Reports

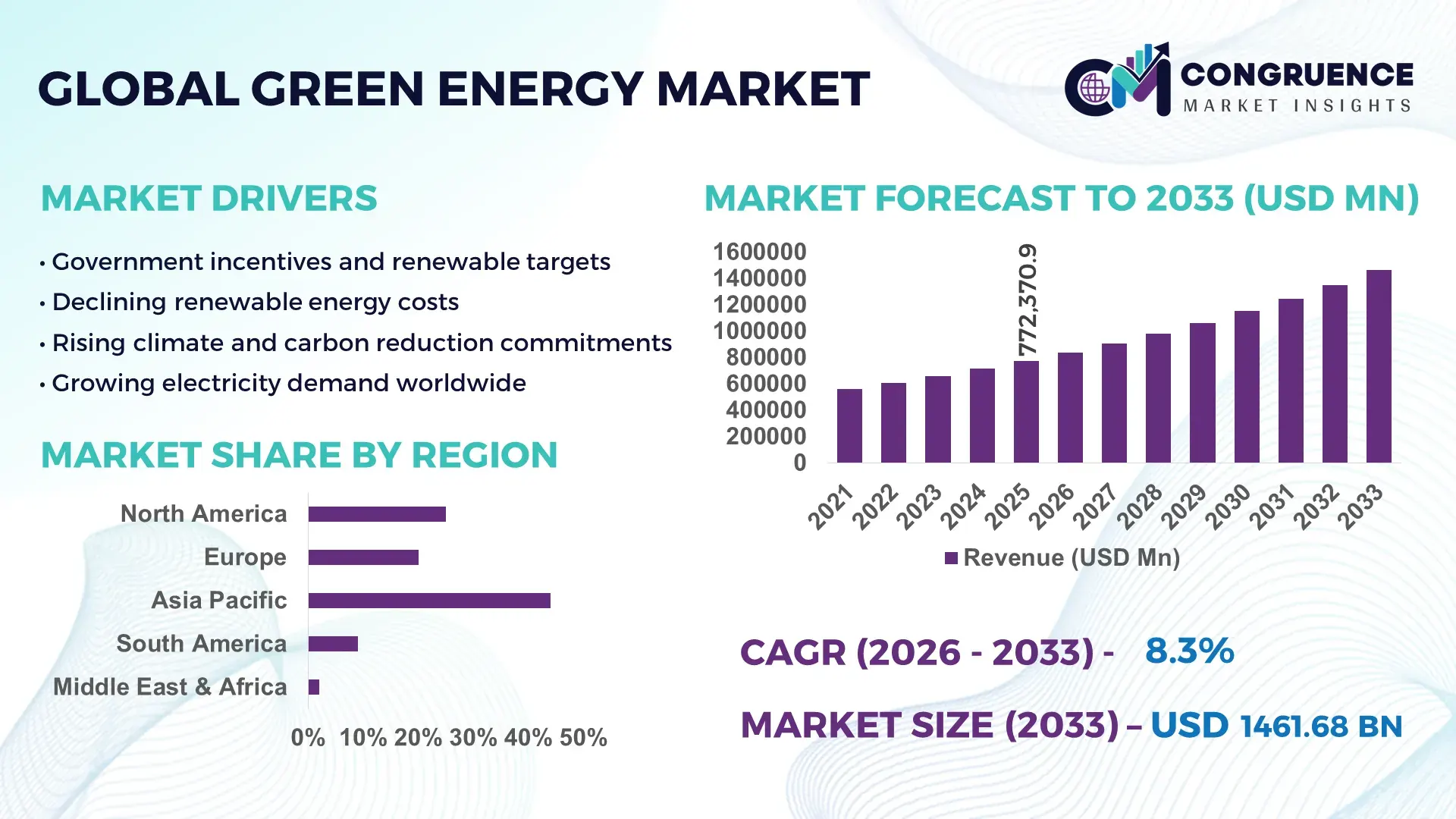

The Global Green Energy Market was valued at USD 772370.86 Million in 2025 and is anticipated to reach a value of USD 1461684.14 Million by 2033 expanding at a CAGR of 8.3% between 2026 and 2033. Growth is driven by accelerated renewable deployment, grid modernization, and large-scale decarbonization commitments across power, transport, and industrial sectors.

China represents the most influential country in the global green energy landscape, supported by large-scale production capacity and sustained capital deployment. As of 2024, China had over 1,200 GW of installed renewable power capacity, including more than 430 GW of solar and 440 GW of wind. Annual clean energy investment exceeded USD 540 billion, with applications spanning utility-scale power generation, electric mobility infrastructure, green hydrogen, and industrial electrification. Advanced manufacturing of solar modules, wind turbines, lithium-ion batteries, and ultra-high-voltage (UHV) transmission systems continues to strengthen technological depth and deployment efficiency nationwide.

Market Size & Growth: Valued at USD 772,370.86 million in 2025, projected to reach USD 1,461,684.14 million by 2033, expanding at a CAGR of 8.3%, supported by accelerating renewable capacity additions and electrification of end-use sectors.

Top Growth Drivers: Renewable power adoption growth at 14%, grid efficiency improvement of 11%, and energy storage deployment increase of 18%.

Short-Term Forecast: By 2028, average levelized cost of electricity (LCOE) from renewables is expected to decline by approximately 15% through scale and technology optimization.

Emerging Technologies: Green hydrogen electrolysis, long-duration energy storage, AI-enabled smart grids, and advanced offshore wind platforms.

Regional Leaders: Asia-Pacific projected at USD 620 billion by 2033 with large-scale solar adoption; Europe at USD 420 billion driven by grid-integrated renewables; North America at USD 350 billion supported by utility-scale wind and storage.

Consumer/End-User Trends: Utilities, industrial manufacturers, and commercial facilities account for over 65% of renewable energy consumption, with rising corporate power purchase agreements.

Pilot or Case Example: In 2024, a large-scale hybrid solar-plus-storage project achieved a 22% grid stability improvement and 18% peak-load reduction.

Competitive Landscape: NextEra Energy holds approximately 7% share, followed by Enel, Ørsted, Iberdrola, Vestas, and Siemens Gamesa.

Regulatory & ESG Impact: Net-zero mandates, renewable portfolio standards, and carbon pricing mechanisms continue to accelerate adoption.

Investment & Funding Patterns: Over USD 1.7 trillion invested globally in recent years, with growth in green bonds, blended finance, and infrastructure funds.

Innovation & Future Outlook: Expansion of integrated energy systems, digital energy management platforms, and cross-sector electrification projects.

The green energy market spans power generation, transportation, industrial processing, and building electrification, with solar and wind contributing over 70% of installed renewable capacity globally. Technological innovations such as high-efficiency photovoltaic cells, floating wind turbines, and grid-scale battery systems are reshaping cost structures and reliability. Regulatory frameworks emphasizing emissions reduction, energy security, and sustainable finance continue to support expansion. Regionally, Asia-Pacific leads consumption growth, Europe focuses on grid integration and offshore assets, while North America advances hybrid renewable-storage models. Emerging trends include green hydrogen commercialization, decentralized energy systems, and deeper digital integration, positioning the market for long-term, resilient growth.

The Green Energy Market holds strategic relevance as it underpins national energy security, industrial decarbonization, and long-term economic resilience. Governments and enterprises increasingly align energy strategies with measurable performance outcomes such as capacity expansion, emissions reduction, and operational efficiency. For instance, advanced bifacial solar photovoltaic technology delivers nearly 12% efficiency improvement compared to conventional monofacial panels, directly enhancing land-use productivity and return on infrastructure investment. From a regional perspective, Asia-Pacific dominates in volume of installed renewable capacity, while Europe leads in adoption with over 68% of large enterprises sourcing electricity from renewables for core operations.

Strategically, organizations are integrating digitalization and automation into green energy assets. By 2028, AI-enabled energy management systems are expected to improve grid balancing efficiency by approximately 20% through predictive demand-response optimization. ESG considerations further reinforce adoption, with firms committing to Scope 2 emission reductions such as 40% lower indirect emissions by 2030 through renewable power procurement and on-site generation. In a measurable micro-scenario, in 2024, Denmark achieved nearly 15% improvement in offshore wind capacity utilization through AI-based turbine performance analytics and predictive maintenance programs.

Future pathways emphasize cross-sector integration, including electrification of transport, green hydrogen for heavy industry, and decentralized energy systems for resilience. As regulatory frameworks tighten and capital increasingly favors sustainable assets, the Green Energy Market is positioned as a foundational pillar supporting compliance, operational stability, and sustainable long-term growth across global economies.

Global decarbonization commitments are a primary driver of growth in the Green Energy Market. More than 140 countries have announced net-zero or carbon-neutral targets, translating into mandatory renewable energy adoption across power generation and industrial sectors. Utilities are increasing renewable penetration to comply with renewable portfolio standards that often require 30–50% clean energy sourcing within the next decade. Corporate demand is also rising, with long-term power purchase agreements exceeding 35 GW annually worldwide. Electrification of transport further amplifies demand, as electric vehicle charging infrastructure increasingly relies on renewable power. These combined policy and corporate actions are directly increasing installed capacity, grid interconnections, and storage deployment, reinforcing sustained demand momentum for green energy technologies.

Despite strong demand, grid infrastructure constraints present a significant restraint for the Green Energy Market. In many regions, transmission and distribution networks were designed for centralized fossil-based generation and struggle to integrate variable renewable sources. Grid congestion has led to renewable curtailment rates exceeding 5–7% in some high-penetration markets, reducing asset utilization. Interconnection delays for new solar and wind projects can extend beyond three years, slowing deployment timelines. Additionally, limited cross-border transmission capacity restricts optimal power balancing between regions. These infrastructure challenges increase system costs and complexity, requiring substantial capital investment and regulatory coordination before full renewable potential can be realized.

Energy storage presents a major opportunity for the Green Energy Market by addressing intermittency and enhancing grid reliability. Global installed battery storage capacity has surpassed 85 GW, yet this represents only a fraction of what is required for high renewable penetration systems. Large-scale lithium-ion and emerging long-duration storage solutions enable peak shifting, frequency regulation, and backup power for critical infrastructure. Industrial users are adopting behind-the-meter storage to reduce demand charges and improve energy resilience. Additionally, storage integration allows higher utilization of renewable assets, reducing curtailment and improving overall system efficiency. As costs decline and performance improves, storage-backed renewable projects are opening new commercial and grid-support applications.

The Green Energy Market faces challenges from supply chain concentration and rising material costs. Key inputs such as polysilicon, rare earth elements, lithium, and cobalt are geographically concentrated, exposing manufacturers to price volatility and geopolitical risk. In recent years, battery-grade lithium prices experienced multi-fold fluctuations, directly impacting project economics. Wind turbine and solar manufacturers also face higher steel, copper, and logistics costs, which can delay projects or compress margins. Additionally, compliance with environmental and labor regulations across supply chains increases operational complexity. Addressing these challenges requires diversification of sourcing, recycling initiatives, and technological innovation to reduce material intensity while maintaining performance.

Rapid Integration of Modular and Prefabricated Energy Infrastructure: Modular and prefabricated construction is increasingly reshaping deployment strategies across the Green Energy market. Around 55% of newly commissioned renewable projects report measurable cost advantages through modular approaches, including 20–25% reductions in on-site labor requirements. Pre-engineered solar mounting systems, wind turbine foundations, and containerized battery storage units enable faster installation cycles, cutting project timelines by up to 30%. Adoption is particularly strong in Europe and North America, where over 60% of utility-scale projects now incorporate some level of off-site fabrication to improve consistency, safety, and execution speed.

Expansion of Hybrid Renewable Energy Systems: Hybrid projects combining solar, wind, and energy storage are gaining traction as grid operators prioritize reliability and flexibility. Nearly 45% of new utility-scale renewable installations now include integrated storage or multi-source generation. These systems have demonstrated up to 18% higher capacity utilization compared to single-source assets and reduced renewable curtailment by approximately 12%. Hybrid configurations are increasingly deployed in regions with high renewable penetration, enabling smoother load balancing and more predictable power delivery for industrial and commercial users.

Acceleration of Digitalization and AI-Driven Asset Management: Digital monitoring platforms and AI-based analytics are becoming standard across green energy assets. More than 50% of large renewable operators have implemented predictive maintenance systems, achieving equipment downtime reductions of nearly 15%. AI-driven forecasting tools improve wind and solar output prediction accuracy by 20–25%, enhancing grid integration and trading efficiency. These technologies also support automated performance benchmarking across asset portfolios, enabling operators to optimize operational expenditure and extend asset lifecycles.

Rising Corporate and Industrial Renewable Power Procurement: Corporate demand for green energy continues to intensify, with large enterprises accounting for over 35% of newly contracted renewable capacity. Long-term power purchase agreements now cover contract durations exceeding 12 years on average, providing developers with greater revenue certainty and financing stability. Industrial sectors such as manufacturing, data centers, and logistics report renewable electricity usage surpassing 40% of total power consumption, driven by sustainability commitments and energy cost optimization objectives.

The Green Energy market demonstrates a well-defined segmentation structure across types, applications, and end-user groups, reflecting varying adoption maturity, technology readiness, and investment priorities. By type, solar, wind, hydro, bioenergy, and emerging hydrogen-based systems form the core technology mix, each contributing differently based on regional resource availability and infrastructure readiness. Application-wise, power generation dominates, while transportation, industrial processes, and residential and commercial energy use are expanding steadily as electrification accelerates. From an end-user perspective, utilities remain central, but industrial enterprises, commercial facilities, and institutional users are increasingly shaping demand patterns. Segmentation insights reveal that decision-makers are prioritizing scalable, flexible, and digitally integrated solutions, with adoption influenced by regulatory mandates, cost competitiveness, and sustainability targets. This structured segmentation highlights where deployment is most concentrated today and where future growth momentum is building across the Green Energy ecosystem.

Solar energy remains the leading type within the Green Energy market, accounting for approximately 38% of total installed renewable capacity globally. Its leadership is supported by widespread availability, declining module costs, and scalability across utility-scale and distributed systems. Wind energy follows with close to 32% share, split between onshore installations and a rapidly expanding offshore segment. However, offshore wind represents the fastest-growing type, supported by stronger capacity factors and large-scale coastal projects, and is expanding at an estimated CAGR of around 11%. Hydropower, bioenergy, geothermal, and emerging green hydrogen technologies collectively contribute nearly 30% of the market, serving niche roles in grid stability, industrial heat, and long-duration energy supply. These remaining segments are particularly relevant in regions with established infrastructure or specific resource advantages.

Power generation is the dominant application segment, representing nearly 65% of green energy deployment, driven by large-scale renewable plants feeding national grids. Solar and wind-based electricity generation form the backbone of this segment due to their rapid deployment timelines and scalability. Transportation applications, including electric mobility powered by renewables and green hydrogen for heavy transport, currently account for about 18% of adoption but are the fastest-growing application area. This segment is expanding at an estimated CAGR of approximately 13%, supported by electrification policies and fuel-switching mandates. Industrial applications such as green hydrogen for steelmaking and renewable-powered process heat contribute around 10%, while residential and commercial uses collectively represent the remaining 7%.

Utilities are the leading end-user segment in the Green Energy market, accounting for roughly 52% of total adoption, as they remain responsible for large-scale generation, grid integration, and power distribution. Industrial end-users follow with about 26% share, driven by decarbonization of manufacturing, mining, and processing operations. However, commercial and corporate users represent the fastest-growing end-user group, expanding at an estimated CAGR of nearly 12%, supported by sustainability commitments and long-term renewable power procurement strategies. These users increasingly rely on on-site solar, corporate power purchase agreements, and energy storage solutions. Residential users and public institutions collectively contribute around 22%, supported by rooftop solar adoption, community energy projects, and public infrastructure electrification.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2026 and 2033.

Asia-Pacific leads due to high renewable capacity additions exceeding 1,400 GW, large-scale manufacturing ecosystems, and strong government-backed deployment programs. Europe follows with over 620 GW of installed renewable capacity and aggressive energy transition targets. North America represents approximately 22% market share, supported by utility-scale solar, wind, and storage integration. South America holds close to 6% share, driven by hydropower and expanding solar installations, while the Middle East & Africa collectively account for around 7%, supported by mega solar projects and diversification away from fossil fuels. Regional growth variations reflect differences in policy frameworks, grid readiness, investment capacity, and end-user adoption intensity across industrial, commercial, and residential sectors.

How is policy-driven electrification reshaping energy deployment patterns?

The region accounts for nearly 22% of the global Green Energy market, with installed renewable capacity exceeding 480 GW. Demand is driven primarily by utilities, data centers, manufacturing, healthcare, and financial services. Regulatory support includes long-term tax credits, clean electricity standards, and incentives for domestic manufacturing of solar panels, wind components, and batteries. Digital transformation is evident through widespread adoption of AI-based grid management and predictive maintenance, improving asset utilization by over 15%. A major local player has expanded utility-scale solar-plus-storage projects, adding more than 8 GW of clean capacity within three years. Consumer behavior shows higher enterprise adoption in healthcare and finance, where renewable power sourcing exceeds 50% of electricity demand to meet ESG and compliance goals.

Why are compliance mandates accelerating advanced renewable adoption?

Europe holds approximately 19% of the global Green Energy market, with Germany, the UK, France, Spain, and Italy as key contributors. The region is supported by binding climate regulations, carbon pricing mechanisms, and renewable energy directives targeting over 65% renewable electricity by the next decade. Offshore wind capacity alone exceeds 35 GW, with rapid deployment of floating wind and green hydrogen pilots. Utilities and industrial users increasingly integrate energy storage and digital energy management platforms. A leading European energy group has deployed cross-border offshore wind hubs supplying power to multiple countries. Consumer behavior reflects strong regulatory pressure, driving demand for transparent, auditable, and traceable green energy procurement across enterprises.

How manufacturing scale and infrastructure investment are shaping deployment?

Asia-Pacific is the largest market by volume, accounting for around 46% of global green energy deployment. China, India, and Japan are the top consuming countries, collectively representing over 70% of regional capacity additions. The region hosts more than 80% of global solar module manufacturing and over 60% of wind turbine production. Infrastructure trends include ultra-high-voltage transmission networks, large pumped hydro storage, and expanding battery gigafactories. A major regional player has commissioned over 15 GW of solar and wind projects annually, strengthening grid-scale supply. Consumer behavior is driven by rapid urbanization, industrial electrification, and large-scale digital infrastructure growth supporting energy demand.

How resource abundance is enabling clean energy diversification?

South America accounts for nearly 6% of the global Green Energy market, led by Brazil, Argentina, and Chile. Hydropower remains dominant, contributing over 50% of renewable generation, while solar and wind installations have surpassed 70 GW combined. Governments offer tax exemptions, long-term power contracts, and grid access incentives to attract private investment. Regional energy trends include hybrid hydro-solar projects and expansion of transmission corridors. A leading Brazilian utility has integrated wind and solar assets to stabilize seasonal hydropower variability. Consumer behavior shows demand closely linked to industrial processing, agriculture, and localized energy needs.

Why diversification strategies are accelerating clean power investments?

The Middle East & Africa region holds about 7% of the global Green Energy market, with strong momentum in the UAE, Saudi Arabia, Egypt, and South Africa. Large-scale solar projects exceeding 2 GW per site are becoming common, supported by competitive auctions and long-term power agreements. Energy demand is driven by construction, desalination, mining, and oil & gas sector decarbonization. Technological modernization includes smart grids, digital substations, and utility-scale battery storage. A regional developer has delivered one of the world’s largest single-site solar plants, supplying clean electricity to over 1 million households. Consumer behavior emphasizes cost stability and energy security over legacy fuel dependence.

China – 32% market share: Dominance driven by massive renewable production capacity, advanced manufacturing ecosystems, and large-scale industrial and grid applications of green energy.

United States – 18% market share: Strong position supported by utility-scale deployment, corporate renewable procurement, and sustained regulatory and investment support for clean energy infrastructure.

The Green Energy market features a moderately consolidated yet highly competitive landscape, characterized by the presence of over 150 active global and regional players operating across solar, wind, hydro, bioenergy, and energy storage segments. The top five companies collectively account for approximately 32% of total installed renewable capacity worldwide, indicating that while large incumbents exert strong influence, significant opportunities remain for mid-sized and specialized players. Market leaders focus on vertical integration, spanning project development, equipment manufacturing, grid services, and digital energy management. Strategic initiatives such as cross-border joint ventures, long-term power purchase agreements, and portfolio diversification into storage and green hydrogen are increasingly common. Innovation trends shaping competition include AI-enabled asset optimization, floating offshore wind platforms, high-efficiency photovoltaic technologies exceeding 23% module efficiency, and large-scale battery systems supporting grid stability. Mergers and acquisitions activity remains selective, with transactions primarily aimed at geographic expansion and technology acquisition rather than consolidation alone. The competitive environment rewards scale, access to low-cost capital, regulatory alignment, and the ability to deliver integrated, resilient energy solutions to utilities, industrial users, and governments.

NextEra Energy

Enel

Iberdrola

Ørsted

Vestas Wind Systems

Siemens Gamesa Renewable Energy

Brookfield Renewable Partners

EDF Renewables

RWE Renewables

China Three Gorges Corporation

Adani Green Energy

Technological advancement remains a central force shaping the Green Energy Market, with continuous innovation improving efficiency, reliability, and system integration across renewable assets. In solar energy, next-generation photovoltaic technologies such as bifacial and heterojunction modules are achieving conversion efficiencies above 22%, enabling up to 15% higher energy yield per installation footprint. Large-format wafers and automated manufacturing lines are further reducing defect rates and improving output consistency. In wind energy, turbine capacities have increased significantly, with offshore units now exceeding 15 MW per turbine, delivering higher capacity factors of nearly 50% and reducing the number of units required per project.

Energy storage technologies are also advancing rapidly, supporting higher renewable penetration. Grid-scale lithium-ion battery systems now provide response times below one second and cycle efficiencies above 90%, while long-duration storage solutions such as flow batteries and compressed air systems enable multi-hour to multi-day energy shifting. Digital technologies are increasingly embedded across the value chain. AI-driven forecasting tools improve solar and wind output prediction accuracy by over 20%, while predictive maintenance platforms reduce unplanned downtime by approximately 15%.

Grid modernization technologies, including smart inverters, digital substations, and advanced energy management systems, enable real-time monitoring and bi-directional power flows essential for distributed energy resources. Green hydrogen technologies are emerging as a critical complement, with electrolyzer efficiencies approaching 70% and large-scale projects targeting industrial decarbonization. Collectively, these technologies are transforming green energy systems into more resilient, data-driven, and scalable infrastructures, supporting long-term operational performance and strategic energy transitions.

• In February 2024, Iberdrola completed the acquisition of the remaining minority stake in Avangrid, gaining full ownership of the U.S.-based renewable energy company. The transaction strengthened Iberdrola’s onshore wind, solar, and grid infrastructure portfolio across more than 24 U.S. states. Source: www.iberdrola.com

• In May 2024, Ørsted announced a strategic review and restructuring of its U.S. offshore wind portfolio, including asset write-downs and revised project timelines, as part of a broader capital discipline initiative focused on improving project execution and long-term returns. Source: www.orsted.com

• In August 2024, First Solar commissioned an additional manufacturing facility in Ohio, increasing its U.S. solar module production capacity to over 14 GW annually, supporting domestic supply chains and utility-scale solar deployment across North America. Source: www.firstsolar.com

• In January 2025, Vestas secured multiple large offshore and onshore wind turbine supply agreements across Europe and Asia, totaling more than 6 GW of capacity, reinforcing its order backlog and expanding deployment of high-capacity turbine platforms. Source: www.vestas.com

The Green Energy Market Report provides a comprehensive assessment of the global transition toward renewable and low-carbon energy systems, covering a broad range of technologies, applications, and regional markets. The scope includes detailed analysis of major energy types such as solar, wind (onshore and offshore), hydropower, bioenergy, geothermal, and emerging green hydrogen solutions. It evaluates deployment across utility-scale, distributed, and hybrid systems, with installed capacity metrics, technology penetration levels, and adoption patterns across industrial, commercial, residential, and public-sector end users.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing regional infrastructure readiness, policy frameworks, manufacturing ecosystems, and consumption trends. More than 30 national markets are assessed to capture variations in grid integration, electrification progress, and renewable deployment intensity. Application coverage extends beyond power generation to include transportation electrification, industrial decarbonization, heating, and energy storage integration.

The report further examines enabling technologies such as battery storage, smart grids, digital energy management platforms, and power electronics, highlighting their role in improving system efficiency and resilience. Emerging segments, including offshore wind, floating solar, long-duration storage, and hydrogen electrolysis, are also addressed. Overall, the report is designed to support strategic planning, investment assessment, and policy evaluation for stakeholders across the global Green Energy ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NextEra Energy, Enel, Iberdrola, Ørsted, Vestas Wind Systems, Siemens Gamesa Renewable Energy, Brookfield Renewable Partners, EDF Renewables, RWE Renewables, China Three Gorges Corporation, Adani Green Energy |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |