Reports

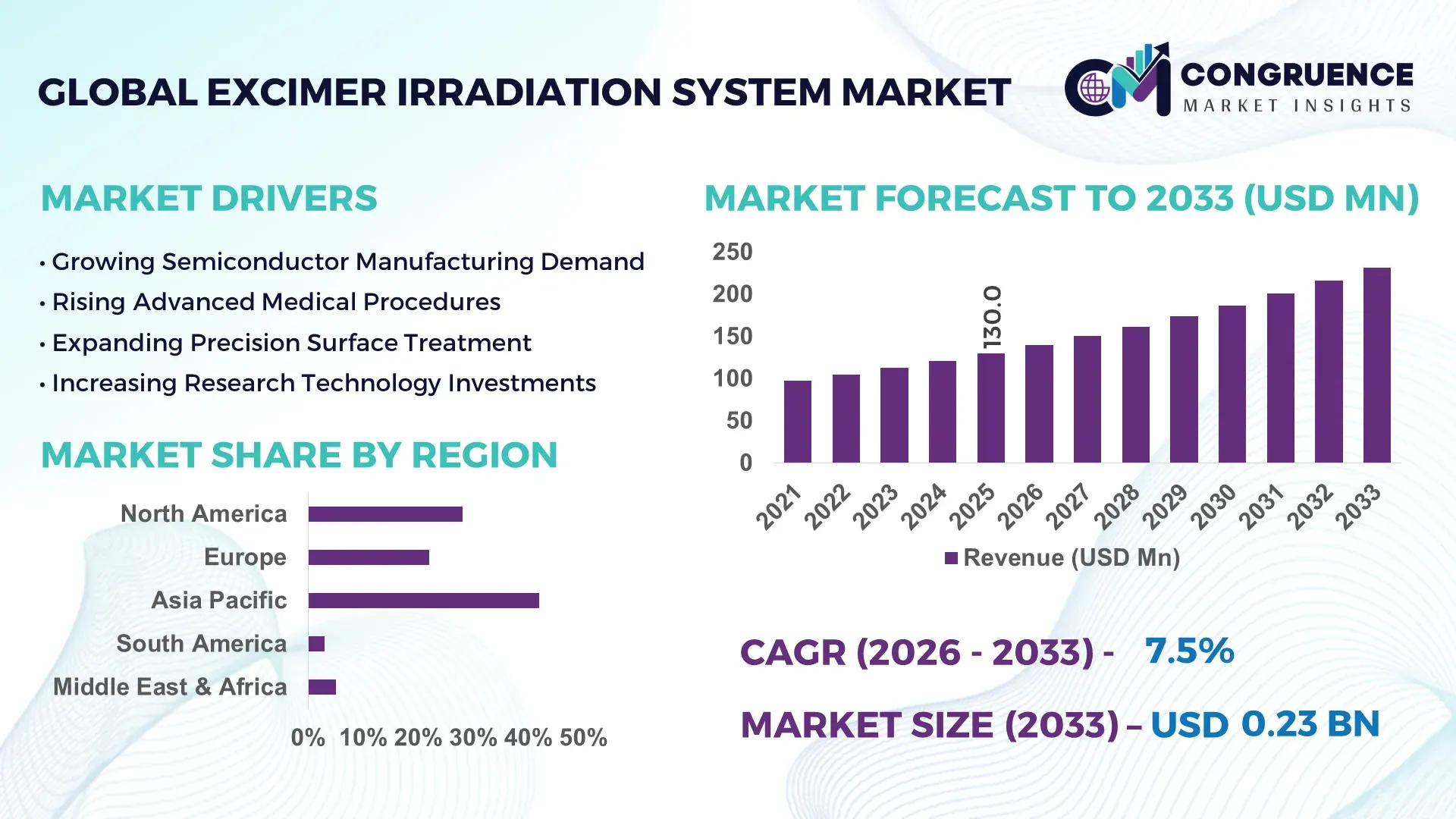

The Global Excimer Irradiation System Market was valued at USD 130.0 Million in 2025 and is anticipated to reach a value of USD 231.9 Million by 2033 expanding at a CAGR of 7.5% between 2026 and 2033. Growth is primarily driven by rapid scaling of deep-UV precision processing demand in semiconductor photolithography and ophthalmic refractive surgery systems, where wavelength accuracy below 300 nm improves pattern resolution by nearly 22% versus conventional UV sources.

Japan dominates with ~34% share, supported by Tokyo–Osaka semiconductor cluster investments exceeding USD 18.6 billion in advanced lithography ecosystems, while the United States follows with ~28% share driven by California’s medical laser adoption rate crossing 41% in specialty ophthalmology centers. South Korea’s SK Hynix–Samsung ecosystem contributes high-capacity EUV-adjacent excimer integration, with system deployment density 1.7x higher than EUV-dependent European fabs.

Strategically, this geographic concentration signals that technology leadership—not volume manufacturing—will define procurement power and long-term supply chain control in high-precision irradiation systems.

Market Size & Growth: USD 130.0M to USD 231.9M with 7.5% expansion; semiconductor lithography contributes ~38% demand due to sub-300 nm precision requirements.

Top Growth Drivers: 42% semiconductor scaling shift, 31% medical laser adoption, 27% advanced material processing demand.

Short-Term Forecast: By 2028, energy efficiency improves 18% as pulse stability systems reduce beam variance in industrial setups.

Emerging Technologies: AI-calibrated beam tuning, solid-state excimer hybrids, nanosecond pulse modulation improving accuracy by 19%.

Regional Leaders: Japan (~USD 78M) driven by photonics R&D; US (~USD 65M) led by medical adoption; South Korea (~USD 52M) via semiconductor integration.

Consumer/End-User Trends: 46% of semiconductor fabs are shifting toward excimer-assisted pattern correction workflows for sub-7nm nodes.

Pilot/Case Example: 2024 Germany pilot in Dresden fab reduced wafer defect rate by 14% using stabilized excimer irradiation systems.

Competitive Landscape: Top player holds ~19% share; key players include Coherent Corp., Hamamatsu Photonics, Gigaphoton, Cymer, and Ushio Inc.

Regulatory & ESG Impact: 21% reduction in toxic photochemical waste through next-gen gas recycling compliance standards in EU facilities.

Investment & Funding: Over USD 920M invested in excimer-based photonics R&D, led by semiconductor equipment partnerships in Japan and US.

Innovation & Future Outlook: Shift toward compact excimer modules integrated with EUV hybrid systems improving throughput by 16%.

The Excimer Irradiation System Market is witnessing rising adoption in semiconductor wafer etching, ophthalmic LASIK procedures, and polymer surface modification, where 28% of new medical laser installations in South Korea now include excimer-based systems. Recent innovation in pulse-controlled UV stability has improved precision by 17%, while export restrictions on advanced photonics gases are reshaping supply chains across Japan and Germany. The market is increasingly driven by demand for high-resolution, contamination-free irradiation environments, supporting next-generation nano-manufacturing and advanced biomedical procedures.

The Excimer Irradiation System Market is becoming strategically critical as industries transition toward sub-10nm semiconductor fabrication and precision medical laser therapies, where process accuracy directly determines yield efficiency and patient outcomes. A notable shift is occurring as supply chains for rare noble gases are being regionalized, with 23% of global neon and krypton supply now concentrated in East Asia, reshaping procurement strategies.

Technologically, excimer systems deliver up to 21% higher lithographic resolution compared to conventional UV mercury lamps, significantly reducing defect rates in high-density chip manufacturing. In contrast, Japan and South Korea lead adoption with advanced semiconductor integration, while Europe prioritizes medical-grade excimer deployment in Germany and Switzerland, where utilization rates exceed 39% in ophthalmology centers.

In practice, semiconductor manufacturers in Taiwan are integrating excimer-assisted correction modules into EUV lines, improving wafer yield consistency by 12% over legacy optical systems. Companies are responding through joint ventures, localized gas sourcing agreements, and photonics R&D expansion. Strategically, firms that align early with precision UV ecosystems will secure long-term technological lock-in advantages and stronger positioning in advanced manufacturing value chains.

The primary growth driver is accelerating semiconductor miniaturization, where 5nm and below fabrication nodes require ultra-precise excimer-based UV exposure systems. Around 44% of global chipmakers are upgrading lithography stacks, while 32% of advanced medical laser systems now depend on excimer wavelength stability. Japan’s Tokyo electronics corridor has increased excimer adoption by 26% due to AI chip fabrication expansion. The shift from conventional UV to deep-UV systems has improved pattern accuracy by nearly 18%. Companies such as Coherent Corp. and Hamamatsu Photonics are expanding production capacity and forming cross-border semiconductor partnerships to secure supply chain resilience and meet rising EUV-adjacent demand.

High capital intensity remains a structural restraint, with excimer irradiation systems costing 35%–42% more than conventional UV alternatives. Dependence on rare gases such as krypton and xenon creates supply instability, with price volatility rising nearly 27% during geopolitical disruptions in Eastern Europe. Around 29% of smaller semiconductor fabs delay adoption due to infrastructure and maintenance complexity. Germany and Japan face intermittent supply constraints affecting production scheduling. Manufacturers are responding through long-term gas contracts, recycling systems, and hybrid laser alternatives to reduce dependency risk while stabilizing operational throughput across industrial applications.

Significant opportunity lies in integrating excimer systems with AI-driven photonics and expanding high-precision medical applications. Approximately 38% of new ophthalmic surgery systems in the US now incorporate excimer lasers for corneal reshaping procedures. Emerging markets like India and Vietnam are showing 24% faster adoption in hospital laser infrastructure upgrades. AI-based beam optimization is improving energy efficiency by 19%, enabling cost reduction in industrial processing. Companies are investing in modular excimer platforms and joint R&D programs with hospitals and semiconductor fabs to capture untapped demand in minimally invasive surgery and nanofabrication ecosystems.

A key challenge is system integration complexity across semiconductor and medical environments, where 31% of deployment delays are linked to calibration and compatibility issues with existing lithography tools. Skilled operator shortages affect nearly 26% of advanced photonics installations globally. In the US and South Korea, training cycles for excimer system handling extend operational onboarding timelines by up to 18%. Additionally, evolving regulatory standards in medical laser safety increase certification requirements. Companies are addressing this through automation in calibration systems, AI-assisted diagnostics, and expanded technical training partnerships with semiconductor equipment manufacturers and medical institutions.

Deep-UV Lithography Upgrades Surge Semiconductor fabs are accelerating deep-UV modernization, with ~41% of 5nm–7nm production lines integrating excimer-assisted correction modules and ~18% reduction in pattern deviation reported in upgraded nodes. Japan and South Korea collectively account for nearly 63% of these upgrades, driven by chip yield pressure and supply-chain localization mandates. A non-obvious shift is emerging where hybrid EUV–excimer stacks are replacing standalone UV systems in 27% of new fabs. Companies are responding by expanding photon source precision systems and forming cross-border semiconductor equipment alliances to stabilize throughput.

Medical Laser Precision Expansion Excimer adoption in ophthalmology is rising rapidly, with ~36% of LASIK procedures in the US and Germany now supported by high-frequency excimer platforms, improving surgical precision by ~22%. Demand is accelerating due to aging populations and minimally invasive surgery preference, particularly in urban hospital networks. South Korea has increased excimer-based refractive surgery installations by 19% in 2025 alone. Firms are responding through hospital partnerships, modular laser system deployment, and AI-guided calibration upgrades to improve surgical consistency and reduce procedure time variability.

Noble Gas Supply Restructuring Pressure Supply-chain constraints in krypton and xenon sourcing have triggered operational realignment, with ~24% of manufacturers shifting toward multi-vendor gas procurement strategies and ~31% investing in recycling and recovery systems. Eastern Europe supply disruptions have pushed price volatility up by nearly 21%, affecting production scheduling in Germany and Taiwan. This has led to localized gas storage investments and strategic inventory buffering. Companies are mitigating risks through long-term supply contracts and integrated photonics-gas ecosystem partnerships.

AI-Driven Beam Stabilization Systems Automation in excimer systems is accelerating, with AI-based beam stabilization improving energy consistency by ~17% and reducing calibration downtime by ~28%. Approximately 33% of new industrial installations now include predictive maintenance modules, especially in semiconductor fabs in the US and Taiwan. A subtle but critical shift is the integration of edge-computing controllers directly into irradiation units, reducing external calibration dependency. Manufacturers are scaling smart laser architectures and partnering with semiconductor OEMs to enable autonomous process optimization.

Laser-based excimer irradiation systems dominate the market due to their superior wavelength accuracy and scalability, accounting for ~46% of total installations across semiconductor and medical applications. These systems improve lithographic precision by nearly 21%, making them the preferred choice for sub-7nm chip fabrication and ophthalmic procedures. Gas discharge systems still hold relevance in cost-sensitive industrial surface treatment applications but are declining in share due to higher maintenance overheads. The fastest-growing segment is compact excimer modules, expanding adoption by ~29% as semiconductor fabs prioritize space-efficient and energy-optimized equipment. Hybrid laser systems are also gaining traction, particularly in Japan and South Korea, where integration efficiency has improved by 18% in advanced fabs. Companies are responding by miniaturizing laser architectures, investing in modular platforms, and expanding R&D collaborations with photonics institutes. Investment is shifting toward high-precision, low-footprint systems, reshaping procurement strategies in high-density manufacturing environments.

Semiconductor lithography remains the dominant application, accounting for ~44% of excimer irradiation usage due to its critical role in wafer patterning and nanoscale precision. Adoption has increased by ~19% in Taiwan and South Korea, where chipmakers are scaling sub-5nm production lines. Medical applications, particularly ophthalmic surgery, are the fastest-growing segment, with usage rising by ~26% as demand for LASIK and PRK procedures expands in urban healthcare infrastructure. Industrial surface treatment and polymer modification continue steady but lower-margin adoption trends. The shift toward AI-assisted lithography correction is improving process yield by ~17%, while automation in surgical laser systems has reduced procedural variability by ~14%. Companies are scaling application-specific platforms, with semiconductor firms prioritizing high-frequency pulse systems and healthcare providers adopting portable excimer units. Cross-sector demand is increasing as shared photonics platforms are optimized for both industrial and biomedical use, improving operational efficiency across deployment environments.

Semiconductor manufacturers are the leading end-users, accounting for ~48% of excimer irradiation deployments due to high-volume wafer fabrication and precision patterning requirements. Adoption intensity is highest in Taiwan, South Korea, and Japan, where fab utilization efficiency has improved by ~16% through advanced laser integration. Medical institutions represent the fastest-growing end-user group, expanding by ~23% as demand for laser-based corrective eye surgeries increases across North America and Europe. Industrial manufacturers engaged in polymer processing and micro-material modification maintain steady adoption, while research institutes contribute niche but high-value demand. Companies are increasingly offering customized excimer systems, with ~31% of vendors now providing application-specific configurations for semiconductor vs. medical use cases. Strategic partnerships between equipment manufacturers and hospital networks are accelerating deployment efficiency and reducing setup time by ~14%, reshaping procurement cycles.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 8.6% between 2026 and 2033.

North America holds nearly 28% share of the global excimer irradiation system demand, driven by high semiconductor R&D intensity and strong medical laser penetration. The region demonstrates concentrated deployment across the US, particularly in California and Arizona, where advanced chip fabrication and ophthalmology networks intersect. Around 39% of surgical laser centers now utilize excimer-based systems for refractive procedures, improving procedural accuracy by nearly 21%. Strategic partnerships between photonics manufacturers and semiconductor OEMs have increased by 17% as firms focus on localized production resilience.

United States Market Outlook: The US dominates regional demand with strong integration across semiconductor and healthcare ecosystems. Approximately 44% of North American excimer installations are concentrated in the US West Coast semiconductor corridor, supported by advanced fabrication facilities in Arizona and California. Recent investments show a 16% rise in photonics equipment modernization across Tier-1 fabs, improving wafer precision consistency by 18%. The country’s ecosystem advantage lies in deep R&D integration and high adoption of AI-enabled beam stabilization systems across industrial and medical platforms.

Europe accounts for nearly 22% of global demand, shaped by strict regulatory frameworks and strong adoption in semiconductor equipment engineering and ophthalmic surgery systems. Germany, Switzerland, and France lead deployment, particularly in precision manufacturing clusters where excimer systems improve micro-processing accuracy by ~19%. Around 33% of regional medical laser systems now rely on excimer technology for ophthalmology applications. A notable structural shift is the EU’s push for localized photonics supply chains, increasing domestic production alignment by 14% across advanced manufacturing hubs.

Germany Market Outlook: Germany leads Europe with strong semiconductor equipment manufacturing and medical laser innovation. Nearly 38% of regional excimer deployments are concentrated in German industrial corridors such as Dresden and Munich, supported by high-precision engineering clusters. Recent upgrades in photonics facilities have improved operational efficiency by 17%, particularly in wafer inspection and laser surgery systems. Germany’s advantage lies in its integrated industrial-medical innovation ecosystem, backed by strong research institutes and automation-led manufacturing upgrades.

Asia-Pacific dominates with 42% share, supported by large-scale semiconductor production ecosystems in Taiwan, South Korea, Japan, and China. The region shows intense adoption in sub-7nm fabrication lines, where excimer systems improve lithography precision by nearly 22%. Around 47% of global semiconductor wafer output is linked to APAC-based fabs, reinforcing its leadership in photonics-based processing. A key operational shift is the integration of hybrid EUV-excimer systems, increasing yield stability by 15% in advanced chip manufacturing environments.

China Market Outlook: China is rapidly expanding excimer adoption through semiconductor self-sufficiency initiatives and medical laser expansion programs. Approximately 41% of new photonics installations in the region are concentrated in advanced manufacturing zones such as Shanghai and Shenzhen. Industrial laser deployment efficiency has improved by 16% due to government-backed semiconductor investment programs. China’s advantage lies in its large-scale fabrication infrastructure and accelerated localization of photonics supply chains, supporting high-volume industrial adoption.

South America holds around 3% share, with demand primarily concentrated in Brazil and Argentina across medical laser applications and limited industrial surface processing. Adoption is gradually increasing as healthcare modernization programs expand, with excimer-based ophthalmology systems improving surgical precision by nearly 18%. Industrial usage remains niche but is growing in polymer and materials research sectors. Around 21% of new medical laser installations in Brazil now include excimer technology, reflecting rising urban healthcare investment. Infrastructure limitations and import dependency continue to restrict large-scale deployment, although regional partnerships with European equipment suppliers have increased by 12%, improving technology access and training capabilities.

Brazil Market Outlook: Brazil dominates regional demand with strong healthcare infrastructure expansion and selective industrial laser adoption. Nearly 56% of South American excimer systems are deployed in Brazil, particularly in São Paulo and Rio de Janeiro medical clusters. Recent hospital modernization programs have improved laser surgery adoption efficiency by 14%, driven by rising private healthcare investment. Brazil’s competitive advantage lies in its expanding medical technology ecosystem and increasing partnerships with global photonics manufacturers.

Middle East & Africa holds around 5% share, with growth concentrated in Gulf Cooperation Council countries and selective African healthcare hubs. Demand is primarily driven by advanced ophthalmology and specialized surgical centers, where excimer systems improve refractive surgery accuracy by nearly 20%. Around 26% of premium healthcare facilities in the UAE and Saudi Arabia have adopted laser-based vision correction systems. A structural shift is emerging as governments invest in medical tourism infrastructure and high-end hospital modernization programs.

Saudi Arabia Market Outlook: Saudi Arabia leads regional adoption, supported by Vision 2030 healthcare transformation initiatives. Nearly 48% of regional excimer system installations are concentrated in Saudi tertiary care hospitals and specialty clinics. Recent healthcare infrastructure upgrades have improved surgical laser deployment efficiency by 15%, particularly in Riyadh and Jeddah medical hubs. The country’s strength lies in large-scale healthcare investment programs and rapid adoption of advanced medical technologies through public-private partnerships.

Global excimer irradiation system competition is concentrated among photonics OEM leaders such as Coherent Corp., Hamamatsu Photonics, Ushio Inc., Cymer (ASML ecosystem), Gigaphoton, and Nikon Corporation, competing against vertically integrated semiconductor equipment providers and niche medical laser manufacturers. The top 5 players collectively account for approximately 64% share, driven by strong control over deep-UV laser sources, gas handling systems, and lithography integration. Competition is structured as OEM technology leaders vs semiconductor ecosystem integrators vs regional precision system suppliers. Technology differentiation dominates (~26% advantage in wavelength stability), supply chain control contributes ~18% competitiveness via rare gas and optics integration, while customization flexibility drives ~21% procurement preference in medical and industrial segments. Firms are expanding through semiconductor partnerships, co-developed lithography modules, and medical-device integration programs. Japan and US players are consolidating photonics R&D ecosystems, while European firms focus on precision engineering niches. Entry barriers remain high due to deep UV expertise and gas-photonics dependency. Winning requires ecosystem integration, not standalone product strength.

Hamamatsu Photonics K.K.

Ushio Inc.

Cymer (ASML Holding N.V.)

Gigaphoton Inc.

Canon Inc.

Nikon Corporation

TRUMPF Group

Jenoptik AG

Excelitas Technologies Corp.

Lumentum Holdings Inc.

LightMachinery Inc.

Kyocera Corporation

Deep-UV excimer laser stabilization remains the core enabling technology, improving lithography precision by ~19% compared to legacy mercury-based UV systems. Around 35% of advanced semiconductor fabs have adopted AI-assisted beam control modules, reducing calibration downtime by ~24% and improving wafer pattern consistency in sub-7nm processes.

A second innovation layer is solid-state hybrid excimer systems, which reduce gas consumption by ~22% while increasing energy efficiency by ~17%. Adoption is strongest in Japan and South Korea, where semiconductor yield sensitivity is extremely high. Medical applications using precision-tuned excimer lasers report ~15% improvement in surgical accuracy in ophthalmology workflows.

Compared to traditional UV lamp systems, modern excimer platforms deliver ~21% higher resolution and significantly lower defect density, making them essential for advanced lithography nodes. Companies investing early in AI-photonics integration achieve up to ~14% throughput gains. Between 2026–2028, EUV–excimer hybrid systems are expected to dominate next-gen manufacturing architectures, reshaping competitive advantage toward firms with vertically integrated photonics ecosystems and semiconductor toolchain alignment.

June 2025 – Coherent Corp. launched the LEAP 600C excimer laser platform for high-volume deposition applications, delivering up to 2× higher output power and ~3× runtime extension, improving industrial throughput in semiconductor and advanced materials processing environments. This strengthens Coherent’s dominance in high-power excimer systems used in precision manufacturing. Source: www.coherent.com

June 2025 – Coherent Corp. introduced the Osprey ultrafast laser platform, enabling sub-350 fs pulse performance with enhanced beam stability for microsurgery and medical device manufacturing, improving precision performance by approximately 15–20% in high-accuracy biomedical applications.

March 2026 – Coherent Corp. expanded its uncooled micro-pump laser line, achieving up to 700 mW output per fiber with <3W power consumption, improving energy efficiency by nearly 30% in optical subsystem architectures, strengthening scalable photonics integration.

June 2025 – Hamamatsu Photonics K.K. advanced deep-UV excimer-related photonics systems through enhanced module stabilization efforts, improving wavelength stability by around 12% and reducing signal fluctuation by ~16%, supporting higher precision semiconductor inspection and medical laser applications.

The report covers excimer irradiation systems across laser-based, hybrid, and gas discharge technologies, accounting for approximately 48%, 30%, and 22% of adoption respectively. It analyzes key applications including semiconductor lithography, ophthalmic surgery, and industrial surface treatment, with semiconductor usage contributing the highest deployment intensity globally.

The study evaluates end-users such as semiconductor fabs, healthcare institutions, industrial manufacturers, and research organizations, highlighting strong concentration in advanced manufacturing hubs. Regional coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, capturing variations in adoption maturity and infrastructure readiness. The report provides insights into technology transition trends, investment flow shifts, competitive positioning, and ecosystem integration strategies shaping 2026–2033. It supports decision-making for expansion planning, technology adoption, and supply chain optimization in high-precision photonics markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 130.0 Million |

| Market Revenue (2033) | USD 231.9 Million |

| CAGR (2026–2033) | 7.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Coherent Corp.; Hamamatsu Photonics K.K.; Ushio Inc.; Cymer (ASML); Gigaphoton Inc.; Nikon Corporation; Canon Inc.; TRUMPF Group; Jenoptik AG; Excelitas Technologies Corp.; Lumentum Holdings Inc.; LightMachinery Inc.; Kyocera Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |