Reports

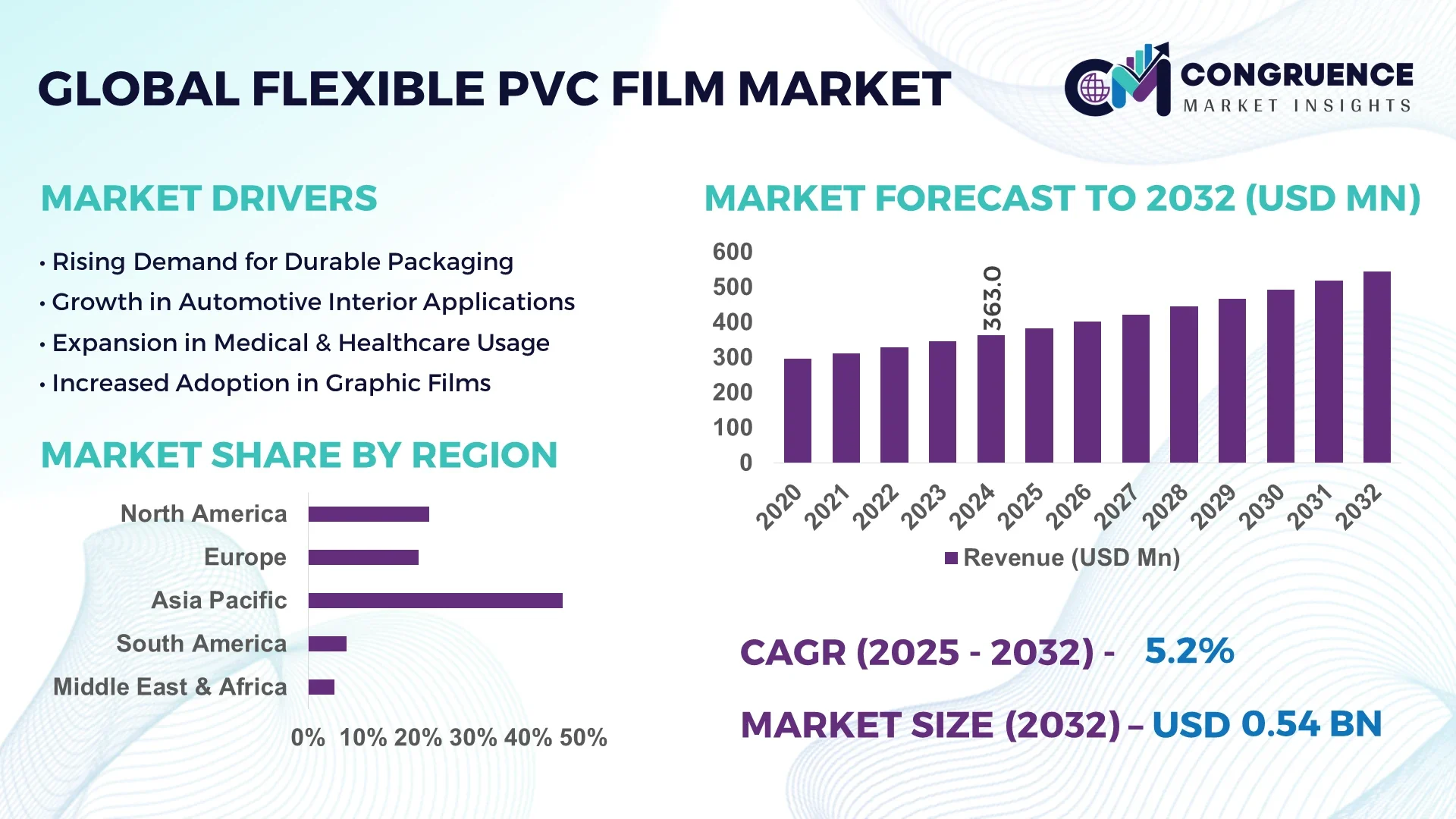

The Global Flexible PVC Film Market was valued at USD 363.0 Million in 2024 and is anticipated to reach a value of USD 546.2 Million by 2032 expanding at a CAGR of 5.24% between 2025 and 2032.

China leads the Flexible PVC Film Market with annual production capacity exceeding 1.2 million metric tons, backed by investments over USD 150 million in advanced calendaring and extrusion lines. The country’s investment supports key applications in packaging, construction membranes, and medical-grade films, with technological upgrades including improved clarity formulations and UV-resistant coatings.

The Flexible PVC Film Market spans critical sectors such as food packaging, where barrier performance is essential; building and construction, deploying films for waterproofing and protective layers; automotive interiors; and healthcare, where medical-grade films are used for IV bags and tubing. In recent years, manufacturers have introduced high-transparency, low-VOC variants and anti-microbial coated films for hygiene-critical applications. Regulatory drivers include stricter limits on phthalate plasticizers, encouraging production of phthalate-free formulations. Environmental pressures push for recyclable or bio-based plasticizer adoption, while economic shifts in emerging markets drive regional consumption. Global demand patterns show strong growth in Asia-Pacific and Latin America due to urbanization and infrastructure projects. Emerging trends include custom-printed decorative films, smart films with embedded sensors for temperature monitoring, and AI-aided production analytics to optimize process parameters. Decision-makers in procurement and R&D are focusing on scalable production lines capable of multi-purpose film output and compliance with evolving substance regulations.

In the Flexible PVC Film Market, artificial intelligence is catalyzing process modernization and quality optimization. AI-driven control systems deployed in extrusion and calendaring lines have decreased thickness variation by up to 18%, while vision-based inspection units detect surface defects with over 95% accuracy before trimming. Real-time data feedback loops—analyzing temperature, viscosity, and line speed—reduce material waste by as much as 12%, enhancing resource efficiency.

Machine learning algorithms also optimize plasticizer dosing for customized film properties, enabling rapid response to shifts in barrier, flexibility, or clarity requirements. These adaptive systems reduce trial batches by an estimated 30%, significantly cutting development time for new film grades. AI-enabled predictive maintenance systems use vibration and thermal data to anticipate gearbox or roller degradation, reducing unplanned downtime by nearly 20% across high-volume production sites.

From a strategic lens, the Flexible PVC Film Market is evolving toward “smart plants” in which AI guides batch switchover scheduling to streamline multi-product lines and minimize cleaning cycles. Centralized cloud dashboards aggregate line performance across facilities, giving decision-makers actionable insights for benchmarking and capacity planning. Supply chain coordination is also enhanced, as sales forecasts and real-time stock levels feed AI-driven procurement systems, reducing buffer stock by 15% in integrated operations. Through embedded AI, the Flexible PVC Film Market transitions from manual trial-and-error production to predictive, data-driven, and adaptive manufacturing environments, improving operational KPIs and responding effectively to evolving end-user demands.

“In 2024, a major Asian film producer implemented AI-based thickness control across four extrusion lines, reducing film scrap by 11% and cutting blend formulation variations by 8%.”

The Flexible PVC Film Market Dynamics outline multiple interrelated forces shaping industry evolution. Demand for high-performance packaging and construction materials drives continuous technological upgrades. Regulatory and environmental mandates—such as restrictions on phthalate plasticizers—are redirecting R&D toward safer plasticizers and recyclable formats. Economic expansion in emerging regions underpins rising consumption, requiring manufacturers to scale capacity and localize output. Concurrently, the integration of AI, sensor-based quality assurance, and modular extrusion platforms enhances operational efficiency. Supply chain resilience—highlighted during disruptions—has prompted geographically diversified production networks. These dynamics collectively require agile investment in flexible, tech-enabled production vessels, compliance-ready formulations, and customer-responsive product development.

In many regions, procurement teams report a 22% increase in demand for recyclable flexible PVC films with phthalate-free plasticizers. Manufacturers have responded by commissioning pilot lines capable of producing up to 5,000 tons per month of bio-plasticizer formulations. These materials are increasingly used in food wrap, labels, and medical-grade tubing due to their compliance with new chemical restrictions.

Raw PVC resin and plasticizer costs can vary by as much as 35% year-over-year, introducing budgeting challenges. Facilities using blended plasticizers must run extensive compatibility tests to ensure film performance—adding up to six weeks and USD 200,000 per product launch in trial and validation costs. Such variability limits the ability to offer long-term fixed-price contracts.

Automotive finishers and interior designers are increasingly specifying digitally printable PVC films for dashboards, door trim, and wall coverings. Since 2023, more than 150,000 square meters per month of digitally printable decorative PVC films have been deployed in new automotive pilot programs, signifying a viable growth pathway in specialty applications.

Processing lines over 15 years old lack interfaces for modern sensors and AI modules. Retrofitting such lines costs approximately USD 1.2 million and requires 4–6 weeks of downtime. Small and mid-sized producers struggle to allocate 60–70% of capex to retrofit projects, inhibiting widespread technology upgrades across the market.

Surge in Anti-Microbial Films: Medical and food-grade segments have seen a 35% YoY increase in anti-microbial flexible PVC film usage, now reaching more than 120,000 tons annually. These formulations inhibit bacterial growth on high-contact surfaces and meet rising hygiene expectations in healthcare environments.

Shift to Digital Printability: The demand for single-unit customization and on-demand decorative finishes has driven 28% of new calendar lines to include digital coating modules capable of full-color print. This supports rapid changeovers and enables manufacturers to cater to diverse design specifications with no minimum order quantities.

Scaling Roll-to-Roll Sensor Integration: By 2024, nearly 40% of flexible PVC film producers have integrated inline sensors—temperature, thickness, gloss—into roll-to-roll lines. These sensors feed live dashboards that trigger automatic line-speed adjustments, reducing edge-gain and thickness outliers by up to 20%.

Modular Extrusion Systems Adoption: Modular extrusion platforms with snap-on die heads and controller units have been installed in over 60 plants globally. These systems reduce product changeover time by 50% and enable flexible processing of different film grades—from clear to UV-stable—on a single line, without turnkey equipment replacement.

The Flexible PVC Film Market is segmented based on product type, application, and end-user profiles, offering a comprehensive view of demand dynamics across industries. Each segment addresses distinct performance needs—ranging from high clarity and softness to durability and chemical resistance. In terms of type, innovations in phthalate-free and anti-microbial films are reshaping product development. Application segmentation shows strong diversity, from packaging and medical uses to industrial and construction-grade films. End-users vary widely, encompassing large-scale manufacturers, healthcare providers, automotive OEMs, and interior design companies. This multi-dimensional segmentation framework helps producers tailor formulations, capacity investments, and marketing strategies to specific market needs, regulatory frameworks, and regional usage trends. The growing preference for specialized and high-performance films is pushing suppliers to broaden their product portfolios while maintaining production efficiency and compliance.

Flexible PVC films are primarily segmented into clear films, opaque films, printed films, and colored films. Clear flexible PVC film leads the segment due to its widespread use in food packaging, protective sheets, and transparent curtains where visibility and flexibility are required. These films offer excellent optical clarity and barrier properties, making them indispensable in both industrial and consumer-facing environments.

The fastest-growing type is phthalate-free flexible PVC film, driven by stricter health and environmental regulations across North America and Europe. These films are increasingly adopted in medical and childcare products, where safety standards prohibit phthalate-based plasticizers. Manufacturers are rapidly shifting formulations to bio-based or non-toxic alternatives, increasing output volumes for this segment.

Other types such as UV-resistant, anti-microbial, and fire-retardant flexible PVC films are also gaining traction. These cater to niche but growing markets like healthcare infrastructure, industrial enclosures, and public transportation interiors. The wide variety of specialized films ensures that type segmentation remains a key strategic focus area for manufacturers.

The leading application area within the Flexible PVC Film Market is food packaging, owing to the film’s excellent sealing, durability, and transparency properties. PVC’s compatibility with thermoforming and vacuum sealing machinery makes it a preferred material in meat, cheese, and fresh produce packaging. It also offers competitive shelf-life performance and cost-effectiveness.

The fastest-growing application is in the healthcare sector, particularly for medical bags, blood storage units, and protective drapes. The increased emphasis on hygiene, sterilization compatibility, and non-leaching film properties has accelerated adoption in clinical environments. Flexible PVC is favored due to its balance of flexibility, durability, and clarity.

Other applications include construction (used in vapor barriers and insulation films), consumer goods (stationery, tablecloths, inflatables), and automotive interiors (trims and protective layers). The expanding scope of decorative and digitally printed films for home furnishing also adds momentum. Application diversity ensures that demand remains resilient, even as trends evolve across end-user sectors.

Among end-users, the packaging industry is the largest consumer of flexible PVC films, particularly in food processing, consumer goods, and industrial logistics. Consistent demand for vacuum-formed packaging and shrink wraps from this sector reinforces its leadership. Food safety requirements, shelf-life expectations, and visual presentation needs make flexible PVC the material of choice.

The fastest-growing end-user group is the medical and healthcare industry. Growing investments in hospital infrastructure, rising volumes of single-use medical devices, and stringent infection control protocols have significantly boosted the use of flexible PVC films. They offer excellent sterilization compatibility, puncture resistance, and are suitable for high-frequency sealing technologies used in medical packaging.

Other notable end-users include the construction sector, where flexible PVC is used for waterproof membranes and protective films, and the automotive industry, where it is applied in seat covers, dashboards, and surface protection films. Emerging end-users in interior décor and smart retail displays are also adopting flexible films for lightweight, customizable visual applications.

Asia-Pacific accounted for the largest market share at 46.2% in 2024; however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.14% between 2025 and 2032.

Asia-Pacific's dominance stems from high-volume consumption in packaging, construction, and healthcare sectors, along with large-scale domestic production capacities. Meanwhile, rising investments in urban infrastructure and industrial manufacturing, especially in the UAE, Saudi Arabia, and South Africa, are accelerating demand across Middle East & Africa. Varying regulatory structures and levels of technological maturity across regions present a dynamic competitive landscape that necessitates localized strategies. Regional developments, particularly in energy-efficient manufacturing processes and circular economy mandates, are further influencing market growth, adoption, and innovation.

North America holds approximately 21.5% of the global flexible PVC film market share in 2024, with strong demand from healthcare packaging and food contact applications. The U.S. and Canada benefit from mature regulatory frameworks that encourage the production of phthalate-free and medical-grade PVC films. The healthcare sector alone drives substantial demand for high-purity films used in IV bags, medical drapes, and tubing. Additionally, FDA-compliant films are widely used in perishable food packaging. The region has seen a sharp uptick in investment in AI-driven extrusion systems that enhance quality control and minimize scrap rates. Initiatives promoting sustainability—such as the move toward recyclable plasticized films—are also shaping R&D priorities. Technological integration and regulatory clarity provide strong tailwinds for innovation and expansion in high-value flexible PVC applications.

Europe accounted for approximately 18.6% of the global flexible PVC film market in 2024, driven by advanced industrial demand and stringent environmental regulations. Key markets include Germany, the UK, France, and Italy, where demand spans healthcare, construction, and specialty consumer goods. European regulatory bodies have enforced strict phthalate usage restrictions, propelling the rapid development and commercialization of non-phthalate flexible PVC variants. Moreover, the European Green Deal and circular economy policies are prompting adoption of recyclable films and bio-based plasticizers. Technological advancements include investments in multilayer extrusion technologies and solvent-free printing solutions. European manufacturers are also capitalizing on increased demand for decorative films in automotive interiors and sustainable packaging. These innovations, paired with a strong industrial base, continue to position Europe as a leader in responsible manufacturing and product evolution.

Asia-Pacific leads the Flexible PVC Film Market with the highest volume share, accounting for 46.2% in 2024. China, India, Japan, and South Korea are the top-consuming nations, with China holding a significant portion due to its manufacturing base and export infrastructure. Construction, food packaging, medical applications, and home décor contribute to the region’s dominant demand. Rising middle-class consumption and industrial growth in Southeast Asia are further fueling expansion. Infrastructure investments and large-scale building projects in urban centers have amplified demand for protective and decorative films. Moreover, tech hubs in China and South Korea are actively deploying AI-powered quality assurance in extrusion lines, supporting scale with precision. Regional manufacturers benefit from competitive labor costs, local raw material sourcing, and supportive industrial policies, enabling them to meet both domestic and global demand efficiently.

South America contributed roughly 6.8% of the global flexible PVC film market share in 2024. Brazil and Argentina lead regional demand, primarily in food packaging, agriculture, and construction-related applications. Government-backed housing programs and export-oriented food processing industries are major consumers of flexible PVC films. Infrastructure expansion and modernization across urban areas have driven demand for moisture barriers, vapor retarders, and clear sheeting in construction. Regulatory compliance for food contact materials in Brazil has spurred the use of specialized PVC formulations. Moreover, Argentina has seen a rise in the adoption of flexible PVC films for agricultural greenhouses and irrigation lining. Trade agreements and reduced import duties on extrusion equipment are expected to further facilitate technology upgrades and domestic production across the region.

The Middle East & Africa region is poised for rapid growth, supported by strong investments in healthcare, infrastructure, and industrial diversification. In 2024, the region held around 6.9% market share, with the UAE, Saudi Arabia, and South Africa leading consumption. PVC films are increasingly used in construction membranes, waterproofing solutions, and hospital infrastructure. Several nations are embracing smart city projects and hospital expansion programs, increasing demand for hygienic and durable PVC films. The shift toward manufacturing localization has led to the setup of regional production units with upgraded calendaring technologies. Additionally, national quality standards and trade partnerships are boosting imports of raw PVC resin and calendaring machinery. Government incentives tied to sustainable material use are expected to support long-term adoption of recyclable flexible films and bio-based additives in this emerging market.

China - 34.5% Market Share

Dominates the Flexible PVC Film Market due to large-scale production capacity, advanced infrastructure, and vertically integrated supply chains.

United States - 18.2% Market Share

Leads in medical and food-grade flexible PVC film consumption due to high regulatory standards and extensive healthcare infrastructure.

The Flexible PVC Film Market features a moderately consolidated competitive landscape, with over 40 globally active manufacturers and a multitude of regional players catering to niche or localized demand. Major players are differentiated by their technological capabilities, innovation pipelines, global distribution networks, and specialization in phthalate-free or high-clarity products. Companies are focusing on backward integration to secure raw materials and reduce input volatility, especially amid fluctuating petrochemical prices.

Strategic initiatives such as capacity expansions, new product launches, and collaborations with end-use industries are common. In 2023 and 2024, several leading manufacturers introduced non-phthalate formulations and bio-based plasticizer solutions to address tightening regulations across Europe and North America. Additionally, digital transformation projects have accelerated, with companies investing in AI-driven production lines to improve quality consistency, reduce scrap rates, and enable real-time monitoring.

Market leaders are increasingly targeting medical, automotive, and high-barrier packaging sectors through customized solutions. The adoption of recyclable and multi-layer films is also shaping competitive strategies, particularly as sustainability credentials become a market differentiator. Mergers and acquisitions have been observed primarily among mid-sized firms seeking geographic expansion and technical synergies. Innovation and compliance remain the primary levers for competitive advantage.

RENOLIT SE

Teknor Apex Company

Hexis S.A.

INOVYN (An INEOS Company)

Nan Ya Plastics Corporation

Achilles Corporation

Oerlemans Plastics B.V.

Grafix Plastics

ChangZhou Tiansheng Plastic Co., Ltd.

Zhejiang Yidong Plastic Co., Ltd.

Hunan Ming Yu Nonwovens Co., Ltd.

The Flexible PVC Film Market is undergoing significant technological advancements aimed at improving material performance, environmental compliance, and production efficiency. One of the most impactful trends is the increasing adoption of phthalate-free plasticizers, which enable manufacturers to comply with evolving regulatory frameworks while maintaining film flexibility and clarity. New-generation plasticizers based on citrates, adipates, and bio-based inputs are replacing traditional phthalate compounds.

Extrusion and calendaring technologies are also evolving. High-speed, energy-efficient twin-screw extruders and automated roll-to-roll calendaring systems now offer better thickness uniformity, optical clarity, and surface finish. These machines are being integrated with machine learning and AI-powered quality control systems to minimize defects, reduce material waste, and streamline production.

Multi-layer co-extrusion is another growing technology, allowing the incorporation of different polymer layers with specific functional properties such as UV resistance, anti-fog capabilities, and antimicrobial surfaces. This has opened new opportunities in healthcare, food packaging, and automotive interiors.

Surface treatment techniques, including corona and plasma treatment, are increasingly used to improve printability and adhesion properties. In addition, digital printing advancements are enabling high-definition and customized design applications, particularly for decorative and retail films.

Recycling technologies are gaining traction, with closed-loop recycling lines being developed to reprocess post-industrial and post-consumer flexible PVC films. This supports circular economy goals and enhances brand positioning for sustainability-conscious manufacturers.

• In March 2024, RENOLIT SE unveiled its latest phthalate-free medical-grade PVC film designed for dialysis bags and blood storage, offering improved transparency and reduced extractables, tailored for use in advanced hospital-grade sterilization systems.

• In January 2024, Teknor Apex launched its BioVinyl™ flexible PVC compounds, incorporating up to 40% renewable content. The films produced using these materials are already being used in eco-conscious packaging across North America and Europe.

• In September 2023, Hexis S.A. expanded its production capacity in France by commissioning a new automated calendaring line capable of producing high-clarity decorative films at 20% higher throughput, aiming to serve the architectural and automotive sectors.

• In December 2023, Nan Ya Plastics Corporation introduced a high-durability UV-resistant flexible PVC film, optimized for outdoor signage and protective coverings, demonstrating 30% longer outdoor performance in accelerated weathering tests.

The Flexible PVC Film Market Report offers a detailed assessment of the industry, covering a broad spectrum of product types, end-use applications, and regional demand profiles. It includes in-depth segmentation analysis by type—such as clear, opaque, printed, and phthalate-free films—alongside their performance characteristics and functional roles across various sectors.

The report evaluates applications ranging from food packaging and medical use to industrial, decorative, and automotive components. Additionally, it investigates end-user dynamics, including healthcare providers, construction firms, consumer goods manufacturers, and OEMs in automotive and electronics. These segments are evaluated based on material performance, compliance requirements, and innovation trends.

Geographically, the report analyzes market performance in five key regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Special attention is given to high-growth sub-regions and countries with large-scale production capacities or emerging consumption patterns.

Technological insights span advancements in phthalate-free formulations, high-speed calendaring, AI-based defect detection, and recyclable film innovations. The report further identifies strategic opportunities in digital printing, green building solutions, and antimicrobial film applications.

Overall, the report serves as a strategic tool for industry professionals, offering a granular view of the evolving landscape, emerging technologies, and actionable insights for market penetration, product innovation, and investment planning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 363.0 Million |

| Market Revenue (2032) | USD 546.2 Million |

| CAGR (2025–2032) | 5.24% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | RENOLIT SE, Teknor Apex Company, Hexis S.A., INOVYN (An INEOS Company), Nan Ya Plastics Corporation, Achilles Corporation, Oerlemans Plastics B.V., Grafix Plastics, ChangZhou Tiansheng Plastic Co., Ltd., Zhejiang Yidong Plastic Co., Ltd., Hunan Ming Yu Nonwovens Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |