Reports

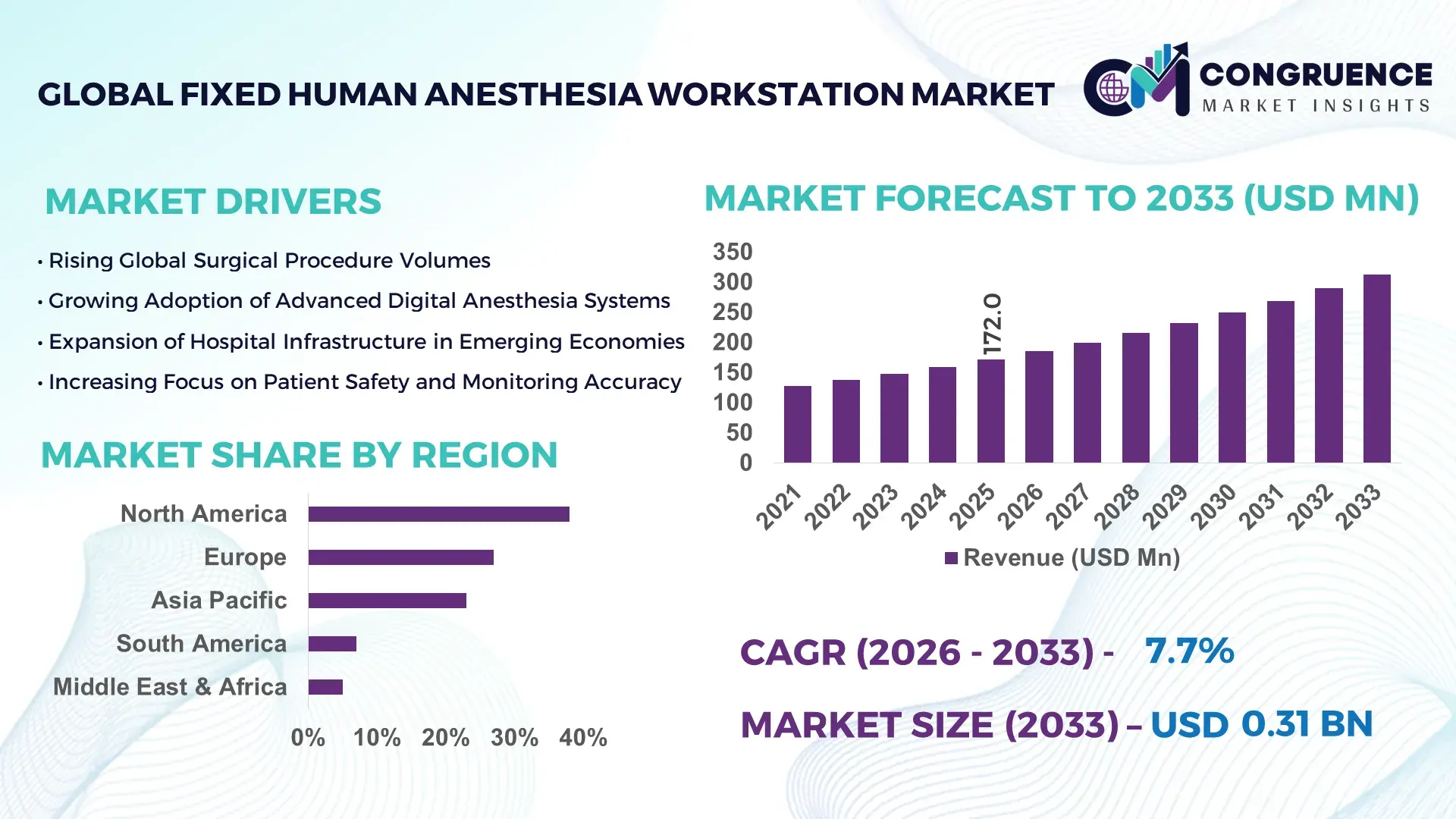

The Global Fixed Human Anesthesia Workstation Market was valued at USD 172.0 Million in 2025 and is anticipated to reach a value of USD 312.3 Million by 2033 expanding at a CAGR of 7.74% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing surgical volumes, modernization of operating rooms, and the integration of digital monitoring technologies in anesthesia delivery systems.

The United States dominates the Fixed Human Anesthesia Workstation Market with over 51 million inpatient surgical procedures performed annually and more than 6,100 hospitals equipped with advanced operating room infrastructure. The country allocates approximately 17% of its GDP to healthcare expenditure, exceeding USD 4.5 trillion annually, supporting consistent procurement of high-end anesthesia systems. Over 65% of tertiary hospitals have transitioned to integrated anesthesia workstations with real-time gas monitoring and electronic medical record connectivity. Domestic production capacity is strengthened by leading medical device manufacturers investing more than USD 2 billion annually in R&D across anesthesia and respiratory platforms, accelerating AI-enabled ventilation controls and closed-loop anesthesia delivery adoption.

Market Size & Growth: Valued at USD 172.0 Million in 2025, projected to reach USD 312.3 Million by 2033 at 7.74% CAGR, driven by rising surgical admissions and digitized operating room adoption.

Top Growth Drivers: 38% increase in minimally invasive surgeries, 42% hospital infrastructure modernization rate, 29% rise in demand for integrated patient monitoring.

Short-Term Forecast: By 2028, smart anesthesia integration is expected to improve workflow efficiency by 24% and reduce anesthetic gas wastage by 18%.

Emerging Technologies: AI-assisted ventilation algorithms, closed-loop anesthesia delivery systems, IoT-enabled gas monitoring platforms.

Regional Leaders: North America projected at USD 118.5 Million by 2033 with strong tertiary care upgrades; Europe at USD 92.4 Million driven by public hospital digitization; Asia-Pacific at USD 76.8 Million supported by 35% rise in surgical infrastructure expansion.

Consumer/End-User Trends: Hospitals account for over 68% of installations, ambulatory surgical centers show 31% adoption growth, specialty clinics increasing portable-fixed hybrid usage by 22%.

Pilot or Case Example: In 2024, a U.S. hospital network reduced anesthesia-related downtime by 27% after implementing AI-based workstation calibration systems.

Competitive Landscape: Market leader holds approximately 34% share, followed by major competitors including GE HealthTech, Dräger, Mindray, and Medtronic.

Regulatory & ESG Impact: 45% of manufacturers aligning with low-emission anesthesia gas compliance standards and targeting 30% reduction in volatile anesthetic leakage by 2030.

Investment & Funding Patterns: Over USD 850 Million invested globally in anesthesia technology upgrades between 2022–2025, with strong public-private hospital modernization programs.

Innovation & Future Outlook: Focus on integrated digital dashboards, automated gas flow regulation, and EMR interoperability shaping next-generation operating room ecosystems.

Hospitals represent nearly 68% of demand, followed by ambulatory surgical centers at 22% and specialty clinics at 10%. Innovations such as AI-enabled ventilation control and real-time gas analytics are improving patient safety metrics by up to 25%. Regulatory mandates for emission reduction and hospital digitization programs are accelerating adoption across North America and Europe, while Asia-Pacific records over 30% infrastructure expansion in surgical suites, indicating strong long-term procurement momentum.

The Fixed Human Anesthesia Workstation Market holds strategic relevance as surgical procedures globally exceed 310 million annually, demanding highly reliable, digitally integrated anesthesia delivery systems. Healthcare providers are prioritizing operating room digitization, where integrated anesthesia platforms are connected to centralized monitoring systems and electronic health records, reducing manual documentation errors by nearly 32%. AI-enabled closed-loop anesthesia systems deliver 28% improvement in dosage precision compared to conventional manual vaporizer systems, enhancing patient safety and regulatory compliance.

North America dominates in volume due to its extensive hospital network, while Western Europe leads in advanced digital adoption, with over 58% of hospitals integrating anesthesia workstations into centralized IT systems. By 2028, predictive maintenance powered by AI analytics is expected to reduce equipment downtime by 26%, improving operating room utilization rates significantly. Firms are committing to ESG metrics including a 30% reduction in anesthetic gas emissions and 20% recyclable component integration by 2030.

In 2024, Germany achieved a 19% improvement in perioperative workflow efficiency through nationwide deployment of smart anesthesia monitoring upgrades in public hospitals. Comparative benchmarking shows that automated gas flow optimization delivers 22% lower anesthetic consumption compared to older constant-flow systems. Moving forward, the Fixed Human Anesthesia Workstation Market is positioned as a critical enabler of surgical resilience, regulatory compliance, digital interoperability, and sustainable hospital operations.

The Fixed Human Anesthesia Workstation Market is influenced by rising global surgical demand, hospital modernization initiatives, and regulatory compliance requirements for patient safety. Over 70% of operating rooms in developed economies have transitioned to digitally integrated anesthesia systems, while emerging economies are increasing public healthcare infrastructure budgets by more than 20% annually. Demand is particularly strong in tertiary hospitals where integrated ventilation, gas delivery, and real-time patient monitoring are essential. Technological innovation, including closed-loop systems and AI-driven alarm management, is reshaping procurement strategies. Additionally, environmental policies targeting anesthetic gas emissions and energy-efficient medical devices are influencing product design and replacement cycles. Competitive intensity remains high, with manufacturers differentiating through digital integration, modular designs, and enhanced safety analytics.

Global surgical procedures exceed 310 million annually, with minimally invasive surgeries increasing by nearly 38% over the last five years. Approximately 65% of hospitals in developed countries are upgrading to advanced anesthesia workstations featuring integrated ventilation and multi-parameter monitoring. These systems reduce manual adjustments by 30% and improve anesthesia delivery precision by 25%. Growing geriatric populations—projected to reach 1.4 billion people aged 60+ by 2030—are increasing demand for complex procedures requiring reliable anesthesia support. Furthermore, 40% of new hospital construction projects incorporate digitally integrated operating room ecosystems, accelerating procurement of next-generation fixed anesthesia workstations.

Advanced fixed anesthesia workstations can cost between USD 40,000 and USD 80,000 per unit, creating procurement challenges for small and mid-sized healthcare facilities. Annual maintenance and calibration costs account for approximately 8–12% of equipment value. In low-income regions, nearly 35% of hospitals continue using legacy anesthesia systems older than 10 years due to budget constraints. Training requirements also pose limitations, as 22% of healthcare facilities report insufficient skilled technicians for advanced digital systems. Additionally, stringent regulatory approvals can extend product launch timelines by 12–18 months, delaying adoption in cost-sensitive markets.

AI-enabled closed-loop anesthesia systems improve dosage accuracy by up to 28% and reduce anesthetic gas wastage by 18%, presenting significant cost-saving opportunities. Hospitals aiming for 30% emission reduction targets are adopting low-flow anesthesia technologies, increasing demand for energy-efficient workstations. Emerging markets are expanding surgical infrastructure by over 25% annually, creating procurement opportunities for mid-range systems. Additionally, ambulatory surgical centers—growing at 9% annually in developed economies—are increasingly investing in compact yet fixed-configured anesthesia systems with digital connectivity, opening new revenue channels for manufacturers focusing on modular and interoperable designs.

Anesthesia workstations must comply with rigorous safety standards including IEC and ISO certifications, requiring extensive validation testing that can take over 24 months. Interoperability with hospital IT systems remains complex, as nearly 30% of healthcare facilities operate on fragmented digital infrastructure. Cybersecurity risks are rising, with healthcare cyber incidents increasing by 38% year-over-year, requiring additional security layers in connected anesthesia systems. Supply chain volatility has also affected electronic component availability, increasing procurement lead times by up to 20%. These factors collectively challenge rapid deployment and technology integration.

32% Growth in AI-Integrated Anesthesia Systems: Hospitals are accelerating AI-based closed-loop anesthesia adoption, with 32% of tertiary care centers implementing automated dosage control systems. These systems improve ventilation precision by 28% and reduce adverse anesthesia events by 15%, strengthening patient safety benchmarks.

27% Reduction in Anesthetic Gas Emissions Through Low-Flow Technology: Adoption of low-flow anesthesia delivery systems has increased by 35% in advanced economies, enabling hospitals to cut volatile anesthetic emissions by 27% and reduce operational gas costs by nearly 18%. Sustainability-focused procurement policies are accelerating this shift.

29% Increase in Operating Room Digital Integration: Approximately 61% of new operating rooms globally are equipped with integrated anesthesia dashboards connected to hospital EMR systems. Digital connectivity has reduced manual documentation errors by 30% and improved perioperative workflow efficiency by 21%.

24% Expansion in Ambulatory Surgical Center Installations: Fixed-configured anesthesia systems in ambulatory surgical centers have grown by 24% over the past three years, driven by outpatient procedure volumes rising 33%. Compact workstation designs with multi-gas monitoring capabilities are increasingly preferred for high-turnover surgical settings.

The Fixed Human Anesthesia Workstation Market is segmented by type, application, and end-user, reflecting differentiated demand patterns across surgical environments and healthcare infrastructure levels. Product differentiation is largely driven by technological integration, ventilation capabilities, and digital interoperability features. From an application standpoint, general surgery and high-acuity procedures represent the largest deployment base due to consistent procedural volumes exceeding 300 million globally each year. End-user segmentation reveals hospital-based operating rooms as the primary installation base, supported by ongoing infrastructure upgrades and compliance mandates. Ambulatory surgical centers and specialty clinics are increasingly adopting compact fixed systems to accommodate high patient turnover. Decision-makers are prioritizing systems offering integrated gas monitoring, automated ventilation adjustments, and EMR connectivity, aligning procurement strategies with patient safety metrics, workflow efficiency benchmarks, and sustainability targets such as 25–30% reductions in anesthetic gas emissions.

The market is segmented into Standalone Fixed Anesthesia Workstations, Integrated Digital Anesthesia Workstations, and Hybrid Modular Fixed Systems. Standalone fixed anesthesia workstations currently account for approximately 46% of total installations, primarily due to their widespread use in secondary hospitals and cost-sensitive facilities. These systems provide reliable ventilation and vaporizer control but limited interoperability. Integrated digital anesthesia workstations hold nearly 38% adoption, offering centralized monitoring, automated gas flow regulation, and EMR integration. However, hybrid modular fixed systems are rising fastest, expanding at an estimated CAGR of 9.2%, driven by demand for scalable configurations and AI-enabled ventilation modules. These systems are expected to surpass 30% adoption by 2033 as hospitals prioritize interoperability and predictive maintenance capabilities. The remaining niche configurations, including compact fixed systems for ambulatory centers, collectively contribute about 16% of installations, serving high-turnover outpatient surgical settings.

In 2024, the U.S. Food and Drug Administration cleared multiple next-generation anesthesia workstations featuring closed-loop ventilation control, enabling automated oxygen concentration adjustments in real time across major tertiary hospitals.

Application segmentation includes General Surgery, Orthopedic Surgery, Cardiovascular Surgery, Neurology, and Others (including oncology and emergency trauma procedures). General surgery dominates with nearly 41% share due to high procedural volumes and standardized anesthesia requirements. Orthopedic and cardiovascular surgeries together account for 33%, reflecting increased demand from aging populations and rising joint replacement procedures, which have grown by over 35% in the past five years globally. Cardiovascular surgery applications are expanding fastest, with an estimated CAGR of 8.8%, driven by the increasing prevalence of cardiac disorders affecting over 520 million people worldwide. Advanced anesthesia systems with real-time hemodynamic monitoring are critical in these high-risk procedures. Neurology and oncology-related applications collectively represent approximately 18%, supported by precision anesthesia protocols and long-duration surgeries. In 2025, nearly 44% of large hospitals globally reported upgrading anesthesia platforms specifically for minimally invasive and robotic-assisted surgeries. Additionally, 39% of surgical centers in developed markets are piloting AI-assisted anesthesia systems to enhance patient safety compliance.

In 2024, the World Health Organization highlighted expanded deployment of advanced anesthesia equipment across more than 120 national surgical upgrade programs to improve perioperative safety standards.

End-user segmentation comprises Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, and Academic & Research Institutes. Hospitals lead the market with approximately 68% of total installations, supported by over 51 million annual inpatient surgeries in the United States alone and strong public healthcare investment across Europe and Asia-Pacific. Large tertiary hospitals are increasingly adopting AI-enabled integrated workstations to meet regulatory and safety benchmarks. Ambulatory Surgical Centers represent about 22% of installations and are the fastest-growing segment, expanding at an estimated CAGR of 9.5% due to outpatient procedure volumes increasing by over 30% in developed economies. Specialty clinics and research institutes collectively contribute around 10%, focusing on niche or experimental surgical procedures. In 2025, more than 42% of U.S. hospitals reported testing digitally connected anesthesia systems integrated with centralized monitoring dashboards. Additionally, 36% of outpatient surgical centers indicated plans to transition toward modular fixed systems within three years to support higher patient throughput.

In 2024, the American Society of Anesthesiologists reported expanded adoption of digitally integrated anesthesia workstations across accredited U.S. hospitals to enhance perioperative safety monitoring standards.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2026 and 2033.

North America’s dominance is supported by over 6,100 hospitals in the United States and more than 51 million inpatient surgical procedures annually. Europe follows with approximately 27% market share, driven by more than 25 million surgical interventions each year across Germany, France, and the UK combined. Asia-Pacific holds nearly 23% share, supported by rapid hospital infrastructure expansion exceeding 30% in key economies such as China and India. South America contributes around 7%, led by Brazil and Argentina with expanding tertiary healthcare networks. The Middle East & Africa collectively represent about 5%, with modernization initiatives in the UAE and Saudi Arabia increasing operating room installations by over 20% in recent years.

North America holds approximately 38% of the global Fixed Human Anesthesia Workstation Market share, supported by high surgical volumes and strong capital expenditure in hospital infrastructure. The United States performs more than 310 million surgical procedures globally each year, with a significant portion conducted within this region. Healthcare spending exceeds 17% of GDP, enabling continuous upgrades to digitally integrated anesthesia systems. Regulatory frameworks from the U.S. FDA emphasize safety compliance and emission reduction in anesthetic gases, encouraging replacement of legacy systems. Over 65% of tertiary hospitals utilize integrated anesthesia workstations connected to EMR systems. GE HealthCare, a key regional player, continues expanding AI-enabled ventilation technologies and predictive maintenance modules. Regional consumer behavior reflects higher enterprise adoption in healthcare networks prioritizing automation, interoperability, and ESG compliance, with 40% of hospitals planning additional digital anesthesia upgrades within three years.

Europe accounts for nearly 27% of the global Fixed Human Anesthesia Workstation Market share. Germany, the UK, and France are primary contributors, collectively performing over 25 million surgical procedures annually. The European Union Medical Device Regulation (EU MDR) has accelerated equipment modernization, requiring stricter safety validation and lifecycle traceability. Sustainability initiatives targeting 30% reduction in anesthetic gas emissions are influencing procurement strategies. Approximately 58% of Western European hospitals have implemented digitally integrated anesthesia systems linked to centralized monitoring dashboards. Dräger, headquartered in Germany, continues investing in low-flow anesthesia technology to support emission reduction goals. Regional adoption patterns indicate regulatory pressure drives demand for highly compliant, interoperable systems, with public hospitals leading modernization programs supported by national healthcare budgets.

Asia-Pacific represents about 23% of the global market and ranks as the fastest-growing regional cluster. China, India, and Japan are the top consuming countries, with China operating more than 36,000 hospitals and India expanding public healthcare infrastructure under national health missions. Surgical volumes in the region are rising by over 30% annually in certain metropolitan centers. Domestic manufacturing capacity is strengthening, with companies such as Mindray expanding production of integrated anesthesia systems with digital ventilation controls. Technological hubs in Japan and South Korea are advancing AI-based monitoring and smart operating room integration. Regional behavior indicates growth driven by expanding healthcare access, rising middle-class demand for surgical care, and government-backed hospital modernization programs targeting installation increases above 25% in tertiary facilities.

South America contributes roughly 7% of the global Fixed Human Anesthesia Workstation Market, with Brazil and Argentina as leading markets. Brazil alone accounts for over 6,000 hospitals and continues upgrading tertiary surgical centers under federal health initiatives. Infrastructure expansion in metropolitan hospitals has increased operating room capacity by nearly 18% in the past five years. Government procurement programs and favorable import duty adjustments for medical devices are supporting modernization. Regional distributors collaborate with multinational manufacturers to deploy digitally integrated anesthesia workstations in private hospital networks. Consumer behavior shows demand closely tied to public healthcare funding cycles, with private hospitals adopting advanced systems nearly 20% faster than public facilities due to higher capital flexibility.

The Middle East & Africa region holds approximately 5% of the global market share. The UAE, Saudi Arabia, and South Africa are key contributors, with hospital infrastructure investments exceeding USD 50 billion collectively in ongoing healthcare development projects. The UAE has expanded operating room capacity by over 22% in major urban centers. Technological modernization includes adoption of AI-enabled anesthesia monitoring systems in flagship hospitals. Trade partnerships with European and U.S. manufacturers ensure access to advanced equipment compliant with international standards. Regional demand is driven by government-led healthcare transformation programs, while private hospital groups demonstrate 15% higher adoption of integrated digital anesthesia platforms compared to public institutions.

United States – 34% Market Share: It leads due to high surgical volumes, strong domestic manufacturing capacity, and continuous hospital digitization initiatives.

Germany – 11% Market Share: It is supported by advanced healthcare infrastructure, strict regulatory compliance under EU MDR, and strong presence of local medical device manufacturers.

The Fixed Human Anesthesia Workstation Market is moderately consolidated, with approximately 25–30 active global and regional competitors participating across developed and emerging markets. The top five companies collectively account for nearly 62% of total market share, reflecting strong brand positioning, established hospital procurement relationships, and vertically integrated manufacturing capabilities. Leading players differentiate through AI-enabled ventilation algorithms, closed-loop anesthesia delivery systems, and integrated patient monitoring dashboards.

Over 45% of recent product launches between 2023 and 2025 have focused on digital interoperability and low-flow anesthesia technologies aimed at reducing anesthetic gas emissions by up to 30%. Strategic initiatives include multi-year hospital supply agreements, technology partnerships for EMR integration, and regional distribution expansions in Asia-Pacific and the Middle East. More than 40% of tier-1 manufacturers have increased R&D allocations toward predictive maintenance modules and cybersecurity layers for connected operating rooms.

Mergers and acquisitions activity has intensified, with at least 6 notable strategic collaborations announced globally since 2024 to enhance ventilation precision, software analytics, and hardware modularity. Competitive intensity is highest in North America and Western Europe, where over 65% of hospitals prioritize integrated digital anesthesia ecosystems. Pricing competition remains evident in emerging economies, where mid-range workstation models account for nearly 48% of installations.

Medtronic plc

Fisher & Paykel Healthcare Corporation Limited

Philips Healthcare

Nihon Kohden Corporation

Getinge AB

Heyer Medical AG

Spacelabs Healthcare

Penlon Limited

Beijing Aeonmed Co., Ltd.

Dameca A/S

Comen Medical Instruments Co., Ltd.

Infinium Medical

Technological evolution in the Fixed Human Anesthesia Workstation Market is centered on digital integration, automation, and sustainability. More than 60% of newly installed systems globally now include integrated multi-parameter monitoring, combining ventilation control, gas flow regulation, and real-time patient data analytics into unified digital dashboards. Closed-loop anesthesia delivery systems improve dosage precision by up to 28% compared to manual vaporizer adjustments, enhancing perioperative safety.

Low-flow anesthesia technology is gaining adoption, reducing volatile anesthetic gas consumption by nearly 25% while maintaining optimal oxygenation levels. Approximately 45% of tertiary hospitals in developed economies have transitioned toward low-flow platforms aligned with emission-reduction targets. AI-driven predictive maintenance systems reduce unplanned downtime by up to 26%, improving operating room utilization rates.

Cybersecurity integration has become a critical requirement, with 38% year-over-year growth in healthcare cyber incidents prompting manufacturers to embed encrypted connectivity protocols. Interoperability standards such as HL7 and FHIR enable seamless data exchange between anesthesia systems and hospital EMRs, reducing manual documentation errors by approximately 30%.

Emerging technologies include touchscreen-based user interfaces, automated alarm prioritization algorithms that cut false alarms by 20%, and modular hardware designs enabling 15% faster installation in new operating rooms. Research prototypes integrating cloud-based analytics allow centralized monitoring of over 50 operating rooms simultaneously within large hospital networks, strengthening data-driven perioperative management strategies.

• In October 2025, GE HealthCare unveiled the Carestation 850 anesthesia delivery system with advanced clinical tools, a large enhanced user interface, smart vaporization control, and customizable applications to improve perioperative precision, operational efficiency, and sustainability goals at the ANESTHESIOLOGY 2025 conference in San Antonio, Texas. The system is designed to support care teams from neonates to adults and is pending FDA 510(k) clearance. Source: www.gehealthcare.com

• In April 2025, Dräger launched the Atlan® A100 anesthesia workstation in India, engineered to optimize patient care with advanced lung-protective ventilation, low-flow anesthesia, infection control enhancements, adaptive piston control, and robust connectivity for data-driven workflows across hospital OR departments. Source: www.draeger.com

• In January 2025, Dräger’s Atlan® A350/A350XL anesthesia machines received an Innovative Technology designation from Vizient, recognizing the workstation’s clinical impact, precise ventilation technology, and sustainability-focused design that reduces anesthetic agent consumption and environmental footprint. Source: www.prnewswire.com

• In 2024, Mindray showcased its A9 Anesthesia Workstation advancements and participated in major industry events such as ANESTHESIOLOGY® 2024, highlighting extended capabilities like high flow nasal cannula support, automated controlled anesthesia (ACA), and integrated ICU-quality ventilation to streamline perioperative workflows and enhance patient safety. Source: www.mindray.com

The Fixed Human Anesthesia Workstation Market Report provides comprehensive analysis across product types, applications, end-user categories, and regional markets. The scope covers standalone, integrated digital, and hybrid modular anesthesia systems deployed across hospitals, ambulatory surgical centers, specialty clinics, and academic institutions. It evaluates over 300 million annual surgical procedures globally to assess demand intensity across general, orthopedic, cardiovascular, neurological, and oncology applications.

Geographic coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, collectively representing more than 95% of global surgical infrastructure. The report assesses over 30 active manufacturers, analyzing competitive positioning, technology portfolios, and distribution footprints across more than 50 countries. It further evaluates digital transformation trends, including AI-enabled ventilation systems, low-flow gas technologies reducing emissions by up to 30%, and interoperability standards integrated into over 60% of newly installed operating rooms.

The scope extends to regulatory compliance frameworks, ESG-driven procurement strategies, and cybersecurity requirements influencing equipment deployment. Additionally, the report examines hospital modernization programs, outpatient surgical growth exceeding 30% in developed markets, and manufacturing capacity expansions across Asia-Pacific. By integrating quantitative benchmarks and qualitative strategic insights, the report equips healthcare executives, procurement leaders, and investors with actionable intelligence to support capital planning, innovation strategy, and long-term operational resilience within the Fixed Human Anesthesia Workstation Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 172.0 Million |

| Market Revenue (2033) | USD 312.3 Million |

| CAGR (2026–2033) | 7.74% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | GE HealthCare; Drägerwerk AG & Co. KGaA; Mindray Medical International Limited; Medtronic plc; Fisher & Paykel Healthcare Corporation Limited; Philips Healthcare; Nihon Kohden Corporation; Getinge AB; Heyer Medical AG; Spacelabs Healthcare; Penlon Limited; Beijing Aeonmed Co., Ltd.; Dameca A/S; Comen Medical Instruments Co., Ltd.; Infinium Medical |

| Customization & Pricing | Available on Request (10% Customization Free) |