Reports

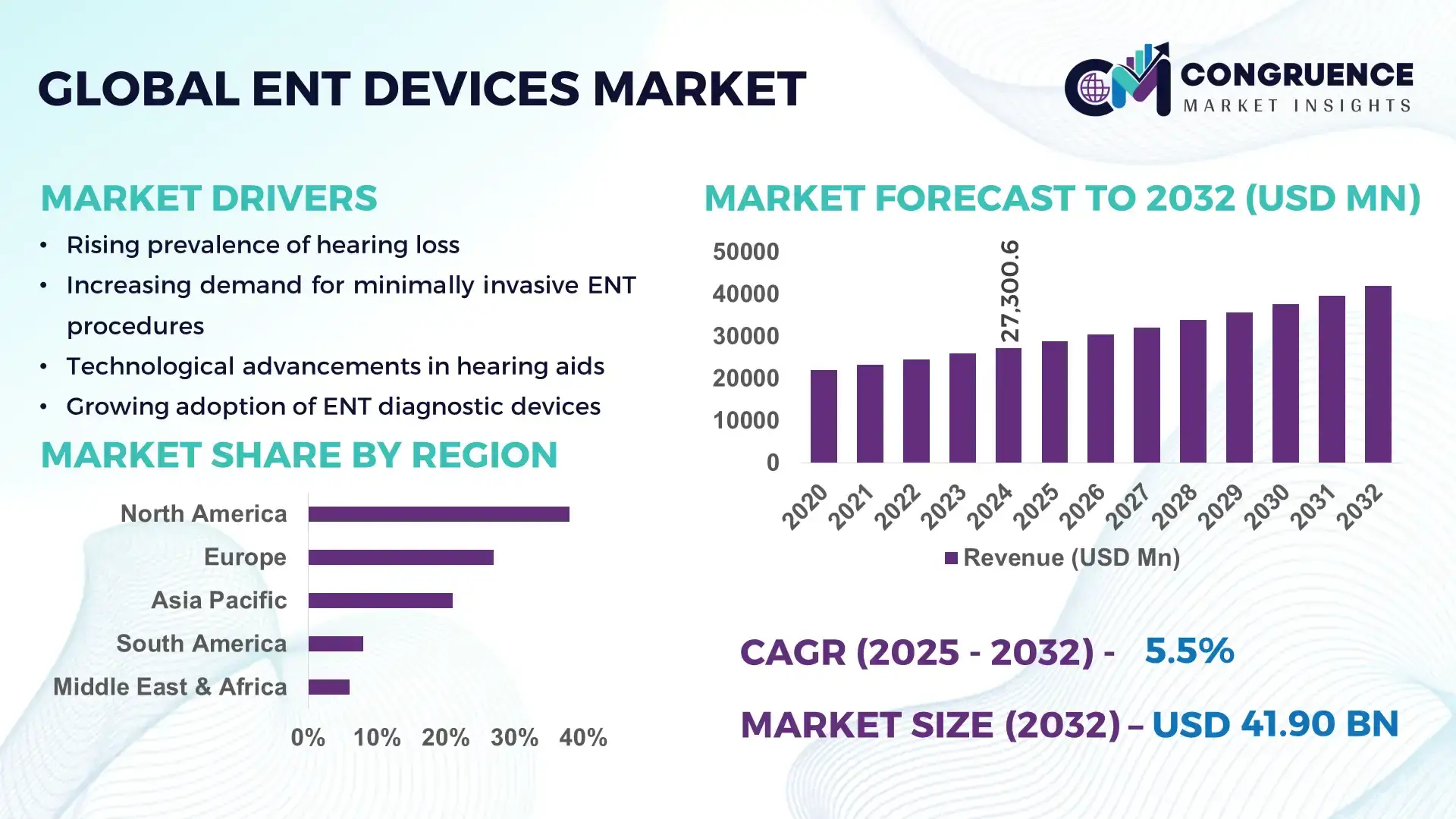

The Global ENT Devices Market was valued at USD 27,300.6 Million in 2024 and is anticipated to reach a value of USD 41,897.9 Million by 2032 expanding at a CAGR of 5.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is driven by rising prevalence of ENT disorders and increasing adoption of minimally invasive ENT procedures worldwide.

The United States, as the dominant country in this space, supports the global ENT Devices Market with over 90% of its regional share of ENT devices demand in 2024, reflecting massive production capacity, advanced regulatory approvals, and high investments in R&D. The U.S. leads in hearing aid manufacturing, diagnostic endoscope production, and deployment of surgical ENT instruments, with hospitals and clinics upgrading diagnostics and treatment technologies rapidly, driving adoption of advanced ENT devices across diagnostic, surgical, and hearing‑care applications.

Market Size & Growth: Current market value USD 27.3 Billion (2024), projected value USD 41.9 Billion by 2032, with 5.5% CAGR — driven by rising ENT disorder prevalence and growth in minimally invasive procedures.

Top Growth Drivers: 42% increase in geriatric population, 38% rise in hearing impairment cases, 33% growth in minimally invasive ENT surgeries.

Short-Term Forecast: By 2028, procedural efficiency in ENT diagnostics expected to improve by 24%, reducing patient waiting times.

Emerging Technologies: AI‑enhanced diagnostic endoscopes, wireless hearing aids, advanced laser‑based sinus and throat surgical tools.

Regional Leaders: North America (~USD 15 Billion by 2032) — strong institutional healthcare infrastructure; Europe (~USD 9 Billion by 2032) — aging population driving demand; Asia Pacific (~USD 11.5 Billion by 2032) — rapid healthcare expansion and rising middle-class adoption.

Consumer/End-User Trends: Growth in outpatient ENT clinics and ambulatory centers; rising preference for home‑care hearing devices and minimally invasive treatment options.

Pilot or Case Example: In 2025, a major U.S. hospital network deployed AI-enabled diagnostic ENT endoscopes, reducing diagnostic errors by 28%.

Competitive Landscape: Market leader holds approx. 18–22% share; major competitors include 4–5 global firms specializing in hearing aids, implants, diagnostic and surgical equipment.

Regulatory & ESG Impact: Stricter medical safety standards and sustainable manufacturing practices are increasing demand for energy-efficient, sterilizable ENT devices.

Investment & Funding Patterns: Recent global investments exceeding USD 1.2 billion in R&D and production infrastructure for advanced ENT diagnostics and hearing solutions.

Innovation & Future Outlook: Integration of IoT-enabled hearing aids, AI‑driven diagnostics, and minimally invasive surgery kits expected to shape the next generation of ENT care.

The market is also witnessing rapid growth in hearing aids, implants, diagnostic endoscopes, and laser-based surgical tools, supported by rising demand from hospital, clinic, and outpatient settings. Technological innovation, regulatory compliance, and expansion in emerging regions are strengthening the future outlook for ENT devices globally.

The ENT Devices Market occupies a strategic position in global healthcare infrastructure due to rising incidence of hearing loss, chronic sinusitis, and throat disorders—especially among aging populations—and increasing demand for minimally invasive diagnostics and treatment. As patient expectations for faster recovery and precision-based care rise, advanced ENT technologies become critical to maintaining high standards of care and expanding access. For providers, adopting next-generation ENT systems delivers measurable improvements in diagnostic accuracy, surgical precision, and overall operational efficiency, offering a competitive advantage.

The rapid evolution of AI‑enhanced diagnostic tools delivers up to 30% higher detection accuracy compared to traditional rigid endoscopes, enabling earlier intervention and reducing misdiagnosis. Regionally, North America leads in volume, driven by well‑developed healthcare infrastructure and robust reimbursement frameworks, while Asia‑Pacific leads in growth potential, with increasing healthcare spending and rising geriatric population driving adoption across clinics and hospitals. By 2027, integration of AI‑powered hearing aids and IoT‑enabled devices is expected to improve patient follow-up compliance by 25% and reduce device rejection rates by 18%.

From an ESG and compliance perspective, manufacturers are committing to 30–40% reductions in device lifecycle waste and enhanced sterilization standards by 2030, aligning with global healthcare sustainability goals. In 2025, a leading manufacturer in the U.S. implemented a digital traceability system for hearing implants, reducing product recall incidents by 22%.

Looking forward, the ENT Devices Market is poised to become a pillar of resilient, technology-driven, and sustainable healthcare delivery, enabling improved patient outcomes, global accessibility, and cost-efficient ENT care models worldwide.

The ENT Devices Market dynamics are shaped by technological innovation, demographic pressure, shifting disease prevalence, and evolving healthcare infrastructure. Expansion of geriatric population and rising incidence of hearing loss, sinus and throat disorders create sustained demand for diagnostic, surgical, and hearing solutions. Growing preference for minimally invasive procedures, outpatient care, and home-based hearing aids is reshaping demand patterns. Meanwhile, rising regulatory and safety standards push manufacturers toward advanced, quality-controlled device development. Additionally, increasing penetration of digital health, tele-audiology, and remote diagnostics is influencing how ENT providers select their equipment portfolios. The market dynamics reflect a shift from volume-based device procurement to value‑based, outcome‑driven ENT care, demanding innovation, quality, and patient-centric solutions.

Increasing global life expectancy and rising proportion of geriatric population directly elevate the prevalence of hearing impairment, chronic sinusitis, and other ENT disorders. Older adults are more susceptible to age‑related auditory decline, requiring diagnostic hearing assessments, hearing aids, and ENT surgeries. As the number of elderly individuals grows, demand for both diagnostic ENT devices and hearing solutions escalates. This demographic trend, combined with higher awareness and increased screening initiatives, is exerting strong upward pressure on market demand, particularly in regions with aging populations.

Strict regulatory approval processes, high compliance costs, and complex reimbursement frameworks in certain countries restrict rapid adoption of advanced ENT devices. Smaller healthcare facilities and clinics may lack resources to navigate regulatory requirements or afford the high upfront cost of sophisticated diagnostic or surgical ENT systems. Additionally, inconsistent insurance reimbursement policies for hearing aids and implants can deter patients from opting for advanced solutions. These structural and financial barriers slow down market penetration and limit growth in underdeveloped or cost-sensitive regions.

Expanding tele‑audiology services, remote diagnostics, and mobile hearing assessment apps open new distribution and adoption channels for ENT devices. As more patients in rural or under‑served areas access remote ENT consultations, demand for portable diagnostic devices, compact hearing aids, and connected ENT equipment increases. This trend offers manufacturers the opportunity to develop portable, cost‑effective ENT devices and establish service‑enabled business models tailored to remote care. Widening digital healthcare access and growing telemedicine acceptance globally amplify this potential.

Advanced ENT devices—such as endoscopes, implants, and surgical tools—require trained ENT specialists and support technicians. In many emerging and rural markets, a shortage of qualified professionals and insufficient training infrastructure limits effective deployment and maintenance of sophisticated ENT equipment. This skill gap can result in underutilization, misdiagnosis, or suboptimal outcomes, deterring hospitals from investing in high-end ENT devices. Overcoming this challenge requires enhanced training programs, certification standards, and ongoing education initiatives.

Surge in AI‑Enabled Diagnostic and Surgical ENT Tools: The adoption of AI‑assisted endoscopy and diagnostic imaging systems has increased by more than 28% in 2024, enabling improved accuracy and earlier detection of ENT disorders, particularly among geriatric patients. Hospitals and clinics increasingly invest in AI‑enhanced visualization and navigation systems to support precision ENT surgeries and diagnostics, boosting procedural efficiency and reducing error rates.

Growing Preference for Wireless Hearing Aids and Implantable Solutions: Wireless and rechargeable hearing aids now account for over 45% of new hearing‑care device purchases globally, reflecting rising consumer demand for portability, comfort, and ease of use. Implantable hearing solutions and cochlear‑implant devices are witnessing increasing adoption in emerging markets as awareness grows and access improves.

Expansion of Outpatient and Ambulatory ENT Care Settings: More than 37% of ENT procedures in 2024 were conducted in outpatient clinics or ambulatory surgery centers rather than traditional hospitals. This shift is driving demand for compact, portable diagnostic tools and minimally invasive surgical devices tailored for outpatient workflows.

Rising Demand from Emerging Markets in Asia‑Pacific and Latin America: Asia‑Pacific and Latin America saw a combined year‑on‑year increase in ENT device adoption of approximately 22% in 2024, driven by growing healthcare infrastructure investment, increasing medical device import volumes, and heightened awareness of ENT disorders. These regions are becoming significant growth engines for hearing‑care and diagnostic device manufacturers worldwide.

The Global ENT Devices Market is broadly segmented by type, application, and end-user. By type, the market includes diagnostic devices, surgical instruments, hearing aids, and implantable devices, each serving specialized needs across otology, rhinology, and laryngology. By application, the market spans hearing care, diagnostics, and ENT surgeries, reflecting evolving patient demands and clinical advancements. End-user segmentation highlights hospitals, outpatient clinics, diagnostic centers, and home healthcare users as key consumers, with varying adoption rates and preferences shaped by regional healthcare infrastructure, reimbursement policies, and demographic trends. This segmentation allows for targeted strategies by manufacturers, investors, and healthcare providers, ensuring that devices are optimized for clinical outcomes, patient compliance, and operational efficiency.

Diagnostic devices lead the ENT Devices Market, accounting for approximately 38% of global adoption due to increasing demand for early detection of hearing and sinus disorders. Hearing aids follow closely, with 30% adoption, driven by the rising incidence of age-related hearing loss and technological advancements such as wireless connectivity and AI-based sound processing. Surgical instruments contribute around 20%, serving ENT surgeries in hospitals and specialized clinics. Implantable devices, including cochlear implants and bone-anchored hearing systems, constitute the remaining 12%, targeting niche patients with severe auditory impairments. The fastest-growing segment is wireless hearing aids, propelled by patient preference for portability and integration with smart devices.

Hearing care represents the largest application segment, accounting for 40% of device usage globally, reflecting rising age-related hearing impairment and awareness campaigns. ENT diagnostics follow with 35%, as hospitals and clinics increasingly implement advanced imaging and endoscopic devices for early detection of sinus, throat, and auditory conditions. ENT surgeries account for 15%, supported by minimally invasive procedures and robotic-assisted interventions, while the remaining 10% covers specialized applications such as research, telemedicine, and mobile hearing services. In 2024, over 42% of U.S. hospitals deployed AI-assisted ENT diagnostic tools, reducing misdiagnoses and procedural errors.

Hospitals constitute the leading end-user segment, with 50% of the market, due to their high procedural volumes and investments in advanced ENT diagnostic and surgical devices. Outpatient clinics and specialized ENT centers account for 28%, driven by patient preference for minimally invasive procedures and ambulatory care. Home healthcare users contribute around 12%, largely in hearing aid adoption and tele-audiology applications, while the remaining 10% includes diagnostic labs, research facilities, and rehabilitation centers. In 2024, 38% of outpatient clinics globally reported piloting AI-based ENT diagnostic devices to enhance accuracy and reduce patient wait times.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2025 and 2032.

North America leads with over 10,400 units of ENT devices sold in hospitals and clinics, while Europe follows at 8,200 units, and Asia-Pacific recorded 7,500 units. Hospitals and outpatient clinics collectively consume more than 60% of devices in North America. In Asia-Pacific, China and India alone account for over 5,000 units, with rapid adoption of tele-audiology and mobile hearing solutions. South America and Middle East & Africa collectively contribute 14% of total consumption, reflecting emerging healthcare infrastructure investments. Increasing awareness of ENT disorders, expansion of diagnostic centers, and modernization of surgical instruments are driving device uptake across all regions.

North America holds approximately 38% of the global ENT devices market, with hospitals and outpatient clinics leading demand. Key industries driving growth include healthcare, research centers, and rehabilitation facilities. Regulatory support from the FDA and reimbursement policies have improved access to hearing aids and diagnostic devices. Technological advancements include AI-assisted diagnostics, robotic-assisted surgeries, and wireless hearing aids. Local player Cochlear Americas expanded its tele-audiology services in 2024, enabling over 150 clinics to remotely monitor patient hearing outcomes. North American consumers show higher adoption in healthcare and finance sectors, preferring connected, portable, and minimally invasive solutions.

Europe accounts for 30% of the global ENT devices market, with Germany, UK, and France as leading markets. Regulatory frameworks such as CE marking and sustainability initiatives influence device design and adoption. Emerging technologies like AI-assisted endoscopy and smart hearing aids are increasingly integrated into hospital workflows. Local player MED-EL GmbH launched advanced cochlear implant systems in 2024, enhancing patient outcomes in over 120 clinics. European consumer behavior is shaped by regulatory compliance and preference for explainable, reliable medical technologies. Hospitals and specialty clinics collectively consume more than 55% of devices, reflecting structured healthcare infrastructure.

Asia-Pacific is projected to register the fastest growth, representing 25% of total global volume. China, India, and Japan are the top-consuming countries, driven by growing healthcare infrastructure and private clinic expansion. The region is witnessing rapid adoption of mobile health apps and tele-audiology platforms. Local player Sonova Group expanded hearing aid distribution across India and China in 2024, reaching over 200,000 new patients. Consumers in the region show strong preference for e-commerce channels and app-enabled devices, reflecting tech-savvy adoption patterns. Government investments in rural hearing care and digital healthcare further support regional growth.

South America holds 8% of the global ENT devices market, with Brazil and Argentina as key contributors. Growth is driven by investments in hospital infrastructure and private clinics. Government incentives for medical device imports and tax reductions have facilitated adoption. Local player Medtronic expanded ENT surgical instrument offerings to 50+ hospitals in 2024. Consumers in South America show a preference for affordable, reliable devices, with demand tied to media campaigns and language-localized product offerings. Clinics and outpatient centers dominate usage, with nearly 65% of devices deployed in urban healthcare hubs.

Middle East & Africa represents 6% of the global ENT devices market. Major growth countries include UAE and South Africa. Demand is driven by oil & gas sector health programs, hospital expansions, and telemedicine initiatives. Technological modernization includes robotic-assisted ENT surgeries and mobile diagnostic tools. Local player Amplifon expanded hearing solutions to 25 clinics across UAE and South Africa in 2024. Regional consumer behavior is influenced by urbanization, rising awareness, and government healthcare partnerships, emphasizing adoption in specialized hospitals and urban clinics.

United States – 38% Market Share: High production capacity and strong end-user demand in hospitals and outpatient clinics drive dominance.

Germany – 12% Market Share: Advanced technological adoption in ENT diagnostics and strict regulatory compliance support market leadership.

The ENT Devices Market exhibits a moderately consolidated structure with over 120 active competitors globally, including both established multinational corporations and regional players. The top five companies collectively account for approximately 48% of total market share, highlighting concentrated leadership in cochlear implants, endoscopy systems, and diagnostic tools. Key strategic initiatives include product launches of AI-enabled hearing aids, mergers and acquisitions to expand regional footprints, and partnerships with hospitals for clinical trials and telehealth integration. Innovation trends such as robotic-assisted ENT surgeries, wireless diagnostic devices, and remote patient monitoring are reshaping competitive dynamics. Major players are investing heavily in R&D, with over 15 new devices introduced across North America, Europe, and Asia-Pacific in 2023–2024. Market positioning is increasingly driven by technological differentiation, regulatory compliance, and customer-centric services. Emerging startups focusing on tele-audiology and mobile-enabled ENT solutions are gaining traction, contributing to a diverse and competitive ecosystem that is responsive to evolving clinical needs and digital healthcare adoption.

William Demant Holding A/S

GN Store Nord

Amplifon S.p.A.

Natus Medical Incorporated

Oticon A/S

The ENT Devices Market is witnessing rapid technological advancements aimed at improving diagnostic precision, patient comfort, and procedural efficiency. AI and machine learning are being integrated into audiometry and hearing aid calibration, enhancing personalized treatment and predictive diagnostics. Robotic-assisted ENT surgeries allow for high-precision procedures, reducing surgical errors and improving patient recovery times, with hospitals reporting over 20% shorter operation durations in pilot trials. Tele-audiology platforms and mobile-enabled devices are enabling remote hearing assessments and continuous monitoring, particularly in underserved regions, with over 150 clinics adopting remote monitoring solutions in 2024. Advanced endoscopy systems with high-definition imaging and flexible optics are improving visualization during surgical interventions, leading to better clinical outcomes. Moreover, innovations in 3D printing allow for patient-specific implants and surgical guides, enhancing procedural accuracy. Wireless cochlear implants, AI-powered diagnostic software, and connected ENT devices are reshaping the clinical workflow, while integration with electronic health records ensures data-driven decision-making and efficient care coordination.

In November 2022, Cochlear received FDA approval for the Nucleus 8 Sound Processor — the company announced the device as the smallest, lightest behind-the-ear cochlear implant processor available, enabling improved wearability and rechargeability for recipients. Source: www.cochlear.com

On 6 August 2024, Sonova launched the Sphere Infinio / Infinio platform, described as the first hearing aid family using real-time AI to distinguish speech from noise; Sonova reported the product as a material tech advancement and market differentiator. Source: www.sonova.com

In October 2024, Sonova resumed supplying a major U.S. retailer (Costco) with a prescription hearing aid model, restarting distribution in 107 U.S. locations and signaling renewed large-scale retail partnerships. Source: www.sonova.com

In April 2024, Amplifon acquired two U.S. companies adding 35 points of sale in Pennsylvania (approx. USD 20 million revenue run-rate cited by the company), strengthening its U.S. retail footprint and service network. Source: corporate.amplifon.com

The ENT Devices Market Report provides a comprehensive analysis of global and regional trends, covering all major device types including cochlear implants, endoscopy systems, audiometry instruments, hearing aids, and surgical tools. The report examines adoption patterns across key applications such as hospitals, outpatient clinics, rehabilitation centers, and home care. Geographic segmentation includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional consumption, infrastructure trends, and technological adoption. End-user insights focus on healthcare providers, research institutions, and specialized ENT centers, providing data on usage volumes, clinical integration, and technology penetration. The report also addresses current and emerging technologies such as AI-assisted diagnostics, robotic-assisted procedures, tele-audiology, and connected hearing solutions, along with recent product launches and R&D initiatives. Additionally, the scope includes regulatory frameworks, ESG considerations, market dynamics, competitive strategies, and investment patterns shaping the future landscape. Emerging niches such as mobile ENT platforms, 3D-printed implants, and minimally invasive surgical devices are also evaluated, offering decision-makers actionable intelligence to guide strategic planning and resource allocation.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 27,300.6 Million |

| Market Revenue (2032) | USD 41,897.9 Million |

| CAGR (2025–2032) | 5.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Cochlear Limited, Medtronic, Sonova Holding AG, William Demant Holding A/S, GN Store Nord, Amplifon S.p.A., Natus Medical Incorporated, Oticon A/S |

| Customization & Pricing | Available on Request (10% Customization Free) |