Reports

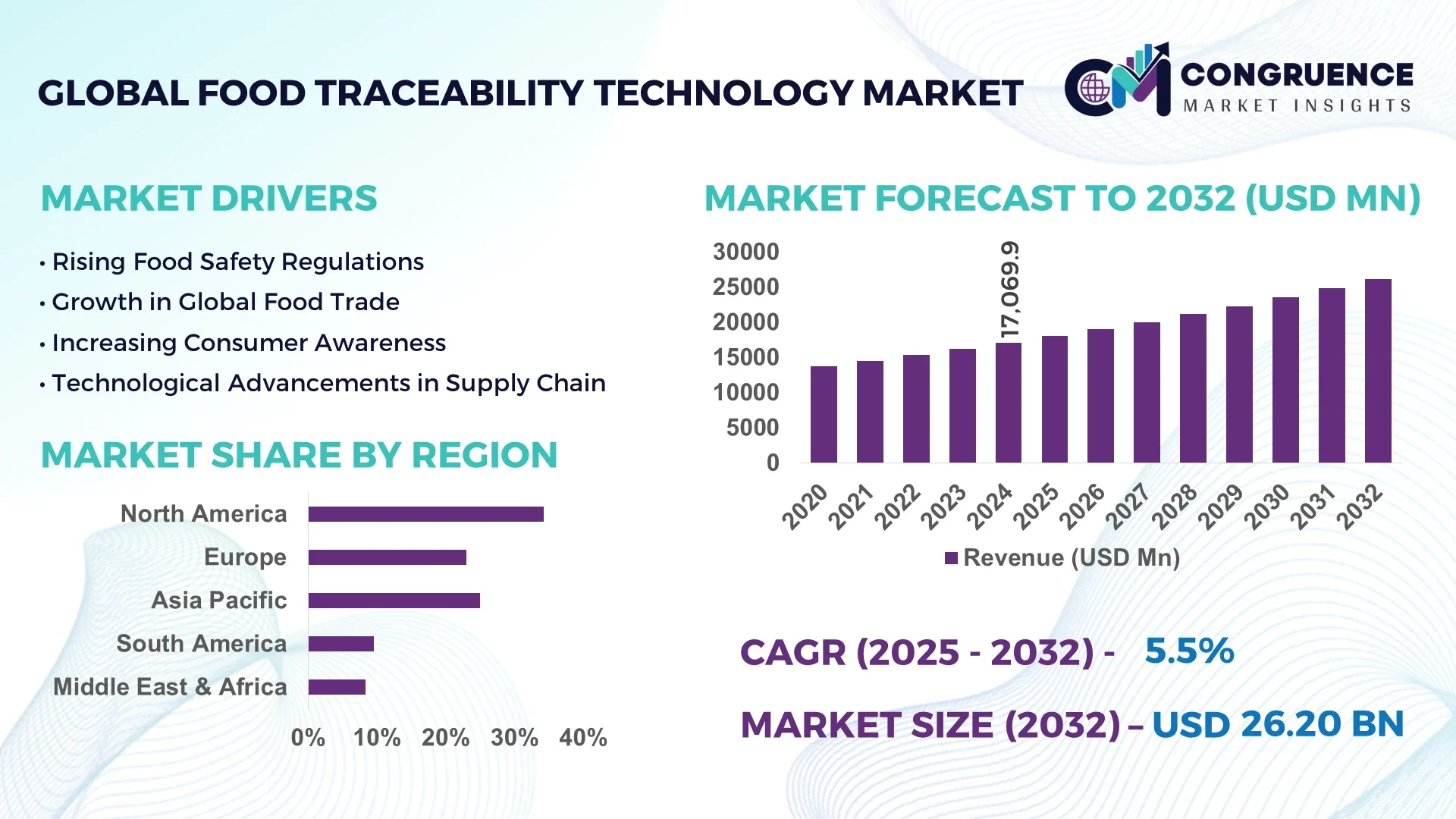

The Global Food Traceability Technology Market was valued at USD 17,069.9 Million in 2024 and is anticipated to reach a value of USD 26,196.9 Million by 2032 expanding at a CAGR of 5.5% between 2025 and 2032.

The United States continues to lead the Food Traceability Technology market, driven by its robust investment in blockchain-enabled traceability systems, high-volume production across the meat and poultry sector, and widespread adoption of cloud-based data platforms that streamline compliance and supply chain transparency across national food safety programs.

The Food Traceability Technology Market is evolving rapidly, fueled by stringent regulatory frameworks such as the Food Safety Modernization Act (FSMA), and increasing demand from consumers for safer, ethically sourced, and sustainably produced food products. Key industry sectors including meat, dairy, seafood, and packaged foods contribute substantially to the market, with meat and seafood processing plants among the highest adopters of traceability systems. Technological innovations such as RFID tagging, real-time GPS tracking, IoT sensors, and blockchain integration are improving supply chain visibility and reducing food fraud incidents. Additionally, rising demand for clean-label and organic food products across Asia-Pacific and Europe is prompting manufacturers to invest in traceability solutions that verify sourcing claims. Cloud-based platforms and digital twin technologies are emerging as game-changers, offering real-time analytics and predictive monitoring that help mitigate recalls and ensure compliance. This market’s future outlook remains strong, supported by continued digitization and growing food safety concerns.

Artificial Intelligence (AI) is revolutionizing the Food Traceability Technology Market by significantly enhancing transparency, predictive accuracy, and operational efficiency across complex food supply chains. AI-driven analytics platforms are enabling real-time decision-making by aggregating data from IoT devices, RFID tags, and blockchain ledgers. These intelligent systems can instantly detect anomalies in temperature, humidity, or handling during food transportation, thereby mitigating potential spoilage or contamination risks. For instance, machine learning algorithms are being used to optimize route planning for perishable goods, minimizing transit time and maintaining product quality.

Furthermore, AI models are aiding manufacturers and distributors in automating compliance checks and identifying potential regulatory violations before products reach retail shelves. In high-risk categories such as dairy, meat, and seafood, computer vision systems powered by AI are used to assess quality in real-time during packaging and distribution. Predictive AI tools are also helping retailers anticipate inventory shortages or surpluses based on consumption trends, reducing waste and enhancing profitability. In the broader context of the Food Traceability Technology Market, these advancements support a more resilient and responsive ecosystem, allowing companies to address disruptions swiftly.

AI integration not only accelerates traceability processes but also supports sustainability goals by reducing food loss across the supply chain. With the rise of cloud-enabled AI platforms, even small and mid-sized enterprises can now adopt scalable traceability solutions without significant infrastructure investment. As digital transformation continues, AI will remain at the forefront of innovations reshaping how traceability technologies are developed, deployed, and scaled globally.

“In March 2024, a leading agri-tech firm deployed an AI-powered traceability engine capable of processing over 2 million data points daily across 40+ food product lines. The system reduced data processing time by 70%, enabling near-instant origin verification and improving batch recall precision across its supply chain.”

The Food Traceability Technology Market is undergoing transformative changes driven by rising global food safety regulations, evolving consumer expectations, and increasing incidences of foodborne illnesses. With globalization of food supply chains, maintaining transparency and accountability from production to point-of-sale has become a business-critical imperative. Government initiatives mandating digital traceability frameworks are playing a significant role in shaping market strategies. Industry players are increasingly investing in cloud-based data management systems, blockchain integration, and real-time analytics to strengthen operational integrity and improve trace-back capabilities. Additionally, demand for eco-labeling and sustainability certifications is pushing companies to enhance their traceability infrastructure. Amid this backdrop, food manufacturers, distributors, and retailers are leveraging advanced technologies to minimize product recalls, improve brand trust, and comply with stringent compliance standards across regions.

Government mandates and regulatory pressures are a major driver propelling the Food Traceability Technology Market forward. With regulations such as the U.S. FDA’s FSMA Rule 204 and Europe’s General Food Law, traceability has transitioned from a value-add to a compliance necessity. These policies require food companies to maintain end-to-end traceability, from sourcing and production to distribution and sale. Consequently, food manufacturers are adopting serialization, barcode labeling, and digital ledger technologies to meet documentation standards and enhance food safety compliance. In addition to mitigating risks of recalls and food fraud, regulatory frameworks incentivize investment in traceability innovations. The implementation of these measures is particularly robust in sectors like seafood, dairy, and packaged food, where consumer safety and origin verification are critically monitored.

One of the primary restraints in the Food Traceability Technology Market is the high initial cost associated with deploying end-to-end traceability infrastructure. SMEs, which make up a substantial portion of the global food processing and retail industry, often lack the financial resources and technical expertise to adopt advanced technologies like blockchain, IoT sensors, and AI-based tracking platforms. These costs include hardware acquisition (e.g., scanners, RFID systems), software licensing, integration with existing ERP systems, and staff training. Additionally, the ongoing need for system updates, data storage, and cybersecurity compliance further adds to operational overhead. As a result, many smaller enterprises are either delaying adoption or opting for fragmented solutions, thereby slowing market-wide uniformity in traceability practices.

The rise of blockchain technology and cloud-based platforms presents a significant growth opportunity in the Food Traceability Technology Market. Blockchain ensures tamper-proof, immutable records of food product journeys, which builds consumer confidence and enhances accountability throughout the supply chain. Cloud-based systems offer scalability, remote access, and cost-efficiency, enabling even mid-sized businesses to implement comprehensive traceability solutions. Companies in emerging markets are increasingly leveraging Software-as-a-Service (SaaS) platforms to digitize and automate their traceability workflows without heavy capital expenditure. Additionally, these technologies support interoperability with global food safety databases and certifications, paving the way for international trade and market expansion. As food fraud and cross-border contamination cases rise, digital platforms offer a streamlined solution to maintain compliance and consumer safety.

A critical challenge impacting the Food Traceability Technology Market is the absence of harmonized traceability standards across different countries and regions. While some developed nations have stringent, clearly defined traceability requirements, others lack robust policy frameworks or enforce inconsistent regulations. This disparity creates operational complexity for multinational food companies managing cross-border supply chains. Integrating traceability systems that comply with varying standards often leads to data silos, increased operational burden, and reduced system efficiency. Furthermore, varying barcode formats, labeling requirements, and data sharing protocols hinder seamless interoperability. The lack of global alignment not only slows adoption but also creates vulnerabilities in monitoring food authenticity and tracking contamination sources during international recalls.

• Surge in Blockchain-Based Authentication Systems: Blockchain technology is rapidly gaining traction in the Food Traceability Technology market, particularly among exporters and organic food producers. Companies are using decentralized ledgers to create tamper-proof digital records that verify the origin and handling of food products. In 2024 alone, over 45% of newly launched traceability platforms in North America integrated blockchain modules for compliance and consumer trust enhancement. This trend is expected to grow further as international trade regulations tighten on origin verification and food fraud prevention.

• AI-Powered Predictive Analytics in Cold Chain Monitoring: Artificial Intelligence has been increasingly applied to cold chain logistics, especially for perishable products such as dairy and seafood. Predictive analytics powered by AI is helping logistics operators reduce spoilage by forecasting temperature fluctuations and automatically rerouting shipments. In 2024, approximately 31% of cold chain solution providers integrated AI-enabled sensors for predictive maintenance and real-time analytics, ensuring continuous quality control from farm to fork.

• Expansion of Mobile-Integrated Traceability Tools: Mobile-first platforms are redefining accessibility and efficiency in traceability systems. QR code-based product scanning and mobile app integration now allow consumers and inspectors alike to retrieve detailed product histories instantly. In Southeast Asia, over 60% of SMEs in the packaged food segment adopted mobile-enabled traceability solutions in 2024, driven by increased smartphone penetration and cost-effective SaaS solutions.

• Growth of Interoperable Cloud Traceability Platforms: Cloud-based traceability systems are becoming the backbone of global food logistics, particularly for multinational food corporations. These platforms facilitate real-time data exchange, scalability, and remote access, improving responsiveness to compliance alerts and quality control incidents. In Europe, over 52% of food manufacturers upgraded to cloud-hosted traceability solutions in 2024, primarily to unify multiple vendor databases into a centralized, easily auditable system.

The Food Traceability Technology market is segmented across three core dimensions—type, application, and end-user—each contributing uniquely to the sector's structural dynamics. From product-based tracking systems like RFID and barcoding to process-oriented platforms integrating cloud and AI, segmentation by type highlights varying technological maturity. In terms of application, traceability systems are increasingly embedded in operations across meat, seafood, dairy, and fresh produce industries to minimize safety risks and boost consumer transparency. The end-user landscape includes food manufacturers, retailers, government agencies, and logistics providers. Food manufacturers currently lead in adoption due to their critical role in quality control and recall management, while logistics and retail sectors are catching up as traceability expectations extend beyond production into last-mile delivery. As traceability becomes a global imperative, detailed segmentation is vital for identifying investment pockets, regulatory focus areas, and technological readiness across the supply chain.

In the Food Traceability Technology market, Radio Frequency Identification (RFID) systems continue to lead due to their precision, real-time tracking capabilities, and minimal human input requirements. These systems are especially favored in the meat and seafood sectors for automating inventory and shipment validation. Barcoding systems also hold a strong market presence, particularly in the packaged food and beverage industry where standardization is easier to implement. Meanwhile, GPS tracking tools are gaining relevance for their use in monitoring in-transit conditions across the cold chain. The fastest-growing type is blockchain-enabled platforms, driven by their immutable data structure, which ensures product authenticity and reduces the risk of fraud. Cloud-based traceability software is also expanding its footprint due to lower upfront costs and easier integration with mobile and web interfaces. Manual and semi-digital systems still exist in emerging markets but are gradually being phased out as digital transformation accelerates. Each technology type plays a distinct role depending on the complexity and scale of the supply chain it serves.

Among various applications, the meat and poultry segment represents the most advanced use of Food Traceability Technology, owing to high regulatory scrutiny, perishability, and the risk of zoonotic diseases. Automated systems track animal history, slaughter dates, and processing methods, enhancing safety and compliance. The seafood segment is the fastest-growing application, primarily because of rising concerns over illegal, unreported, and unregulated (IUU) fishing. Traceability tools here validate the source and journey of seafood products, especially in Asia-Pacific coastal economies. Dairy traceability is also becoming critical, with IoT sensors being adopted to monitor temperature and contamination during transit. Fresh fruits and vegetables, often affected by microbial outbreaks, are also seeing increased traceability adoption to manage recalls more efficiently. Packaged foods rely on barcoding and serialization for batch identification and recall readiness. Each application faces unique traceability challenges, but digital systems are helping bridge gaps in visibility and accountability across the board.

Food manufacturers are the dominant end-users in the Food Traceability Technology market, primarily due to their central role in integrating raw material tracking with production, packaging, and compliance workflows. Large-scale manufacturers have adopted comprehensive digital platforms that integrate with ERP and quality management systems to ensure real-time tracking of inputs and outputs. Retailers are emerging as a fast-growing end-user segment, driven by consumer demand for transparency and the need to meet retail-specific labeling and sourcing standards. Supermarkets and online grocery platforms are particularly investing in mobile-accessible, cloud-based traceability tools to improve customer engagement and supply chain validation. Logistics and distribution companies are also integrating temperature and location tracking tools to ensure food safety across transportation chains. Additionally, government agencies and regulatory bodies are adopting traceability systems to monitor safety compliance and facilitate efficient recall management. Each end-user segment leverages traceability differently based on its position in the value chain, but together they form an interconnected framework supporting safer and more transparent food systems.

North America accounted for the largest market share at 34.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.7% between 2025 and 2032.

The Food Traceability Technology market in North America remains dominant due to its advanced digital infrastructure, well-established regulatory mandates, and strong food safety enforcement frameworks. Meanwhile, Asia-Pacific is witnessing accelerated adoption of traceability systems driven by rising food exports, increasing incidences of food fraud, and growing government investments in digital agriculture. Across regions, varying factors such as modernization of food logistics, AI-enabled platforms, and mobile traceability apps are influencing adoption patterns and future market trajectories. Key growth drivers also include sustainability goals, demand for product origin verification, and integration of real-time analytics to manage recalls and compliance. Overall, regional dynamics are shaped by the interplay of technological maturity, policy enforcement, and sector-specific digitization strategies.

Digitization of Food Safety Enhances Systemic Compliance Across Production Networks

In 2024, North America commanded 34.2% of the Food Traceability Technology market, driven by its advanced ecosystem of smart logistics, stringent FDA traceability regulations, and high awareness of food safety. The meat, poultry, and packaged food sectors lead the adoption curve, with widespread use of RFID systems, blockchain, and AI-powered traceability dashboards. Government mandates like the FSMA Rule 204 have compelled food processors and distributors to invest in digital infrastructure to meet traceability and recall response standards. Cloud-based compliance tracking and mobile QR scanning tools are also being rapidly adopted by food retailers. Additionally, increased funding support for agri-tech and traceability startups is accelerating technology penetration, especially among mid-sized enterprises. The region continues to evolve into a global innovation hub, integrating automation and AI across multiple points of the food supply chain.

Sustainability Compliance and Smart Labeling Drive Traceability Integration

Holding 26.7% of the global Food Traceability Technology market in 2024, Europe is emerging as a key region driven by sustainability regulations and transparency mandates across food industries. Countries such as Germany, the United Kingdom, and France are leading in the adoption of blockchain-based food tracking and eco-labeled product certifications. The European Food Safety Authority (EFSA) and related regulatory bodies have tightened traceability requirements across dairy, seafood, and fresh produce sectors. Additionally, traceability integration with environmental labeling schemes is supporting the European Union's Green Deal goals. Digital twins and AI-enhanced risk monitoring systems are being increasingly deployed to manage real-time contamination alerts and ensure quick response. The focus on local sourcing, coupled with consumer demand for clean-label and ethically sourced foods, is pushing companies to implement more transparent and automated traceability platforms.

Rising Export Volumes and Smart Agriculture Propel Digital Food Safety Solutions

Asia-Pacific ranked as the fastest-growing region in the Food Traceability Technology market in 2024, with China, India, and Japan emerging as the top adopters. Rapid expansion in food exports, increasing food safety scandals, and urbanization of food supply chains have accelerated traceability integration across sectors. Smart agriculture initiatives and widespread use of mobile traceability platforms are helping bridge infrastructure gaps in rural production zones. Japan is focusing on high-precision tracking systems in its seafood and dairy sectors, while India is leveraging government-funded platforms to digitize post-harvest logistics. China continues to scale blockchain-based systems in retail to combat food fraud. Regional innovation hubs are focusing on low-cost IoT sensors and AI-driven trace-back models to manage risks, ensure transparency, and enhance export credibility. Rising consumer demand for organic and certified produce further reinforces the push for traceability compliance.

Government Mandates and Export-Oriented Growth Spur Traceability Deployment

South America contributed 6.3% to the global Food Traceability Technology market in 2024, with Brazil and Argentina leading the way. These nations are major exporters of meat, soybeans, and fresh produce, making traceability a key requirement for international trade. Brazil has implemented traceability systems across cattle and poultry supply chains in response to EU import regulations. Argentina, meanwhile, is investing in agro-logistics infrastructure to enable end-to-end visibility from farm to port. Government incentives, digital labeling requirements, and enhanced food inspection protocols are encouraging agribusinesses to adopt RFID and cloud-based tracking solutions. Furthermore, regional agritech startups are playing a growing role in digitizing farm-level data to improve recall management and satisfy global sustainability standards.

Modernization of Agri-Logistics and Import Oversight Drive Traceability Uptake

The Middle East & Africa region represented 4.5% of the global Food Traceability Technology market in 2024, with the UAE and South Africa emerging as pivotal countries for technology adoption. A growing reliance on food imports and heightened consumer awareness have pushed governments to implement strict quality assurance measures. UAE’s smart food control systems and real-time product verification platforms have gained momentum, especially across its retail and hospitality sectors. South Africa is investing in digitized cold chain monitoring for dairy and fresh produce, supported by partnerships with international tech firms. The region is also experiencing increased use of mobile traceability apps to ensure compliance in informal food markets. Regulatory harmonization efforts and free trade agreements with Europe and Asia are creating additional incentives for modernization across food value chains.

United States – 26.3% market share

Strong digital infrastructure, comprehensive FDA regulations, and widespread enterprise adoption across meat and packaged food industries.

China – 17.5% market share

Rapid deployment of blockchain and mobile traceability platforms to combat food fraud and enhance transparency in domestic and export markets.

The Food Traceability Technology market is highly competitive and characterized by continuous innovation, strategic collaborations, and digital transformation. As of 2024, over 130 active companies operate globally within this space, ranging from established technology giants to specialized agri-tech startups. Market leaders are aggressively expanding their capabilities through AI integration, blockchain development, and cloud-native platforms to offer scalable and interoperable solutions. Strategic partnerships between food manufacturers and tech firms are increasing, particularly in regions such as North America and Asia-Pacific, where digital adoption is high.

Notable trends include the launch of traceability-as-a-service (TaaS) models and the development of mobile-first platforms targeting small and medium enterprises. Innovation is also being driven by increased investment in IoT-enabled sensors for real-time environmental tracking and the application of digital twins for quality assurance. Mergers and acquisitions are shaping market consolidation, with key players acquiring niche firms to enhance supply chain intelligence or regional reach. Furthermore, the demand for compliance-ready solutions has intensified R&D activity, leading to the rollout of customizable modules tailored for industries like seafood, dairy, and packaged foods. As regulatory frameworks tighten globally, competitive differentiation is becoming increasingly dependent on technological agility and compliance integration.

IBM Corporation

SAP SE

Zebra Technologies Corporation

Trimble Inc.

Bio-Rad Laboratories, Inc.

Avery Dennison Corporation

OPTEL Group

Intellias Ltd.

Trace One

Rfxcel Corporation

Technological advancements in the Food Traceability Technology market are fundamentally reshaping how stakeholders across the supply chain track, verify, and manage food safety and quality. Among the most impactful technologies is blockchain, which offers immutable records and tamper-proof data trails for enhanced transparency and trust. Major food exporters are integrating blockchain into their systems to validate product authenticity and origin, particularly in the seafood and organic produce sectors.

Artificial Intelligence (AI) is also emerging as a key driver, enabling predictive analytics for spoilage detection, route optimization in logistics, and automated compliance checks. AI-integrated systems are currently being deployed in cold chain operations to monitor temperature-sensitive products in real time. IoT-based sensors are gaining traction across agriculture and transportation, offering real-time insights into environmental conditions such as temperature, humidity, and handling activity, which are critical for maintaining product integrity.

Cloud-based platforms are becoming essential for centralized data management and remote access. These platforms support real-time collaboration between producers, distributors, and regulators, reducing response time during recalls or compliance audits. Additionally, QR codes and mobile traceability applications are enhancing consumer engagement by providing product origin and handling history at the point of purchase. Together, these technologies are not only improving traceability efficiency but also reinforcing food safety, operational transparency, and regulatory alignment across global markets.

• In August 2024, IBM launched an AI-powered traceability platform designed specifically for dairy supply chains. The platform automates compliance tracking and integrates blockchain for origin validation, already adopted by over 150 regional cooperatives in Europe and North America.

• In February 2024, India’s Ministry of Agriculture rolled out a national food traceability portal for horticulture products, equipped with QR code-based tracking and satellite integration, covering more than 3,000 farm clusters within the first quarter of launch.

• In October 2023, OPTEL Group introduced a cloud-native serialization and traceability suite tailored for seafood supply chains. The platform facilitates real-time validation of catch data, processing location, and cold chain integrity using smart sensor integration.

• In July 2023, Avery Dennison deployed RFID-enabled labeling systems for major U.S. poultry producers. The technology reduced manual scanning by 60% and enabled real-time monitoring of logistics from farms to processing units.

The Food Traceability Technology Market Report provides a comprehensive analysis of the current landscape and future outlook for technologies and applications shaping global traceability practices in the food sector. The report covers a diverse array of market segments, including RFID systems, barcode technology, GPS tracking, blockchain solutions, cloud-based traceability platforms, and AI-powered analytics tools. These technologies are examined in terms of adoption patterns, scalability, and use-case scenarios across the supply chain.

Geographically, the report focuses on key regions such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into region-specific regulatory frameworks, infrastructure readiness, and adoption trends. From the application perspective, the report analyzes traceability integration in sectors including meat and poultry, dairy, seafood, fresh produce, and packaged foods, each with unique compliance and safety demands.

Additionally, the report highlights key end-user segments such as food manufacturers, logistics providers, government agencies, and retailers, reflecting varied technological needs and investment capacities. The scope extends to niche and emerging market areas like organic certification systems, cold chain optimization, and mobile-first traceability tools for SMEs. Decision-makers will gain actionable insights into competitive dynamics, innovation drivers, and market readiness for future technologies reshaping food safety, regulatory compliance, and consumer trust.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 17069.9 Million |

|

Market Revenue in 2032 |

USD 26196.9 Million |

|

CAGR (2025 - 2032) |

5.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

TDK Corporation, Murata Manufacturing Co., Ltd., Panasonic Industry Co., Ltd., Vishay Intertechnology, Inc., Taiyo Yuden Co., Ltd., Bourns, Inc., Samsung Electro-Mechanics, Sumida Corporation, Würth Elektronik GmbH & Co. KG, Chilisin Electronics Corp. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |