Reports

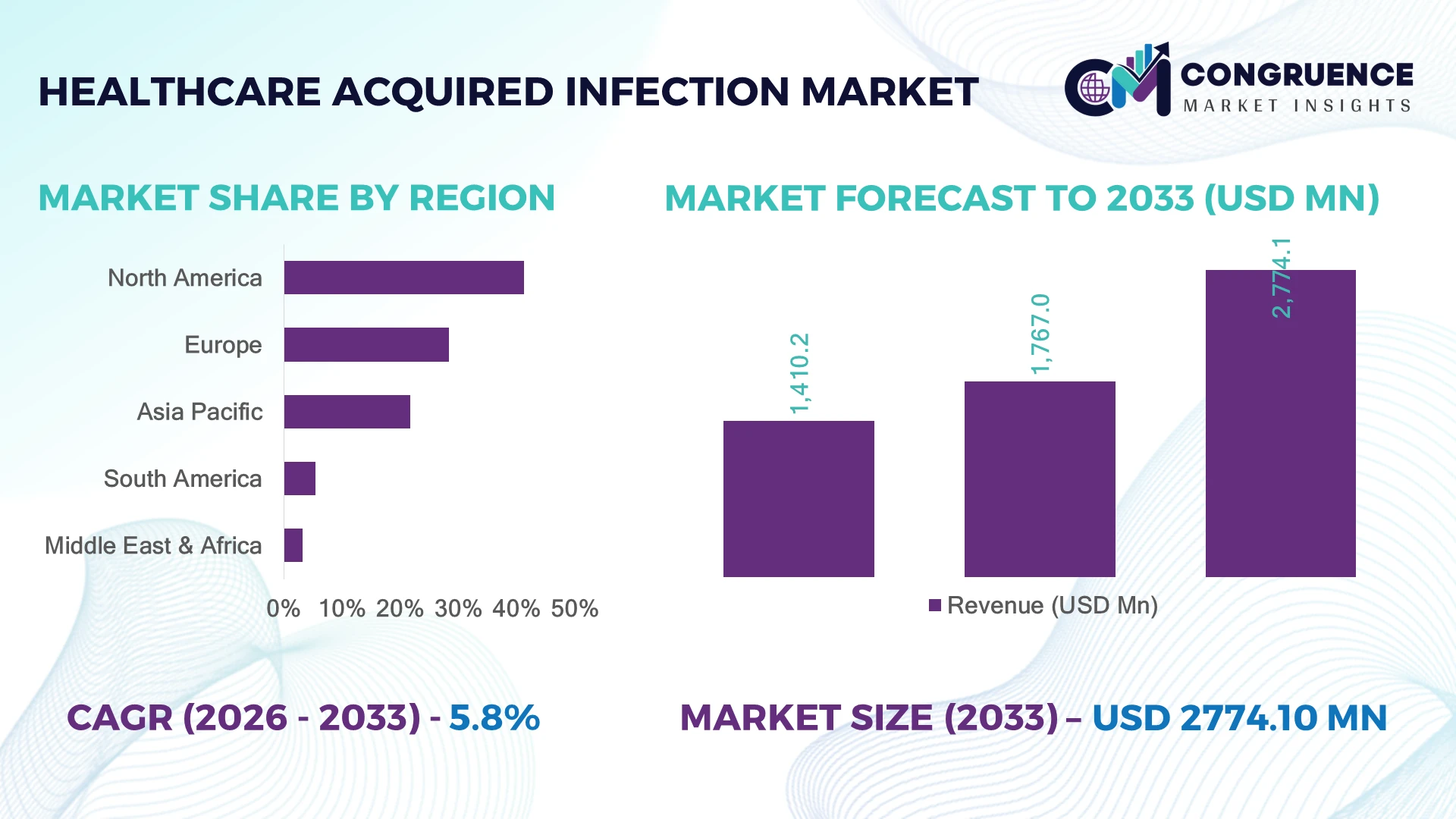

The Global Healthcare-Acquired Infection Market was valued at USD 1,767.0 Million in 2025 and is anticipated to reach a value of USD 2,774.1 Million by 2033 expanding at a CAGR of 5.8% between 2026 and 2033. Growth is driven by stricter infection prevention protocols, rising antimicrobial resistance, expanding hospital surveillance programs, and accelerated adoption of rapid molecular diagnostics across acute and long-term care facilities.

The United States dominates the global Healthcare-Acquired Infection Market with approximately 39% market share, supported by extensive acute-care infrastructure, nationwide infection surveillance programs, and continuous investments exceeding USD 2 billion in hospital infection prevention technologies and digital monitoring. Compared with Germany, which emphasizes standardized antimicrobial stewardship across public hospitals, the U.S. demonstrates broader AI-enabled surveillance deployment following strengthened post-pandemic healthcare preparedness initiatives.

This leadership strengthens innovation pipelines, regulatory compliance, and competitive expansion strategies across global healthcare systems.

Market Size & Growth: USD 1,767.0 Million (2025) reaching USD 2,774.1 Million (2033) at 5.8% CAGR, driven by advanced molecular diagnostics and automated infection surveillance.

Top Growth Drivers: Hospital surveillance adoption +28%, antimicrobial stewardship implementation +24%, rapid diagnostic utilization +31%.

Short-Term Forecast: By 2028, automated infection reporting is expected to improve hospital response efficiency by 35% while reducing manual reporting time.

Emerging Technologies: AI-powered surveillance, rapid PCR diagnostics, and UV-C disinfection robotics are transforming high-growth infection control operations.

Regional Leaders: North America (~USD 760 Million), Europe (~USD 520 Million), Asia-Pacific (~USD 360 Million) lead through digital healthcare expansion and laboratory modernization.

Consumer/End-User Trends: More than 68% of tertiary hospitals are expanding continuous infection monitoring and antimicrobial stewardship initiatives.

Pilot/Case Example: In 2024, AI-assisted infection surveillance programs reduced healthcare-associated bloodstream infections by nearly 27% in participating hospital networks.

Competitive Landscape: Leading companies collectively account for approximately 42% of global activity, including Becton Dickinson, bioMérieux, 3M, STERIS, and Getinge.

Regulatory & ESG Impact: Updated infection-control regulations improved hospital compliance rates by over 30%, while reusable sterilization systems reduced medical waste generation.

Investment & Funding: More than USD 1.5 billion supports laboratory modernization, strategic partnerships, and digital infection-control infrastructure amid regional healthcare expansion.

Innovation & Future Outlook: Next-generation genomic surveillance, predictive analytics, and integrated digital infection platforms are strengthening long-term clinical decision-making and operational resilience.

Healthcare-Acquired Infection Market demand continues expanding across acute-care hospitals, diagnostic laboratories, ambulatory surgical centers, and long-term care facilities as healthcare providers prioritize rapid detection and infection containment. AI-assisted surveillance, multiplex molecular testing, and automated sterilization technologies are improving clinical workflows, while over 40% of major healthcare networks are accelerating digital infection monitoring initiatives. Strengthened infection-control regulations and resilient medical supply-chain planning are reinforcing sustained technology deployment, setting the stage for broader strategic market development.

Healthcare-acquired infection management has become a strategic priority as healthcare providers focus on patient safety, operational efficiency, and regulatory compliance. Competitive differentiation increasingly depends on integrated surveillance platforms, advanced diagnostics, and standardized infection prevention workflows. Healthcare infrastructure modernization and digital hospital transformation are accelerating procurement of intelligent monitoring systems, while stronger reporting requirements are reshaping procurement priorities across public and private healthcare networks.

AI-enabled infection surveillance platforms identify infection risks approximately 40% faster than traditional manual monitoring systems while reducing administrative workload by nearly 30% through automated reporting and predictive analytics. North America leads in enterprise-wide digital deployment and integrated surveillance networks, whereas Asia-Pacific is expanding through rapid hospital construction, laboratory modernization, and government-backed infection control initiatives. During the next two to three years, automated surveillance integration across large hospital systems is expected to exceed 70% in several developed healthcare markets.

Healthcare organizations are increasingly deploying connected infection prevention ecosystems that combine laboratory diagnostics, electronic health records, and environmental monitoring into unified operational platforms. Companies are expanding strategic partnerships with hospital networks, investing in AI-enabled software capabilities, and strengthening regional manufacturing and service footprints to improve implementation speed. Organizations that integrate predictive infection intelligence with scalable clinical workflows will secure stronger competitive positioning, greater operational resilience, and lasting value within the evolving global healthcare landscape.

Healthcare providers are accelerating investments in digital infection surveillance and rapid molecular diagnostics to reduce preventable hospital-acquired infections and comply with increasingly stringent reporting standards. More than 70% of large hospitals in the United States have implemented electronic infection surveillance, while AI-assisted monitoring has improved early outbreak detection by approximately 35% and reduced manual surveillance workloads by nearly 30%. Updated infection-control regulations and strengthened antimicrobial stewardship programs following the COVID-19 period have intensified technology adoption across tertiary care facilities. This operational shift enables earlier intervention, standardized clinical decision-making, and lower treatment complexity. In response, leading companies are expanding cloud-based surveillance platforms, forming partnerships with healthcare systems, and integrating laboratory diagnostics with electronic health records to strengthen competitive differentiation and long-term customer retention.

Healthcare-acquired infection management remains constrained by uneven digital infrastructure, limited laboratory capacity, and integration costs across developing healthcare systems. Approximately 45% of hospitals in lower-income countries continue to face inadequate microbiology laboratory capabilities, while interoperability challenges increase implementation timelines by nearly 25% for enterprise surveillance platforms. Dependence on imported diagnostic reagents and specialized laboratory consumables further exposes healthcare providers to procurement disruptions and inventory fluctuations, particularly in countries relying on international medical supply chains. These structural constraints slow deployment, increase operational expenditure, and delay standardized infection reporting. Companies are mitigating these risks by localizing manufacturing, expanding distributor partnerships, developing modular software architectures, and securing long-term procurement agreements that improve supply continuity and deployment efficiency.

The convergence of artificial intelligence, genomic sequencing, and connected hospital infrastructure is creating new value across infection prevention ecosystems. Predictive infection analytics can improve risk identification by nearly 40%, while automated clinical decision support reduces response times by approximately 30%. India and Saudi Arabia are expanding digitally connected hospital infrastructure through national healthcare modernization initiatives, creating strong demand for integrated infection management platforms. Cloud-native surveillance, pathogen genomics, and real-time environmental monitoring represent emerging technology priorities that extend beyond traditional laboratory diagnostics. Companies are increasing R&D investments, collaborating with digital health providers, and building interoperable software ecosystems capable of supporting remote monitoring, predictive epidemiology, and enterprise-wide infection intelligence, creating differentiated long-term competitive advantages.

Long-term market expansion depends on seamless integration between infection surveillance systems, laboratory information systems, and electronic health records while maintaining consistent cybersecurity and clinical accuracy. Nearly 32% of healthcare organizations report shortages of trained infection prevention specialists, and complex multi-vendor system integration can extend deployment schedules by more than 20%. In the United Kingdom, increasing cybersecurity expectations for connected healthcare infrastructure have added additional validation and compliance requirements for digital clinical platforms. These execution challenges affect deployment consistency, user adoption, and operational scalability across large healthcare networks. Companies must strengthen workforce training, expand cybersecurity capabilities, develop standardized interoperability frameworks, and establish strategic partnerships with healthcare IT providers to deliver resilient, enterprise-scale infection management solutions.

AI-Powered Surveillance Expansion – Healthcare systems are rapidly replacing manual infection monitoring with AI-enabled surveillance platforms, improving early outbreak detection by nearly 35% while reducing infection reporting time by approximately 30%. Large hospital networks in the United States are integrating predictive analytics with electronic health records following stricter infection reporting requirements. Technology providers are scaling cloud-based platforms and expanding software partnerships to deliver enterprise-wide infection intelligence and standardized clinical workflows.

Rapid Molecular Diagnostics Adoption – Multiplex PCR and syndromic molecular testing now account for more than 45% of advanced hospital infection investigations in leading tertiary hospitals, reducing diagnostic turnaround times by over 60% compared with conventional culture methods. Growing antimicrobial resistance is accelerating deployment across critical care departments. Companies are expanding manufacturing capacity and collaborating with hospital laboratories to improve workflow automation and testing consistency.

Smart Sterilization Automation – Healthcare providers are deploying automated sterilization systems, UV-C disinfection robots, and digital instrument tracking, lowering equipment processing errors by nearly 25% while improving sterilization compliance above 90%. Workforce shortages are encouraging greater process automation throughout central sterile departments. Manufacturers are strengthening robotics portfolios and integrating IoT-based asset monitoring to improve operational efficiency and equipment utilization.

Integrated Infection Prevention Ecosystems – Hospitals are consolidating surveillance software, laboratory information systems, and environmental monitoring into unified digital platforms, improving operational visibility by approximately 40% while reducing duplicated administrative tasks by nearly 28%. Enterprise buyers increasingly prefer interoperable solutions over standalone products. Companies are responding through platform acquisitions, interoperability partnerships, and modular software development that supports scalable deployment across multi-site healthcare organizations.

Diagnostics remain the leading segment of the Healthcare-Acquired Infection Market, accounting for an estimated 46% of overall demand due to their central role in early pathogen identification, antimicrobial stewardship, and regulatory compliance. Hospitals increasingly prioritize rapid molecular diagnostics and automated microbiology platforms to reduce treatment delays and improve patient outcomes. Therapeutics continue to represent a mature segment driven by rising antimicrobial resistance and the need for targeted treatment strategies, while Infection Control Products maintain stable demand through sterilization systems, disinfectants, personal protective equipment, and environmental hygiene solutions. Infection Control Products represent the fastest-growing segment as hospitals modernize sterilization infrastructure and invest in automated disinfection technologies. Adoption of connected sterilization equipment has increased by approximately 29% among large healthcare networks, while integrated infection prevention solutions improve operational efficiency by nearly 32%. Companies are expanding product portfolios through acquisitions, introducing AI-enabled monitoring technologies, and strengthening partnerships with hospital systems. Investment priorities increasingly emphasize integrated prevention ecosystems that combine diagnostics, disinfection, and surveillance into unified clinical workflows.

Surgical Site Infections (SSIs) represent the largest application segment because they remain one of the most closely monitored hospital-acquired complications requiring continuous surveillance, sterilization, and antimicrobial management. SSIs account for approximately 30% of healthcare-associated infections in many acute-care settings, driving sustained demand for rapid diagnostics and infection prevention technologies. Bloodstream Infections and Hospital-Acquired Pneumonia continue to require intensive monitoring due to high treatment complexity, while Gastrointestinal Infections and other healthcare-associated conditions support specialized diagnostic and containment strategies. Hospital-Acquired Pneumonia (HAP/VAP) is emerging as the fastest-growing application due to expanded intensive care utilization and advanced respiratory monitoring technologies. AI-assisted monitoring has reduced critical-care infection response times by nearly 28%, while automated surveillance deployment has improved workflow efficiency by approximately 34%. Companies are expanding respiratory infection diagnostics, strengthening ICU-focused partnerships, and integrating predictive analytics into critical care platforms. Demand is increasingly shifting toward continuous monitoring solutions capable of supporting real-time infection prevention rather than reactive clinical intervention.

Hospitals remain the dominant end-user segment, representing approximately 68% of market demand because of their extensive patient volumes, critical care capacity, and regulatory infection reporting obligations. Large tertiary hospitals continue investing in integrated surveillance software, rapid laboratory diagnostics, and automated sterilization systems to improve clinical efficiency and reduce preventable infections. Diagnostic Laboratories remain strategically important by supporting pathogen identification and antimicrobial susceptibility testing, while Long-Term Care Facilities are expanding infection monitoring programs for vulnerable patient populations. Ambulatory Surgical Centers (ASCs) represent the fastest-growing end-user segment as outpatient surgical procedures continue increasing and facilities strengthen infection prevention protocols. Digital infection monitoring adoption among ASCs has expanded by nearly 31%, while automated sterilization investments have improved procedural workflow efficiency by approximately 24%. Companies are introducing scalable cloud-based surveillance platforms, flexible pricing models, and specialized infection management solutions tailored to outpatient environments. Competitive strategies increasingly focus on interoperable platforms that can serve hospitals, laboratories, and ambulatory facilities through a unified infection prevention ecosystem.

North America accounted for the largest market share at 41.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America remains the leading Healthcare-Acquired Infection Market owing to its mature healthcare infrastructure, extensive infection surveillance networks, and widespread deployment of molecular diagnostics. The region contributes approximately 41.2% of global demand, supported by high adoption of AI-enabled infection monitoring across large hospital systems. More than 72% of tertiary healthcare facilities have implemented electronic infection surveillance integrated with electronic health records, improving response speed and compliance with evolving reporting requirements. Continued investment in laboratory modernization, antimicrobial stewardship, and automated sterilization technologies is strengthening operational efficiency. Strategic collaborations between healthcare providers and technology companies continue to accelerate enterprise-scale deployment and integrated infection prevention programs.

United States Market Outlook: The United States represents the largest national market because of its extensive acute-care infrastructure, strong reimbursement environment, and rigorous infection reporting standards. More than 6,000 hospitals actively participate in standardized healthcare quality monitoring programs, while large healthcare systems continue expanding AI-assisted infection surveillance and rapid molecular diagnostics. Domestic manufacturers and digital health companies are increasing partnerships with hospital networks to strengthen predictive infection management, laboratory automation, and enterprise interoperability across nationwide healthcare facilities.

Europe maintains a strong position through harmonized infection prevention standards, advanced laboratory capabilities, and expanding digital healthcare infrastructure. The region accounts for approximately 28.4% of the global market, with hospitals prioritizing antimicrobial stewardship, rapid pathogen detection, and automated surveillance systems. More than 65% of major university hospitals have integrated digital infection reporting into clinical workflows, improving regulatory compliance and operational transparency. Healthcare modernization programs and sustainable sterilization practices continue supporting technology upgrades, while strategic collaborations between diagnostic manufacturers and public healthcare systems strengthen long-term operational resilience.

Germany Market Outlook: Germany leads the European market through its highly developed hospital network, advanced microbiology laboratories, and strong investment in digital healthcare modernization. Large university hospitals continue deploying automated microbiology platforms and integrated laboratory information systems to improve infection surveillance efficiency. National antimicrobial stewardship initiatives and structured infection prevention frameworks encourage continuous adoption of molecular diagnostics, while domestic medical technology companies expand innovation through collaborative healthcare research and enterprise partnerships.

Asia-Pacific is emerging as the fastest-expanding regional market, driven by hospital construction, laboratory modernization, and digital healthcare transformation across developing economies. The region represents approximately 21.7% of global demand, with governments increasing investment in infection prevention technologies and diagnostic capacity. More than 30% of newly commissioned tertiary hospitals across major Asian economies are incorporating centralized digital infection surveillance platforms during initial infrastructure development. Growing healthcare expenditure, expanding intensive care capacity, and rising awareness of antimicrobial resistance continue accelerating enterprise deployment of advanced infection management solutions.

China Market Outlook: China dominates the regional market through its extensive hospital network, expanding domestic diagnostics manufacturing, and national healthcare modernization initiatives. Thousands of tertiary hospitals continue adopting automated microbiology laboratories and AI-supported clinical decision systems to strengthen infection monitoring. Local manufacturers are expanding molecular diagnostics production while healthcare providers invest in digital hospital ecosystems that improve laboratory efficiency, standardize infection reporting, and enhance patient safety across large healthcare networks.

South America continues strengthening its Healthcare-Acquired Infection Market through gradual hospital modernization, expanding laboratory capabilities, and improved infection prevention policies. The region contributes approximately 5.4% of global demand, with public healthcare systems prioritizing surveillance modernization and standardized infection reporting. Digital laboratory adoption has increased by nearly 24% among major referral hospitals, improving diagnostic turnaround and operational visibility. Budget limitations remain a constraint, yet increasing partnerships with international diagnostic suppliers and healthcare technology providers are enhancing deployment capacity and supporting broader infection prevention initiatives.

Brazil Market Outlook: Brazil remains the largest market in South America because of its extensive hospital infrastructure, expanding diagnostic laboratory network, and national healthcare system. Large metropolitan hospitals continue investing in automated laboratory platforms and centralized infection surveillance software to improve compliance and patient safety. Private healthcare providers are strengthening partnerships with global diagnostics companies while increasing investments in molecular testing capabilities and hospital digitalization programs that support scalable infection management.

The Middle East & Africa market is advancing through healthcare infrastructure expansion, hospital digitalization, and national healthcare diversification initiatives. The region accounts for approximately 3.3% of global demand, supported by investments in specialized medical facilities, laboratory modernization, and infection prevention technologies. Several newly developed tertiary hospitals are deploying integrated infection surveillance platforms alongside automated sterilization systems to improve operational consistency. Public-private partnerships and healthcare infrastructure investments continue strengthening enterprise adoption despite differences in healthcare maturity across individual countries.

Saudi Arabia Market Outlook: Saudi Arabia leads regional development through large-scale healthcare investment, hospital expansion projects, and digital health transformation under Vision 2030. Newly commissioned hospitals increasingly deploy integrated laboratory information systems, AI-assisted infection surveillance, and advanced sterilization technologies. National healthcare authorities continue supporting enterprise modernization through strategic procurement programs and technology partnerships, enabling broader deployment of connected infection prevention solutions across both public and private healthcare institutions.

The Healthcare-Acquired Infection Market is characterized by competition between global diagnostics leaders including Becton, Dickinson and Company (BD), bioMérieux, Thermo Fisher Scientific, 3M, and STERIS and regional infection-control manufacturers offering cost-focused sterilization and consumable solutions. The top five companies collectively account for approximately 43% of the market, creating a moderately consolidated competitive structure. Competition centers on molecular diagnostics, AI-enabled surveillance, sterilization technologies, laboratory automation, and integrated infection prevention platforms rather than price alone. Advanced diagnostic platforms reduce pathogen identification time by over 60%, while automated surveillance improves workflow efficiency by nearly 35%, strengthening customer retention. Companies increasingly compete through acquisitions, hospital partnerships, manufacturing expansion, and vertically integrated service offerings combining diagnostics, software, and sterilization solutions. Consolidation is shifting competitive advantage toward technology ecosystems with interoperable digital platforms. Regulatory validation, clinical evidence, and established hospital relationships remain significant entry barriers. Success depends on delivering clinically validated, integrated, scalable solutions with rapid deployment and strong service capabilities.

bioMérieux SA

Thermo Fisher Scientific Inc.

3M Company

STERIS plc

Getinge AB

Ecolab Inc.

Abbott Laboratories

F. Hoffmann-La Roche Ltd.

Siemens Healthineers AG

Danaher Corporation

Cardinal Health, Inc.

Advanced Sterilization Products (Fortive)

Baxter International Inc.

Healthcare-acquired infection management is rapidly shifting from reactive laboratory testing to integrated digital prevention ecosystems. Artificial intelligence, rapid multiplex PCR, next-generation sequencing, and cloud-based surveillance platforms are enabling continuous infection monitoring across hospitals. More than 65% of large tertiary healthcare systems have implemented digital infection surveillance, while AI-assisted analytics reduce manual reporting effort by approximately 30%. Integration with electronic health records enables faster outbreak detection and standardized antimicrobial stewardship, providing measurable operational advantages for healthcare providers.

Rapid molecular diagnostics outperform conventional culture-based testing by reducing pathogen identification time by more than 60%, allowing earlier targeted therapy and improved infection containment. Automated sterilization tracking, IoT-enabled environmental monitoring, and robotic UV-C disinfection further improve compliance by nearly 25% while lowering process variability. Technology leaders with integrated software, diagnostics, and laboratory automation portfolios benefit from stronger customer retention than vendors offering standalone infection-control products.

Between 2026 and 2028, predictive infection intelligence, digital twins for hospital operations, and genomic surveillance platforms will reshape enterprise infection prevention strategies. Healthcare providers are expected to expand interoperable platforms supporting laboratory systems, pharmacy data, and clinical workflows, increasing enterprise deployment beyond 75% among major healthcare networks. Organizations adopting unified infection management technologies now will achieve stronger operational resilience, faster regulatory compliance, and more sustainable competitive differentiation as healthcare systems continue prioritizing digital quality improvement initiatives.

September 2024 – Becton, Dickinson and Company (BD) announced new clinical evidence showing its BD MaxPlus™ and BD MaxZero™ needle-free connectors achieved more than 2× lower central line-associated bloodstream infection rates versus comparator designs, strengthening hospital infection prevention programs. Source: www.news.bd.com

February 2025 – bioMérieux entered a strategic research partnership with Vall d'Hebron University Hospital to advance infectious disease research, laboratory automation, and data surveillance, reinforcing innovation across clinical microbiology and antimicrobial resistance management.

June 2025 – bioMérieux completed the acquisition of Day Zero Diagnostics, expanding genome sequencing and machine-learning capabilities for rapid infectious disease diagnostics with a transaction valued at approximately €19 million, strengthening precision infection detection.

November 2024 – The World Health Organization (WHO) released its updated global Infection Prevention and Control report, highlighting that strengthened IPC programs and improved WASH implementation can substantially reduce healthcare-associated infections, prompting governments to expand national infection prevention investments.

The report provides comprehensive analysis of the Healthcare-Acquired Infection Market across Diagnostics, Therapeutics, and Infection Control Products, evaluating demand trends across Surgical Site Infections, Bloodstream Infections, Urinary Tract Infections, Hospital-Acquired Pneumonia, Gastrointestinal Infections, and other clinical applications. It further assesses adoption across hospitals, diagnostic laboratories, ambulatory surgical centers, long-term care facilities, and other healthcare providers while examining competitive positioning across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 40% of the analysis emphasizes digital infection prevention technologies and enterprise deployment patterns.

The study evaluates AI-enabled surveillance, molecular diagnostics, laboratory automation, genomic sequencing, connected sterilization systems, and interoperable healthcare software while assessing innovation strategies adopted by leading global companies. It delivers strategic insights supporting investment prioritization, technology adoption, partnership evaluation, regional expansion planning, competitive benchmarking, procurement decisions, and operational transformation, enabling stakeholders to identify high-potential opportunities and evolving market dynamics throughout the 2026–2033 forecast period.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,767.0 Million |

| Market Revenue (2033) | USD 2,774.1 Million |

| CAGR (2026–2033) | 5.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Becton, Dickinson and Company (BD); bioMérieux SA; Thermo Fisher Scientific Inc.; 3M Company; STERIS plc; Getinge AB; Ecolab Inc.; Abbott Laboratories; F. Hoffmann-La Roche Ltd.; Siemens Healthineers AG; Danaher Corporation; Cardinal Health, Inc.; Advanced Sterilization Products (Fortive); Baxter International Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |