Reports

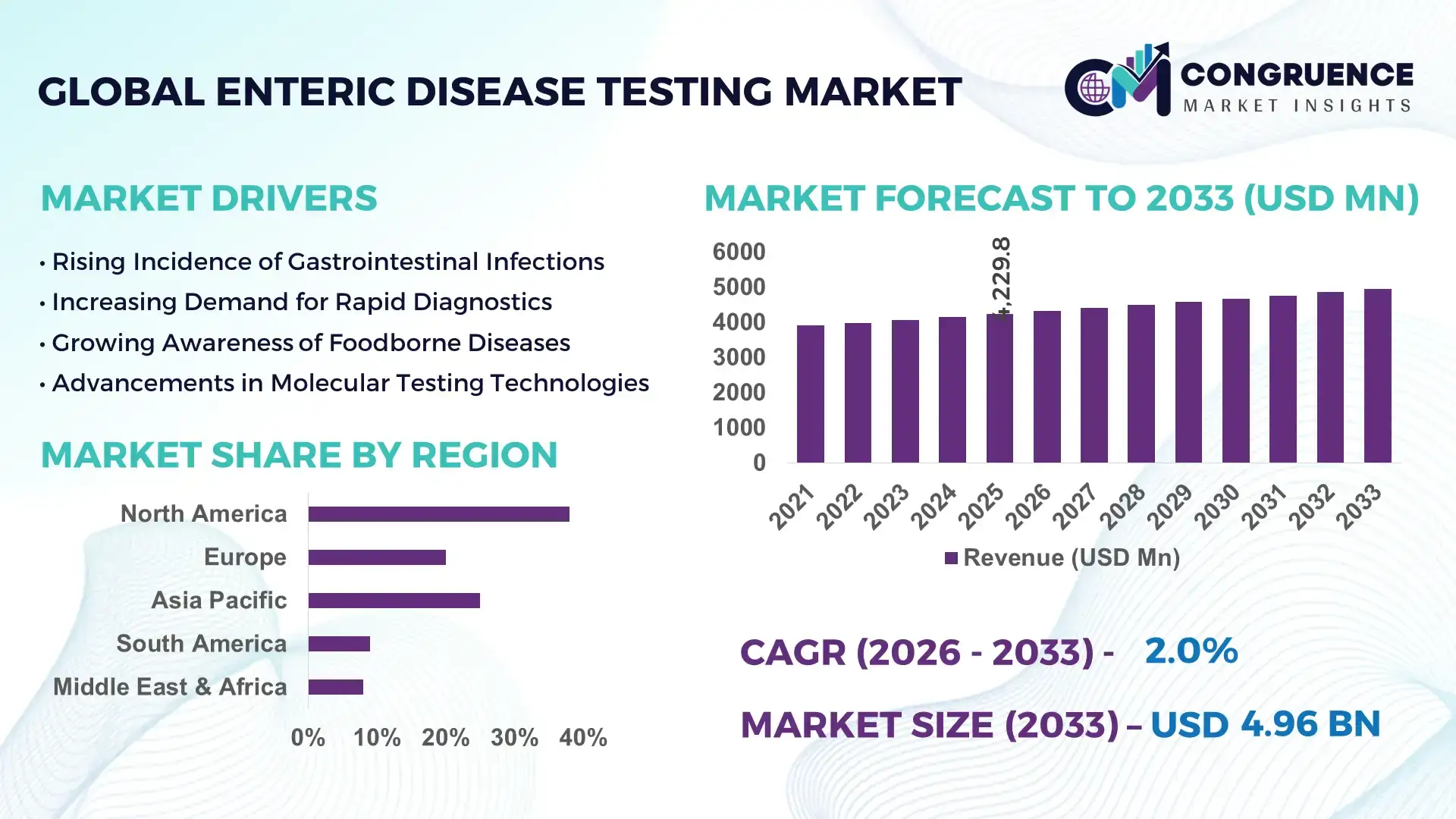

The Global Enteric Disease Testing Market was valued at USD 41286.42 Million in 2025 and is anticipated to reach a value of USD 64329.04 Million by 2033 expanding at a CAGR of 5.7% between 2026 and 2033. Rising prevalence of gastrointestinal infections and increasing demand for rapid diagnostic solutions are key growth drivers.

The United States continues to lead the Enteric Disease Testing market with advanced diagnostic infrastructure, high laboratory testing volumes, and continuous investment in molecular diagnostics. The country performs over 2.5 billion clinical laboratory tests annually, with infectious disease diagnostics accounting for a significant share. More than 70% of large hospitals in the U.S. have adopted multiplex PCR panels for enteric pathogen detection, enabling faster and more accurate results. Additionally, federal and private sector investments exceeding USD 5 billion annually in diagnostic R&D support innovation in next-generation sequencing and point-of-care testing platforms. The widespread adoption of automated laboratory systems and strong integration of digital health technologies further enhance testing efficiency and scalability across clinical and research settings.

Market Size & Growth: Valued at USD 41,286.42 million in 2025, projected to reach USD 64,329.04 million by 2033 at a CAGR of 5.7%, driven by increasing infectious disease burden and rapid diagnostics adoption.

Top Growth Drivers: Multiplex testing adoption (45%), diagnostic accuracy improvement (38%), rising healthcare screening rates (32%).

Short-Term Forecast: By 2028, automated diagnostic systems are expected to improve lab efficiency by 30% and reduce turnaround time by 25%.

Emerging Technologies: Multiplex PCR panels, next-generation sequencing (NGS), and AI-integrated diagnostic platforms.

Regional Leaders: North America projected at USD 21 billion by 2033 with advanced lab automation; Asia-Pacific at USD 18 billion with expanding healthcare access; Europe at USD 14 billion with strong regulatory frameworks.

Consumer/End-User Trends: Hospitals account for over 60% of testing demand, while outpatient diagnostic centers show 20% faster adoption of point-of-care solutions.

Pilot or Case Example: In 2024, a hospital network implemented AI-based diagnostic workflows, achieving a 35% reduction in diagnostic delays.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players including major global diagnostics firms and biotechnology companies.

Regulatory & ESG Impact: Increasing compliance with infection control guidelines and waste reduction protocols is improving diagnostic sustainability by 15%.

Investment & Funding Patterns: Over USD 3 billion invested globally in diagnostic innovation and laboratory automation projects in recent years.

Innovation & Future Outlook: Integration of AI, cloud diagnostics, and portable testing devices is shaping the future of scalable and real-time disease detection.

The Enteric Disease Testing market is characterized by strong contributions from hospital laboratories, which account for over 55% of total testing volumes, followed by diagnostic laboratories and research institutions. Technological advancements such as real-time PCR assays and syndromic testing panels have significantly improved detection rates by over 40% compared to traditional culture methods. Regulatory frameworks promoting early disease detection and infection control are driving adoption across developed and emerging economies. In Asia-Pacific, increasing healthcare expenditure and population-scale screening programs are accelerating consumption patterns, while Europe focuses on stringent quality standards and laboratory accreditation systems. Future growth is expected to be driven by decentralized testing, digital diagnostics integration, and increasing use of portable diagnostic devices in remote healthcare settings.

The Enteric Disease Testing market holds strategic importance in global healthcare systems due to its role in early detection, outbreak control, and disease surveillance. The shift toward rapid, accurate, and multiplex diagnostic solutions is transforming laboratory workflows and improving patient outcomes. Multiplex PCR technology delivers up to 60% faster detection compared to conventional culture-based methods, significantly enhancing clinical decision-making and reducing hospital stay durations.

Regionally, North America dominates in testing volume due to advanced healthcare infrastructure, while Asia-Pacific leads in adoption growth with over 40% of healthcare facilities integrating modern diagnostic platforms. This dual dynamic highlights the global expansion of high-efficiency diagnostic systems across both mature and emerging markets. By 2028, AI-powered diagnostic platforms are expected to improve detection accuracy by 35% while reducing laboratory processing time by nearly 30%. Automation and digital integration are also enabling real-time data sharing, enhancing epidemiological tracking and response capabilities. From a compliance and ESG perspective, firms are committing to reducing diagnostic waste by 20% and improving energy-efficient laboratory operations by 25% by 2030.

In 2024, a leading healthcare system implemented AI-integrated testing workflows, achieving a 32% reduction in diagnostic errors and improving turnaround time by 28%. These measurable outcomes demonstrate the value of technological integration in scaling diagnostic efficiency. As healthcare systems continue to prioritize infection control and precision diagnostics, the Enteric Disease Testing Market is emerging as a critical pillar supporting resilience, regulatory compliance, and sustainable healthcare growth.

The increasing global burden of gastrointestinal infections is a primary driver of the Enteric Disease Testing market. According to global health estimates, diarrheal diseases affect over 1.7 billion cases annually, necessitating rapid and accurate diagnostic interventions. Hospitals and diagnostic centers are expanding their testing capabilities to address rising patient volumes, with multiplex diagnostic panels improving detection efficiency by over 40%. The growing awareness of foodborne illnesses and water contamination has also led to increased screening programs, particularly in urban and semi-urban populations. Furthermore, government-led public health campaigns and mandatory testing protocols in outbreak scenarios are significantly boosting demand for advanced enteric disease diagnostics across healthcare systems.

The high cost associated with advanced diagnostic technologies, including multiplex PCR systems and next-generation sequencing platforms, presents a major restraint for the Enteric Disease Testing market. Initial setup costs for automated laboratory systems can exceed hundreds of thousands of dollars, limiting adoption among small and mid-sized healthcare facilities. Additionally, the cost of consumables and maintenance further increases operational expenses, particularly in low- and middle-income regions. Limited reimbursement policies and budget constraints in public healthcare systems also restrict widespread implementation of high-end diagnostic tools. These financial barriers slow down the transition from traditional methods to advanced testing solutions, affecting overall market penetration.

The rapid expansion of point-of-care (POC) diagnostics presents significant opportunities for the Enteric Disease Testing market. Portable diagnostic devices enable rapid testing in remote and resource-limited settings, improving accessibility and early detection rates. POC testing solutions can deliver results within 30 minutes, reducing dependency on centralized laboratories and enhancing patient management efficiency. Increasing demand for decentralized healthcare services and home-based testing is further driving innovation in compact and user-friendly diagnostic tools. Emerging markets are particularly benefiting from these advancements, with mobile healthcare units and community health programs integrating POC diagnostics to expand coverage and improve disease surveillance capabilities.

Regulatory complexities and stringent quality compliance requirements pose significant challenges for the Enteric Disease Testing market. Diagnostic products must adhere to rigorous validation and approval processes, which can extend development timelines and increase costs. Compliance with international standards for accuracy, sensitivity, and specificity requires continuous investment in quality assurance and testing protocols. Additionally, variations in regulatory frameworks across different regions create barriers for global market entry and product standardization. Laboratories must also maintain accreditation and adhere to strict operational guidelines, which can be resource-intensive. These factors collectively impact the speed of innovation and commercialization within the enteric disease diagnostics industry.

• Expansion of Multiplex Molecular Diagnostics Adoption: Multiplex PCR-based testing is rapidly transforming the Enteric Disease Testing market, with over 65% of advanced diagnostic laboratories integrating syndromic panels capable of detecting 15–25 pathogens simultaneously. These platforms have improved diagnostic accuracy by nearly 45% compared to traditional culture methods while reducing turnaround time from 72 hours to under 6 hours. Adoption is particularly strong in North America and Europe, where over 70% of tertiary care hospitals have transitioned to molecular-based enteric testing workflows to enhance clinical outcomes and infection control efficiency.

• Increasing Penetration of Point-of-Care Testing Solutions: Point-of-care (POC) diagnostic devices are witnessing accelerated deployment, especially in emerging markets, with adoption rates increasing by 35% over the past three years. These compact systems deliver results within 20–40 minutes and are being used in over 50% of rural healthcare centers in parts of Asia-Pacific. The reduction in patient wait time by up to 60% and improved early detection rates by 30% are driving strong demand for decentralized testing solutions across outpatient and emergency care settings.

• Integration of Artificial Intelligence in Diagnostic Workflows: AI-enabled diagnostic platforms are improving testing efficiency and accuracy across laboratories, with implementation rates exceeding 40% in high-volume diagnostic centers. AI algorithms can analyze complex datasets, reducing diagnostic errors by 25% and enhancing pathogen detection sensitivity by up to 35%. Automated reporting systems powered by AI have also reduced manual workload by 30%, allowing laboratories to process up to 20% more samples daily without additional infrastructure investments.

• Growth in Next-Generation Sequencing for Pathogen Identification: Next-generation sequencing (NGS) technologies are gaining traction for comprehensive enteric pathogen profiling, with adoption increasing by 28% annually in research and reference laboratories. NGS enables identification of rare and emerging pathogens with up to 99% accuracy, compared to 70–80% for conventional methods. Additionally, sequencing platforms can process thousands of samples simultaneously, improving throughput by 50% and supporting large-scale epidemiological surveillance programs, particularly in regions with high infectious disease burden.

The Enteric Disease Testing market is segmented by type, application, and end-user, each playing a critical role in shaping overall demand patterns and technological adoption. By type, molecular diagnostics dominate due to their high sensitivity and rapid turnaround capabilities, while immunoassays and culture-based methods continue to serve cost-sensitive and confirmatory testing needs. In terms of application, clinical diagnostics account for the majority of testing volumes, driven by hospital-based screening and outbreak management programs. Food safety and environmental testing are also gaining importance, particularly in regions with strict regulatory frameworks. From an end-user perspective, hospitals and diagnostic laboratories lead in adoption due to high patient inflow and advanced infrastructure, while research institutes and public health agencies contribute significantly to surveillance and epidemiological studies. Increasing demand for accurate, rapid, and scalable testing solutions continues to drive segmentation-based innovation across the market.

The Enteric Disease Testing market by type is primarily segmented into molecular diagnostics, immunoassays, and conventional culture-based methods. Molecular diagnostics currently account for approximately 52% of total adoption due to their superior sensitivity, specificity, and ability to detect multiple pathogens simultaneously. Immunoassays hold around 28% share, offering cost-effective and rapid screening solutions, especially in low-resource settings. However, adoption in molecular diagnostics is rising fastest, expanding at an estimated 8.5% CAGR, driven by increasing demand for rapid and accurate diagnostics in clinical settings.

Conventional culture-based testing methods, while gradually declining in preference, still contribute nearly 20% of total usage due to their role in confirmatory diagnostics and antimicrobial susceptibility testing. These methods remain relevant in regulatory and research environments where pathogen isolation is essential.

By application, clinical diagnostics dominate the Enteric Disease Testing market, accounting for approximately 60% of total usage due to high patient volumes and increasing prevalence of gastrointestinal infections. Food safety testing represents around 22% of the market, driven by stringent regulations and growing awareness of foodborne illnesses. Environmental testing contributes nearly 18%, focusing on water quality monitoring and contamination detection. However, adoption in food safety applications is growing fastest, with an estimated CAGR of 7.9%, supported by increasing global trade and regulatory compliance requirements.

Clinical diagnostics continue to benefit from advancements in rapid testing technologies, enabling faster patient management and infection control. Food safety testing is gaining traction as governments enforce stricter quality standards, while environmental monitoring is expanding due to rising concerns over waterborne diseases.

Hospitals represent the leading end-user segment in the Enteric Disease Testing market, accounting for approximately 58% of total adoption due to high patient throughput and access to advanced diagnostic infrastructure. Diagnostic laboratories follow with around 30% share, providing specialized testing services and supporting large-scale screening programs. Research institutes and public health organizations collectively contribute nearly 12%, focusing on surveillance and epidemiological studies. However, diagnostic laboratories are the fastest-growing segment, expanding at an estimated CAGR of 7.5%, driven by increasing outsourcing of testing services and rising demand for specialized diagnostics.

Hospitals benefit from integrated diagnostic systems that enable rapid testing and immediate clinical decision-making, while diagnostic laboratories are expanding capacity through automation and digital integration. Research institutions play a critical role in advancing testing methodologies and monitoring disease patterns.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America processed over 900 million diagnostic tests annually, supported by advanced laboratory infrastructure and high healthcare spending. Europe followed with a 27% share, driven by strict regulatory frameworks and over 65% adoption of molecular diagnostic technologies in clinical laboratories. Asia-Pacific held approximately 24% share, with more than 50% of new diagnostic facilities being established in urban healthcare centers across China and India. South America and the Middle East & Africa collectively contributed around 11%, with improving diagnostic accessibility and rising public health initiatives. Increasing government investments, expanding diagnostic networks, and adoption of rapid testing technologies are driving regional diversification and strengthening global market penetration.

How is advanced diagnostic infrastructure transforming testing efficiency and adoption rates?

North America holds approximately 38% share of the Enteric Disease Testing market, supported by highly developed healthcare systems and widespread adoption of advanced diagnostic technologies. The region performs over 900 million clinical tests annually, with infectious disease diagnostics accounting for nearly 20% of total testing volume. Key industries driving demand include hospital networks, diagnostic laboratories, and public health agencies, all of which rely on rapid and accurate testing solutions. Regulatory frameworks emphasize strict quality standards and infection control protocols, leading to over 70% adoption of molecular diagnostic platforms in tertiary care centers. Technological advancements such as AI-based diagnostics and automated laboratory systems have improved efficiency by 30% and reduced diagnostic turnaround time by 25%. A leading diagnostics company in the region has implemented multiplex PCR platforms across more than 500 healthcare facilities, improving pathogen detection rates by 40%. Consumer behavior reflects high reliance on hospital-based testing and growing demand for same-day diagnostic results.

What factors are accelerating precision diagnostics and regulatory-driven adoption trends?

Europe accounts for approximately 27% of the Enteric Disease Testing market, with key markets including Germany, the United Kingdom, and France contributing significantly to testing volumes. The region processes over 600 million diagnostic tests annually, with molecular diagnostics adoption exceeding 65% in advanced laboratories. Regulatory bodies enforce strict compliance standards, leading to increased demand for high-accuracy diagnostic solutions and standardized laboratory practices. Sustainability initiatives are also influencing market dynamics, with over 40% of laboratories implementing eco-friendly diagnostic processes and waste reduction measures. Emerging technologies such as next-generation sequencing and digital pathology platforms are gaining traction, improving detection accuracy by up to 35%. A major European diagnostics provider has expanded its automated testing systems across 300 laboratories, increasing sample processing capacity by 25%. Consumer behavior in the region is influenced by regulatory pressure, driving demand for reliable, traceable, and high-quality diagnostic outcomes.

Why is rapid healthcare expansion driving large-scale diagnostic adoption and innovation?

Asia-Pacific ranks as the fastest-growing region in the Enteric Disease Testing market, accounting for approximately 24% of global demand and processing over 700 million tests annually. Major consuming countries include China, India, and Japan, where increasing population density and rising incidence of infectious diseases are driving demand for diagnostic services. Infrastructure expansion is significant, with more than 50% of new diagnostic laboratories being established in urban areas over the past five years. The region is also emerging as a manufacturing hub for diagnostic equipment, contributing to cost-effective production and wider accessibility. Technological trends include the rapid adoption of point-of-care testing devices and mobile diagnostic platforms, improving detection rates by 30% in remote areas. A regional diagnostics company has deployed portable testing kits across 1,000 rural healthcare centers, increasing testing coverage by 40%. Consumer behavior reflects growing awareness of early disease detection and increasing reliance on affordable diagnostic solutions.

How are healthcare investments and policy reforms improving diagnostic accessibility?

South America holds approximately 6% share of the Enteric Disease Testing market, with Brazil and Argentina serving as the primary contributors to regional demand. The region conducts over 150 million diagnostic tests annually, with increasing investment in healthcare infrastructure supporting market expansion. Government incentives aimed at improving public health systems have led to a 20% increase in diagnostic facility development over recent years. Trade policies and regional collaborations are facilitating the import of advanced diagnostic technologies, enhancing testing capabilities. A local healthcare provider has expanded its diagnostic network by 15%, improving access to testing services in underserved areas. Infrastructure improvements and public health initiatives are driving adoption of modern diagnostic tools. Consumer behavior in the region shows growing reliance on public healthcare systems, with increasing demand for cost-effective and accessible testing solutions.

What role does healthcare modernization play in expanding diagnostic capabilities?

The Middle East & Africa region accounts for approximately 5% of the Enteric Disease Testing market, with key growth countries including the United Arab Emirates and South Africa. The region processes over 120 million diagnostic tests annually, with increasing investments in healthcare infrastructure supporting market development. Technological modernization trends include the adoption of automated laboratory systems and digital diagnostic platforms, improving testing efficiency by 25%. Government initiatives and trade partnerships are facilitating the expansion of diagnostic services and access to advanced technologies. A regional healthcare provider has implemented digital diagnostic systems across 100 facilities, enhancing testing capacity by 30%. Demand trends are influenced by rising awareness of infectious diseases and increasing healthcare spending. Consumer behavior reflects a gradual shift toward private healthcare services and growing adoption of advanced diagnostic solutions.

United States – 34% share, driven by advanced diagnostic infrastructure, high testing volumes, and continuous investment in molecular diagnostics.

China – 18% share, supported by large population base, expanding healthcare infrastructure, and increasing adoption of rapid diagnostic technologies.

The Enteric Disease Testing market is moderately fragmented, with over 120 active global and regional competitors operating across molecular diagnostics, immunoassays, and culture-based testing segments. The top five companies collectively account for approximately 42% of the total market, reflecting a competitive environment characterized by continuous innovation and strategic expansion. Leading players are focusing on product development, with more than 60 new diagnostic platforms introduced globally over the past three years. Strategic partnerships and collaborations have increased by 25%, enabling companies to expand their technological capabilities and geographic reach.

Mergers and acquisitions remain a key growth strategy, with over 15 major deals completed in the last two years to strengthen product portfolios and market positioning. Companies are also investing heavily in research and development, with annual R&D spending exceeding 12% of total operational budgets for leading firms. Innovation trends include the integration of artificial intelligence, cloud-based diagnostics, and portable testing devices, improving diagnostic accuracy by up to 35% and reducing processing time by 30%. Competitive differentiation is increasingly driven by speed, accuracy, and scalability of diagnostic solutions, positioning the market for sustained technological advancement and intensified competition.

Abbott Laboratories

Thermo Fisher Scientific Inc.

Bio-Rad Laboratories Inc.

Becton, Dickinson and Company

QIAGEN N.V.

bioMérieux S.A.

Danaher Corporation

Hologic Inc.

Meridian Bioscience Inc.

Luminex Corporation

Cepheid Inc.

DiaSorin S.p.A.

Technological advancements are fundamentally reshaping the Enteric Disease Testing market, with a strong shift toward rapid, high-throughput, and precision diagnostic solutions. Multiplex polymerase chain reaction (PCR) platforms are now widely adopted, enabling simultaneous detection of 15–25 enteric pathogens in a single test, improving diagnostic efficiency by nearly 45% compared to traditional culture-based techniques. These systems reduce turnaround time from 48–72 hours to under 6 hours, significantly enhancing clinical decision-making and patient management.

Next-generation sequencing (NGS) technologies are gaining prominence, particularly in reference laboratories and research institutions, where they enable comprehensive pathogen identification with up to 99% accuracy. NGS platforms can process thousands of samples per run, increasing throughput by over 50% and supporting large-scale epidemiological surveillance. Additionally, real-time PCR systems integrated with automated sample preparation workflows are improving laboratory productivity by approximately 30%, reducing manual errors and operational costs.

Artificial intelligence and machine learning are increasingly integrated into diagnostic workflows, with over 40% of advanced laboratories deploying AI-enabled data analysis tools. These systems enhance detection sensitivity by up to 35% and reduce diagnostic errors by 25%. Digital pathology and cloud-based reporting systems are also enabling real-time data sharing, improving collaboration across healthcare networks and accelerating outbreak response times by nearly 20%.

Emerging technologies such as microfluidics-based lab-on-chip devices and biosensors are further driving innovation, offering portable and point-of-care solutions capable of delivering results within 20–30 minutes. These compact systems are particularly valuable in remote and resource-limited settings, where they improve testing accessibility by over 40%. The integration of automation, AI, and portable diagnostics is positioning the market for scalable, efficient, and data-driven diagnostic ecosystems.

• In February 2025, Thermo Fisher Scientific expanded its gastrointestinal pathogen testing portfolio by enhancing its multiplex PCR panels to detect over 20 pathogens in a single run, improving diagnostic turnaround time by 30% and increasing laboratory throughput efficiency across clinical settings. Source: www.thermofisher.com

• In October 2024, bioMérieux announced updates to its BIOFIRE® FILMARRAY® Gastrointestinal Panel, improving detection sensitivity for bacterial and viral pathogens and reducing result delivery time to approximately 1 hour, supporting faster clinical decision-making in hospital environments. Source: www.biomerieux.com

• In March 2025, QIAGEN introduced an advanced syndromic testing solution integrating automated sample preparation with real-time PCR, enabling up to 25% higher processing capacity and reducing manual intervention in high-volume diagnostic laboratories. Source: www.qiagen.com

• In August 2024, Abbott Laboratories expanded its molecular diagnostics capabilities by deploying upgraded Alinity m systems across multiple healthcare facilities, enhancing testing accuracy by 20% and enabling scalable infectious disease testing, including enteric pathogens, in decentralized laboratory networks. Source: www.abbott.com

The Enteric Disease Testing Market Report provides a comprehensive analysis of diagnostic technologies, product segments, application areas, and geographic trends shaping the industry. The report covers key testing methodologies, including molecular diagnostics, immunoassays, and conventional culture-based techniques, with molecular testing accounting for over 50% of total diagnostic adoption due to its superior accuracy and rapid results. It also evaluates emerging technologies such as next-generation sequencing, microfluidics, and AI-integrated diagnostic platforms, which are improving detection rates by up to 35% and increasing laboratory throughput by 30%.

From an application perspective, the report examines clinical diagnostics, food safety testing, and environmental monitoring, with clinical applications representing approximately 60% of total testing demand. It further explores the role of decentralized and point-of-care diagnostics, which have expanded testing accessibility by over 40% in remote and underserved regions. End-user analysis includes hospitals, diagnostic laboratories, research institutions, and public health agencies, with hospitals accounting for nearly 58% of total testing volume due to high patient inflow and advanced infrastructure.

Geographically, the report provides detailed insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional testing volumes exceeding 900 million annually in developed markets and rapid infrastructure expansion in emerging economies. The scope also includes regulatory frameworks, quality standards, and digital transformation trends influencing market adoption. Additionally, the report addresses niche segments such as portable diagnostic devices and home-based testing solutions, which are gaining traction with adoption rates increasing by over 30% in recent years.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Abbott Laboratories, Thermo Fisher Scientific Inc., Bio-Rad Laboratories Inc., Becton, Dickinson and Company, QIAGEN N.V., bioMérieux S.A., Danaher Corporation, Hologic Inc., Meridian Bioscience Inc., Luminex Corporation, Cepheid Inc., DiaSorin S.p.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |