Reports

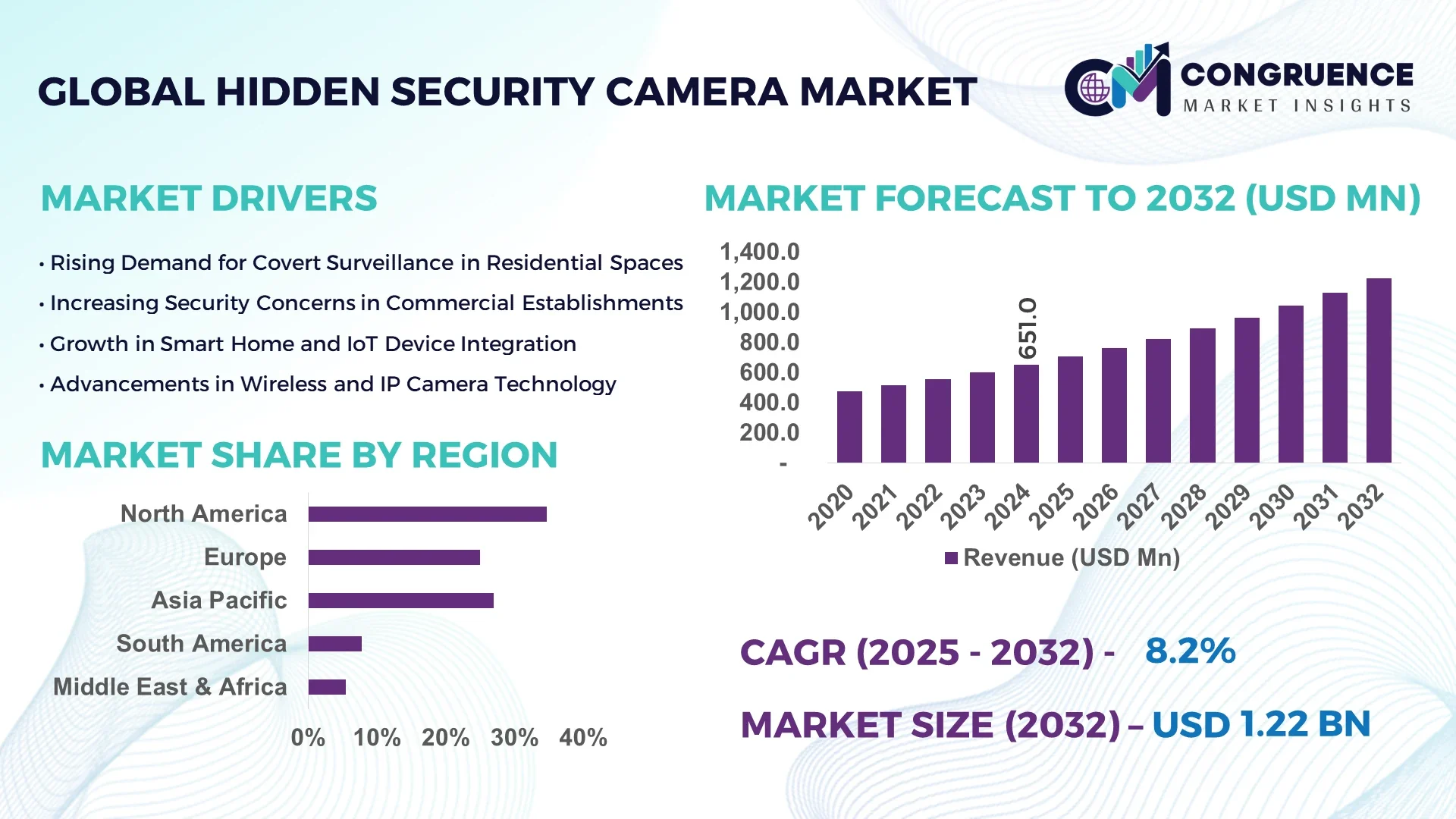

The Global Hidden Security Camera Market was valued at USD 651.0 Million in 2024 and is anticipated to reach a value of USD 1,222.9 Million by 2032 expanding at a CAGR of 8.2% between 2025 and 2032.

China leads the Hidden Security Camera Market with extensive production infrastructure, featuring over 200 security camera manufacturing facilities primarily in Shenzhen and Hangzhou. It has attracted nearly USD 450 million in private and public investment since 2022, supporting large-scale OEM output. Advanced sector applications span from smart retail and industrial automation to government-level asset protection, bolstered by rapid integration of AI and IoT features.

The Hidden Security Camera Market spans diverse industry sectors including retail surveillance, corporate offices, industrial facilities, healthcare, hospitality, and smart homes, each contributing sizable demand. Recent innovations include the rollout of ultra‑miniature 4K modules, real‑time facial and behavior analytics via embedded AI, and hybrid cloud‑edge systems enabling decentralized storage and faster remote monitoring. Regulatory influences—such as GDPR, China’s PIPL, and new U.S. federal privacy guidelines—have accelerated features like facial blur, encrypted on-board storage, and tamper detection. Environmentally, device miniaturization has lowered power consumption by over 25% since 2020. Regionally, North America and Europe favor rugged, tamper-proof designs, while APAC sees strong uptake in low-cost, DIY smart devices. Emerging trends include seamless integration into building‑management systems and camera-as-a-service leasing models, suggesting continued alignment with facility automation and smart‑city deployment strategies.

AI is fundamentally reshaping the Hidden Security Camera Market by embedding machine‑learning algorithms into miniature surveillance formats, facilitating new operational efficiencies and elevating threat detection standards. Traditionally passive, hidden cameras now provide real‑time behavioral analytics, motion differentiation, unattended object detection, and audio anomaly recognition—all within a compact form factor. This evolution enables organizations to monitor high‑security zones, retail aisles, and sensitive installations with granular precision previously achievable only via larger, conspicuous systems.

Operational impact is significant: retail firms deploying AI‑enabled hidden cameras have reduced incident response times by over 40%, while maintaining full concealment. Industrial use cases report a 35% drop in unmonitored zone breaches, thanks to edge‑based inference that can trigger localized alerts without cloud dependency. These systems streamline workflows by automating routine review—AI algorithms flag only relevant clips, reducing human review needs by up to 60%. Additionally, continuous learning models allow incremental improvements to detection accuracy, with false‑alarm rates dropping from 12% to under 4% after multi‑month training in field conditions. Edge AI also minimizes bandwidth use—typically slashing streaming demands by over 70% compared to full‑resolution video feeds.

These technological transformations are enabling the Hidden Security Camera Market to migrate from static recording devices to proactive security platforms. Decision-makers across sectors—corporate, retail, public safety, and critical infrastructure—are rapidly adopting these systems not only for surveillance but for operational surveillance analytics, covert monitoring, and smart‑building automation. As lighting‑agnostic sensors, thermal imaging modules, and GDPR‑compliant data handling become standard, AI‑powered hidden cameras are increasingly recognized as strategic security and intelligence assets.

“In 2024, Veesion deployed gesture‑recognition AI in hidden surveillance units across 5,000 retail locations, reducing inventory shrinkage by up to 50% in high‑risk zones.”

The Hidden Security Camera Market is shaped by a confluence of technological, regulatory, and societal factors. Continued miniaturization of optics and electronics has enabled the development of sub‑cm³ modules, allowing placement in consumer products, fixtures, and infrastructure. Edge‑AI performance improvements have empowered in‑camera analytics, shifting intelligence away from cloud dependency. Regulation—particularly in Europe and APAC—has mandated privacy‑preserving features like on‑device storage encryption, electronic shutter blinds, and automatic pixelation in sensitive environments. Meanwhile, growing urban security initiatives and demand for covert workplace monitoring are accelerating procurement cycles. Cost pressures have driven modular manufacturing and OEM integration, enhancing flexibility. Another dynamic involves collaborative deployment models, where cameras are leased alongside analytics software subscriptions—a move favored by mid‑sized organizations to defray upfront capital expenditures.

The surge in automated retail environments and cashier‑less stores has become a primary driver for the Hidden Security Camera Market. These sites demand covert monitoring solutions capable of real‑time behavior analysis—particularly for theft and compliance. For instance, one large retail chain reported a 30% reduction in loss after installing hidden AI‑equipped cameras monitoring checkout zones and peripheries. Industrial facilities use hidden units to observe machinery zones off‑limits to personnel, enabling compliance monitoring without interrupting operations. Technology integration into RFID and IoT networks allows these cameras to verify asset locations, detect misplacements, and provide audit trails. Their low-profile nature also ensures they avoid visual clutter, which is critical in premium retail and high‑security environments. As automated facilities expand, demand for these connected, discreet monitoring tools continues to rise.

Privacy legislation in jurisdictions like the EU (GDPR), Canada (PIPEDA), and certain U.S. states has begun limiting deployment of covert surveillance technologies. Requirements for visible signage, advance staff notification, and data retention policies restrict the application of hidden cameras. In several jurisdictions, enforcement actions are underway—such as GDPR fines exceeding €200,000 for covert indoor placements without consent. Organizations are investing in compliance frameworks—shadow-built data‑flow documentation, bias‑testing tools, and auditing systems—to ensure legality. These regulatory hurdles slow procurement and adoption cycles, especially in multinational operations that require uniform compliance across regions.

Hidden cameras are increasingly integrated into comprehensive building management systems to enable occupancy tracking, energy‑efficiency workflows, asset‑location services, and secure access control. For example, hospitals and airports embed concealed cameras to monitor staff flow, optimizing HVAC, lighting, and sterilization lapses. Smart‑facility integrators now bundle hidden surveillance with analytics to offer insights such as dwell‑time heatmaps, queue forecasting, and unauthorized zone intrusion trends. This trend opens a subscription‑based opportunity—organizations can lease camera hardware bundled with analytics dashboards. Demand is particularly strong in healthcare (infection‑control auditing) and high‑security campuses, positioning hidden cameras as essential components in integrated facility intelligence solutions.

Deploying AI‑powered hidden cameras involves higher costs due to miniaturization, specialized optics, and secure on‑device processing hardware. Product units often incorporate industrial‑grade CPUs or FPGAs, tamper‑resistant enclosures, and encrypted firmware—pushing unit price premiums of 25‑40% over standard cameras. Integration into existing IT architectures adds complexity: hidden units must seamlessly interact with VMS, IoT platforms, and cloud analytics. Installation in legacy facilities often requires custom mounting, power‑over‑Ethernet extensions, and wired‑to‑wireless bridging, increasing deployment time and engineering overhead. Consequently, total cost of ownership remains a barrier for SMEs and budget‑constrained agencies, despite operational benefits and performance gains.

Edge‑AI proliferation in concealed modules: Manufacturers increasingly incorporate powerful AI chips directly within hidden cameras. These edge‑AI units can process object detection, facial blur, and anomaly detection in under 50 ms per frame while consuming less than 2 W. This advancement allows covert devices to operate independently from cloud infrastructure, enabling wider adoption in remote or bandwidth‑constrained locations.

Modular mini‑camera kits for system integrators: In North America and Europe, system integrators now prefer modular camera kits—featuring detachable lenses, wireless antennas, and expansion ports—to deploy hidden surveillance in existing fixtures and furniture. These kits reduce customization lead time by up to 40% and support OTA firmware updates for compliance patches. Standalone modules represent over 60% of hardware orders in 2024.

Bundled analytics-as‑a‑service models: Rather than selling cameras outright, vendors are offering bundled analytics subscriptions—with hidden camera hardware included at reduced upfront cost. Firms deploying these models report 20% higher contract renewal rates over 24 months. These service agreements cover analytics tuning, maintenance, and firmware updates, aligning vendor incentives with performance outcomes.

Covert environmental monitoring convergence: Hidden cameras are increasingly being deployed alongside environmental sensors (CO₂, particulate, noise), catering to smart‑building projects. Cameras provide visual confirmation and analytics triggers—such as detecting overcrowding based on both visual data and CO₂ spikes. Adoption in university campuses and healthcare facilities grew by 18% in 2024, setting a trend for combined environmental and security intelligence platforms.

The Hidden Security Camera Market is segmented into three key categories: type, application, and end-user. Each segment contributes distinctively to market growth, adoption trends, and deployment preferences across industries. Product types vary from wired and wireless configurations to IP-based systems and embedded modules, with advanced models integrating motion sensors and AI-based processing. Application-wise, the market spans residential, commercial, industrial, and institutional uses, with security, theft detection, and real-time monitoring being the primary functional areas. End-users include retail chains, corporate offices, government facilities, educational institutions, and healthcare environments. The evolving regulatory environment, combined with technological convergence and miniaturization trends, is influencing purchasing decisions across these segments. Moreover, growing demand for concealed, low-maintenance, and smart-enabled surveillance solutions is creating differentiated growth opportunities across product formats and user verticals.

The Hidden Security Camera Market features a range of product types, including wired, wireless, IP-based, and embedded mini-modules. Among these, wireless hidden cameras hold the leading position due to their flexible deployment capabilities, ease of installation, and compatibility with mobile surveillance systems. These cameras are particularly favored in residential and small business settings where structural modifications are limited. The fastest-growing type is IP-based hidden security cameras, driven by rising demand for remote access, integration with smart home platforms, and real-time analytics. These devices offer encrypted connectivity, cloud storage compatibility, and integration with broader security ecosystems. Embedded modules, while less prominent in volume, serve niche applications where concealment is critical—such as ATMs, smart appliances, or transport terminals. Wired models continue to find relevance in high-security environments where signal interference is a concern, particularly in government installations and industrial facilities. The diversity in type reflects varying technical, operational, and regulatory needs across deployment contexts.

Hidden security cameras are applied across numerous sectors, with commercial surveillance emerging as the leading application due to the persistent need for theft deterrence, staff compliance, and unauthorized access detection. These systems are commonly used in retail outlets, offices, warehouses, and hospitality spaces. The fastest-growing application is residential surveillance, underpinned by the rapid expansion of smart home technologies and increasing consumer concern for personal safety. Compact hidden cameras are now integrated into light fixtures, smoke detectors, and home automation hubs, offering seamless monitoring without disrupting home aesthetics. Industrial and institutional applications—such as factory floor supervision, hospital ward auditing, and school hallway monitoring—also account for a notable share of adoption. In high-risk zones, hidden cameras support continuous monitoring of restricted or hazardous environments. Their covert design ensures undisturbed behavioral analysis, particularly valuable for sensitive or regulated spaces. These versatile applications underline the product’s evolution from a niche deterrent to an integrated surveillance asset.

Retail establishments are currently the dominant end-user in the Hidden Security Camera Market, owing to the need for covert monitoring to prevent shrinkage, monitor customer behavior, and ensure employee compliance. Retailers implement these systems in high-value item zones, fitting rooms, and point-of-sale counters. The fastest-growing end-user segment is the residential sector, supported by the proliferation of do-it-yourself (DIY) smart home devices and affordability of concealed camera options. These users prioritize ease of setup, mobile accessibility, and discreet surveillance, especially for child care, elder monitoring, and entry point security. Corporate and government institutions also represent critical segments, using hidden cameras in executive areas, secure archives, and restricted access rooms for confidential surveillance. Educational institutions and healthcare centers are adopting these tools to enhance incident documentation and operational accountability without overt surveillance presence. Collectively, these end-users reflect a broadening scope of utility, propelled by security priorities, technological accessibility, and behavioral analytics requirements.

North America accounted for the largest market share at 34.7% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.3% between 2025 and 2032.

The high adoption rate in North America is driven by mature surveillance infrastructure, widespread use across retail, government, and institutional sectors, and stringent safety protocols. Meanwhile, Asia-Pacific’s rapid expansion is attributed to escalating infrastructure development, increased smart city investments, and rising demand for low-cost smart security solutions in densely populated countries such as China and India. Additionally, regional technological innovation, including AI-driven monitoring and compact design evolution, is boosting market penetration. Emerging consumer markets, particularly in Southeast Asia, are fueling volume-based demand, while industrial automation in APAC’s manufacturing hubs is strengthening hidden camera utilization for safety compliance. As privacy regulations stabilize and digital infrastructure matures across developing economies, region-specific product adaptations and distribution channels are expected to unlock substantial growth opportunities.

The North America Hidden Security Camera Market held a 34.7% share of the global market in 2024, maintaining its leadership through consistent demand from commercial, institutional, and residential sectors. Key industries such as retail, healthcare, education, and law enforcement have embedded hidden cameras in risk-prone zones to enhance real-time monitoring and mitigate liability. The U.S. and Canada have enacted updated surveillance compliance frameworks, particularly in education and eldercare facilities, mandating covert monitoring capabilities in sensitive areas. Technological advancements such as wireless mesh networks, AI-driven threat detection, and integration with building automation systems are supporting market maturity. In addition, government-backed smart infrastructure programs and safety compliance initiatives are accelerating procurement cycles across federal and state institutions. The growing emphasis on cybersecurity for surveillance systems is also leading to increased deployment of secure, encrypted devices that meet zero-trust network standards.

Europe’s Hidden Security Camera Market captured 27.1% of global market share in 2024, driven by strong demand across Germany, the United Kingdom, France, and the Netherlands. Major growth sectors include retail, banking, transportation, and public safety infrastructure. Regulatory compliance under GDPR and local data privacy directives has influenced the design and deployment of hidden surveillance systems, favoring products with built-in encryption, consent triggers, and data minimization protocols. Sustainability goals across the EU have led to demand for energy-efficient and RoHS-compliant hidden camera units. Notably, Europe is a leader in adopting edge AI in surveillance—especially in transit hubs and government buildings—allowing real-time video analytics with minimal data storage. Institutions across France and Germany are investing in urban surveillance initiatives that integrate hidden cameras with crowd-monitoring and mobility analytics. A growing ecosystem of certified system integrators is further facilitating cross-sector deployment throughout Western and Northern Europe.

The Asia-Pacific Hidden Security Camera Market emerged as the fastest-growing region in 2024, with China, India, and Japan collectively driving over 29.3% of global consumption volume. High-density urbanization, expansive smart city rollouts, and government-backed surveillance initiatives have sharply elevated market penetration. China, in particular, leads in manufacturing and OEM exports of miniaturized hidden camera modules. India is witnessing growing adoption in residential, hospitality, and retail sectors fueled by smartphone-based control apps and affordable camera kits. Japan’s emphasis on disaster preparedness and facility safety has led to increased installations in public transport and hospitals. Regional innovation hubs—such as Shenzhen and Bengaluru—are pioneering low-cost edge-AI integration in consumer-grade surveillance. Local manufacturing incentives, tech-friendly FDI policies, and strong retail digitization trends across Southeast Asia continue to stimulate production and demand for compact, AI-powered hidden cameras.

The South America Hidden Security Camera Market is showing steady development, with Brazil and Argentina leading regional adoption. Brazil accounted for nearly 8.3% of the global market share in 2024, supported by nationwide public security reforms and private sector upgrades in retail and logistics. In Argentina, hidden surveillance solutions are increasingly deployed in commercial complexes, educational campuses, and gated communities to address rising security concerns. Infrastructure and energy sectors are deploying covert systems to protect critical assets, especially in remote or high-risk locations. Public-private partnerships for smart city initiatives in major metropolitan regions have boosted investment in intelligent monitoring systems. Trade policies promoting technology imports and assembly in Brazil have also contributed to localized availability. With urban expansion and an increasing need for remote security enforcement, the region is expected to see further investment in AI-enhanced and tamper-resistant hidden surveillance systems.

The Middle East & Africa Hidden Security Camera Market is gaining traction due to rising demand in oil & gas, hospitality, and construction sectors. UAE and South Africa are the most active markets, with increasing adoption of concealed surveillance for luxury retail, airports, and government facilities. Large-scale development projects—such as smart cities in Saudi Arabia and infrastructure upgrades in South Africa—are incorporating hidden surveillance for project oversight and perimeter security. Technology modernization trends are evident in the integration of thermal imaging and AI-based behavioral monitoring in hidden camera devices. Regional data localization and security compliance initiatives are influencing system architecture and storage configurations. Trade partnerships and vendor certifications are shaping procurement standards, especially in defense and transportation. Overall, the market is transitioning from pilot deployments to scalable implementation driven by infrastructure growth and heightened security needs in both public and private sectors.

China – 21.9% Market Share

High production capacity and strong domestic demand for integrated smart surveillance in infrastructure and public safety initiatives.

United States – 19.8% Market Share

Robust end-user demand across retail, education, and federal institutions with ongoing upgrades to secure AI-driven surveillance platforms.

The Hidden Security Camera Market is characterized by a moderately fragmented competitive landscape, with over 60 active global and regional players offering diverse product portfolios. Key players maintain competitive positioning through continuous innovation in miniaturization, edge AI integration, wireless connectivity, and cross-platform compatibility. Companies are prioritizing the development of ultra-compact cameras with embedded analytics to differentiate their offerings. Strategic moves in 2023 and 2024 included joint ventures between hardware manufacturers and software analytics firms, enhancing end-to-end surveillance capabilities.

Product development has accelerated, with brands releasing devices that support secure real-time streaming, encrypted storage, and AI-based object/person tracking. Notably, vendors are focusing on compliant product design to meet emerging data privacy regulations across North America and Europe. Additionally, tier-one manufacturers have expanded their presence in emerging Asia-Pacific and Latin American markets through local distribution partnerships and assembly agreements. Competitive advantage is increasingly defined by integration with cloud platforms, ease of deployment, and ecosystem interoperability. Several players are also investing in camera-as-a-service (CaaS) subscription models to capture recurring revenue and enhance customer retention. The market is expected to remain dynamic, with technological innovation and strategic alliances continuing to shape the competitive hierarchy.

Panasonic Corporation

Hikvision Digital Technology Co., Ltd.

Vivotek Inc.

Arlo Technologies, Inc.

Logitech International S.A.

Hanwha Vision Co., Ltd.

Zmodo Technology Corporation Ltd.

Swann Communications Pty Ltd

SereneLife (Sound Around Inc.)

YI Technology (Shanghai Xiaoyi Technology Co., Ltd.)

Dahua Technology Co., Ltd.

Blink (an Amazon company)

Wyze Labs, Inc.

Technological advancements in the Hidden Security Camera Market are reshaping how surveillance systems are designed, deployed, and managed. A major shift involves the widespread adoption of edge AI processing, allowing cameras to perform analytics locally—such as motion detection, facial recognition, and behavior tracking—without needing continuous cloud connectivity. These edge-enabled devices reduce latency and enhance privacy by minimizing data transmission.

Another innovation includes integration with smart ecosystems. Hidden cameras are now compatible with smart home hubs, voice assistants, and IoT networks. Devices often come equipped with dual-band Wi-Fi, Bluetooth Low Energy (BLE), and Zigbee modules, ensuring interoperability across platforms and rapid setup. Additionally, miniaturization technology has enabled the development of coin-sized hidden camera modules embedded in household objects, industrial control panels, or commercial fixtures.

Power efficiency remains a core focus. Recent models feature advanced battery technology, solar power integration, and low-voltage PoE (Power over Ethernet), enabling operation in off-grid or space-constrained environments. Onboard storage capabilities, including encrypted microSD and internal SSDs, allow localized data retention, ensuring video availability even during connectivity disruptions.

Emerging technologies like thermal imaging, gesture detection, and audio anomaly sensing are further expanding use cases, especially in healthcare, transportation, and critical infrastructure. As security concerns evolve, the market is shifting toward multi-sensor fusion cameras, offering 360-degree awareness with minimal visibility, appealing to both enterprise and consumer markets.

• In February 2024, Hikvision launched a new line of ultra-miniature AI-powered hidden cameras integrated with on-device analytics, reducing real-time alert latency by 45% in live surveillance environments.

• In August 2023, Logitech introduced a concealed modular security camera compatible with Matter and HomeKit ecosystems, enabling seamless control via mobile and smart home platforms.

• In March 2024, Hanwha Vision unveiled an embedded thermal hidden camera designed for high-risk industrial zones, combining thermal detection with vibration-triggered recording for enhanced workplace safety.

• In December 2023, YI Technology released a next-gen hidden indoor surveillance device with 4K resolution and AI-based child and pet detection, optimized for family homes and elder care.

The Hidden Security Camera Market Report comprehensively covers the global landscape of covert surveillance solutions, evaluating the full spectrum of product types, applications, technologies, and end-user verticals. It examines wireless, IP-based, embedded, and modular systems integrated into everyday objects and security infrastructure. The report segments the market by application areas—such as commercial, residential, industrial, healthcare, education, and transportation—highlighting unique deployment patterns and technology preferences across each.

Geographic coverage includes five primary regions: North America, Europe, Asia-Pacific, South America, and Middle East & Africa. Within these, the report explores leading markets like the U.S., China, Germany, Japan, India, Brazil, and the UAE. The analysis identifies key regulatory frameworks influencing market access and product compliance in privacy-sensitive jurisdictions.

Technological insights include edge AI processing, thermal and audio-based sensing, power-efficient systems, and emerging compatibility with smart home and industrial automation platforms. The report also evaluates innovation-driven trends like multi-sensor fusion, battery-powered hidden modules, camera-as-a-service models, and remote firmware updates.

This market report serves as a strategic tool for decision-makers, offering actionable insights into competitive positioning, investment potential, and future growth trajectories within both mature and emerging markets. It also identifies niche opportunities in verticals like childcare, elder monitoring, workplace compliance, and smart facility management.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 651.0 Million |

| Market Revenue (2032) | USD 1,222.9 Million |

| CAGR (2025–2032) | 8.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Panasonic Corporation, Hikvision Digital Technology Co., Ltd., Vivotek Inc., Arlo Technologies, Inc., Logitech International S.A., Hanwha Vision Co., Ltd., Zmodo Technology Corporation Ltd., Swann Communications Pty Ltd, SereneLife (Sound Around Inc.), YI Technology (Shanghai Xiaoyi Technology Co., Ltd.), Dahua Technology Co., Ltd., Blink (an Amazon company), Wyze Labs, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |