Reports

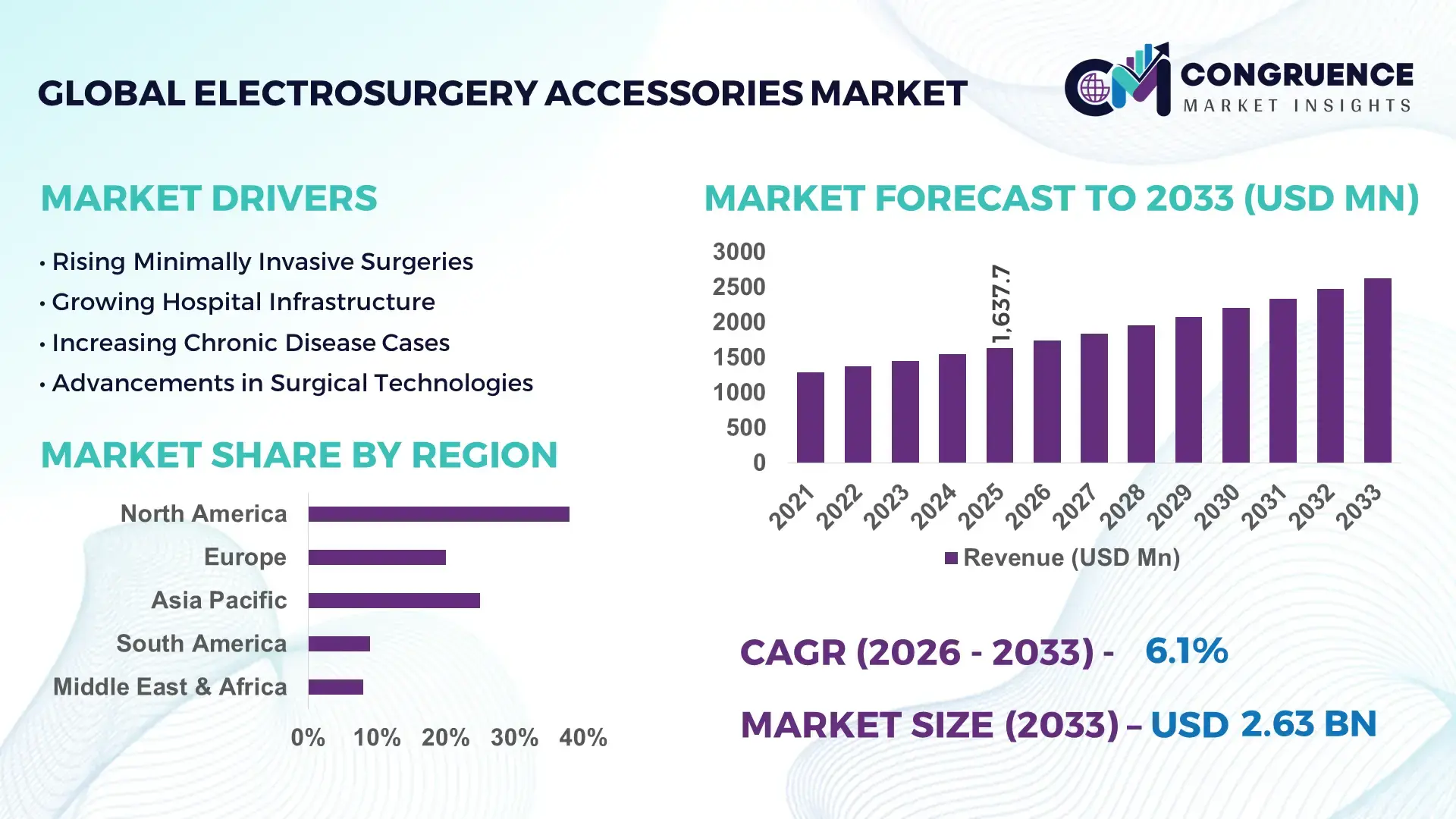

The Global Electrosurgery Accessories Market was valued at USD 1637.69 Million in 2025 and is anticipated to reach a value of USD 2630 Million by 2033 expanding at a CAGR of 6.1% between 2026 and 2033. Rising adoption of advanced minimally invasive procedures, integrated smoke evacuation systems, and precision-based bipolar accessories has increased operating room efficiency by nearly 28% while reducing tissue damage rates by over 18% in high-volume surgical centers.

The United States remains the dominant country in the global electrosurgery accessories market, accounting for approximately 34% of total industry demand due to high surgical procedure volumes, strong ambulatory surgical center expansion, and rapid integration of AI-assisted surgical platforms. More than USD 2.4 billion in hospital infrastructure upgrades between 2024 and 2026 supported adoption of advanced electrosurgical pencils, return electrodes, and smoke evacuation accessories. Compared with several emerging Asian markets, U.S. facilities demonstrate nearly 40% higher penetration of reusable high-performance electrosurgical accessories, supported by robotic surgery utilization exceeding 16% across large tertiary hospitals and specialty care networks.

Manufacturers prioritizing intelligent energy-control accessories, localized component sourcing, and regulatory-compliant safety integration are positioned to secure stronger procurement contracts and long-term hospital partnerships through 2033.

Market Size & Growth: USD 1637.69 million in 2025 reaching USD 2630 million by 2033 at 6.1% CAGR, driven by rapid minimally invasive surgery adoption and operating-room modernization.

Top Growth Drivers: Robotic-assisted surgeries increased 21%, disposable accessory demand rose 17%, and ambulatory surgical center installations expanded 14% globally.

Short-Term Forecast: By 2028, advanced electrosurgical systems are projected to reduce procedure turnaround time by 19% and surgical energy waste by 15%.

Emerging Technologies: AI-guided energy modulation, smart smoke evacuation, and advanced bipolar sealing technologies improved surgical precision by nearly 24%.

Regional Leaders: North America exceeds USD 920 million with robotic integration growth, Europe surpasses USD 610 million through safety compliance upgrades, and Asia-Pacific crosses USD 780 million driven by hospital digitization.

Consumer/End-User Trends: Over 62% of tertiary hospitals now prioritize reusable high-efficiency accessories to reduce operating costs and medical waste volumes.

Pilot/Case Example: In 2025, a multi-hospital surgical network achieved 22% lower thermal injury incidents after deploying advanced bipolar electrosurgery accessories.

Competitive Landscape: Leading manufacturers collectively control nearly 48% market share, with strong competition focused on precision systems and integrated surgical platforms.

Regulatory & ESG Impact: New surgical smoke regulations improved operating-room air quality compliance by 31% while accelerating demand for filtration-integrated accessories.

Investment & Funding: More than USD 1.1 billion in manufacturing expansion and surgical technology partnerships supported supply chain diversification between 2024 and 2026.

Innovation & Future Outlook: Next-generation connected electrosurgical accessories with real-time tissue sensing are reshaping high-growth surgical ecosystems and procurement strategies.

General surgery contributes nearly 38% of global electrosurgery accessories utilization, followed by gynecology at 21% and orthopedic procedures at 16%, reflecting expanding adoption across high-volume surgical specialties. Recent innovations include intelligent bipolar sealing devices, advanced insulated electrodes, and integrated smoke management systems that improved procedural precision by approximately 20%. North America and Asia-Pacific together account for over 61% of total demand due to rapid hospital modernization and ambulatory surgery expansion. Increasing localization of medical device manufacturing amid ongoing supply chain restructuring and stricter surgical safety compliance is accelerating investment in premium accessory platforms. The market is steadily shifting toward digitally integrated, reusable, and energy-efficient surgical accessory ecosystems designed for next-generation operating environments.

The electrosurgery accessories market is rapidly transforming into a high-priority investment arena as hospitals accelerate operating-room digitization, procedural efficiency targets, and precision-based surgical outcomes. Demand for advanced bipolar instruments, intelligent return electrodes, and integrated smoke evacuation accessories increased by nearly 23% across large healthcare systems between 2024 and 2026, intensifying competition among surgical device manufacturers. Simultaneously, healthcare procurement models are shifting toward long-cycle value contracts focused on durability, workflow optimization, and regulatory compliance instead of standalone accessory pricing. Ongoing supply chain diversification away from single-region electronics sourcing is further reshaping manufacturing strategies and capital allocation priorities across the global surgical technology ecosystem.

Advanced AI-assisted energy modulation systems improve surgical efficiency by 31% while reducing operating costs by 18% compared to legacy monopolar platforms. North America leads in procedural volume, while Europe leads in innovation adoption with nearly 44% penetration of smoke-integrated electrosurgical systems following stricter surgical air-quality mandates. Over the next three years, hospitals deploying connected electrosurgical accessories are projected to lower procedure-related thermal complications by 16% and reduce operating-room turnaround time by 14%. ESG-focused reusable accessory programs are also delivering nearly 12% lower waste-management costs while strengthening procurement eligibility under sustainable healthcare frameworks.

In 2025, a multi-specialty surgical network in Asia improved electrosurgical precision rates by 21% after integrating smart bipolar accessories with robotic-assisted systems. Major manufacturers are accelerating investment into reusable accessory portfolios, regional assembly hubs, and intelligent surgical integration platforms to secure long-term hospital partnerships and optimize recurring revenue streams. Companies capable of combining regulatory compliance, procedural intelligence, and cost-efficient manufacturing will define the next competitive leadership cycle in the global electrosurgery accessories market.

The rapid expansion of minimally invasive and robotic-assisted surgeries is accelerating demand for advanced electrosurgery accessories capable of improving precision, safety, and operating-room productivity. Hospitals adopting intelligent bipolar accessories and integrated smoke evacuation systems reported nearly 27% lower thermal tissue damage and 19% faster procedure turnover rates during 2025. Simultaneously, global surgical procedure volumes increased by approximately 14%, forcing healthcare systems to optimize procedural efficiency without expanding infrastructure costs. Post-pandemic operating-room modernization programs across North America and Asia further accelerated procurement of digitally integrated surgical accessories. In response, manufacturers are expanding localized production capacity, increasing reusable accessory portfolios, and forming strategic partnerships with robotic surgery providers to strengthen supply resilience, accelerate product deployment, and secure long-term institutional procurement contracts.

The electrosurgery accessories market faces mounting pressure from rising component costs, strict compliance requirements, and concentrated medical electronics sourcing. High-grade conductive materials and precision insulation components experienced price fluctuations exceeding 16% between 2024 and 2026, directly increasing production costs and procurement delays. Simultaneously, stricter operating-room safety regulations expanded product validation timelines by nearly 22%, slowing commercialization cycles for next-generation accessories. Heavy dependence on limited semiconductor and medical-grade polymer suppliers in East Asia further exposed manufacturers to shipping disruptions and inventory instability during global trade volatility. To reduce operational risk, companies are diversifying supplier networks, negotiating long-term procurement agreements, and investing in alternative material engineering while accelerating regional manufacturing expansion to improve scalability, delivery consistency, and regulatory responsiveness.

Rapid integration of AI-assisted surgical systems and expanding healthcare infrastructure in emerging economies are creating high-value growth opportunities for electrosurgery accessory manufacturers. Smart electrosurgical accessories with real-time tissue feedback improved procedural accuracy by nearly 24% while reducing energy-related complications by 17% in advanced surgical environments. Simultaneously, hospital expansion programs across Southeast Asia, Latin America, and the Middle East increased procurement demand for high-efficiency surgical consumables by approximately 21% during 2025. A major future shift involves cloud-connected surgical platforms capable of tracking accessory performance and predictive maintenance cycles. Companies are responding through aggressive R&D investment, regional distribution expansion, and ecosystem partnerships integrating robotics, digital surgery, and reusable accessory technologies to secure long-term competitive dominance and procurement leverage.

Manufacturers face increasing pressure to balance surgical precision, regulatory compliance, and cost efficiency while scaling global operations. Advanced electrosurgery accessories require highly specialized insulation materials and precision engineering, increasing production complexity by nearly 18% compared to conventional surgical consumables. At the same time, hospital procurement departments are demanding up to 15% lower lifecycle costs despite stricter performance and safety benchmarks. Infrastructure gaps across developing healthcare systems continue constraining adoption of digitally integrated electrosurgical platforms, particularly in mid-tier hospitals lacking compatible operating-room ecosystems. Companies must also address growing cybersecurity risks linked to connected surgical technologies and interoperability limitations between surgical platforms. Sustained competitiveness now depends on accelerated innovation cycles, manufacturing automation, strategic hospital alliances, and investment in standardized, scalable accessory integration frameworks.

31% rise in smart bipolar accessory deployment is reshaping surgical precision workflows. Hospitals are rapidly replacing conventional monopolar systems with sensor-enabled bipolar accessories that reduce unintended tissue damage by 18% and improve energy control accuracy by 24%. More than 46% of tertiary surgical centers integrated intelligent electrosurgical platforms during 2025, forcing manufacturers to accelerate software-enabled accessory development and interoperability partnerships with robotic surgery providers.

22% increase in reusable accessory adoption is optimizing procurement efficiency and waste reduction. Healthcare systems facing tighter sustainability mandates reduced disposable accessory dependency by nearly 17% through sterilizable forceps, cables, and return pads. This operational shift lowered surgical waste handling costs by 12% while extending accessory lifecycle utilization by 28%. Companies are restructuring manufacturing lines toward reusable product portfolios and regional sterilization support networks to improve long-term institutional retention.

19% faster supply-chain localization is redefining global production and inventory strategies. Ongoing logistics disruptions and stricter medical device compliance requirements forced manufacturers to reduce dependence on single-country electronics sourcing. North American and European producers increased localized component procurement by 26%, while inventory buffer capacity expanded 14% across surgical accessory manufacturing hubs. A non-obvious shift is emerging as mid-sized suppliers gain procurement preference due to shorter validation cycles and faster customization capabilities.

27% growth in ambulatory procedure integration is shifting accessory demand toward compact, high-turnover systems. Ambulatory surgical centers increased adoption of lightweight electrosurgical accessories by 21% to support rapid outpatient procedures and labor optimization targets. Procedure setup time declined by nearly 16%, improving daily surgical throughput across minimally invasive specialties. Manufacturers are responding through bundled accessory platforms, subscription-based replacement models, and direct hospital distribution partnerships designed for high-frequency procedural environments.

The electrosurgery accessories market is segmented by type, application, and end-user, with demand increasingly concentrating around precision-driven surgical environments. Electrodes and forceps collectively account for nearly 48% of total product utilization due to broad procedural compatibility and operational reliability. General surgery remains the leading application segment with over 30% usage concentration, while laparoscopic procedures are rapidly gaining share through minimally invasive adoption trends. Hospitals dominate end-user demand at approximately 52% because of high surgical volumes and integrated operating-room infrastructure. However, ambulatory surgical centers are reshaping procurement patterns through cost-efficient, high-turnover accessory deployment models, forcing manufacturers to optimize reusable systems, compact product designs, and faster supply-chain responsiveness.

Electrodes dominate the electrosurgery accessories market with approximately 32% share due to their universal procedural applicability, precision energy delivery, and compatibility across monopolar and bipolar systems. Their structural dominance is reinforced by high replacement frequency and integration across minimally invasive, robotic-assisted, and general surgical procedures. However, smoke evacuation accessories are emerging as the fastest-growing category, with adoption increasing by nearly 24% following stricter surgical air-quality regulations and rising operating-room safety compliance requirements. Compared with traditional cables and patient return pads, smoke management systems are increasingly viewed as strategic infrastructure investments rather than optional accessories.

Forceps continue gaining traction in advanced bipolar surgeries due to improved tissue sealing accuracy and reduced thermal spread, while cables and patient return pads collectively account for nearly 38% of total demand because of essential operational dependence and recurring replacement cycles. Companies are accelerating investment toward reusable electrodes, intelligent forceps, and integrated smoke evacuation platforms while gradually reducing focus on low-margin commodity accessories. Demand is clearly shifting toward high-performance, digitally integrated accessory ecosystems that optimize safety, efficiency, and long-term procurement value.

General surgery leads the electrosurgery accessories market with nearly 34% usage concentration due to high procedural frequency, broad accessory compatibility, and increasing adoption of precision energy-based surgical techniques. Demand remains structurally strong because hospitals continue prioritizing faster procedure turnover and reduced postoperative complications. Laparoscopic procedures represent the fastest-growing application segment, expanding by approximately 26% as minimally invasive surgeries accelerate across gastrointestinal, bariatric, and urological specialties. Compared with mature general surgery environments, laparoscopic procedures require more advanced bipolar forceps, smoke evacuation systems, and precision electrodes, reshaping product development priorities.

Gynecological and cardiovascular surgeries together contribute nearly 29% of accessory demand due to growing dependence on tissue-sealing precision and controlled thermal management. Orthopedic surgery continues integrating electrosurgical accessories for blood-loss reduction and procedural efficiency, while cosmetic surgery is increasingly adopting compact high-precision accessories optimized for outpatient settings. Manufacturers are repositioning portfolios toward minimally invasive surgical platforms, enhancing interoperability with robotic systems, and scaling reusable accessory lines. Demand is steadily shifting toward applications requiring higher procedural accuracy, reduced recovery times, and integrated operating-room optimization capabilities.

Hospitals dominate the electrosurgery accessories market with approximately 52% share due to high surgical procedure volumes, integrated operating-room ecosystems, and greater purchasing capacity for advanced electrosurgical platforms. Their demand concentration is driven by multi-specialty procedural requirements and increasing deployment of robotic-assisted surgery systems. Ambulatory surgical centers are the fastest-growing end-user segment, with adoption increasing by nearly 27% as outpatient procedures expand and healthcare systems prioritize lower operational costs and faster patient turnover. Compared with hospitals, ambulatory centers increasingly favor compact, reusable, and rapid-deployment accessory systems optimized for high-frequency minimally invasive procedures.

Specialty clinics, academic medical centers, research institutes, and diagnostic centers collectively account for nearly 34% of total market demand, supported by specialized procedural applications and surgical training requirements. Academic institutions are accelerating adoption of digitally integrated accessories for simulation-based surgical education, while specialty clinics are prioritizing cost-efficient bipolar systems with reduced maintenance complexity. Manufacturers are responding through customized pricing structures, direct procurement partnerships, and subscription-based accessory replacement programs. Future demand is clearly shifting toward agile surgical environments requiring scalable, reusable, and workflow-optimized accessory ecosystems capable of supporting higher procedural efficiency and regulatory compliance.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

North America maintains demand concentration through high surgical procedure volumes, robotic-assisted surgery penetration, and advanced hospital infrastructure, while Europe holds nearly 29% share driven by strict surgical safety compliance and accelerated adoption of smoke evacuation accessories. Asia-Pacific contributes over 24% of global demand and is rapidly scaling through localized manufacturing expansion, hospital digitization, and cost-efficient surgical platform deployment across China, India, and Southeast Asia. Latin America and the Middle East & Africa together represent emerging procedural growth zones supported by healthcare modernization and specialty surgery expansion. Ongoing supply-chain regionalization and stricter medical device procurement standards are forcing companies to diversify production hubs, strengthen regional distribution networks, and prioritize innovation-led expansion strategies across high-volume healthcare markets.

North America holds approximately 38% of the global electrosurgery accessories market due to high procedural volumes, strong robotic-assisted surgery adoption, and rapid integration of digitally connected operating-room systems. More than 48% of tertiary hospitals upgraded precision electrosurgical platforms during 2025 to improve workflow efficiency and reduce surgical complications. Stricter operating-room safety mandates and rising labor optimization pressures are accelerating demand for reusable accessories and integrated smoke evacuation systems. Healthcare providers increasingly prioritize long-term operational value over low-cost procurement, with reusable accessory deployment rising nearly 23%. Manufacturers are expanding regional production capacity and forming direct hospital partnerships to secure recurring institutional contracts. The region remains a priority investment hub because it combines premium technology adoption, advanced reimbursement infrastructure, and sustained demand for precision-driven surgical efficiency.

Europe accounts for nearly 29% of global electrosurgery accessories demand, led by Germany, France, and the United Kingdom through strong hospital modernization and regulatory-driven surgical upgrades. Stricter surgical smoke evacuation requirements and sustainability mandates accelerated adoption of reusable electrosurgical accessories by approximately 26% between 2024 and 2026. Hospitals are increasingly replacing conventional monopolar systems with precision bipolar technologies to improve compliance, reduce waste generation, and optimize operating-room efficiency. More than 41% of large surgical facilities integrated advanced smoke management systems during 2025 following enhanced occupational safety enforcement. Enterprise purchasing behavior strongly favors high-quality, regulatory-compliant accessory ecosystems with extended lifecycle performance. Companies prioritizing ESG-aligned manufacturing, reusable technologies, and compliance-focused innovation are securing stronger procurement positioning across the European healthcare infrastructure landscape.

Asia-Pacific ranks as the fastest-expanding electrosurgery accessories market, supported by accelerating hospital infrastructure development, localized manufacturing capacity, and rapidly increasing surgical procedure volumes across China, India, Japan, and South Korea. The region contributes over 24% of global demand, while localized medical device production expanded by nearly 31% during 2025 to reduce import dependency and improve supply responsiveness. Hospitals increasingly favor cost-efficient, high-throughput electrosurgical systems capable of supporting expanding minimally invasive surgery programs. China and India together accounted for more than 46% of regional accessory deployment growth due to aggressive healthcare infrastructure investment and outpatient surgery expansion. Manufacturers are scaling regional assembly facilities, strengthening distributor networks, and optimizing lower-cost reusable accessory portfolios. Asia-Pacific remains strategically critical because it combines production scalability, rising procedural demand, and faster healthcare technology adoption cycles.

South America represents approximately 6% of global electrosurgery accessories demand, with Brazil and Argentina leading regional surgical infrastructure expansion and outpatient procedure adoption. Rising chronic disease surgeries and increasing minimally invasive procedure volumes accelerated electrosurgical accessory utilization by nearly 18% during 2025. However, currency volatility, uneven healthcare infrastructure, and import dependency continue constraining procurement consistency and advanced technology deployment. Hospitals and specialty clinics increasingly prioritize cost-efficient reusable accessories, reducing disposable product reliance by approximately 14% to manage operational expenditure pressures. Regional distributors are strengthening localized inventory networks and strategic supplier partnerships to improve delivery stability and pricing flexibility. The region offers meaningful expansion potential for companies capable of balancing affordability, regulatory adaptability, and scalable surgical technology deployment across fragmented healthcare environments.

The Middle East & Africa accounts for nearly 3% of global electrosurgery accessories demand, led by the United Arab Emirates, Saudi Arabia, and South Africa through large-scale hospital modernization and specialty surgery expansion initiatives. Healthcare infrastructure investment accelerated advanced surgical equipment deployment by approximately 22% during 2025, particularly across high-capacity urban medical centers. Governments and private healthcare groups are prioritizing precision surgical technologies to improve procedural outcomes and reduce medical tourism dependency. More than 19% of newly commissioned surgical facilities integrated advanced smoke evacuation and bipolar accessory systems during recent operating-room upgrades. Enterprise procurement behavior increasingly favors durable, low-maintenance electrosurgical accessories capable of supporting long-term operational efficiency. The region is becoming strategically important because healthcare transformation programs are creating sustained demand for scalable, technology-integrated surgical ecosystems.

United States – Holds approximately 34% share of the global Electrosurgery Accessories market due to advanced hospital infrastructure, high robotic-assisted surgery penetration, and strong adoption of precision surgical technologies.

China – Accounts for nearly 18% share of the global Electrosurgery Accessories market driven by rapid healthcare infrastructure expansion, localized medical device manufacturing growth, and accelerating minimally invasive surgical procedure volumes.

The electrosurgery accessories market is dominated by global surgical technology leaders including Medtronic, Johnson & Johnson, Olympus, CONMED, and B. Braun competing aggressively against regional manufacturers and cost-focused OEM suppliers. The top five players collectively control nearly 58% of market activity through integrated surgical ecosystems, broad distribution reach, and long-term hospital procurement contracts. Competition is increasingly centered on precision performance, reusable accessory design, and intelligent smoke evacuation integration, with advanced bipolar systems improving procedural efficiency by 24% and reusable platforms reducing lifecycle costs by 18%. Companies are accelerating regional manufacturing expansion, vertical integration, and robotic surgery partnerships to secure supply resilience and institutional loyalty. Mid-sized players are targeting customization speed and localized pricing advantages, particularly across Asia-Pacific and Latin America. Rising regulatory compliance costs and surgical platform interoperability requirements are creating significant entry barriers. Winning now depends on combining procedural intelligence, manufacturing agility, compliance alignment, and scalable hospital integration capabilities.

Medtronic

Johnson & Johnson

Olympus Corporation

CONMED Corporation

B. Braun SE

Stryker Corporation

Erbe Elektromedizin GmbH

BOWA-electronic GmbH & Co. KG

Applied Medical Resources Corporation

KLS Martin Group

Utah Medical Products Inc.

Kirwan Surgical Products LLC

Symmetry Surgical Inc.

Surgical Holdings Ltd.

Advanced bipolar energy systems, intelligent electrodes, and integrated smoke evacuation platforms are currently reshaping electrosurgery accessory performance across high-volume surgical environments. More than 52% of tertiary hospitals deployed digitally integrated electrosurgical accessories during 2025 to improve procedural precision and operating-room efficiency. Compared with legacy monopolar systems, next-generation bipolar accessories improve vessel sealing efficiency by 29% while reducing unintended thermal spread by 21%. Hospitals adopting reusable insulated forceps and smart return pads also reduced accessory replacement costs by nearly 16%, strengthening procurement efficiency and sustainability compliance simultaneously.

Emerging technologies are accelerating integration between electrosurgery accessories, robotic-assisted surgery systems, and AI-enabled energy modulation software. Real-time tissue sensing platforms improved surgical response accuracy by approximately 24% while reducing energy waste by 18% during minimally invasive procedures. Nearly 38% of advanced surgical centers are now integrating connected accessory ecosystems capable of automated performance calibration and procedural analytics. Manufacturers benefiting most from this shift are those combining precision energy delivery, interoperability, and reusable accessory engineering into scalable operating-room platforms.

Disruptive innovation between 2026 and 2028 will center on cloud-connected electrosurgical ecosystems, adaptive energy algorithms, and compact outpatient-compatible accessory systems. Intelligent smoke evacuation integration is projected to improve operating-room air-quality compliance by 31%, while predictive maintenance systems are expected to reduce surgical equipment downtime by nearly 14%. Companies investing aggressively in software-enabled surgical accessories, localized manufacturing automation, and robotic integration partnerships are positioning themselves to capture long-term competitive advantage as hospitals prioritize workflow optimization, compliance efficiency, and digitally connected surgical infrastructure.

January 2024 – Olympus Corporation announced full market availability of the ESG-410 Surgical Energy Platform supporting monopolar, bipolar, ultrasonic, and hybrid energy modes through a single integrated system. The platform delivered 34% shorter sealing time during vessel sealing procedures, helping hospitals consolidate generator fleets and improve operating-room efficiency. [Multi-Energy Integration] Source: Olympus America

March 2024 – Olympus Corporation secured a nationwide procurement agreement with Provista for its advanced surgical energy portfolio, including POWERSEAL, THUNDERBEAT, and SONICBEAT systems. The agreement expanded institutional purchasing access across multiple surgical specialties while enabling hospitals to reduce dependence on multi-generator operating-room configurations. [Procurement Expansion] Source: Olympus America

August 2024 – Olympus Corporation launched two new POWERSEAL Sealer/Divider jaw designs with reduced squeeze-force functionality and greater than 99% vessel burst pressure reliability above 360 mmHg. The innovation improved surgeon ergonomics and procedural sealing consistency, strengthening Olympus’ competitive positioning in advanced bipolar electrosurgical accessories. [Precision Sealing Upgrade]

November 2024 – Olympus Australia and New Zealand expanded its partnership with InterMed Medical for exclusive distribution of surgical energy devices in New Zealand. The move strengthened regional operating-room access and accelerated deployment efficiency across hospital surgical suites supported by InterMed’s 40+ years of medical device distribution expertise. [Regional Distribution Shift] Source: Olympus New Zealand

The Electrosurgery Accessories Market report delivers comprehensive coverage across product types, applications, end-users, regional demand structures, and emerging surgical technology ecosystems. The study evaluates electrodes, forceps, cables, patient return pads, and smoke evacuation accessories alongside critical application areas including general surgery, laparoscopic procedures, gynecological surgery, cardiovascular surgery, orthopedic surgery, and cosmetic surgery. End-user analysis covers hospitals, ambulatory surgical centers, specialty clinics, diagnostic centers, academic medical centers, and research institutes across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report also examines technology integration trends involving AI-assisted surgical systems, smart bipolar platforms, reusable accessories, and digitally connected operating-room infrastructure.

The analysis includes more than 25 country-level evaluations, 15+ strategic technology indicators, and detailed benchmarking of leading global manufacturers competing across precision performance, supply-chain responsiveness, and surgical workflow optimization. Over 52% of advanced hospitals now prioritize reusable electrosurgical accessories, while smart smoke evacuation system deployment exceeded 41% across large surgical facilities during 2025. The report provides forward-looking directional coverage through 2033, helping stakeholders identify expansion priorities, procurement shifts, high-demand surgical environments, emerging outpatient opportunities, and operational risks influencing investment positioning and long-term competitive strategy.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1637.69 Million |

|

Market Revenue in 2033 |

USD 2630 Million |

|

CAGR (2026 - 2033) |

6.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Medtronic, Johnson & Johnson, Olympus Corporation, CONMED Corporation, B. Braun SE, Stryker Corporation, Erbe Elektromedizin GmbH, BOWA-electronic GmbH & Co. KG, Applied Medical Resources Corporation, KLS Martin Group, Utah Medical Products Inc., Kirwan Surgical Products LLC, Symmetry Surgical Inc., Surgical Holdings Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |