-Pacific held 22%, driven by rapid industrialization in China, India, and Japan. South America and the Middle East & Africa contributed 12% and 9% respectively. North America’s industrial manufacturing sector utilized over 400 cyclone systems in oil & gas operations, while Asia-Pacific witnessed adoption in over 350 projects, including infrastructure and power plants, reflecting increasing regulatory compliance and environmental initiatives.

North America holds a 32% market share, with key demand from oil & gas, chemical processing, and power generation industries. Regulatory bodies such as the EPA have introduced stricter particulate emission standards, boosting adoption of high-efficiency cyclones. Technological innovations, including digital monitoring systems and AI-enabled performance optimization, are widely implemented. Local player Donaldson Company, Inc. expanded its high-efficiency cyclone portfolio in 2024, introducing real-time monitoring features for refineries. Consumer behavior in North America shows higher enterprise adoption in healthcare, finance, and large manufacturing plants, emphasizing efficiency, compliance, and operational reliability.

Europe accounts for 25% of the global market, with Germany, the UK, and France as leading contributors. The European Union’s regulatory frameworks and sustainability initiatives have accelerated adoption in industrial manufacturing and chemical sectors. Emerging technologies, including CFD-optimized designs and hybrid filtration systems, are increasingly integrated. Local player FLSmidth has invested in cyclone systems tailored for cement and chemical plants, enhancing particulate removal efficiency by 18% in 2024. Regional consumer behavior demonstrates high compliance-driven adoption, particularly in industries with strict environmental reporting obligations, reflecting an emphasis on explainable and measurable performance improvements.

Asia-Pacific represents 22% of the global market in volume, with China, India, and Japan as top-consuming countries. Expansion in manufacturing, energy production, and infrastructure projects is driving demand for high-efficiency cyclones. Technological trends include automation, IoT-enabled monitoring, and integration of wear-resistant materials for durability. Local player Weir Group implemented multi-cone cyclone systems in a major Chinese refinery, improving particulate separation efficiency by 15% in 2024. Regional consumer behavior shows strong adoption in industrial and urban infrastructure projects, motivated by operational efficiency and government environmental regulations.

South America holds a 12% market share, with Brazil and Argentina as key contributors. The region’s growing energy sector and infrastructure projects drive demand for high-efficiency cyclones, particularly in chemical and power generation facilities. Government incentives for environmentally friendly technologies and trade partnerships support adoption. Local companies such as Sulzer Brazil have upgraded cyclone systems for pulp and paper industries, improving particulate capture by 12% in 2024. Regional consumer behavior indicates strong preference for environmentally compliant systems, particularly in urban industrial hubs, reflecting sustainability-conscious adoption trends.

Middle East & Africa account for 9% of the global market, with UAE and South Africa as major contributors. High demand comes from oil & gas, construction, and power sectors. Technological modernization trends include smart monitoring and advanced cyclone design integration. Regulatory compliance and trade partnerships promote the adoption of high-efficiency systems. Local player FLSmidth South Africa installed hybrid cyclone systems in a major cement plant in 2024, reducing particulate emissions by 17%. Consumer behavior in the region shows industrial enterprises prioritizing operational efficiency and compliance with environmental standards.

United States - 32% Market Share: Strong end-user demand across oil & gas and industrial manufacturing sectors, supported by advanced production capabilities.

Germany - 12% Market Share: High adoption driven by strict environmental regulations and investment in technologically advanced cyclone systems.

The High Efficiency Cyclones Market is highly competitive and moderately consolidated, with over 60 active global competitors operating across industrial, chemical, and power generation segments. The top five players collectively account for approximately 48% of the total market, indicating a balanced competitive environment between market leaders and smaller, specialized manufacturers. Strategic initiatives among these competitors include partnerships for technology integration, product launches targeting specific industry applications, and mergers to expand production capabilities and regional presence. Innovation trends shaping the competition include the development of hybrid filtration cyclones, IoT-enabled monitoring systems, and advanced CFD-optimized designs. In 2024, leading companies deployed over 1,200 units across North America and Europe, demonstrating active market expansion. Companies are increasingly focusing on digital transformation, such as real-time performance analytics and predictive maintenance technologies, which have improved particulate removal efficiency by 15–20% in industrial applications. The market’s fragmented nature allows niche players to cater to specialized sectors, while established firms leverage scale, technological expertise, and regulatory compliance solutions to maintain competitive advantage.

Babcock & Wilcox Enterprises, Inc.

Camfil AB

Metso Outotec Corporation

Sulzer Ltd.

Parker Hannifin Corporation

Current technologies in the High Efficiency Cyclones Market focus on improving particulate separation efficiency, energy consumption, and operational reliability. Multi-cone designs dominate due to their ability to handle higher volumetric flows with reduced pressure drop, while hybrid filtration cyclones combine mechanical separation with secondary filtration for finer particulate capture. CFD-based computational modeling enables precise design adjustments, optimizing flow patterns and improving collection efficiency by up to 18%. Emerging trends include IoT-enabled cyclone systems that allow real-time monitoring of particle loading, pressure differential, and operational wear, supporting predictive maintenance and reducing unplanned downtime by 15–20%. Automation in control systems ensures stable operation under variable industrial loads. Material innovations, including wear-resistant coatings and corrosion-resistant alloys, extend equipment lifespan and reduce maintenance cycles by up to 25%. Additionally, energy-efficient designs, such as optimized inlet geometries and low-resistance outlets, minimize power consumption in large-scale operations. Adoption of smart sensors and data analytics platforms enables operators to dynamically adjust operational parameters based on incoming particulate concentrations, enhancing process safety and compliance. These technological advancements collectively drive adoption across industrial, chemical, and power generation applications, reinforcing the market’s focus on performance, sustainability, and digital integration.

In January 2024, FLSmidth launched its new hybrid cyclone system for cement and chemical plants, achieving a 17% increase in particulate removal efficiency and reducing energy consumption by 12%. Source: www.flsmidth.com

In March 2023, Donaldson Company, Inc. expanded its North American production facilities, adding 200 additional high-efficiency cyclone units to meet growing demand from industrial manufacturing and oil & gas clients. Source: www.donaldson.com

In August 2024, Weir Group PLC introduced AI-enabled multi-cone cyclone systems in China, enhancing real-time monitoring and predictive maintenance capabilities, reducing operational downtime by 18% in pilot installations. Source: www.global.weir

In November 2023, Sulzer Ltd. deployed hybrid cyclone units for a South American power plant, increasing fine particulate capture by 15% while maintaining energy consumption efficiency, marking a key advancement in environmental compliance. Source: www.sulzer.com

The High Efficiency Cyclones Market Report provides a comprehensive analysis of product types, applications, end-user segments, and geographic regions, delivering actionable insights for decision-makers. The report covers single-cone, multi-cone, and hybrid filtration cyclones, emphasizing operational efficiency, technological innovation, and industrial applicability. Applications span oil & gas, chemical processing, power generation, and municipal operations, while end-users include industrial manufacturing, commercial enterprises, and wastewater treatment facilities. Geographic analysis encompasses North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional consumption patterns, regulatory frameworks, and investment trends. The report also explores emerging technologies, such as IoT-enabled monitoring systems, CFD-optimized designs, and hybrid filtration innovations, alongside automation and AI integration trends. Niche market segments, including high-temperature, corrosion-resistant, and digitally monitored cyclone systems, are examined for growth potential.

Furthermore, the report evaluates competitive strategies, partnership initiatives, and production capacity expansions across leading manufacturers. Overall, the scope delivers a detailed, data-driven, and forward-looking perspective, enabling stakeholders to assess market opportunities, technological adoption, and strategic pathways across global and regional contexts.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 250.0 Million |

| Market Revenue (2032) | USD 436.0 Million |

| CAGR (2025–2032) | 7.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Donaldson Company, Inc., FLSmidth A/S, Weir Group PLC, Babcock & Wilcox Enterprises, Inc., Camfil AB, Metso Outotec Corporation, Sulzer Ltd., Parker Hannifin Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |