Reports

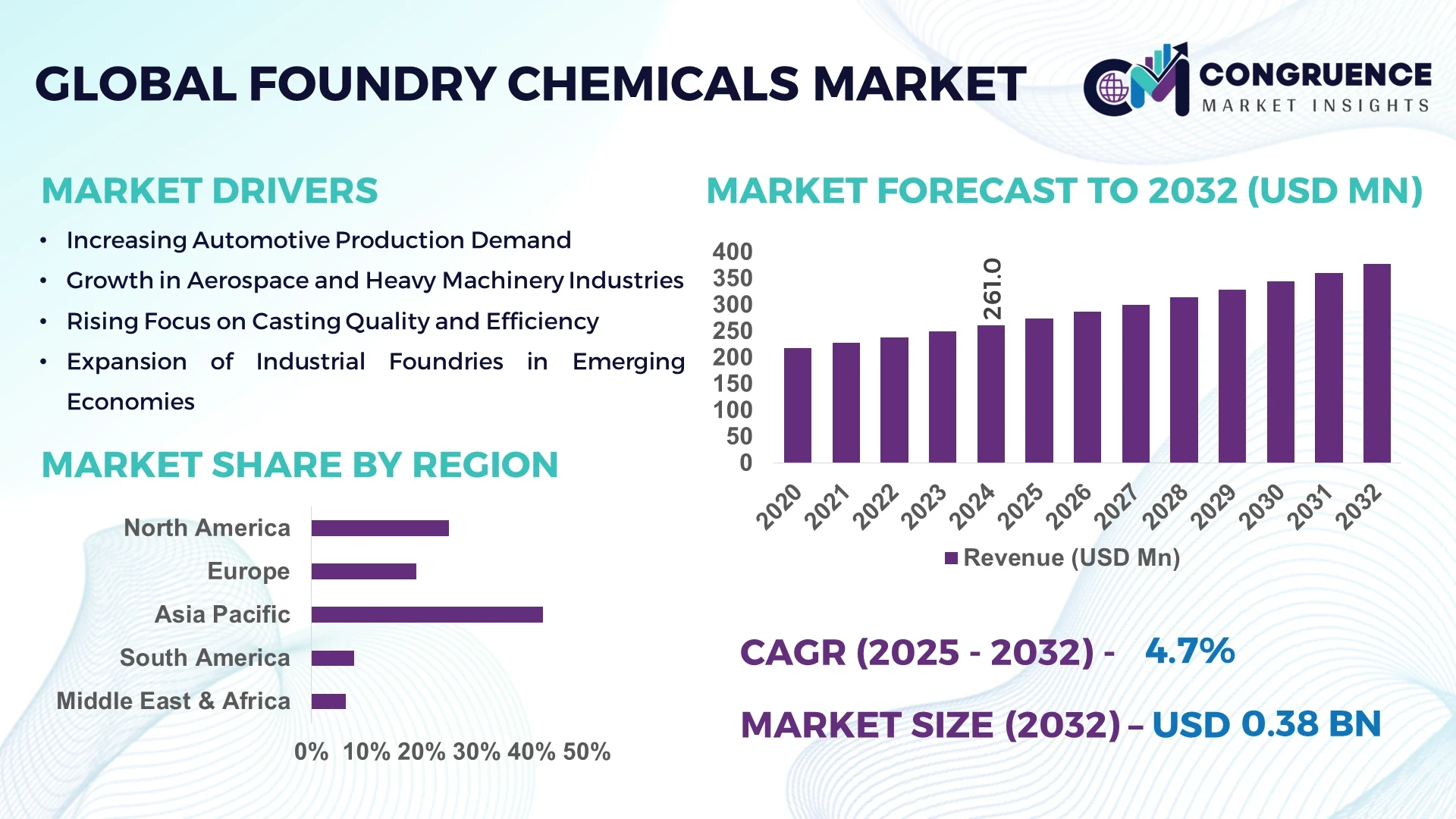

The Global Foundry Chemicals Market was valued at USD 261.0 Million in 2024 and is anticipated to reach a value of USD 376.9 Million by 2032, expanding at a CAGR of 4.7% between 2025 and 2032.

China maintains a pivotal role in the Foundry Chemicals Market, characterized by substantial production capacities and significant investments in the sector. The nation's extensive industrial base, particularly in automotive and heavy machinery manufacturing, drives the demand for advanced foundry chemicals. Technological advancements in casting processes and a focus on enhancing the quality of cast components underscore China's commitment to innovation in the foundry chemicals industry.

The Foundry Chemicals Market encompasses a diverse range of products, including binders, coatings, fluxes, and hot topping compounds, which are integral to the metal casting process. These chemicals are primarily utilized in the automotive, construction, and heavy machinery sectors, where high-precision cast components are essential. Recent technological innovations have led to the development of eco-friendly and high-performance chemicals that enhance the quality and efficiency of casting processes. Regulatory frameworks in various regions are increasingly emphasizing sustainability, prompting manufacturers to adopt greener alternatives. Economic factors, such as the growth of industrial activities and infrastructure development, are driving the demand for foundry chemicals. Regional consumption patterns indicate a significant uptake in Asia-Pacific, owing to rapid industrialization and the expansion of manufacturing capabilities. Emerging trends include the integration of digital technologies in foundry operations and a shift towards more sustainable and cost-effective chemical solutions. The future outlook for the market remains positive, with continued advancements in technology and a growing emphasis on environmental considerations shaping the industry's trajectory.

Artificial Intelligence (AI) is revolutionizing the Foundry Chemicals Market by enhancing process optimization, predictive maintenance, and quality control. AI algorithms analyze vast datasets from casting processes to predict potential defects, enabling proactive adjustments and reducing waste. Machine learning models are employed to optimize chemical formulations, leading to improved performance and cost-efficiency. Furthermore, AI-driven automation in chemical mixing and application processes accelerates production timelines and ensures consistency in product quality. The integration of AI technologies facilitates real-time monitoring and control, allowing for dynamic adjustments to chemical processes based on operational data. As the industry continues to embrace digital transformation, AI is poised to play a crucial role in driving innovation and efficiency in the foundry chemicals sector.

"In 2024, a leading foundry chemicals manufacturer implemented an AI-based predictive maintenance system across its production facilities. This initiative led to a 15% reduction in equipment downtime and a 10% increase in overall production efficiency."

The Foundry Chemicals Market is influenced by various dynamics, including technological advancements, regulatory changes, and shifts in industrial demand. Innovations in chemical formulations and casting technologies are driving the development of more efficient and sustainable solutions. Regulatory pressures are prompting manufacturers to adopt eco-friendly chemicals and processes, aligning with global sustainability goals. Economic factors, such as fluctuations in raw material costs and energy prices, impact production costs and pricing strategies. Additionally, the evolving needs of end-user industries, such as automotive and construction, necessitate continuous adaptation and innovation within the foundry chemicals sector.

Advancements in casting technologies, such as 3D printing and automated molding, are significantly influencing the Foundry Chemicals Market. These technologies require specialized chemicals that can withstand the unique conditions of modern casting methods. The development of high-performance binders and coatings tailored for these advanced processes is driving market growth. Manufacturers are investing in research and development to create chemicals that enhance the efficiency and quality of cast components produced through these innovative techniques.

The Foundry Chemicals Market faces challenges related to environmental regulations and compliance standards. Stricter environmental laws are necessitating the development and adoption of greener chemicals, which can be more expensive and complex to produce. Compliance with these regulations requires significant investment in research, development, and testing, potentially increasing operational costs for manufacturers. Additionally, the transition to eco-friendly chemicals may involve modifications to existing production processes, further adding to the financial burden.

The rise in electric vehicle (EV) production presents a significant opportunity for the Foundry Chemicals Market. EVs require lightweight and high-strength components, driving the demand for advanced casting materials and chemicals. Foundries are increasingly producing aluminum and magnesium castings to meet the specific requirements of EV manufacturers. This shift is prompting the development of specialized foundry chemicals that enhance the performance and durability of components used in electric vehicles.

Volatility in the prices of raw materials, such as silica sand and resins, poses a challenge to the Foundry Chemicals Market. Fluctuating costs can impact the pricing strategies of manufacturers and affect the overall profitability of the industry. Additionally, supply chain disruptions can lead to shortages of essential materials, hindering production capabilities. Manufacturers must adopt strategic sourcing and inventory management practices to mitigate the impact of raw material price fluctuations on their operations.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Foundry Chemicals Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Shift Towards Sustainable and Eco-friendly Chemicals: There is a growing emphasis on sustainability within the Foundry Chemicals Market. Manufacturers are developing and adopting eco-friendly chemicals that minimize environmental impact. This shift is driven by regulatory pressures and consumer demand for greener products, leading to innovations in biodegradable binders and low-emission coatings.

Integration of Digital Technologies in Foundry Operations: The integration of digital technologies, such as IoT and AI, is transforming foundry operations. Real-time monitoring and data analytics are enabling predictive maintenance and process optimization. This digital transformation enhances efficiency, reduces downtime, and improves the overall quality of cast components.

Focus on Lightweight Materials for Automotive Applications: The automotive industry is increasingly focusing on lightweight materials to improve fuel efficiency and reduce emissions. This trend is driving the demand for advanced foundry chemicals that facilitate the production of lightweight aluminum and magnesium castings. Manufacturers are investing in research to develop chemicals that enhance the performance and durability of these materials.

The Foundry Chemicals Market is segmented into types, applications, and end-users, reflecting the diverse needs of the global casting and molding industry. By type, the market includes binders, coatings, additives, and mold release agents, each fulfilling specific operational roles in casting processes. Application-wise, chemicals are used across automotive, aerospace, heavy machinery, construction, and general engineering sectors, with tailored formulations meeting the unique performance and regulatory requirements of each industry. End-user segmentation highlights industrial foundries, municipal and commercial casting facilities, and specialized component manufacturers, illustrating the widespread adoption of chemical solutions for efficiency, quality, and compliance. Understanding these segments enables manufacturers and investors to target resources strategically, optimize product offerings, and prioritize high-demand regions.

Binders are the leading product type in the Foundry Chemicals Market due to their critical role in holding sand particles together during molding and core-making processes. Phenolic, furan, and sodium silicate binders are extensively used for their thermal stability and binding strength, ensuring high-quality castings. Membrane and resin binders are seeing significant growth as sustainable and low-emission alternatives gain traction in environmentally conscious foundries. Coatings represent another essential category, applied for mold protection, improved surface finish, and defect reduction in final cast components. Additives and mold release agents also contribute by enhancing chemical performance, reducing casting cycle times, and improving operational efficiency. Emerging specialty chemicals, such as bio-based binders, are carving out niche applications, particularly in high-tech automotive and aerospace foundries seeking sustainable solutions. The interplay of performance, sustainability, and regulatory compliance continues to shape type-based adoption patterns.

The automotive sector is the leading application area for foundry chemicals due to the high volume of engine blocks, transmission housings, and structural components requiring precision casting. Foundries serving the automotive industry rely on high-performance binders and coatings to ensure dimensional accuracy and reduce defects. Aerospace is the fastest-growing application, driven by the rising demand for lightweight, high-strength components that require specialized chemical formulations to withstand extreme operating conditions. Heavy machinery and construction equipment applications also maintain steady demand, with foundries using durable binders and additives to produce large, high-load cast components. Other applications, including general engineering and electrical equipment, leverage foundry chemicals for mold release efficiency, heat resistance, and surface finish improvements. Increasing focus on material optimization, emission reduction, and process efficiency influences the adoption patterns across all applications.

Industrial foundries represent the leading end-user segment in the Foundry Chemicals Market, accounting for the bulk of chemical consumption due to large-scale production of automotive, aerospace, and machinery components. These facilities prioritize high-performance binders, advanced coatings, and optimized additives to maintain product quality, minimize defects, and streamline operations. The fastest-growing end-user segment is specialized component manufacturers, including aerospace and high-tech automotive suppliers, driven by increasing demand for lightweight, precision-engineered parts. Municipal and commercial foundries also contribute, often adopting standardized chemical solutions to meet regulatory compliance and sustainability requirements. Other end-users, such as small-scale engineering foundries, utilize chemicals for niche applications like custom castings and prototyping. End-user adoption is influenced by production volume, quality standards, automation levels, and regulatory obligations, creating differentiated demand across the market landscape.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.7% between 2025 and 2032.

The region’s dominance is driven by rapidly growing automotive, construction, and heavy machinery industries, which rely heavily on advanced foundry chemicals for precision casting. Rising industrialization in China, India, and Japan has led to increased demand for high-performance binders, coatings, and additives. Additionally, government initiatives promoting industrial growth and investments in modern manufacturing facilities are supporting the expansion of the Foundry Chemicals Market in Asia-Pacific.

North America holds a market share of approximately 25% in the Foundry Chemicals Market. The region is driven by strong demand from automotive, aerospace, and heavy machinery industries. Regulatory frameworks in the United States and Canada have encouraged the adoption of environmentally friendly binders and low-emission coatings. Technological advancements, including AI-assisted chemical dosing systems and digital twin simulations, are improving operational efficiency and reducing defect rates. Manufacturers in North America are also investing in R&D to develop sustainable chemical solutions and optimize production processes, ensuring high-quality castings and compliance with environmental standards.

Europe accounts for approximately 20% of the global Foundry Chemicals Market, with Germany, the UK, and France as leading contributors. The region emphasizes sustainable and low-emission binders, aligning with strict EU environmental regulations and the REACH compliance framework. European foundries are increasingly adopting digital process monitoring and AI-driven chemical optimization tools. High-performance coatings and specialized additives are widely used in automotive, aerospace, and industrial machinery sectors. Regulatory initiatives encouraging green manufacturing practices and technological upgrades are fostering innovation, driving demand for advanced and eco-friendly foundry chemicals across the region.

Asia-Pacific represents the largest market volume globally, contributing 42% to the Foundry Chemicals Market. China, India, and Japan are the top-consuming countries, driven by large-scale automotive, aerospace, and construction equipment production. Rapid industrialization, infrastructure expansion, and investments in modern foundry facilities are increasing demand for binders, coatings, and additives. Regional technology trends include adoption of digital twin simulations, AI-assisted process optimization, and energy-efficient chemical formulations. Innovation hubs in China and Japan are developing next-generation eco-friendly binders and high-performance coatings to meet quality and regulatory requirements.

South America holds a market share of 7%, with Brazil and Argentina as key contributors. The region is witnessing growing demand from automotive and heavy machinery foundries. Investments in industrial infrastructure, modernization of casting facilities, and government incentives for local manufacturing are supporting market growth. Energy sector developments, particularly in Brazil, are also increasing the adoption of specialized foundry chemicals. Manufacturers are incorporating sustainable binders and coatings to meet environmental standards and improve operational efficiency, strengthening the market presence in South America.

The Middle East & Africa region represents 6% of the Foundry Chemicals Market. Key growth countries include the UAE and South Africa, where oil & gas, construction, and automotive sectors are driving demand. Technological modernization, such as automated chemical dosing and digital monitoring systems, is enhancing production efficiency. Local regulations and trade partnerships are encouraging adoption of eco-friendly binders and coatings. Investments in industrial facilities and infrastructure projects are further fueling the demand for high-performance foundry chemicals in the region.

China – 28% Market Share

High production capacity, robust industrial base, and rapid adoption of advanced chemical solutions in automotive and heavy machinery sectors.

United States – 25% Market Share

Strong end-user demand from aerospace and automotive industries, supported by advanced technological integration and regulatory compliance initiatives.

The competitive environment in the Foundry Chemicals Market is characterized by a diverse mix of global and regional players, with over 50 active companies providing specialized chemical solutions for industrial casting processes. Key competitors are positioned across multiple product segments, including binders, coatings, additives, and mold release agents, focusing on technological innovation and operational efficiency. Strategic initiatives such as partnerships, joint ventures, and new product launches are shaping market dynamics. Several companies have invested in R&D centers to develop sustainable, low-emission binders and high-performance coatings, responding to regulatory pressures and environmental concerns. Innovation trends, including AI-assisted chemical dosing, automated process monitoring, and bio-based chemical formulations, are increasingly influencing competition. Companies are leveraging digitalization and smart manufacturing technologies to enhance production quality and reduce waste, creating differentiation in a highly fragmented market. The overall landscape emphasizes sustainability, operational excellence, and advanced chemical solutions as critical competitive levers for maintaining and expanding market presence.

BASF SE

Arkema S.A.

Huntsman Corporation

Clariant AG

Trelleborg AB

Evonik Industries AG

Nouryon N.V.

Kao Chemicals

Shree Pushkar Chemicals

Chem-Trend L.P.

Current and emerging technologies are significantly shaping the Foundry Chemicals Market. AI-driven process optimization allows for precise control over binder and additive dosing, reducing waste and improving the consistency of cast components. Digital twin simulations enable foundries to test chemical formulations virtually, minimizing trial-and-error and accelerating production timelines. Advanced coatings incorporating nanomaterials are improving surface finish, mold protection, and thermal resistance. Sustainable technologies, including bio-based binders and low-emission additives, are being widely adopted to meet environmental regulations and reduce the carbon footprint of foundries. Automation technologies, such as robotic mold handling and chemical dispensing systems, increase operational efficiency while reducing human error. Innovations in sensor-based monitoring enable real-time assessment of chemical properties, temperature, and moisture, optimizing casting outcomes. Emerging trends also include smart foundry solutions integrating IoT platforms for predictive maintenance and process intelligence, positioning the market for continued technological advancement and industrial modernization.

In March 2023, BASF launched a new range of eco-friendly furan binders designed for automotive and heavy machinery applications, reducing formaldehyde emissions by 35% while maintaining thermal stability in large-scale castings.

In July 2023, Evonik Industries introduced a high-performance mold coating system that enhances surface finish and reduces casting defects by 28% in aerospace component production.

In January 2024, Clariant developed a bio-based resin for foundry applications, utilizing 42% renewable raw materials, improving environmental compliance, and reducing VOC emissions during casting operations.

In October 2024, Huntsman Corporation implemented AI-assisted chemical dosing technology in its European plants, increasing binder efficiency by 18% and minimizing waste in complex metal casting processes.

The Foundry Chemicals Market Report encompasses a detailed assessment of global chemical solutions used in industrial casting, including binders, coatings, additives, mold release agents, and emerging bio-based products. The report covers segmentation by type, application, and end-user, highlighting trends in automotive, aerospace, heavy machinery, construction, and general engineering industries. Regional coverage includes Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, providing insights into industrial hubs, production facilities, and technological adoption patterns. The report evaluates market dynamics, including drivers, restraints, opportunities, challenges, and innovation trends, offering a comprehensive perspective for decision-makers. Additionally, it assesses the competitive landscape, profiling key players and strategic initiatives that shape the market. Emerging technologies such as AI-assisted dosing, digital twin simulations, and sustainable chemical formulations are explored, alongside operational and regulatory considerations. This scope provides a full understanding of the market’s breadth, growth potential, and opportunities for investment and strategic planning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 261.0 Million |

| Market Revenue (2032) | USD 376.9 Million |

| CAGR (2025–2032) | 4.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | BASF SE, Arkema S.A., Huntsman Corporation, Clariant AG, Trelleborg AB, Evonik Industries AG, Nouryon N.V., Kao Chemicals, Shree Pushkar Chemicals, Chem-Trend L.P. |

| Customization & Pricing | Available on Request (10% Customization is Free) |