Reports

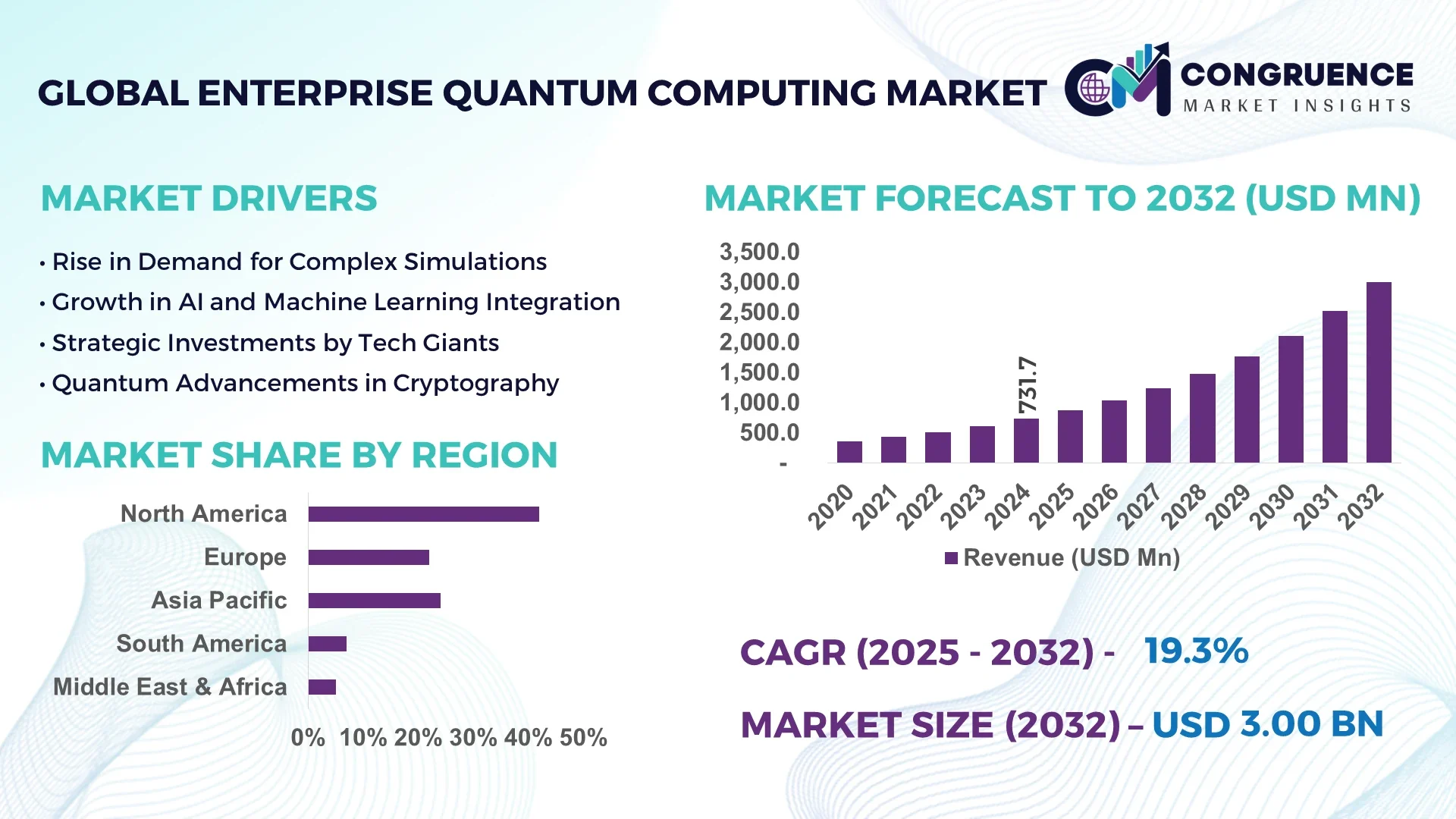

The Global Enterprise Quantum Computing Market was valued at USD 731.66 Million in 2024 and is anticipated to reach a value of USD 3002.18 Million by 2032 expanding at a CAGR of 19.3% between 2025 and 2032.

The United States leads in the Enterprise Quantum Computing Market with substantial production capacity driven by aggressive corporate investments, active R&D consortia, and the deployment of superconducting qubit systems in pharmaceutical modeling, logistics, and financial modeling.

The Enterprise Quantum Computing Market is witnessing a rapid rise in adoption across pharmaceuticals, aerospace, automotive, and advanced materials industries, where quantum algorithms accelerate molecular simulations and complex system optimizations. In financial services, enterprise quantum computing is being deployed for portfolio optimization and risk analysis, reducing computation time drastically while improving modeling precision. Notable technological innovations include error-correction techniques, hybrid quantum-classical workflow integrations, and cloud-based quantum infrastructure accessibility that are democratizing enterprise quantum computing for mid-scale enterprises. Regulatory frameworks supporting research and tax credits are catalyzing additional investments in the market. Additionally, regional consumption is expanding in Germany and Japan, with enterprises leveraging quantum computing for supply chain management and drug discovery, supported by university-industry collaborations. With the increasing availability of quantum-as-a-service models, the market is positioned to witness new trends in algorithm marketplaces, talent development, and sector-specific quantum software advancements targeting business efficiency and resilience.

Artificial Intelligence is transforming the Enterprise Quantum Computing Market by accelerating data-driven modeling, optimization tasks, and algorithm training across sectors requiring high-precision and large-scale computation. AI frameworks are now integrated within enterprise quantum computing workflows to enhance quantum algorithm performance, enabling rapid processing of large datasets in healthcare, finance, and manufacturing while reducing classical pre-processing time. AI-enhanced quantum simulations support drug molecule optimization in the pharmaceutical sector, cutting down R&D cycles and improving cost-efficiency in compound development pipelines.

Within the Enterprise Quantum Computing Market, machine learning models assist quantum error correction, using reinforcement learning to dynamically tune qubits for higher stability, which results in improved operational performance in enterprise environments. AI also enables better scheduling and resource allocation across quantum processors, reducing idle times and increasing computational throughput for businesses utilizing quantum-as-a-service models. Enterprise quantum computing providers are embedding AI capabilities to automate circuit design, reducing complexity in programming quantum systems and allowing domain experts to focus on business-specific problem-solving without the barriers of quantum coding intricacies.

In the automotive sector, the Enterprise Quantum Computing Market benefits from AI-driven quantum algorithms applied to traffic flow optimization and materials simulation for battery advancements. AI’s synergistic role with quantum hardware and hybrid architectures facilitates enterprise-scale simulations of supply chains and manufacturing processes, enhancing operational performance and sustainability tracking. The ongoing integration of AI with quantum computing infrastructure, supported by GPU and QPU co-processing, strengthens process optimization for enterprises aiming to leverage next-generation computation for competitive advantage.

"In April 2025, IBM announced its AI-enhanced quantum workflow system deployed with a European pharmaceutical client, demonstrating a 34% reduction in molecular simulation processing time for drug discovery pipelines using hybrid AI-quantum methods in the enterprise quantum computing market."

The Enterprise Quantum Computing Market is evolving rapidly due to the convergence of advanced quantum algorithms, scalable qubit technologies, and hybrid quantum-classical system developments targeting industrial applications. Enterprises in sectors like pharmaceuticals, automotive, aerospace, and financial services are adopting quantum computing to solve optimization and simulation challenges that are computationally infeasible on classical systems. Investments in cloud-based quantum services are expanding accessibility for mid-sized enterprises, while government-backed quantum initiatives are providing structured frameworks for ecosystem development. The market is also experiencing increased collaboration between universities, quantum startups, and technology corporations, fueling innovation in error correction and quantum software integration, which are critical for scalable deployment in enterprise environments.

The adoption of enterprise quantum computing in drug discovery and financial modeling is a key driver for market growth, supported by measurable advancements in molecular simulation and risk analysis optimization. Quantum computing enables pharmaceutical enterprises to simulate complex molecular structures and protein folding patterns with higher accuracy, reducing the R&D timelines for drug development. In the financial sector, enterprise quantum computing allows real-time risk analysis and portfolio optimization, managing vast datasets with improved computational efficiency. The integration of quantum algorithms into enterprise systems reduces process complexity and enhances operational decision-making, making enterprise quantum computing an essential tool for high-value sectors aiming to improve precision and efficiency in critical workflows.

A significant restraint for the Enterprise Quantum Computing Market is the limited availability of a skilled workforce capable of managing and programming quantum systems within enterprise environments. Despite technological advancements, quantum computing requires specialized expertise in quantum algorithms, error correction methods, and system architecture integration. Enterprises face challenges in developing and retaining talent proficient in quantum programming languages and hybrid quantum-classical workflows, impacting the pace of adoption across industries. This talent gap is further complicated by the evolving nature of quantum technologies, which require continuous upskilling of existing teams and investments in workforce development, limiting the scalability of enterprise quantum computing for some organizations.

The rise of quantum-as-a-service platforms presents a major opportunity within the Enterprise Quantum Computing Market, offering scalable and cost-effective access to quantum hardware and software for businesses of varying sizes. These cloud-based services enable enterprises to test and deploy quantum algorithms without the high upfront investment associated with building dedicated quantum infrastructure. This model is particularly beneficial for sectors like logistics, energy, and advanced manufacturing, where companies can leverage quantum computing for optimization tasks such as supply chain management and predictive maintenance. The increasing availability of quantum-as-a-service is expected to democratize quantum technology, allowing enterprises to experiment, innovate, and integrate quantum solutions into their operations at lower risk and cost.

Hardware stability and high error rates remain persistent challenges in the Enterprise Quantum Computing Market, impacting the reliability of quantum systems for enterprise-scale deployment. Quantum computers are highly sensitive to environmental disturbances, leading to decoherence and computational errors during operations, which limits their effectiveness in running complex enterprise workloads. Although advancements in error correction and fault-tolerant qubit designs are underway, the current hardware limitations restrict the ability of enterprises to fully leverage quantum computing for mission-critical tasks. These challenges necessitate the continuous refinement of hardware systems and the integration of robust error mitigation strategies, which require additional investment and can slow the pace of market adoption for enterprise quantum computing solutions.

• Advancement in Quantum Error Correction Techniques: The Enterprise Quantum Computing market is experiencing a measurable shift with advanced quantum error correction methods reducing operational error rates by up to 30% in enterprise-scale systems. Companies are deploying surface code and cat code techniques in superconducting and trapped ion quantum computers to stabilize qubit operations during long computations. This advancement is enabling extended runtime of quantum algorithms for practical enterprise workloads, particularly in optimization and material simulation, increasing the reliability of quantum results for businesses in pharmaceuticals and aerospace sectors seeking precision modeling.

• Integration of Quantum Computing in Hybrid Cloud Infrastructure: Enterprises are increasingly adopting hybrid cloud infrastructures to leverage quantum computing while maintaining classical computing reliability. Notably, over 40% of enterprises piloting quantum solutions are now using hybrid environments for workflow distribution between quantum processors and classical data centers. This trend is facilitating scalable, real-time problem-solving across industries like finance and logistics, where latency-sensitive quantum tasks can now be executed while maintaining system compatibility, leading to operational efficiency and measurable reductions in computation times for high-complexity workloads.

• Growth in Quantum Algorithm Marketplaces: The rise of quantum algorithm marketplaces is redefining how enterprises access and deploy quantum solutions. These marketplaces enable businesses to purchase or license pre-validated quantum algorithms for use in supply chain optimization, risk modeling, and drug discovery. This trend is increasing adoption among enterprises lacking in-house quantum expertise, fostering rapid testing and deployment of quantum solutions. The availability of industry-specific quantum algorithms in structured marketplaces supports enterprises in shortening development cycles and focusing on measurable results in productivity and accuracy.

• Expansion of Quantum-as-a-Service Adoption: Quantum-as-a-Service (QaaS) offerings are expanding, with enterprises across Europe, North America, and parts of Asia actively subscribing to quantum cloud services for research and operational deployments. This trend has led to a measurable increase in the use of quantum computing for portfolio optimization and material science simulations without requiring dedicated hardware investments. QaaS models are driving accessibility, with enterprises able to conduct pilot programs and refine use cases using real quantum hardware remotely, supporting operational readiness while minimizing capital expenditure.

The Enterprise Quantum Computing market is segmented by type, application, and end-user, reflecting diverse technological developments and adoption patterns. In the type segment, the market includes superconducting qubits, trapped ion qubits, photonic quantum systems, and quantum annealing, with superconducting qubits leading due to stability and scalability in enterprise environments. The application segment covers areas such as simulation, optimization, machine learning, and cryptography, where simulation holds a clear lead driven by pharmaceutical and materials industries requiring high-precision modeling. End-user segmentation highlights sectors including healthcare, automotive, aerospace, and financial services, with healthcare and financial services showing significant traction in operational quantum deployment for drug discovery and portfolio optimization, respectively. These segmentations provide a clear insight into technological and operational shifts within the Enterprise Quantum Computing market.

Superconducting qubits lead the Enterprise Quantum Computing market due to their stability and compatibility with advanced error correction protocols, enabling enterprise applications in logistics and pharmaceuticals. The fastest-growing type is trapped ion quantum systems, driven by their longer coherence times and precision control capabilities, making them attractive for simulation-intensive sectors such as advanced materials and aerospace engineering. Photonic quantum systems, while niche, are gaining relevance due to their low error rates and potential for room-temperature operations, aligning with enterprise sustainability goals and reduced infrastructure dependencies. Quantum annealing remains relevant for optimization-focused industries, offering enterprises an accessible entry point for near-term quantum use cases. This diverse type segmentation illustrates the strategic alignment of enterprise quantum adoption with technological maturity and operational needs.

Simulation stands as the leading application within the Enterprise Quantum Computing market, used extensively for molecular modeling and materials science to reduce R&D cycle times in pharmaceutical and advanced materials sectors. Optimization is the fastest-growing application as enterprises in logistics, finance, and energy sectors leverage quantum computing to refine routing, resource allocation, and risk analysis, supported by measurable efficiency gains. Machine learning within quantum frameworks is also gaining adoption, particularly for data-intensive tasks in healthcare and autonomous systems, aiding pattern recognition and predictive analytics. Cryptography, while currently in pilot stages, remains a critical application area as enterprises anticipate the integration of quantum-safe encryption strategies in preparation for future cybersecurity challenges within enterprise infrastructures.

Healthcare is the leading end-user within the Enterprise Quantum Computing market, using quantum systems for complex molecular simulations and precision drug development, reducing discovery times and enhancing treatment pipelines. The fastest-growing end-user segment is financial services, where enterprises are utilizing quantum computing for portfolio optimization, fraud detection, and risk management, supported by the need for faster and more accurate processing of large datasets in real-time trading environments. The automotive and aerospace sectors are also contributing significantly, adopting quantum computing to optimize materials simulations and streamline design processes for lightweight, high-strength components, aligning with sustainability and efficiency goals within manufacturing operations. These end-user dynamics highlight the growing operational and strategic relevance of enterprise quantum computing across industries focused on advanced simulation and optimization capabilities.

North America accounted for the largest market share at 42% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21.4% between 2025 and 2032.

The Enterprise Quantum Computing Market is witnessing notable traction across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, driven by technological collaborations, industry-specific demand, and government-backed quantum programs. North America leads due to high adoption across financial services and pharmaceutical industries, while Europe sees increased quantum application in automotive and sustainability projects. Asia-Pacific is emerging as a significant hub with advancements in semiconductor fabrication and national quantum mission initiatives, with Japan, China, and India driving volume consumption. South America and the Middle East & Africa are showing growing interest in enterprise quantum computing for energy optimization and infrastructure modeling, supported by regional digitization efforts and industrial diversification programs, indicating multi-regional expansion of the Enterprise Quantum Computing Market.

Pioneering Technology Deployment Driving Advanced Computation Solutions

North America holds a 42% market share within the Enterprise Quantum Computing Market, propelled by high adoption in pharmaceuticals, advanced materials, and financial services industries. Notable regulatory support includes government funding initiatives for quantum computing innovation hubs, ensuring competitive R&D environments across states. Financial institutions are using enterprise quantum computing for real-time portfolio optimization, while pharmaceutical companies integrate quantum simulations for drug discovery pipelines. Digital transformation trends are evident with increasing integration of quantum cloud services across enterprises, aiming to reduce simulation and optimization timelines. Technological advancements include improved qubit stability and hybrid classical-quantum workflows, which are being deployed to enhance operational efficiencies, reinforcing the region’s position as a leader in the Enterprise Quantum Computing Market.

Emerging Advanced Simulation Applications for Industry Transformation

Europe commands a 27% share in the Enterprise Quantum Computing Market, with Germany, the UK, and France as key growth drivers due to their advanced research infrastructure and active participation in cross-border quantum programs. Regulatory bodies in the region are supporting sustainability initiatives and clean energy transitions, encouraging the adoption of quantum computing for material simulations and optimization in the automotive and energy sectors. Enterprises are leveraging emerging quantum technologies for logistics optimization, aligning with digital transformation strategies for operational efficiency. The adoption of quantum cloud-based services is gaining traction, while continuous investments in academic and industrial collaborations are strengthening Europe’s competitive positioning in the enterprise quantum landscape.

Expanding Quantum Infrastructure Enabling Industrial Advancement

Asia-Pacific ranks as the fastest-growing region in the Enterprise Quantum Computing Market, led by top-consuming countries such as China, Japan, and India, where enterprises are increasingly integrating quantum computing into their R&D and operational frameworks. The region is witnessing significant infrastructure investments in semiconductor and quantum processor manufacturing, aligning with national missions on quantum technology advancement. Japan and China are using enterprise quantum computing in pharmaceutical modeling and manufacturing optimization, while India is advancing its quantum initiatives for defense and strategic sectors. Regional tech trends emphasize the development of quantum software ecosystems and emerging innovation hubs, driving increased enterprise-level experimentation with quantum workflows across high-impact industries.

Leveraging Quantum Computing for Industrial and Energy Sector Efficiency

In South America, Brazil and Argentina are key contributors to the Enterprise Quantum Computing Market, with the region showing steady growth driven by industrial and energy sector optimization requirements. The market is benefiting from government incentives supporting digital infrastructure and innovation clusters, promoting enterprise experimentation with quantum computing for advanced materials simulation and energy grid optimization. The region’s enterprises are also exploring quantum computing for logistics and resource allocation modeling to enhance operational efficiency. Trade policies and cross-border technology collaborations are fostering a supportive environment for adopting enterprise quantum computing solutions, creating pathways for broader industrial applications across the continent.

Adoption of Quantum Technologies Supporting Industrial Modernization

The Middle East & Africa region is witnessing increasing demand within the Enterprise Quantum Computing Market, particularly in sectors such as oil & gas, construction, and logistics. Countries including the UAE and South Africa are emerging as major growth hubs, leveraging quantum computing for operational optimization and predictive maintenance in energy and infrastructure projects. Technological modernization trends are evident through investments in smart city initiatives and industrial digitization programs, with enterprises testing quantum applications to reduce operational costs and improve efficiency. Local regulations and trade partnerships are fostering an environment for advanced technology adoption, supporting the regional growth of enterprise quantum computing solutions across high-value sectors.

United States (42%)

High production capacity and strong end-user demand across pharmaceuticals and financial services drive the United States' leadership in the Enterprise Quantum Computing Market.

China (19%)

Strong end-user demand and national quantum initiatives position China as a leading country in the Enterprise Quantum Computing Market, supported by rapid technological advancements and industrial integration.

The Enterprise Quantum Computing market is characterized by a dynamic and rapidly evolving competitive environment, with over 60 active competitors globally focusing on scalable hardware, advanced quantum algorithms, and integrated quantum software solutions for enterprise deployment. Key players are prioritizing strategic initiatives such as technology partnerships, acquisitions, and joint research ventures to strengthen market positioning and accelerate commercialization. For example, alliances between quantum hardware manufacturers and cloud service providers are enhancing the availability of quantum-as-a-service offerings, increasing adoption among enterprises seeking operational optimization and advanced simulation capabilities.

Product launches focusing on superconducting qubits, trapped ion systems, and hybrid quantum-classical workflows are intensifying competition, with companies actively differentiating through improved qubit stability and error correction features. The market is also witnessing an increase in the development of industry-specific quantum applications, such as molecular simulations for pharmaceuticals and portfolio optimization in financial services, indicating a trend toward specialization to capture enterprise customers. Innovation in quantum software frameworks that simplify programming complexity and reduce operational barriers is becoming a critical competitive factor, with players investing in proprietary development and ecosystem-building activities to secure technological leadership within the Enterprise Quantum Computing market.

IBM Corporation

Rigetti Computing

D-Wave Quantum Inc.

IonQ Inc.

Honeywell Quantum Solutions

PsiQuantum

Microsoft Corporation

Google Quantum AI

Alibaba Quantum Laboratory (AQL)

Xanadu Quantum Technologies Inc.

Zapata Computing

Quantinuum

Technological advancements within the Enterprise Quantum Computing Market are centered on scalable qubit systems, quantum error correction, and the integration of hybrid quantum-classical workflows. Superconducting qubits continue to dominate enterprise deployment due to their scalability and compatibility with advanced error correction methods, with systems now achieving error rates below 1% for select gate operations. Trapped ion quantum computers are gaining traction for their longer coherence times and precision control, enabling stable execution of complex algorithms in simulation and optimization applications for enterprises.

Emerging technologies such as photonic quantum computing are being tested within enterprise environments for their room-temperature operation potential, reducing the infrastructural demands associated with cryogenic cooling. Quantum software frameworks are advancing with the introduction of hardware-agnostic quantum programming platforms, simplifying algorithm development for enterprises. Additionally, improvements in hybrid quantum-classical computing architectures are enabling enterprises to distribute computational workloads effectively, using quantum processors for high-complexity segments while leveraging classical systems for less resource-intensive tasks.

Quantum cloud services are expanding, providing enterprises access to multi-qubit systems for testing and operational workflows without significant hardware investments. Quantum-safe cryptography is emerging as a critical application area, with enterprises evaluating integration strategies to protect data in a post-quantum cybersecurity environment. These technological trends position the Enterprise Quantum Computing Market for continued growth and adoption across industries seeking efficiency and advanced computational capabilities.

• In February 2024, IBM unveiled its 1,121-qubit Condor quantum processor, marking a significant milestone for enterprise-scale quantum computing applications, enabling larger and more complex simulations for drug discovery and financial modeling with enhanced stability and lower error rates.

• In April 2024, IonQ announced the deployment of its trapped-ion quantum systems within a European automotive enterprise for advanced battery materials simulation, demonstrating a 25% reduction in simulation time for complex chemical reactions in battery research workflows.

• In September 2023, Quantinuum launched a quantum machine learning toolkit for enterprises, enabling businesses to develop and test quantum-enhanced models for supply chain optimization and predictive maintenance across manufacturing and logistics sectors.

• In November 2023, Google Quantum AI reported the successful implementation of advanced quantum error correction on its Sycamore processor, reducing logical error rates by 15x during enterprise-scale computation trials for financial risk modeling and optimization tasks.

The Enterprise Quantum Computing Market Report provides comprehensive coverage of the technological, industrial, and regional dynamics influencing the market’s evolution. The report analyzes key market segments, including hardware (superconducting qubits, trapped ion systems, photonic quantum computing), software (quantum programming frameworks, simulation platforms), and services (quantum-as-a-service, cloud-based quantum offerings), reflecting the market’s multidimensional structure. The report examines applications within pharmaceuticals, financial services, automotive, aerospace, energy, and advanced materials, where enterprises leverage quantum computing for simulation, optimization, and machine learning tasks. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing numerical insights on consumption patterns, regional technological initiatives, and enterprise adoption rates.

Additionally, the report includes analysis of emerging and niche segments such as quantum-safe cryptography and quantum algorithm marketplaces, providing insights into how enterprises are preparing for post-quantum cybersecurity requirements and accessing validated quantum solutions. The report evaluates technological enablers such as error correction, hybrid quantum-classical workflows, and advances in scalable qubit systems, aligning them with current and projected enterprise use cases. This structured analysis assists decision-makers and industry professionals in understanding the deployment strategies, technological pathways, and operational considerations shaping the enterprise adoption of quantum computing, providing a foundation for strategic planning, investment evaluation, and technology benchmarking within the Enterprise Quantum Computing Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 731.66 Million |

|

Market Revenue in 2032 |

USD 3002.18 Million |

|

CAGR (2025 - 2032) |

19.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM Corporation, Rigetti Computing, D-Wave Quantum Inc., IonQ Inc., Honeywell Quantum Solutions, PsiQuantum, Microsoft Corporation, Google Quantum AI, Alibaba Quantum Laboratory (AQL), Xanadu Quantum Technologies Inc., Zapata Computing, Quantinuum |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |