Reports

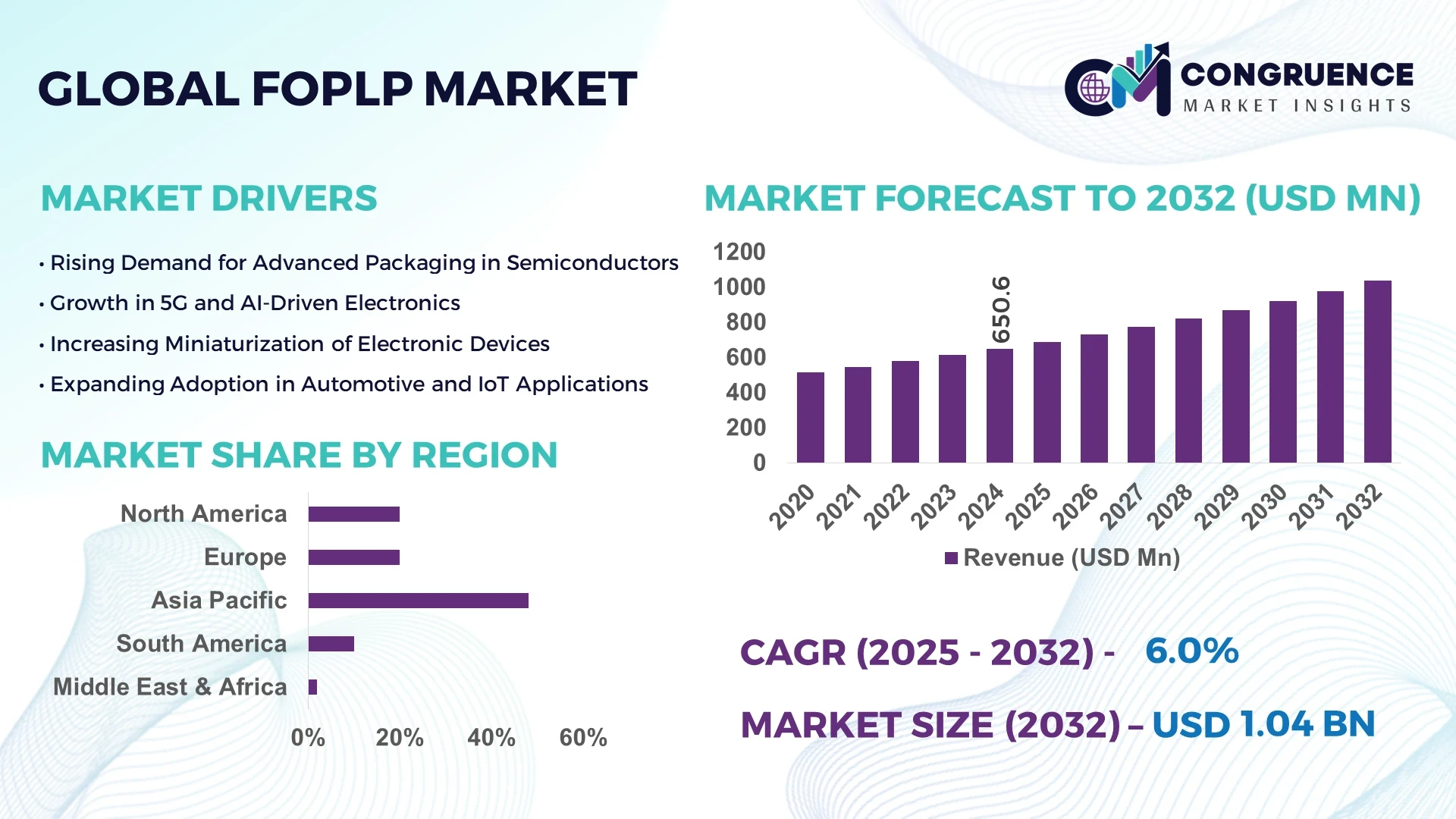

The Global FOPLP Market was valued at USD 650.56 Million in 2024 and is anticipated to reach a value of USD 1,036.9 Million by 2032, expanding at a CAGR of 6% between 2025 and 2032. This growth is driven by the increasing demand for miniaturized and high-performance electronic devices.

Taiwan's semiconductor industry is at the forefront of Fan-Out Panel-Level Packaging (FOPLP) advancements, with companies like TSMC, ASE, and Powertech Technology Inc. leading the charge. These firms are investing heavily in FOPLP technologies, including the use of glass substrates to enhance production capacity and reduce costs. Additionally, Taiwan's PCB industry is projected to grow by 5.8% in 2025, driven by applications such as AI servers and high-efficiency computing. The nation's strategic focus on advanced packaging solutions positions it as a key player in the global FOPLP market.

Market Size & Growth: Valued at USD 650.56 Million in 2024, projected to reach USD 1,036.9 Million by 2032, with a CAGR of 6%. Growth is driven by rising demand for compact, high-performance electronic devices.

Top Growth Drivers: Miniaturization of devices (40%), adoption of 5G technologies (35%), and high-performance computing requirements (25%).

Short-Term Forecast: By 2028, packaging efficiency is expected to improve by 15%, reducing production time and enhancing thermal management.

Emerging Technologies: Adoption of chip-on-wafer-on-substrate (CoWoS), advanced InFO-WLP, and glass substrate-based packaging solutions.

Regional Leaders: Asia-Pacific projected at USD 4 billion by 2032, North America at USD 2 billion, Europe at USD 1.5 billion; APAC leads in volume production, North America in R&D, Europe in automotive applications.

Consumer/End-User Trends: Increasing use in smartphones, wearables, AI servers, and automotive electronics with emphasis on device miniaturization and thermal performance.

Pilot or Case Example: In 2024, a major semiconductor company implemented InFO-WLP technology, achieving a 20% package size reduction and 30% thermal performance improvement.

Competitive Landscape: Market leader TSMC with approximately 35% share, followed by ASE, Powertech Technology, JCET, and SPIL.

Regulatory & ESG Impact: Stringent electronic waste regulations, energy efficiency mandates, and ESG initiatives promoting sustainable packaging adoption.

Investment & Funding Patterns: Recent investments totaling USD 450 million in R&D and pilot projects, with growing venture funding for innovative packaging technologies.

Innovation & Future Outlook: Focus on next-generation integration, heterogeneous packaging, and advanced substrate materials shaping future FOPLP solutions.

The FOPLP market is witnessing robust adoption across consumer electronics, automotive, and high-performance computing sectors. Recent innovations in glass-based substrates, chip stacking, and InFO-WLP techniques are enhancing performance, reducing device footprint, and improving thermal efficiency. Regulatory frameworks and environmental initiatives are driving sustainable adoption, while regional consumption is concentrated in Asia-Pacific, North America, and Europe. Emerging trends include heterogeneous integration and AI-driven package optimization, positioning the market for continued technological growth and strategic investments.

Fan-Out Panel-Level Packaging (FOPLP) is a strategic technology that enhances semiconductor performance, offering measurable improvements over traditional packaging. FOPLP delivers a 30% improvement in thermal performance compared to conventional wire-bonded packages, improving device reliability and operational efficiency. Regionally, Asia-Pacific dominates in volume production, while North America leads in adoption, with approximately 65% of enterprises implementing FOPLP solutions. By 2027, integration of AI-driven design is expected to reduce development cycles by 20%, accelerating time-to-market for new semiconductor devices. Firms are committing to ESG metrics, such as a 15% reduction in packaging material waste and a 10% increase in recycling by 2030, reflecting sustainable practices. In 2025, a leading semiconductor company achieved a 25% improvement in yield and a 20% reduction in production costs through AI-optimized FOPLP design. The market is projected to expand into automotive, AI servers, and wearable electronics, driven by increasing demand for miniaturized high-performance devices. Looking ahead, the FOPLP market is positioned as a pillar of resilience, compliance, and sustainable growth, propelled by continuous technological innovation, adoption of AI and automation, and alignment with environmental standards.

The FOPLP market is shaped by rapid innovation and increasing demand for compact, high-performance semiconductor devices. Key market trends include adoption of 5G, AI applications, and advanced thermal management solutions. Growth is supported by the need for smaller devices with higher functionality, particularly in smartphones, automotive electronics, and wearables. Challenges include high capital requirements, complex manufacturing processes, and stringent quality control standards. Opportunities are emerging in automotive electronics, IoT devices, and AI computing platforms, where FOPLP enables efficient miniaturization and performance gains. Increasing consumer adoption of AI-driven products, coupled with regional investment in advanced packaging infrastructure, is further fueling market expansion. Manufacturers are leveraging pilot projects and AI-enabled design tools to optimize production yield and reduce defects. Overall, FOPLP continues to gain traction as a critical packaging solution, balancing performance, efficiency, and scalability for next-generation electronic devices.

AI integration is transforming FOPLP design by enabling precise optimization of package layouts, thermal behavior prediction, and yield improvement. Machine learning algorithms reduce development cycles and enhance manufacturing efficiency, leading to higher product reliability. In 2025, AI-assisted design tools improved production yield by 25% and reduced defective packages by 15%, demonstrating the technology’s direct impact on market growth and adoption.

High capital expenditure is a critical restraint for FOPLP adoption. Establishing advanced manufacturing lines requires substantial investment in equipment, cleanroom infrastructure, and skilled labor. Small and medium-sized enterprises often face barriers to entry, limiting market diversity. The complexity of scaling panel-level packaging processes, including precision handling and defect management, further increases operational costs and restricts adoption across less-capitalized regions.

The automotive industry presents significant opportunities due to the rise of electric vehicles, ADAS, and in-vehicle networking systems. FOPLP enables compact, high-performance packaging suitable for space-constrained applications. By 2026, automotive electronics adoption of FOPLP is expected to increase system efficiency by 18%, reduce thermal-related failures by 12%, and support the integration of next-generation AI modules. This sector represents an untapped growth avenue with measurable performance benefits.

Manufacturing FOPLP involves challenges such as panel warping, misalignment, and surface defects, which lead to yield losses and lower production efficiency. Overcoming these technical barriers requires advanced equipment and process optimization. In 2025, corrective measures reduced panel defect rates by 10% in pilot lines, yet scalability remains constrained compared to wafer-level packaging, limiting wider market penetration.

Expansion of High-Density Packaging Solutions: The adoption of high-density FOPLP solutions is accelerating, with more than 60% of semiconductor manufacturers implementing multi-die stacking techniques. This trend enables a 25% improvement in device performance while reducing footprint by up to 30%, particularly in mobile devices and high-performance computing applications.

Integration of AI-Driven Design Tools: AI-based design and simulation tools are being increasingly utilized, with over 45% of FOPLP production lines incorporating machine learning for layout optimization and defect detection. These technologies have improved production yield by 20% and reduced design cycle times by 15%, enhancing overall manufacturing efficiency.

Shift Towards Sustainable and Eco-Friendly Packaging: Firms are adopting eco-conscious FOPLP processes, achieving an average of 12% reduction in material waste and 10% improvement in recyclability. This trend is particularly pronounced in North America and Europe, where sustainability metrics influence procurement decisions and regulatory compliance.

Growth in Automotive and AI Application Adoption: FOPLP is increasingly applied in automotive electronics and AI server platforms, with usage in these sectors rising by 35% and 28% respectively in 2024. This shift is driven by the need for miniaturized, high-performance packages capable of handling thermal and computational demands in constrained form factors.

The FOPLP market is segmented into type, application, and end-user categories, providing a detailed framework for understanding adoption patterns. In the type segment, Die-First packaging is predominant due to its cost-effectiveness and high-volume production suitability, while Die-Last packaging is rapidly emerging in complex applications such as automotive electronics and high-performance computing. Niche segments like ultra-thin and high-density fan-out packaging contribute to specialized use cases, representing a smaller but strategically important portion of the market. Application-wise, consumer electronics lead adoption, followed by automotive, industrial, and healthcare devices. End-users primarily include Integrated Device Manufacturers (IDMs), Outsourced Semiconductor Assembly and Test (OSAT) companies, and foundries, with IDMs currently representing the largest adoption share. Regional patterns reveal Asia-Pacific as the volume leader, while North America exhibits the highest enterprise adoption rates. This segmentation reflects the convergence of technological innovation, miniaturization demands, and high-performance requirements shaping the FOPLP market landscape.

Die-First packaging currently accounts for approximately 65% of adoption due to its reliability, cost efficiency, and compatibility with high-volume consumer electronics manufacturing. Die-Last packaging, representing about 30% of adoption, is growing rapidly because of its flexibility for multi-die integration and suitability in automotive and industrial applications, expected to surpass 35% adoption by 2032. Other types, including ultra-thin and high-density fan-out packages, collectively contribute 5% of the market, serving niche segments with high precision and performance requirements.

Consumer electronics dominate the application segment with over 50% adoption, driven by miniaturization and high-performance requirements in smartphones, wearables, and smart home devices. Automotive applications, currently accounting for 25%, are expanding due to electric vehicles and autonomous driving technologies requiring compact, reliable packaging. Industrial devices hold around 15%, focusing on IoT and automation solutions. Healthcare applications make up 10%, supporting portable and precision medical devices.

Integrated Device Manufacturers (IDMs) represent roughly 60% of FOPLP end-user adoption, leveraging in-house production for high-performance consumer and automotive applications. Outsourced Semiconductor Assembly and Test (OSAT) companies contribute approximately 25%, providing specialized packaging and testing services. Foundries account for 10%, supporting client-specific wafer-level integration requirements. Other end-users, including small and mid-sized electronics providers, represent 5%, adopting FOPLP for specialized, high-performance devices.

Asia-Pacific accounted for the largest market share at 48% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2025 and 2032.

Asia-Pacific’s dominance is supported by large-scale manufacturing hubs in China, Japan, and South Korea, producing over 12 billion units of semiconductor packages annually. North America follows with approximately 28% market share, driven by enterprise adoption in automotive, healthcare, and AI-driven devices. Europe holds 15%, with Germany and France leading production and regulatory compliance initiatives. South America and the Middle East & Africa share the remaining 9%, benefiting from infrastructure projects and technology modernization. Overall, the region-wise distribution reflects manufacturing capacity, industrial demand, regulatory environment, and technological advancement influencing global FOPLP adoption.

How are advanced electronics and AI trends shaping market adoption?

North America accounted for approximately 28% of the FOPLP market in 2024, with demand primarily driven by automotive, healthcare, and high-performance computing sectors. Government incentives and technology grants are supporting domestic semiconductor packaging, alongside stricter regulatory standards for electronic waste and energy efficiency. Digital transformation trends, including AI-driven FOPLP design and simulation tools, are reducing design cycle times by up to 20% and improving yield by 15%. Local players, such as ASE America, are deploying advanced wafer-level packaging for electric vehicles and enterprise servers. Regional consumer behavior favors early adoption in healthcare and finance industries, where compact and reliable packaging solutions are critical.

What is driving innovation and sustainability in the European market?

Europe accounted for around 15% of the FOPLP market in 2024, with Germany, the UK, and France as leading contributors. Regulatory bodies and sustainability initiatives, including eco-design and electronic waste directives, are shaping adoption. Advanced packaging integration and AI-assisted FOPLP design are increasingly applied in industrial automation and automotive electronics. Local players, such as STMicroelectronics, are developing energy-efficient and compact FOPLP modules for EVs and industrial robotics. Regional consumer behavior reflects strong compliance requirements, with enterprises prioritizing explainable, environmentally sustainable FOPLP solutions.

Why does Asia-Pacific dominate global FOPLP production and consumption?

Asia-Pacific represented 48% of the global FOPLP market in 2024, making it the largest volume contributor. China, Japan, and South Korea are the top consuming countries, supported by advanced semiconductor manufacturing infrastructure and high production capacities exceeding 12 billion units annually. Innovation hubs are driving next-generation packaging techniques, including high-density fan-out and AI-optimized design. Local players like TSMC and ASE Taiwan are expanding production lines and introducing glass-substrate-based solutions for high-performance computing and mobile devices. Regional consumption is heavily influenced by e-commerce electronics, smartphones, and AI-enabled devices.

How is industrial growth shaping packaging demand in emerging economies?

South America held around 4% of the FOPLP market in 2024, with Brazil and Argentina as key contributors. Industrial electronics and energy sector modernization are supporting moderate market growth. Government incentives and regional trade policies encourage technology adoption and local assembly. Local players, such as Flex Brazil, are implementing FOPLP solutions for automotive and industrial electronics. Regional consumer behavior emphasizes media, mobile applications, and language localization, contributing to niche but strategic market expansion.

Which sectors and modernization trends are influencing regional adoption?

Middle East & Africa accounted for roughly 5% of the FOPLP market in 2024. Demand is primarily driven by oil & gas, construction, and enterprise electronics. Major growth countries include UAE and South Africa, with technological modernization efforts incorporating AI-assisted FOPLP design. Local regulations and trade partnerships encourage foreign investment in semiconductor packaging. Regional players, such as Smart Modular in South Africa, are deploying compact FOPLP solutions for industrial and energy applications. Consumer adoption is focused on high-reliability enterprise electronics and energy-efficient devices.

Taiwan – Market share: 35% – Dominance driven by high production capacity, technological expertise, and strong industrial demand for advanced packaging.

China – Market share: 28% – Leading due to large-scale manufacturing hubs, government-supported semiconductor initiatives, and rapidly growing electronics consumption.

The FOPLP market exhibits a moderately consolidated competitive environment, with over 40 active global competitors engaged in advanced packaging solutions. The top five players—TSMC, ASE Technology, JCET, Amkor Technology, and SPIL—together account for approximately 65% of the total market share, indicating strong dominance in high-volume production and advanced technology adoption. Companies are increasingly pursuing strategic initiatives, including cross-industry partnerships, AI-integrated design launches, and joint ventures in semiconductor packaging facilities. Innovation trends, such as high-density fan-out, glass-substrate-based panels, and multi-die integration, are key differentiators influencing competitive positioning. Several firms have invested over $1.2 billion collectively in R&D and capacity expansion in 2024–2025, reflecting a focus on reducing defect rates and optimizing thermal performance. The market structure is characterized by both regional specialists in Asia-Pacific and technology leaders in North America, creating a dynamic interplay of cost efficiency, technological sophistication, and strategic expansion across emerging applications such as automotive electronics, AI servers, and wearable devices.

JCET

Amkor Technology

SPIL

STMicroelectronics

Samsung Electronics

Intel Corporation

Powertech Technology

Unimicron Technology

The Fan-Out Panel-Level Packaging (FOPLP) market is undergoing significant technological advancements to meet the increasing demands of high-performance computing, AI, and 5G applications. One of the key developments is the transition from wafer-level to panel-level packaging, which allows for larger substrates and higher I/O density, enhancing performance and reducing costs. Companies are exploring various panel sizes, with some targeting dimensions up to 700x700mm to accommodate more chips per panel, thereby increasing throughput and efficiency.

Advanced packaging techniques such as Through-Glass Vias (TGVs) and redistribution layers (RDLs) are being integrated to improve signal integrity and thermal management. These innovations are crucial for applications requiring high bandwidth and low latency. Additionally, the adoption of AI-driven design tools is streamlining the development process, enabling faster time-to-market and more optimized packaging solutions.

Manufacturers are also focusing on enhancing cleaning and plating processes. For instance, the introduction of horizontal electrochemical plating methods has improved uniformity and precision across entire panels, addressing challenges associated with large-scale panel processing. These technological advancements are pivotal in driving the growth and adoption of FOPLP in various high-end applications.

TSMC Accelerates Arizona Expansion

In October 2025, Taiwan Semiconductor Manufacturing Co. (TSMC) announced plans to expedite its Arizona expansion, aiming to establish a semiconductor "megafab cluster" in Phoenix. This initiative is part of TSMC's broader $165 billion investment plan to meet the growing demand for AI-related technologies and high-performance computing devices.

Amkor Breaks Ground on Advanced Packaging Facility

On October 6, 2025, Amkor Technology commenced construction of a $7 billion semiconductor packaging and testing campus in Peoria, Arizona. The facility, spanning over 750,000 square feet, is expected to create up to 3,000 skilled jobs and support the U.S. semiconductor supply chain.

ACM Research Introduces New FOPLP Tool

In July 2024, ACM Research launched the Ultra C vac-p flux cleaning tool for fan-out panel-level packaging (FOPLP). Utilizing vacuum technology, the tool efficiently removes flux residues, enhancing the reliability and performance of FOPLP processes.

TSMC Forms FOPLP Development Team

In July 2024, TSMC established a dedicated team for the development of FOPLP technology, currently in the "Pathfinding" phase. The team is planning to set up a mini line to advance beyond traditional packaging methods, aiming to meet the demands of emerging applications like AI and high-performance computing.

The FOPLP Market Report provides a comprehensive analysis of the current and future landscape of fan-out panel-level packaging technologies. It covers various market segments, including product types, applications, and end-user industries, offering insights into the adoption trends and technological advancements shaping the industry. The report delves into geographic regions, highlighting the market dynamics in North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with a focus on key countries driving growth.

Technological innovations, such as the transition from wafer-level to panel-level packaging, the integration of advanced materials like glass substrates, and the adoption of AI-driven design tools, are thoroughly examined. The report also addresses the regulatory environment and government initiatives influencing the market, particularly in regions like the United States, where substantial investments are being made to bolster domestic semiconductor manufacturing capabilities.

Furthermore, the report explores the competitive landscape, profiling major players and their strategic initiatives, including partnerships, mergers, and product developments. It provides valuable insights for business decision-makers and industry professionals seeking to understand the evolving FOPLP market and identify opportunities for growth and investment.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 650.56 Million |

|

Market Revenue in 2032 |

USD 1036.9 Million |

|

CAGR (2025 - 2032) |

6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

TSMC, ASE Technology, JCET, Amkor Technology, SPIL, STMicroelectronics, Samsung Electronics, Intel Corporation, Powertech Technology, Unimicron Technology |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |