Reports

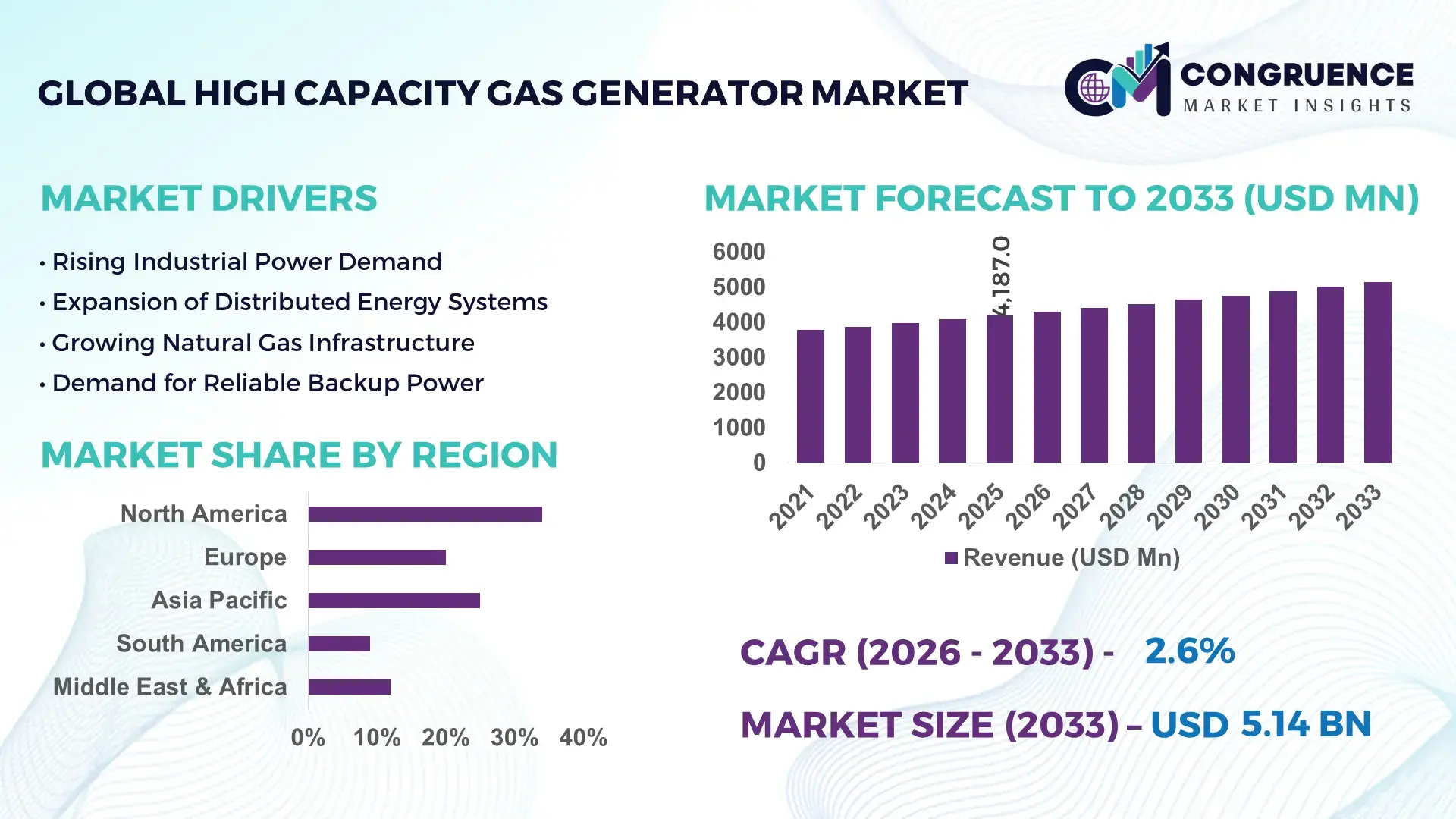

The Global High Capacity Gas Generator Market was valued at USD 4187.01 Million in 2025 and is anticipated to reach a value of USD 5141.42 Million by 2033 expanding at a CAGR of 2.6% between 2026 and 2033. Growth is primarily driven by increasing demand for reliable industrial power backup and continuous gas supply in energy-intensive sectors.

The United States remains the dominant country in the high capacity gas generator market, supported by advanced industrial infrastructure and strong capital expenditure in distributed energy systems. The country operates over 4,000 large-scale industrial gas generation units above 1 MW capacity across oil & gas, petrochemical, and data center facilities. Annual investments in onsite power generation and industrial backup systems exceed USD 8 billion, with natural gas-based generators accounting for more than 60% of new industrial standby installations. The adoption rate of high capacity gas generators in U.S. data centers has surpassed 70%, reflecting strong integration with digital infrastructure. Technological advancements, including low-NOx combustion systems and digital control modules, are increasingly embedded in large-capacity gas generator fleets to enhance fuel efficiency by up to 12% and reduce operational emissions.

Market Size & Growth: Valued at USD 4187.01 Million in 2025, projected to reach USD 5141.42 Million by 2033 at a CAGR of 2.6%, driven by industrial energy security and rising demand for high-load power backup solutions.

Top Growth Drivers: Industrial infrastructure expansion (35%), data center capacity growth (28%), and natural gas availability improvement (22%).

Short-Term Forecast: By 2028, advanced gas generator control systems are expected to reduce operational downtime by 18% and improve fuel efficiency by 10%.

Emerging Technologies: Low-emission combustion chambers, AI-based predictive maintenance, hybrid gas-solar generator integration.

Regional Leaders: North America projected above USD 1,850 Million by 2033 with strong data center adoption; Asia-Pacific nearing USD 1,600 Million driven by manufacturing expansion; Europe exceeding USD 1,200 Million supported by industrial decarbonization initiatives.

Consumer/End-User Trends: Oil & gas, utilities, mining, and hyperscale data centers account for over 65% of installations, favoring high-capacity units above 2 MW.

Pilot Example: In 2024, a Middle Eastern petrochemical complex improved power reliability by 21% after deploying 5 MW gas generator systems with digital monitoring.

Competitive Landscape: Caterpillar holds approximately 18% share, followed by Cummins, Siemens Energy, Mitsubishi Heavy Industries, and Wärtsilä.

Regulatory & ESG Impact: Stricter emission norms are pushing 30% reduction targets in NOx levels across new installations by 2030.

Investment & Funding: Over USD 3.5 billion invested globally in distributed gas-based generation projects during 2024–2025.

Innovation & Future Outlook: Integration with microgrids, carbon capture compatibility, and hydrogen-ready gas turbines are shaping next-generation deployments.

Industrial manufacturing contributes nearly 40% of total high capacity gas generator installations, followed by oil & gas at 25%, utilities at 18%, and data centers at 12%. Recent product innovations include modular 10 MW scalable units, digital twin-enabled monitoring platforms, and dual-fuel capability systems that allow up to 30% hydrogen blending. Environmental regulations targeting lower carbon intensity and rising electricity tariff volatility are encouraging industries to adopt high efficiency gas-based power systems. Asia-Pacific shows strong consumption growth due to expanding steel and cement manufacturing clusters, while Europe emphasizes low-emission distributed generation. Increasing electrification of industrial operations and grid instability in emerging economies are expected to sustain steady deployment of high capacity gas generator solutions.

The High Capacity Gas Generator Market plays a strategic role in ensuring industrial energy resilience, grid stability, and operational continuity for mission-critical sectors. With industrial electricity demand projected to increase by more than 20% over the next decade in emerging economies, high-output gas generators above 1 MW are becoming essential assets for distributed energy systems and captive power plants. Advanced lean-burn combustion technology delivers 15% efficiency improvement compared to conventional rich-burn systems, lowering fuel consumption and emission intensity.

Asia-Pacific dominates in volume due to large-scale manufacturing clusters, while Europe leads in adoption with over 45% of new industrial facilities integrating low-emission gas generators compliant with strict environmental norms. By 2028, AI-driven predictive maintenance systems are expected to cut unplanned downtime by 25% and extend equipment lifecycle by 10%, enhancing return on capital investments. Firms are committing to ESG metrics such as 30% emission intensity reduction by 2030 through cleaner fuel integration and digital performance optimization.

In 2024, Germany achieved a 17% reduction in industrial outage frequency through deployment of high efficiency gas-based backup systems integrated with smart grid frameworks. Strategic partnerships between equipment manufacturers and energy service providers are expanding turnkey distributed generation projects. With growing hydrogen blending capabilities and carbon capture compatibility, the High Capacity Gas Generator Market is positioned as a critical pillar of industrial resilience, regulatory compliance, and sustainable energy transition.

Rapid industrialization across Asia and the Middle East has increased demand for continuous, high-load power systems capable of supporting heavy machinery, refining units, and process manufacturing. Global data center capacity has expanded by more than 15% annually in key digital hubs, requiring reliable multi-megawatt backup solutions. High capacity gas generators provide faster start-up times and lower emission profiles compared to diesel alternatives, reducing operational carbon footprint by up to 20%. Industrial facilities operating 24/7 prioritize gas-based systems due to stable fuel pricing and integration with onsite gas pipelines. Growing electrification of mining and petrochemical operations further strengthens installation volumes for high-capacity units exceeding 2 MW.

Despite operational efficiency, high capacity gas generators require substantial upfront capital investment, particularly for units above 5 MW. Infrastructure costs related to gas pipeline connectivity, storage systems, and safety compliance can increase total project expenditure by 25–30%. In regions lacking reliable natural gas supply networks, additional LNG storage or compression facilities are necessary, raising complexity and extending deployment timelines. Furthermore, maintenance of advanced combustion and emission control systems demands specialized technical expertise, which may not be readily available in emerging markets. Financing constraints and long procurement cycles in public sector projects also delay adoption, particularly for large-scale industrial installations.

Hydrogen-ready gas generators present significant growth opportunities as industries transition toward low-carbon energy systems. Modern high capacity units can accommodate hydrogen blending ratios of up to 30%, reducing CO₂ emissions proportionally while maintaining power output stability. Integration with solar and battery storage in hybrid microgrids enhances operational flexibility and lowers fuel consumption by approximately 12%. Industrial parks and smart cities are increasingly adopting hybrid distributed energy models to improve grid independence. Government-backed decarbonization incentives and carbon pricing mechanisms are accelerating pilot projects that combine gas-based generation with carbon capture technologies, creating new revenue streams and long-term demand for advanced high capacity gas generator systems.

Stricter emission standards targeting nitrogen oxides and methane leakage require continuous technological upgrades, increasing R&D and compliance costs for manufacturers. Advanced after-treatment systems and low-NOx burners add up to 15% to equipment pricing. Simultaneously, fluctuations in natural gas prices impact operational expenditure planning for end-users, particularly in import-dependent economies. Regulatory approval processes for large-scale generation projects can extend beyond 12 months, delaying commissioning schedules. Additionally, competition from renewable energy storage solutions, which have witnessed battery cost reductions exceeding 40% over the past decade, creates pressure on traditional gas-based generation providers to enhance efficiency and environmental performance.

Shift Toward 5–20 MW Modular Gas Generator Units: Industrial buyers are increasingly favoring modular high capacity gas generator systems in the 5 MW to 20 MW range, which now account for nearly 48% of new large-scale installations globally. These modular configurations reduce onsite commissioning time by up to 30% and lower engineering complexity by 22% compared to conventional monolithic systems. Prefabricated skid-mounted units are enabling faster deployment in remote mining and oilfield environments, where project timelines have shortened by an average of 4–6 months. In North America and Europe, over 60% of newly approved industrial standby power projects above 10 MW now specify modular gas-based systems.

Growing Integration of Hydrogen Blending Capabilities: Approximately 35% of newly manufactured high capacity gas generators above 2 MW are now hydrogen-ready, supporting blending ratios between 20% and 30%. Pilot projects in Europe have demonstrated carbon emission reductions of up to 18% when operating at 25% hydrogen blend without compromising output stability. Industrial clusters in Germany and the Netherlands reported that more than 40 large-scale generator units were retrofitted in 2024 to enable partial hydrogen use, reflecting strong alignment with decarbonization targets. This measurable shift toward low-carbon fuel adaptability is accelerating procurement of advanced combustion technologies.

Digitalization and AI-Driven Predictive Maintenance Adoption: Around 52% of high capacity gas generator installations commissioned in 2024 incorporated advanced digital monitoring platforms. AI-based predictive analytics have reduced unplanned downtime by 23% and lowered maintenance costs by 15% across heavy industrial facilities. Remote performance diagnostics and IoT-enabled sensors are now standard in over 65% of units above 3 MW capacity. In large petrochemical complexes, real-time load optimization has improved fuel efficiency by nearly 12%, demonstrating quantifiable operational gains.

Rising Demand from Data Centers and Critical Infrastructure: Data centers represent nearly 14% of global high capacity gas generator deployments, with hyperscale facilities installing multi-unit configurations exceeding 10 MW each. Backup power reliability requirements exceeding 99.999% uptime standards are driving procurement of gas-based systems capable of full-load operation within 90 seconds. In Asia-Pacific, more than 120 new data center projects approved in 2024 included onsite gas generator capacity ranging between 5 MW and 25 MW. This expansion reflects a 19% year-on-year increase in high-capacity installations dedicated to digital infrastructure resilience.

The High Capacity Gas Generator market is segmented by type, application, and end-user, reflecting diverse operational requirements across industrial and commercial sectors. By type, systems are categorized into natural gas generators, biogas generators, dual-fuel generators, and hydrogen-ready gas generators, each designed to meet specific fuel availability and emission standards. In terms of application, prime power generation dominates installations in off-grid industrial sites, followed by standby power systems for mission-critical operations such as data centers and hospitals. Peak shaving and load management applications are also expanding in regions with volatile electricity tariffs. From an end-user perspective, oil & gas, manufacturing, utilities, mining, and digital infrastructure operators collectively account for more than 70% of installed capacity. Segmentation trends indicate increasing preference for fuel-flexible and digitally integrated systems capable of operating above 1 MW output while complying with stringent emission norms.

Natural gas generators currently account for approximately 46% of total high capacity gas generator installations, driven by extensive pipeline infrastructure and stable combustion performance. Dual-fuel gas generators hold around 24% adoption, particularly in regions requiring operational flexibility between diesel and gas. Hydrogen-ready gas generators represent about 18% of installed units but are expanding at the fastest rate, registering a CAGR of 5.8% due to decarbonization mandates and carbon reduction targets. While biogas-based high capacity units contribute nearly 12%, they remain niche solutions concentrated in waste-to-energy and agricultural processing facilities. Combined, these remaining segments contribute 30% of overall deployments beyond natural gas dominance. Hydrogen-ready systems are witnessing accelerated adoption because they allow up to 30% hydrogen blending without significant hardware modifications, supporting measurable emission reduction strategies.

Prime power generation represents the leading application, accounting for nearly 44% of high capacity gas generator usage, particularly in mining, oil extraction, and remote industrial operations. Standby power applications hold about 33% of installations, primarily within data centers and healthcare facilities requiring uninterrupted operations. However, peak shaving and grid support applications are expanding fastest, registering a CAGR of 4.9%, driven by rising industrial electricity tariffs and grid congestion challenges. These emerging applications are expected to exceed 28% of new deployments by 2033. The remaining 23% includes combined heat and power (CHP) installations and microgrid integration projects supporting energy efficiency objectives.

The oil & gas sector leads end-user adoption, representing approximately 29% of total high capacity gas generator installations due to continuous drilling and refining operations requiring high-load reliability. Manufacturing industries account for 25%, while utilities contribute around 18% of installed capacity for grid stabilization and distributed energy generation. Data centers, currently holding about 15% adoption, are expanding fastest with a CAGR of 6.2%, fueled by hyperscale cloud expansion and AI-driven computing demand. Mining and heavy infrastructure projects collectively contribute the remaining 13%, supporting off-grid power requirements in remote locations. Data center operators are increasingly adopting multi-unit gas generator arrays exceeding 20 MW total capacity to ensure uptime standards above 99.999%.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2026 and 2033.

North America’s leadership is supported by over 120 GW of installed gas-based distributed generation capacity, with more than 45% of new industrial facilities integrating high capacity gas generator systems above 2 MW. Europe holds approximately 27% share, driven by stringent emission policies and over 80 GW of combined heat and power installations utilizing natural gas technologies. Asia-Pacific contributes nearly 25% of global demand, with China and India accounting for more than 60% of regional installations due to rapid industrialization and power infrastructure expansion exceeding 15 GW annually. Middle East & Africa represent about 9% share, supported by oil & gas upstream operations and mega infrastructure projects, while South America contributes close to 5%, with Brazil leading regional deployment across mining and agribusiness sectors. Regional consumption patterns reveal that over 65% of installations globally are concentrated in industrial clusters and energy-intensive economic zones.

How Are Industrial Energy Security and Digital Infrastructure Investments Reshaping Large-Scale Gas Power Deployment?

North America holds approximately 34% of the global high capacity gas generator market share, supported by strong demand from oil & gas, data centers, manufacturing, and utilities. More than 50% of new hyperscale data center projects commissioned in 2024 integrated onsite gas generator systems exceeding 10 MW capacity. Regulatory frameworks such as stricter emission limits on diesel generators are encouraging a shift toward low-NOx gas-based systems capable of reducing emissions by up to 20%. Digital transformation trends are prominent, with nearly 60% of new installations incorporating AI-enabled predictive maintenance and remote monitoring solutions. Caterpillar, a leading local player, expanded its modular 5–15 MW gas generator lineup in 2024, improving fuel efficiency by 8% and reducing commissioning time by 25%. Enterprise adoption is notably higher in healthcare and financial services, where uptime standards above 99.999% are mandatory, reinforcing preference for advanced high capacity gas generator systems.

Why Is Industrial Decarbonization Accelerating Adoption of Cleaner High-Output Power Systems?

Europe accounts for nearly 27% of the global high capacity gas generator market, with Germany, the United Kingdom, and France representing over 55% of regional installations. Regulatory oversight from environmental authorities has intensified compliance requirements, mandating up to 30% reduction in NOx emissions for new industrial generation assets by 2030. More than 40% of newly installed large-scale gas generators in 2024 were certified hydrogen-ready, supporting up to 25% fuel blending. Combined heat and power systems exceed 80 GW capacity across the region, reflecting widespread industrial cogeneration adoption. Siemens Energy has advanced digital twin integration across its high capacity gas generator portfolio, enabling predictive diagnostics that reduce maintenance intervals by 18%. Consumer behavior in this region reflects strong regulatory pressure, resulting in higher demand for transparent performance monitoring, carbon reporting, and emission-optimized generator technologies.

What Is Driving Rapid Industrial Power Expansion Across Emerging Manufacturing Hubs?

Asia-Pacific ranks second in total market volume with nearly 25% global share and leads in new capacity additions exceeding 15 GW annually. China, India, and Japan collectively account for over 65% of regional demand, primarily driven by steel, cement, petrochemical, and semiconductor manufacturing expansion. Infrastructure investments surpassing USD 1 trillion equivalent across industrial corridors have increased demand for reliable onsite generation above 3 MW capacity. Regional innovation hubs are emphasizing hybrid gas-solar microgrid systems, improving fuel efficiency by 10–12%. Mitsubishi Heavy Industries expanded its hydrogen-compatible gas generator platforms in 2024, targeting industrial clients seeking emission reductions above 15%. Consumer behavior indicates strong adoption among manufacturing exporters and e-commerce logistics operators requiring stable high-load operations, reinforcing consistent demand for scalable high capacity gas generator solutions.

How Are Energy Infrastructure Gaps Supporting Industrial Backup Power Investments?

South America contributes approximately 5% of global high capacity gas generator installations, with Brazil and Argentina accounting for nearly 70% of regional demand. Brazil’s mining and agribusiness sectors operate more than 3 GW of captive gas-based generation capacity to mitigate grid instability. Infrastructure modernization programs have accelerated natural gas pipeline expansions exceeding 1,000 km in recent years, improving fuel accessibility. Government-backed energy diversification policies provide fiscal incentives for cleaner gas-based generation projects. WEG, a regional manufacturer, enhanced its 2–8 MW gas generator systems in 2024 with advanced emission control features, improving efficiency by 9%. Regional buyers prioritize cost stability and operational continuity, particularly in remote extraction sites where grid reliability remains below 95%, supporting steady procurement of high capacity gas generator systems.

Why Are Hydrocarbon-Rich Economies Investing in Advanced Distributed Gas Power Systems?

Middle East & Africa hold nearly 9% of global market share, largely driven by oil & gas upstream operations and mega construction projects. The UAE and Saudi Arabia together account for over 50% of regional installations exceeding 5 MW capacity. Large-scale industrial zones operate gas-based generators totaling more than 8 GW capacity to ensure uninterrupted energy supply. Technological modernization initiatives emphasize integration with smart grid platforms and hybrid renewable systems, improving fuel efficiency by up to 11%. Local regulations promote reduced flaring and increased utilization of associated gas for power generation. In South Africa, industrial facilities added over 500 MW of distributed gas capacity in 2024 to offset load-shedding challenges. Consumer behavior across this region shows strong preference for durable, high-output generator systems capable of operating in extreme climatic conditions above 45°C.

United States – 28% market share: The High Capacity Gas Generator market in the United States leads due to extensive industrial production capacity, over 120 GW distributed gas generation base, and strong demand from hyperscale data centers.

China – 19% market share: The High Capacity Gas Generator market in China is driven by large-scale manufacturing clusters, expanding petrochemical complexes, and annual industrial capacity additions exceeding 10 GW.

The High Capacity Gas Generator market exhibits a moderately consolidated structure, with the top five companies collectively accounting for approximately 52% of global installations. Over 40 active international and regional manufacturers compete across capacity ranges above 1 MW. Market leaders focus on modularization, hydrogen compatibility, and digital integration to strengthen competitive positioning. In 2024 alone, more than 25 new high-output gas generator models were introduced globally, with 60% featuring low-emission combustion systems. Strategic partnerships between generator manufacturers and energy service providers increased by 18% year-on-year to deliver turnkey distributed generation projects. Mergers and acquisitions activity remains selective, targeting technology enhancement and regional expansion. Competitive intensity is further shaped by aftersales service contracts, which account for nearly 35% of lifecycle value. Innovation trends emphasize AI-driven monitoring platforms, carbon capture readiness, and scalable hybrid integration, reinforcing differentiation strategies among leading high capacity gas generator suppliers.

Caterpillar Inc.

Cummins Inc.

Siemens Energy

Mitsubishi Heavy Industries

Wärtsilä Corporation

General Electric Vernova

Rolls-Royce Power Systems

MAN Energy Solutions

Kawasaki Heavy Industries

WEG S.A.

Technological advancement in the High Capacity Gas Generator Market is centered on efficiency optimization, emission reduction, digital intelligence, and fuel flexibility. Modern high-capacity systems above 5 MW are increasingly equipped with lean-burn combustion technology, enabling up to 15% higher thermal efficiency compared to conventional rich-burn configurations. Advanced low-NOx burner systems now limit nitrogen oxide emissions to below 25 ppm in compliant industrial installations, aligning with stricter environmental standards across North America and Europe.

Hydrogen-ready platforms represent a significant innovation frontier. More than 30% of newly engineered high capacity gas generator models launched since 2023 are capable of operating with 20–30% hydrogen blending without major hardware retrofits. Select industrial pilot installations have demonstrated stable performance at 50% hydrogen mix under controlled conditions, signaling future scalability. Dual-fuel engines, capable of switching between natural gas and diesel with automated load synchronization in under 60 seconds, are gaining traction in mission-critical facilities.

Digitalization is transforming asset management strategies. Approximately 55% of installations above 3 MW now integrate IoT-enabled sensors and cloud-based supervisory control systems. AI-driven predictive analytics have reduced unplanned downtime by 20–25% and extended maintenance intervals by up to 18%. Digital twin technology allows simulation-based load forecasting and real-time performance benchmarking, improving fuel efficiency by nearly 10% in industrial operations. Integration with microgrid controllers and battery energy storage systems further enhances operational resilience, enabling seamless transition between grid-connected and island modes within 100 milliseconds. Carbon capture readiness and exhaust heat recovery systems are also being embedded in next-generation platforms, supporting industrial decarbonization pathways while maintaining high-load reliability.

• In March 2024, Wärtsilä launched its 46TS engine platform for large-scale power generation, delivering output above 23 MW per unit and achieving electrical efficiency exceeding 51% in simple cycle mode. The engine is designed for future hydrogen blending and flexible grid support. Source: www.wartsila.com

• In April 2024, Mitsubishi Heavy Industries announced successful validation of a gas turbine system capable of 100% hydrogen firing at its Takasago Hydrogen Park, marking a milestone in zero-carbon thermal power generation technology for high-capacity applications. Source: www.mhi.com

• In May 2025, Siemens Energy secured a contract to supply SGT-800 industrial gas turbines for a large Middle Eastern power project, each unit delivering up to 62 MW with high operational flexibility and rapid ramp-up capability suited for grid stabilization.

• In February 2025, Cummins introduced enhancements to its QSK60G gas generator platform, improving transient response by 15% and enabling compatibility with renewable natural gas (RNG) for large industrial and data center installations.

The High Capacity Gas Generator Market Report provides comprehensive coverage of generator systems typically rated above 1 MW, with detailed analysis across capacity bands including 1–5 MW, 5–20 MW, and above 20 MW installations. The study evaluates technology configurations such as natural gas-fired systems, dual-fuel engines, hydrogen-ready platforms, and combined heat and power (CHP) integrated units. It examines performance parameters including efficiency levels exceeding 50% in advanced systems, emission thresholds below 25 ppm NOx, and hydrogen blending capability up to 30% in commercially available models.

Geographically, the report assesses five major regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—covering more than 25 key countries representing over 90% of global industrial gas-based generation capacity. Application analysis spans prime power, standby power, peak shaving, microgrid integration, and cogeneration systems, with particular focus on energy-intensive industries such as oil & gas, manufacturing, mining, utilities, and hyperscale data centers operating above 10 MW load requirements.

The scope further includes evaluation of digital transformation trends, where over 50% of new installations incorporate AI-based monitoring and remote diagnostics. It addresses regulatory frameworks influencing emission standards, fuel transition strategies including hydrogen and renewable natural gas, and infrastructure expansion trends exceeding 15 GW annual additions in emerging economies. Additionally, the report reviews competitive benchmarking of more than 40 active global manufacturers, lifecycle service models, and technology roadmaps supporting decarbonization and grid resilience objectives.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

2.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Caterpillar Inc., Cummins Inc., Siemens Energy, Mitsubishi Heavy Industries, Wärtsilä Corporation, General Electric Vernova, Rolls-Royce Power Systems, MAN Energy Solutions, Kawasaki Heavy Industries, WEG S.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |