Reports

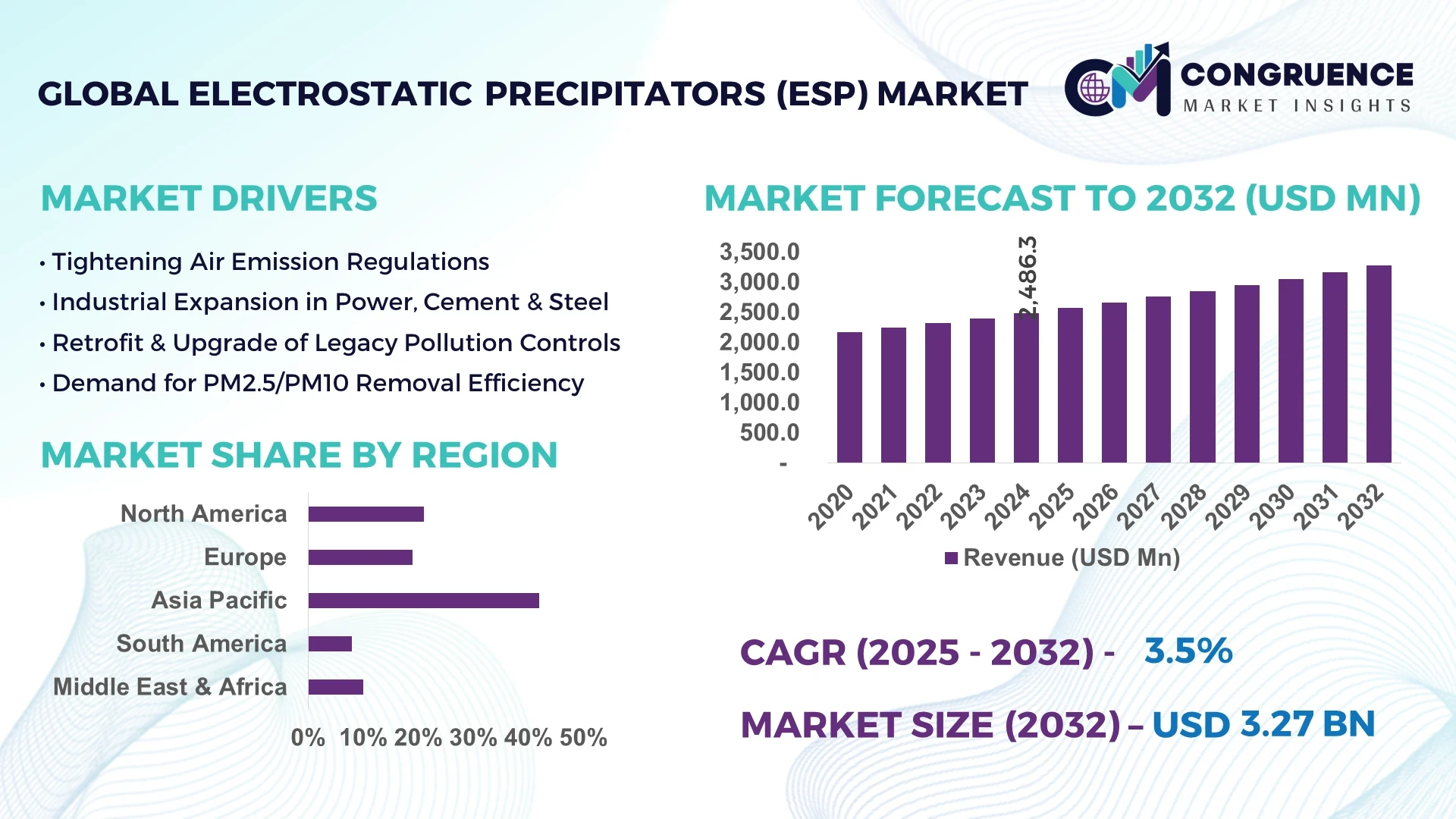

The Global Electrostatic Precipitators (ESP) Market was valued at USD 2486.27 Million in 2024 and is anticipated to reach a value of USD 3273.95 Million by 2032 expanding at a CAGR of 3.5% between 2025 and 2032.

China exhibits remarkable production capacity in ESP systems, backed by substantial investments in emissions control across coal-fired power plants and steel manufacturing facilities. Leading domestic players maintain advanced manufacturing infrastructure, delivering high-voltage ESP modules optimized for large industrial systems and deploying digital fault-diagnostic features that enhance system reliability and maintenance responsiveness.

Across the ESP market, power generation remains the primary industrial sector, followed by contributions from cement production, chemicals, metal processing, and marine applications. Recent innovations include tubular ESP designs offering compact footprints, electrode materials with improved corrosion resistance, and wet-ESP variants capable of capturing submicron and acidic particulates with efficiencies approaching 99.9%. Regulatory drivers—such as tightening particulate emissions standards under EU directives and Asia-Pacific air quality mandates—continue to accelerate retrofitting and new installations. Energy-efficient models incorporating digital controls and real-time performance monitoring are gaining traction, supporting predictive maintenance and lower operating costs. Emerging trends reveal integration of hybrid pollution control systems—combining ESPs with scrubbers or flue gas desulfurization systems—and expansion into marine and transportation sectors. Regional consumption growth is particularly robust in Asia-Pacific, Europe, and North America, driven by industrial modernization, infrastructure expansion, and sustainable emission management strategies.

Artificial Intelligence (AI) is fundamentally reshaping the Electrostatic Precipitators (ESP) Market by introducing advanced real-time performance optimization and enhancing operational efficiency. In industrial installations, AI algorithms analyze streaming sensor data—such as particulate concentrations, gas flow dynamics, temperature fluctuations, and electrode current—to calibrate key parameters like voltage levels, rapping intervals, and gas distribution with precision. This ensures maximized dust collection efficiency while minimizing energy consumption. Predictive maintenance powered by AI enables early detection of equipment anomalies—such as voltage drift or electrode wear—so that corrective actions can be scheduled proactively, drastically reducing unplanned downtime.

In cement plant applications, AI-driven control systems enable tighter regulation of ESP performance under variably changing particulate loads, maintaining output purity with lower energy inputs. Across coal-fired power generators, integration of machine learning models supports adaptive adjustment of rapping cycles and power input in response to fluctuating flue gas characteristics. This not only boosts average collection efficiency but also extends electrode lifespan by reducing abrasive wear.

In Australia and similar advanced markets, AI-enabled predictive maintenance platforms now forecast filter degradation patterns, enabling timely interventions and lowering maintenance costs. The ESP market benefits from these digital transformations as AI-based solutions foster sustainable operations, lower lifecycle costs, and align with industry 4.0 objectives in emission control systems.

“In March 2024, FLSmidth launched its advanced precipitator control system with integrated artificial intelligence capabilities for predictive maintenance and performance optimization across cement industry applications.”

The Electrostatic Precipitators (ESP) Market is influenced by a combination of stringent environmental regulations, industrial modernization, and technological advancements in emissions control systems. Demand is particularly strong in heavy industries such as power generation, cement, steel, and chemical processing, where compliance with particulate emission standards is critical. Market trends indicate a shift toward energy-efficient and digitally integrated ESP solutions, capable of real-time monitoring and predictive maintenance. The adoption of hybrid pollution control systems is expanding, especially in regions with multi-pollutant emissions regulations. Furthermore, growing awareness about air quality management and sustainable industrial practices is driving investment in advanced ESP technologies, while evolving manufacturing capabilities and automation are improving operational efficiency and lifecycle value.

The tightening of global air quality standards is a primary growth driver for the Electrostatic Precipitators (ESP) Market. Regulatory bodies in regions such as the European Union, China, and North America have imposed strict limits on particulate matter emissions from coal-fired power plants, cement production facilities, and metal smelters. For instance, emission thresholds for PM2.5 and PM10 have been reduced significantly over the past decade, necessitating the installation of advanced ESP systems. These regulations are pushing industries to replace outdated equipment with modern, high-efficiency ESP units capable of achieving particulate collection rates exceeding 99%. Additionally, national clean air programs in emerging economies are creating substantial demand for ESP installations across both retrofit and new industrial projects.

One of the notable restraints in the Electrostatic Precipitators (ESP) Market is the significant capital expenditure associated with high-performance units. Advanced ESP systems incorporating digital control modules, corrosion-resistant materials, and hybrid filtration technologies require substantial upfront investment. Moreover, the maintenance of large-scale ESP installations, particularly in industries with high dust loads such as cement and steel, demands specialized expertise and consistent servicing. Over time, electrode replacements, rapping mechanism adjustments, and power supply upgrades add to operational costs. For small and medium-scale industries, these financial barriers can deter adoption, especially in regions where regulatory enforcement is inconsistent or where low-cost alternatives like fabric filters are available.

The integration of Artificial Intelligence (AI) and Internet of Things (IoT) technologies presents a significant opportunity for the Electrostatic Precipitators (ESP) Market. AI-powered monitoring platforms can process real-time operational data—such as particulate density, gas flow velocity, and voltage fluctuations—to automatically adjust system parameters for peak efficiency. IoT-enabled sensors allow for continuous remote monitoring, reducing downtime and enabling condition-based maintenance. Industries deploying these solutions report extended component lifespans, reduced power consumption, and improved compliance with fluctuating emission norms. With the Industry 4.0 shift accelerating globally, the deployment of smart ESP systems is expected to grow rapidly, particularly in advanced manufacturing hubs and regions investing heavily in industrial digitalization.

Maintaining consistent performance of Electrostatic Precipitators (ESP) under fluctuating industrial process conditions is a persistent challenge. Variations in particulate size distribution, gas temperature, humidity, and chemical composition can impact the charging and collection efficiency of the ESP. For example, in cement plants or waste-to-energy facilities, rapid shifts in feedstock or combustion processes can cause instability in gas flow and particle resistivity, leading to reduced efficiency. Addressing these challenges often requires complex control system upgrades, specialized electrode designs, or the addition of conditioning agents—all of which increase operational complexity and costs. In high-variability industrial environments, achieving stable performance while keeping energy consumption low remains a technical and economic hurdle for manufacturers and end-users.

Adoption of Modular and Prefabricated ESP Units: Modular and prefabricated construction methods are gaining traction in the Electrostatic Precipitators (ESP) market, enabling faster deployment and reduced on-site labor requirements. These pre-engineered units are manufactured under controlled factory conditions, ensuring high precision and consistent quality. In Europe and North America, industrial projects are increasingly favoring such solutions to meet strict project timelines and improve installation safety. This approach also simplifies retrofitting in older facilities, where limited downtime is available for upgrades.

Growth of Hybrid Pollution Control Systems: Hybrid ESP systems, combining electrostatic precipitation with fabric filters or wet scrubbing technologies, are becoming increasingly popular in industries with complex emission profiles. This configuration allows for improved removal of ultrafine particulates, acidic aerosols, and heavy metals, achieving compliance with multi-pollutant regulations. Adoption is particularly strong in sectors such as coal-fired power generation, waste-to-energy plants, and cement manufacturing, where emission limits are tightening globally.

Integration of Digital Monitoring and Control Platforms: Advanced digital platforms with IoT-enabled sensors are being integrated into ESP systems to provide real-time performance monitoring. These solutions track variables such as voltage, dust load, gas flow, and particulate resistivity, allowing operators to make data-driven adjustments. Predictive analytics can detect performance deviations before they affect compliance, minimizing downtime and maintenance costs. Industrial users are increasingly adopting these systems to optimize efficiency and extend operational lifespans.

Expansion in Marine and Offshore Applications: ESP installations are finding new demand in marine and offshore industries, particularly in ship exhaust cleaning systems and offshore oil production platforms. As the International Maritime Organization (IMO) enforces stricter sulfur oxide and particulate emissions regulations, shipbuilders and operators are integrating compact, corrosion-resistant ESP units. These systems are designed to withstand harsh marine environments while ensuring compliance with international emission standards.

The Electrostatic Precipitators (ESP) market is segmented based on type, application, and end-user, each category reflecting distinct industry demands and growth patterns. By type, the market covers dry ESP, wet ESP, tubular ESP, and other specialized variants, with dry ESP dominating due to their widespread use in power and cement plants. Application segmentation spans industries such as power generation, cement, metals, chemicals, pulp and paper, and marine operations, where emission reduction requirements dictate adoption levels. End-user segmentation encompasses large-scale industrial operators, government utilities, and commercial entities, with heavy industries accounting for the largest share. Each segment demonstrates unique growth dynamics, influenced by regulatory enforcement, technological innovation, and regional industrialization trends.

Dry electrostatic precipitators hold the largest share in the market due to their proven performance in removing particulate matter from flue gases in coal-fired power plants and large-scale cement production facilities. Their ability to operate efficiently under high-temperature and high-dust-load conditions makes them the preferred choice for heavy industries. Wet ESPs, while less common, are gaining rapid adoption in applications requiring the removal of fine, sticky, or corrosive particles, such as in chemical processing and waste-to-energy plants. Tubular ESPs are niche products, typically used in small to medium-sized installations or specific process industries like pulp and paper. The fastest-growing category is wet ESPs, driven by the rising need to handle submicron particulates and acidic aerosols in compliance with increasingly stringent emission norms. Other specialized designs, such as compact modular ESPs, are also finding traction in facilities with limited space or requiring mobile emission control solutions.

Power generation is the leading application for electrostatic precipitators, supported by their critical role in reducing particulate emissions from coal-fired plants and biomass energy facilities. These installations require large-capacity ESP systems capable of continuous operation under high-load conditions. Cement manufacturing is the second-largest application, where dust-laden exhaust gases from kilns and grinders necessitate high-efficiency particulate control. The fastest-growing application is waste-to-energy, as municipalities and private operators expand incineration facilities to manage urban waste while adhering to strict air quality regulations. Metal smelting and refining industries also rely heavily on ESP systems to capture fine metal particles and dust, preventing environmental contamination. Other applications, such as pulp and paper production, chemicals, and marine exhaust cleaning, contribute to the market’s diversification, each with tailored ESP configurations to suit process-specific needs.

Heavy industrial operators remain the dominant end-user segment in the Electrostatic Precipitators market, particularly in sectors such as power, cement, and steel, where large-scale ESP installations are essential for compliance and operational efficiency. These industries have the resources to invest in advanced, high-capacity systems with digital monitoring capabilities. The fastest-growing end-user category is municipal and environmental management authorities, driven by the rapid expansion of waste-to-energy plants and stricter emission control mandates in urban areas. The marine sector is emerging as a notable contributor, following international regulations on particulate emissions from ships. Smaller industrial facilities, such as mid-scale manufacturing plants and specialty chemical producers, also represent a growing segment, particularly where space-saving, modular ESP solutions are viable. Each end-user category is influenced by differing priorities—ranging from operational cost reduction to sustainability goals—which in turn shape technology adoption patterns across the market.

Asia-Pacific accounted for the largest market share at 42% in 2024 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 4.8% between 2025 and 2032.

Asia-Pacific’s dominance is attributed to its vast industrial base, high energy demand, and extensive adoption of large-scale ESP installations in power generation and cement production. Meanwhile, Middle East & Africa is benefiting from accelerated industrial diversification, stringent air quality regulations, and infrastructure investments, particularly in energy, construction, and petrochemical sectors. Across all regions, the push for emission reduction compliance and adoption of advanced digital monitoring systems is reshaping procurement priorities.

Technological Innovation Driving Industrial Emission Compliance

Holding a 21% market share in 2024, the region is driven by demand from power generation, oil & gas, and manufacturing sectors. Recent government air quality mandates are compelling industries to adopt high-efficiency ESP systems with real-time monitoring capabilities. Key technological advancements include AI-integrated controls, predictive maintenance software, and energy-efficient electrode designs. Investment incentives in sustainable infrastructure and emission-reduction projects are fostering adoption in both retrofit and new plant installations, particularly in states with aggressive clean air policies.

Emission Control Modernization in Industrial Operations

Accounting for 19% market share in 2024, the region is anchored by industrial hubs in Germany, the UK, and France. EU directives on particulate matter emissions are pushing industries toward modern, energy-efficient ESP systems with hybrid filtration capabilities. Sustainability programs and carbon reduction targets are accelerating adoption in steel, cement, and waste-to-energy sectors. Advanced electrode materials, wet ESP technologies, and automated performance optimization tools are being implemented to meet stringent environmental compliance standards.

Industrial Expansion and Large-Scale Infrastructure Growth Fueling ESP Adoption

With a commanding 42% market volume in 2024, the region’s market strength is led by China, India, and Japan, where coal-fired power plants, cement production, and heavy manufacturing dominate demand. Massive infrastructure development projects, coupled with industrial pollution control mandates, are driving widespread ESP deployment. Innovation hubs in China and Japan are producing high-capacity, modular ESP units integrated with IoT sensors and AI-driven controls, enhancing operational efficiency in both large and mid-scale facilities.

Energy Transition and Environmental Policy Shaping ESP Deployment

Holding an estimated 8% share in 2024, Brazil and Argentina lead demand, supported by growth in power generation, mining, and cement manufacturing. Regional governments are implementing environmental regulations targeting particulate matter emissions, creating demand for advanced ESP installations. Infrastructure modernization, particularly in urban industrial zones, is contributing to increased procurement, while trade agreements are facilitating access to new ESP technologies from global suppliers.

Diversification Beyond Oil & Gas Driving ESP Technology Uptake

Representing a 10% share in 2024, major demand centers include the UAE, Saudi Arabia, and South Africa. Expansion in petrochemical, construction, and energy sectors is fueling adoption of ESP systems designed for high-dust and high-temperature environments. Technological modernization, including corrosion-resistant wet ESP designs and remote operational controls, is being prioritized to meet new environmental standards. Trade partnerships and industrial investment programs are enhancing technology transfer and market access across the region.

China – 28% market share – Driven by high production capacity, extensive coal power infrastructure, and large-scale industrial applications requiring advanced ESP systems.

United States – 15% market share – Strong demand from power generation and manufacturing sectors, supported by strict emission regulations and advanced technology adoption.

The Electrostatic Precipitators (ESP) market is characterized by a moderately consolidated competitive landscape, with approximately 35 to 40 active global and regional players operating across diverse industrial sectors. Competition is driven by technological innovation, regulatory compliance demands, and the need for energy-efficient and high-performance emission control solutions. Leading companies are focusing on expanding product portfolios to include AI-driven monitoring systems, modular designs, and hybrid pollution control units. Strategic partnerships with engineering, procurement, and construction (EPC) firms are becoming more common to secure large-scale industrial contracts. Mergers and acquisitions are reshaping market positioning, with several major players integrating specialized technology providers to enhance product capabilities. In addition, manufacturers are investing heavily in R&D to develop corrosion-resistant electrode materials, compact wet ESP systems, and IoT-enabled performance analytics platforms. Regional manufacturers are competing by offering cost-effective, locally customized solutions, while global leaders maintain a strong presence through brand reputation, innovation, and after-sales service networks. The competitive environment continues to evolve with rising adoption of Industry 4.0 integration and demand for predictive maintenance features.

FLSmidth A/S

Mitsubishi Hitachi Power Systems, Ltd.

General Electric Company

Siemens Energy AG

Babcock & Wilcox Enterprises, Inc.

Thermax Limited

Hamon Group

Feida Group Company Limited

Balcke-Dürr GmbH

KC Cottrell Co., Ltd.

Electrostatic Precipitators (ESP) technology continues to evolve rapidly, driven by the imperative to boost efficiency, extend durability, and meet stringent emission compliance. One prominent development is the emergence of IoT-integrated ESP systems, outfitted with real-time sensors that monitor variables such as voltage, particulate concentration, and gas temperature. These platforms enable data-driven adjustments, minimizing unscheduled downtime and optimizing energy use. Additionally, AI and machine learning algorithms are increasingly embedded into controls, allowing predictive adjustments to rapping intervals and voltage levels based on operational trends. Material innovation represents another key advancement. Modern ESP units now feature corrosion-resistant alloys, ceramic coatings, and high-performance power supplies that can endure acidic and high-temperature environments. These enhancements significantly prolong component lifespan and reduce maintenance intervals, notably in harsh industrial settings. Hybrid designs—combining wet and dry precipitation methods—are gaining traction, especially for ultrafine particulate removal where traditional ESPs fall short.

Retrofitting solutions offer a cost-effective route to modernization. Modular ESP upgrades—including high-frequency switch-mode power modules and sectional voltage controls—allow legacy plants to boost performance without full system replacement. Such modular setups can handle variable load conditions while adhering to evolving emission norms. Finally, compact and scalable ESP variants are becoming more prevalent in niche applications, such as offshore industries and marine exhaust cleaning. These compact models offer high particulate capture efficacy with smaller spatial footprints, incorporating advanced rapping mechanisms and digital feedback loops. For decision-makers, these emerging technologies underscore a shift toward intelligent, resilient, and sustainable particulate emission control infrastructure.

• In September 2023, a major provider delivered an ESP unit for a 700,000-tonne chemical pulp project in China, enhancing emissions control in high-volume pulp production.

• In early 2024, plate ESP technology was launched capable of removing particles larger than 5 micrometers with up to 99.95% efficiency—targeted for power generation and cement applications.

• In 2023, over 19,000 ESP units were installed globally, up 9% from the prior year; Asia-Pacific accounted for more than 11,500 of those units, led by China, India, and South Korea.

• In 2023, more than 6,500 ESP units shipped with SCADA connectivity, enabling real-time emission monitoring and reducing unscheduled downtime by nearly 24%.

The scope of the Electrostatic Precipitators (ESP) Market Report encompasses a comprehensive evaluation across product types, functionalities, regional divisions, application sectors, and technological innovations. It examines the full range of ESP systems—dry, wet, tubular, and hybrid configurations—analyzing usage in power generation, cement, metals, chemicals, waste-to-energy, marine, and specialty sectors. The report segments by design (e.g., plate versus tubular), by scale (compact modular units versus large industrial installations), and by technological enhancements (advanced materials, digital controls, retrofitting modules).

Geographically, the report covers all major markets—including North America, Europe, Asia-Pacific, South America, and Middle East & Africa—providing detailed insights into regional deployment volumes, infrastructure drivers, regulatory landscapes, and innovation hubs. It also explores emerging niches such as offshore installations, marine exhaust systems, and retrofit modernization in legacy plants. Moreover, the report delves into value chain considerations—highlighting suppliers of smart controls, electrode materials, monitoring platforms, and EPC partnerships. Strategic areas include digital transformation, performance diagnostics, and modular design adoption. Tailored for decision-makers, the report delivers actionable clarity on market breadth, emerging segments, and technological trajectories that define the current and future ESP landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2486.27 Million |

|

Market Revenue in 2032 |

USD 3273.95 Million |

|

CAGR (2025 - 2032) |

3.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

FLSmidth A/S, Mitsubishi Hitachi Power Systems, Ltd., General Electric Company, Siemens Energy AG, Babcock & Wilcox Enterprises, Inc., Thermax Limited, Hamon Group, Feida Group Company Limited, Balcke-Dürr GmbH, KC Cottrell Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |