Reports

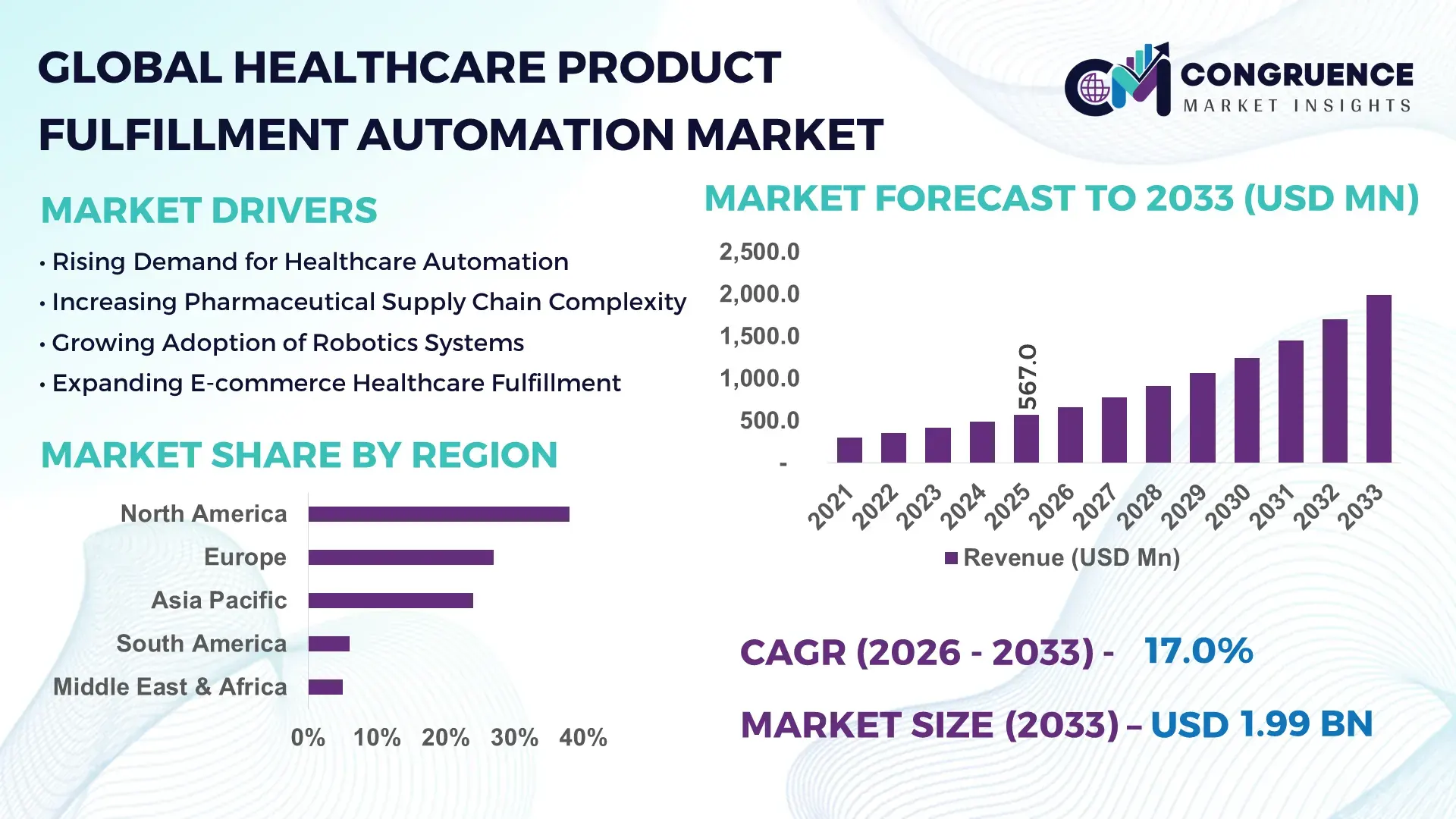

The Global Healthcare Product Fulfillment Automation Market was valued at USD 567.0 Million in 2025 and is anticipated to reach a value of USD 1,991.0 Million by 2033 expanding at a CAGR of 17.0% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is driven by increasing demand for error-free, high-speed medical supply chain operations across hospitals and pharmacies.

The United States leads the Healthcare Product Fulfillment Automation Market with over 38% deployment concentration of automated healthcare warehouses and distribution centers. More than 62% of large hospital networks in the country have adopted robotic picking and automated dispensing systems. Annual investments in healthcare logistics automation exceed USD 1.2 billion, with over 45% directed toward AI-enabled inventory optimization. The country operates over 2,500 automated pharmaceutical fulfillment facilities, with robotic systems handling up to 70% of order processing tasks. Key applications include hospital pharmacies, e-commerce drug distribution, and cold-chain biologics handling. Additionally, over 55% of healthcare distributors in the U.S. have integrated real-time tracking systems, improving delivery accuracy by nearly 30% and reducing manual labor dependency significantly.

Market Size & Growth: USD 567.0 million in 2025 projected to reach USD 1,991.0 million by 2033 at 17.0% CAGR, driven by rising demand for automated medical supply chains.

Top Growth Drivers: Automation adoption (65%), operational efficiency improvement (40%), error reduction in order fulfillment (35%).

Short-Term Forecast: By 2028, fulfillment automation is expected to reduce logistics costs by 28% and improve delivery speed by 32%.

Emerging Technologies: AI-driven warehouse management systems, autonomous mobile robots (AMRs), IoT-enabled inventory tracking.

Regional Leaders: North America (USD 720 million by 2033, high hospital automation), Europe (USD 520 million, regulatory-driven adoption), Asia-Pacific (USD 460 million, rapid hospital expansion).

Consumer/End-User Trends: Hospitals and e-pharmacies show 60% adoption growth, focusing on accuracy and faster deliveries.

Pilot or Case Example: In 2024, a hospital network implemented robotic fulfillment systems, improving order accuracy by 45% and reducing downtime by 25%.

Competitive Landscape: Market leader holds ~18% share, followed by 4–5 major automation solution providers.

Regulatory & ESG Impact: Compliance with drug traceability laws increased adoption by 30%, while ESG goals drive 20% energy-efficient automation uptake.

Investment & Funding Patterns: Over USD 2.5 billion invested in healthcare logistics automation projects globally in recent years.

Innovation & Future Outlook: Integration of predictive analytics and robotics is expected to improve operational efficiency by over 35%.

Healthcare Product Fulfillment Automation Market integrates robotics, AI-driven inventory systems, and cold-chain automation, with hospitals contributing nearly 48% of demand, followed by pharmaceutical distributors at 32%. Regulatory mandates for drug traceability influence over 40% of deployments. North America leads consumption at 38%, while Asia-Pacific shows fastest adoption growth. Emerging trends include AI-based demand forecasting and autonomous fulfillment centers.

The Healthcare Product Fulfillment Automation Market holds strong strategic relevance as healthcare systems globally prioritize operational efficiency, patient safety, and cost optimization. Automation technologies such as autonomous mobile robots and AI-enabled warehouse systems are reshaping logistics workflows by reducing manual errors and enhancing throughput. For instance, AI-powered fulfillment systems deliver nearly 35% improvement in order accuracy compared to traditional manual processes. These technologies enable real-time tracking, predictive inventory management, and optimized storage utilization, making them critical for large-scale healthcare providers and pharmaceutical distributors.

Regionally, North America dominates in volume, while Asia-Pacific leads in adoption with over 52% of healthcare enterprises integrating at least one form of automation into their logistics operations. The increasing penetration of e-pharmacies and same-day delivery expectations is accelerating demand for automated fulfillment centers. By 2028, AI-driven predictive analytics is expected to reduce stockouts by 40% and improve supply chain responsiveness significantly.

From a compliance perspective, firms are committing to ESG metrics such as 25% energy consumption reduction and 30% packaging waste reduction by 2030 through automated systems. In 2025, a leading healthcare provider in the United States achieved a 38% reduction in order processing time through robotic picking and AI-based demand forecasting.

Looking ahead, the Healthcare Product Fulfillment Automation Market is positioned as a cornerstone for resilient healthcare supply chains, ensuring regulatory compliance, operational efficiency, and sustainable growth in an increasingly digital healthcare ecosystem.

The Healthcare Product Fulfillment Automation Market is experiencing strong transformation driven by digitalization, increasing healthcare demand, and supply chain complexities. The growing need for accuracy in pharmaceutical distribution and medical supply delivery is encouraging healthcare providers to adopt automated solutions such as robotic picking, automated storage systems, and AI-powered inventory management. Over 58% of healthcare organizations are prioritizing automation to reduce human errors and enhance efficiency. Additionally, the surge in e-commerce-based pharmaceutical delivery has increased the need for faster and more reliable fulfillment systems. Cold-chain logistics requirements for biologics and vaccines further necessitate automated monitoring systems. Regulatory requirements for drug traceability and serialization are also influencing adoption, with over 45% of global distributors integrating compliance-focused automation tools.

The increasing demand for efficient pharmaceutical logistics is a key driver of the Healthcare Product Fulfillment Automation Market. Healthcare supply chains require high precision, as even minor errors can lead to critical consequences. Automated systems such as robotic picking and AI-based inventory management improve accuracy rates by over 40%, significantly reducing dispensing errors. Additionally, hospitals and pharmacies are experiencing growing patient volumes, with over 60% reporting increased demand for rapid drug delivery services. Automation enables faster order processing, reducing delivery times by up to 35%. E-commerce pharmaceutical platforms are expanding rapidly, with more than 50% of urban consumers preferring online medicine purchases. This trend is pushing logistics providers to adopt automated fulfillment systems to handle high order volumes efficiently while maintaining compliance with strict healthcare regulations.

High initial capital investment is a significant restraint in the Healthcare Product Fulfillment Automation Market. Implementing advanced automation systems, including robotics and AI-based platforms, requires substantial upfront costs, often exceeding 25% of total operational budgets for healthcare facilities. Small and mid-sized healthcare providers face challenges in allocating resources for such investments. Additionally, maintenance and system integration costs can increase operational expenses by 15–20%. Workforce training is another barrier, as over 40% of healthcare staff require specialized training to operate automated systems effectively. Integration with legacy systems can also lead to delays and inefficiencies, with nearly 30% of organizations reporting challenges in system compatibility. These financial and operational constraints limit adoption, particularly in developing regions where budget allocations for healthcare infrastructure remain constrained.

The expansion of e-pharmacy platforms and home healthcare services presents significant opportunities for the Healthcare Product Fulfillment Automation Market. With more than 55% of patients preferring home delivery of medications, there is a growing need for efficient and scalable fulfillment systems. Automated warehouses can process orders up to 50% faster, enabling same-day or next-day delivery services. The rise in chronic diseases has increased demand for regular medication supply, further driving automation adoption. Additionally, telehealth services are expanding, with over 48% of healthcare providers integrating digital platforms, creating new demand for automated logistics solutions. Advanced technologies such as AI-driven demand forecasting and IoT-based tracking systems are enhancing supply chain visibility, reducing stockouts by nearly 30%, and improving patient satisfaction levels significantly.

Regulatory complexities pose a major challenge for the Healthcare Product Fulfillment Automation Market. Healthcare supply chains are subject to strict regulations related to drug safety, traceability, and storage conditions. Compliance requirements such as serialization and track-and-trace systems increase implementation complexity, with over 50% of companies reporting delays due to regulatory approvals. Additionally, maintaining compliance with varying international standards can increase operational costs by up to 18%. Data security and patient privacy regulations also add to the complexity, requiring robust cybersecurity measures. Nearly 35% of healthcare organizations have reported challenges in aligning automation systems with compliance frameworks. These regulatory hurdles can slow down the adoption of automation technologies, particularly for companies operating across multiple regions.

Rapid Adoption of Autonomous Mobile Robots (AMRs): Over 48% of healthcare warehouses have integrated AMRs to streamline picking and transportation tasks. These robots improve operational efficiency by nearly 35% and reduce labor dependency by 28%, enabling faster order fulfillment and minimizing human errors in high-volume environments.

Expansion of AI-Driven Predictive Inventory Systems: Approximately 52% of healthcare providers are deploying AI-based inventory solutions that reduce stockouts by 30% and improve demand forecasting accuracy by 40%. These systems enable real-time decision-making and optimize storage utilization significantly.

Growth in Cold-Chain Automation Technologies: Around 45% of pharmaceutical logistics operations now utilize automated temperature monitoring systems, ensuring compliance with strict storage requirements. These technologies reduce product spoilage by 25% and enhance traceability across supply chains.

Integration of IoT and Real-Time Tracking Systems: Nearly 58% of healthcare distributors are implementing IoT-enabled tracking systems, improving shipment visibility by 50% and reducing delivery delays by 20%. These solutions enhance transparency and support regulatory compliance effectively.

The Healthcare Product Fulfillment Automation Market is segmented based on type, application, and end-user, each playing a critical role in shaping overall industry dynamics. Automation solutions vary significantly, ranging from robotic systems to software-based inventory platforms. Applications span across hospital pharmacies, distribution centers, and e-commerce healthcare platforms, reflecting diverse operational needs. End-users include hospitals, pharmaceutical companies, and logistics providers, each contributing differently to market demand. Over 48% of automation deployment is concentrated in hospital-based applications, while pharmaceutical distribution accounts for nearly 32%. The increasing demand for precision, compliance, and speed is driving adoption across all segments.

Robotic systems dominate the Healthcare Product Fulfillment Automation Market, accounting for approximately 44% of total adoption due to their efficiency in handling high-volume operations. Automated storage and retrieval systems (AS/RS) hold around 28%, offering optimized space utilization and improved inventory accuracy. However, AI-based warehouse management systems are the fastest-growing segment, expanding at a rate exceeding 19% annually due to their ability to enhance decision-making and predictive analytics capabilities. Conveyor and sorting systems, along with barcode and RFID technologies, collectively contribute nearly 28% of the market, supporting logistics efficiency and traceability.

• In 2025, a large hospital network implemented robotic dispensing systems, improving order accuracy for over 5 million prescriptions annually and reducing manual intervention by 35%.

Hospital pharmacy automation leads the market with approximately 48% share, driven by the need for precision and regulatory compliance. Pharmaceutical distribution accounts for nearly 30%, focusing on large-scale logistics efficiency. E-commerce healthcare fulfillment is the fastest-growing application, expanding at over 20% annually due to increasing online medicine purchases. Other applications, including diagnostic supply chains and clinical trial logistics, collectively contribute around 22%. In 2025, over 42% of hospitals globally reported testing automation systems to enhance operational efficiency. Additionally, nearly 60% of consumers prefer faster delivery options, influencing adoption trends.

• In 2025, automated fulfillment systems were deployed across over 200 healthcare distribution centers, improving delivery accuracy for millions of orders annually.

Hospitals represent the largest end-user segment, accounting for approximately 48% of the market, driven by increasing patient volumes and demand for efficient supply chain management. Pharmaceutical companies hold around 30%, focusing on large-scale distribution and compliance requirements. Logistics providers are the fastest-growing segment, expanding at over 18% annually due to rising demand for outsourced fulfillment services. Other end-users, including clinics and diagnostic centers, contribute nearly 22%. Over 55% of healthcare organizations have adopted automation solutions to improve operational efficiency and reduce costs.

• In 2025, over 500 healthcare facilities globally integrated automated fulfillment systems, improving operational efficiency and reducing order processing times significantly.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 19.0% between 2026 and 2033.

North America leads with over 2,500 automated healthcare fulfillment centers and more than 60% adoption among large hospitals. Europe follows with approximately 27% share, driven by regulatory compliance and sustainability initiatives. Asia-Pacific holds around 24% share, supported by rapid healthcare infrastructure expansion in China, India, and Japan. South America and Middle East & Africa collectively account for nearly 11%, with increasing investments in healthcare logistics.

North America holds approximately 38% of the Healthcare Product Fulfillment Automation Market, driven by strong healthcare infrastructure and technological adoption. The region’s demand is fueled by hospital networks, pharmaceutical distributors, and e-commerce healthcare platforms. Regulatory frameworks emphasizing drug traceability and patient safety encourage automation adoption. Over 62% of hospitals in the region utilize automated fulfillment systems. Companies are investing heavily in robotics and AI, with local players implementing advanced warehouse automation technologies. Consumer behavior reflects high adoption of online pharmacy services, with over 58% preferring digital ordering and home delivery.

Europe accounts for nearly 27% of the Healthcare Product Fulfillment Automation Market, with key markets including Germany, the UK, and France. Strict regulatory frameworks drive demand for compliant automation systems. Sustainability initiatives encourage energy-efficient solutions, with over 35% of facilities adopting green automation technologies. Adoption of AI and IoT solutions is increasing rapidly, improving operational efficiency. Local companies focus on developing advanced logistics systems. Consumer behavior shows a preference for reliable and compliant healthcare delivery systems.

Asia-Pacific represents approximately 24% of the market and is the fastest-growing region. Countries such as China, India, and Japan are investing heavily in healthcare infrastructure and automation technologies. The region is witnessing rapid growth in e-commerce healthcare platforms, with over 50% of urban populations adopting online pharmacy services. Automation adoption is supported by government initiatives and increasing healthcare demand. Consumer behavior is influenced by mobile-based healthcare services and digital platforms.

South America accounts for around 6% of the market, with Brazil and Argentina as key contributors. Investments in healthcare infrastructure and logistics are increasing, supporting automation adoption. Government initiatives promoting digital healthcare are encouraging growth. Local companies are exploring automation solutions to improve efficiency. Consumer behavior reflects growing demand for accessible healthcare services.

Middle East & Africa holds approximately 5% of the market, with growth driven by modernization initiatives in healthcare systems. Countries such as the UAE and South Africa are investing in advanced logistics infrastructure. Automation technologies are being adopted to improve efficiency and compliance. Consumer behavior reflects increasing demand for reliable healthcare delivery systems.

United States – 34% Market share: Driven by high automation deployment and advanced healthcare infrastructure

Germany – 11% Market share: Supported by strong pharmaceutical manufacturing and regulatory compliance

The Healthcare Product Fulfillment Automation Market is moderately fragmented, with over 40 active global and regional competitors offering diverse automation solutions. The top five companies collectively account for approximately 52% of the market, indicating a semi-consolidated structure. Leading players focus on robotics, AI integration, and advanced warehouse management systems to strengthen their market position.

Strategic initiatives such as partnerships, mergers, and acquisitions are common, with over 25 major collaborations recorded in the past two years. Companies are investing in R&D, allocating nearly 12–15% of their budgets to innovation. Product launches focusing on AI-driven automation and IoT-enabled tracking systems are increasing, with over 30 new solutions introduced recently. Competitive differentiation is driven by technological capabilities, scalability, and compliance features, making innovation a key factor in maintaining market leadership.

SSI Schaefer Group

Dematic

Honeywell Intelligrated

Swisslog Healthcare

Omnicell, Inc.

BD (Becton, Dickinson and Company)

McKesson Corporation

AmerisourceBergen Corporation

Cardinal Health, Inc.

Tecsys Inc.

Manhattan Associates

Körber Supply Chain

TGW Logistics Group

The Healthcare Product Fulfillment Automation Market is being shaped by rapid advancements in robotics, artificial intelligence, and digital supply chain technologies. Autonomous mobile robots (AMRs) are increasingly deployed, with over 48% of automated warehouses utilizing them for picking and transportation tasks. These robots improve operational efficiency by up to 35% and significantly reduce manual labor requirements. AI-driven warehouse management systems are gaining traction, with approximately 52% of healthcare facilities implementing predictive analytics to optimize inventory levels and reduce stockouts by nearly 30%.

IoT-enabled tracking systems are transforming logistics visibility, with more than 58% of healthcare distributors adopting real-time monitoring solutions. These systems enhance shipment transparency and reduce delivery delays by 20%. Cold-chain automation technologies are also critical, with around 45% of pharmaceutical logistics operations using automated temperature monitoring to ensure compliance and reduce spoilage rates by 25%.

Cloud-based platforms are facilitating integration across supply chains, enabling seamless data exchange and improving decision-making. Blockchain technology is emerging as a solution for drug traceability, with pilot projects showing up to 40% improvement in supply chain transparency. Additionally, digital twin technology is being explored to simulate warehouse operations, improving efficiency by 28%. These technological advancements are driving the evolution of automated healthcare fulfillment systems, making them more efficient, reliable, and scalable.

• In December 2025, Omnicell, Inc. announced the launch of its Titan XT automated dispensing system, designed to unify cloud-based intelligence with automation. The system enables enterprise-wide medication inventory visibility and integrates nursing workflows, supporting fully connected healthcare fulfillment ecosystems. Source: www.ir.omnicell.com

• In May 2025, Omnicell, Inc. introduced its MedTrack RFID-enabled product line to enhance medication tracking and workflow efficiency. The system enables real-time visibility of drug inventory and supports “grab-and-go” dispensing, reducing documentation burden and improving fulfillment accuracy across operating rooms and clinical settings.

• In October 2025, Omnicell, Inc. deployed IVX robotic compounding systems in a central fill pharmacy, enabling automated preparation and dispensing of millions of medication doses. The deployment achieved zero medication picking errors across nearly nine million doses, significantly improving fulfillment precision and patient safety.

• In 2025, Omnicell, Inc. expanded its automation capabilities through a new innovation lab focused on robotics and AI-driven medication management solutions. The initiative aims to address workforce shortages and enhance fulfillment efficiency by developing next-generation automation technologies for healthcare supply chains.

The Healthcare Product Fulfillment Automation Market Report provides a comprehensive analysis of automation technologies applied across healthcare logistics and supply chains. The scope covers multiple segments including robotic systems, automated storage solutions, AI-driven warehouse management systems, and IoT-enabled tracking technologies. The report evaluates applications across hospital pharmacies, pharmaceutical distribution centers, e-commerce healthcare platforms, and diagnostic supply chains, offering insights into operational efficiencies and adoption trends.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing regional variations in infrastructure development, regulatory frameworks, and technology adoption. It highlights key markets such as the United States, Germany, China, India, and Brazil, providing detailed insights into regional demand patterns and technological advancements.

The report also focuses on end-user industries including hospitals, pharmaceutical companies, logistics providers, and clinics, examining their adoption behavior and operational requirements. Emerging technologies such as AI, robotics, blockchain, and digital twin systems are analyzed for their impact on supply chain optimization. Additionally, the report covers innovation trends, investment patterns, and regulatory influences shaping the market. Overall, it provides a strategic overview for stakeholders to understand market dynamics, identify growth opportunities, and make informed business decisions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 567.0 Million |

| Market Revenue (2033) | USD 1,991.0 Million |

| CAGR (2026–2033) | 17.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Daifuku Co., Ltd.; SSI Schaefer Group; Dematic; Honeywell Intelligrated; Swisslog Healthcare; Omnicell, Inc.; BD (Becton, Dickinson and Company); McKesson Corporation; AmerisourceBergen Corporation; Cardinal Health, Inc.; Tecsys Inc.; Manhattan Associates; Körber Supply Chain; TGW Logistics Group |

| Customization & Pricing | Available on Request (10% Customization Free) |