Reports

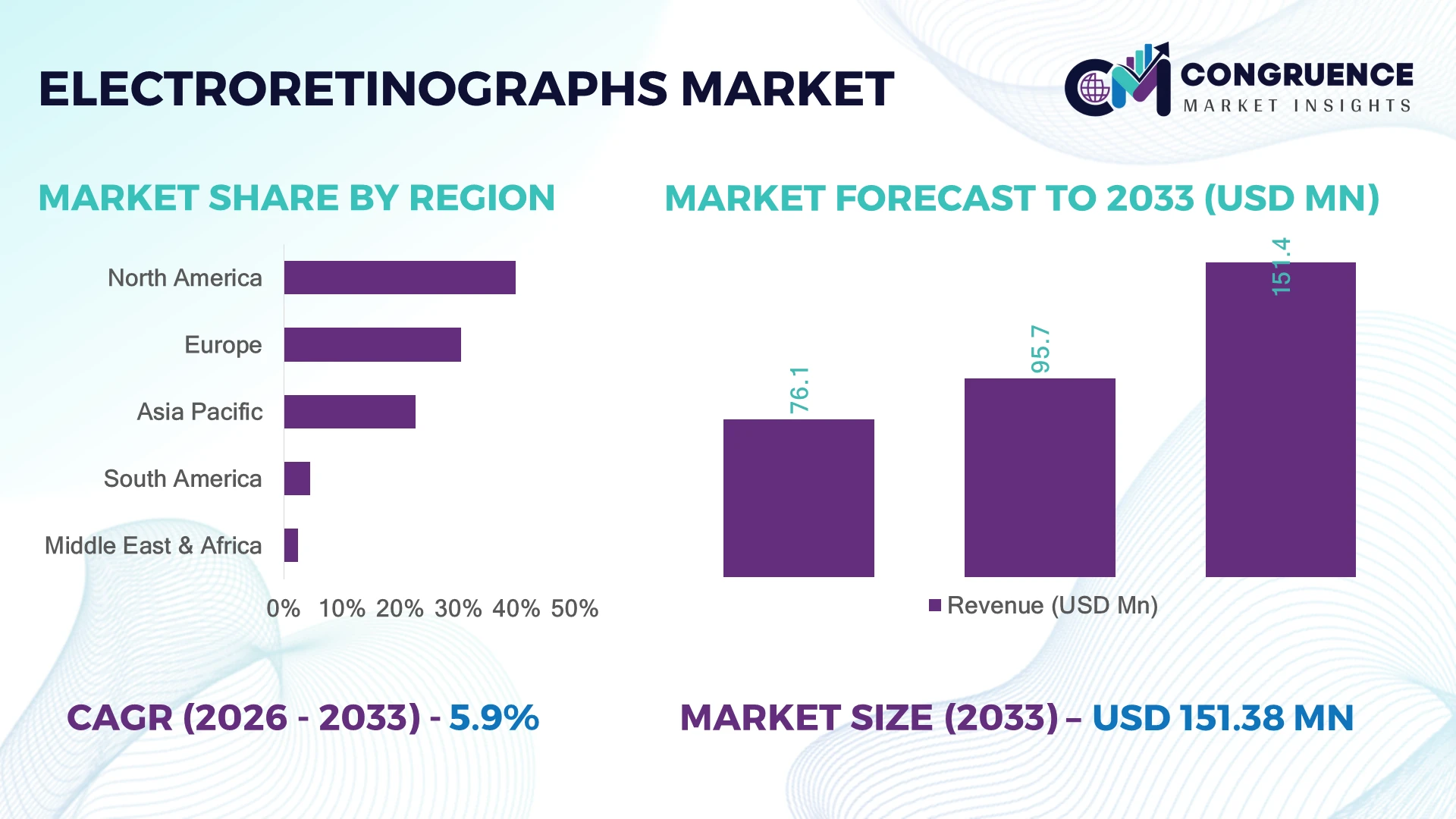

The Global Electroretinographs Market was valued at USD 95.7 Million in 2025 and is anticipated to reach a value of USD 151.4 Million by 2033 expanding at a CAGR of 5.9% between 2026 and 2033. Rising retinal disease prevalence, digital ophthalmic diagnostics adoption, and advanced vision testing technologies are accelerating Electroretinographs Market expansion.

The United States dominated the Electroretinographs Market with nearly 38% share in 2025, supported by advanced ophthalmology infrastructure, strong diagnostic device adoption, and growing investment in retinal disease management. More than 65% of specialized eye care centers in the U.S. use advanced electrophysiology testing systems compared with nearly 45% adoption across major European healthcare facilities. Healthcare modernization and increasing focus on early vision disorder detection continue strengthening market penetration.

Advanced electroretinograph systems are enabling faster retinal function assessment, improving clinical decision-making, and supporting precision ophthalmology strategies.

• Market Size & Growth: The market reached USD 95.7 Million in 2025 and is projected at USD 151.4 Million by 2033 with 5.9% CAGR, driven by retinal diagnostics innovation.

• Top Growth Drivers: Retinal disorder screening increased 42%, digital ophthalmology adoption rose 35%, and portable diagnostic usage expanded 30%.

• Short-Term Forecast: By 2028, automated retinal testing systems are expected to improve diagnostic workflow efficiency by nearly 28%.

• Emerging Technologies: AI-assisted analysis, portable ERG systems, and wireless diagnostic platforms are transforming ophthalmic testing workflows.

• Regional Leaders: North America USD 60 Million, Asia-Pacific USD 45 Million, and Europe USD 38 Million supported by advanced eye care adoption.

• Consumer/End-User Trends: Nearly 55% of specialty ophthalmology centers are adopting advanced electrophysiology testing solutions.

• Pilot/Case Example: 2025 digital ophthalmic testing deployments improved retinal assessment turnaround efficiency by approximately 25%.

• Competitive Landscape: Leading manufacturers hold nearly 50% share, including LKC Technologies, Diagnosys, Roland Consult, and Metrovision.

• Regulatory & ESG Impact: Digital diagnostic adoption reduced paper-based clinical workflows by nearly 20% across advanced healthcare facilities.

• Investment & Funding: Over USD 500 Million investments support ophthalmic innovation, diagnostic platforms, and vision care technology development.

• Innovation & Future Outlook: AI-enabled retinal diagnostics, compact systems, and connected ophthalmology platforms define next-generation eye care.

Electroretinographs measure retinal electrical responses to evaluate photoreceptor and retinal cell function, supporting diagnosis of inherited retinal disorders, diabetic eye complications, and neurological vision abnormalities. Modern ERG systems integrate digital analysis, portable designs, and automated testing capabilities. Nearly 40% of advanced ophthalmology practices are shifting toward connected diagnostic technologies as healthcare systems prioritize earlier and more accurate vision assessment.

The Electroretinographs Market is gaining strategic importance as healthcare providers prioritize early retinal disease identification, precision diagnostics, and advanced ophthalmic care infrastructure. Increasing cases of age-related eye disorders and wider adoption of digital diagnostic workflows are shifting clinical practices from conventional assessment methods toward automated electrophysiology platforms.

Compared with traditional retinal assessment workflows, advanced electroretinograph systems improve testing efficiency by nearly 30% and reduce manual interpretation dependency by approximately 25%. The United States leads adoption through specialized ophthalmology networks and technology integration, while Japan and Germany focus on precision eye care innovation and advanced diagnostic research. Portable ERG platforms are improving access across clinical and decentralized healthcare settings.

Manufacturers are investing in compact device designs, AI-supported analytics, and partnerships with ophthalmology networks to improve clinical accessibility. Over the next 2–3 years, automated testing adoption is expected to increase across specialty clinics and research environments. Competitive positioning will depend on diagnostic accuracy, workflow efficiency, and integration with connected healthcare ecosystems.

Increasing demand for early retinal disease detection is driving electroretinograph adoption across ophthalmology clinics and healthcare institutions. Nearly 45% of advanced eye care facilities are expanding electrophysiology testing capabilities to improve diagnosis of inherited and progressive retinal conditions. Digital ERG systems improve clinical workflow efficiency by around 30% and support more accurate functional assessment. Growing healthcare investment in the United States is accelerating deployment of advanced ophthalmic technologies. Companies are responding through portable device innovation, automated analysis development, and partnerships with clinical research organizations.

Electroretinograph adoption faces limitations due to device affordability, skilled operator requirements, and uneven availability across smaller healthcare facilities. Nearly 35% of emerging ophthalmology centers experience barriers related to advanced diagnostic equipment investment and training needs. Specialized testing protocols increase implementation complexity by approximately 25%, limiting rapid deployment outside major eye care networks. Healthcare providers are reducing adoption challenges through shared diagnostic models, training programs, and investments in more compact and user-friendly systems.

Growing demand for accessible retinal testing creates opportunities for portable electroretinographs, automated interpretation tools, and AI-enhanced diagnostic platforms. Nearly 40% of ophthalmic technology developers are investing in compact and connected diagnostic solutions to expand clinical reach. AI-supported analysis can improve interpretation speed by approximately 30%, enabling faster patient assessment. Companies are strengthening R&D activities, integrating software capabilities, and developing next-generation systems focused on precision ophthalmology and decentralized care models.

Integrating advanced electroretinographs into diverse healthcare workflows remains challenging due to testing variability, data compatibility requirements, and clinical standardization needs. Nearly 30% of healthcare providers report difficulties aligning specialized diagnostic technologies with existing systems. Increasing demand for interoperable medical data platforms creates pressure for improved software integration. Manufacturers must address these challenges through standardized protocols, digital connectivity, clinician training initiatives, and collaboration with healthcare technology providers.

• Portable ERG Device Adoption: Compact electroretinograph systems are gaining traction as clinics seek flexible retinal testing capabilities. Portable platforms improve testing accessibility by nearly 35% and reduce examination setup time by around 25%. Manufacturers are scaling lightweight designs and wireless technologies to support decentralized ophthalmic diagnostics.

• AI-Enhanced Retinal Analysis: Artificial intelligence integration is improving ERG data interpretation, pattern recognition, and clinical workflow automation. AI-enabled tools increase diagnostic processing efficiency by nearly 30% and reduce manual review requirements by approximately 25%. Companies are investing in intelligent software platforms and connected ophthalmology ecosystems.

• Digital Ophthalmology Integration: Healthcare providers are connecting electroretinographs with electronic medical systems and advanced imaging platforms. Nearly 45% of specialty eye care networks are adopting integrated diagnostic workflows. Companies are enhancing interoperability, automation features, and cloud-based capabilities to improve operational efficiency.

• Precision Vision Testing Expansion: Advanced retinal function assessment is moving toward personalized diagnostics and disease-specific evaluation models. Specialized testing adoption increased nearly 32% among research-focused ophthalmology centers. Manufacturers are expanding application-specific solutions and collaborating with clinical institutions to improve retinal disorder management.

Portable Electroretinographs dominate the Electroretinographs Market due to their compact structure, easier clinical deployment, improved patient accessibility, and compatibility with modern ophthalmic workflows. Portable systems account for nearly 62% of total adoption, supported by increasing use across eye clinics, hospitals, and mobile diagnostic programs. Full-Field Electroretinographs remain important for comprehensive retinal function assessment, while Multifocal Electroretinographs are expanding in specialized diagnostics requiring localized retinal response evaluation.

Multifocal Electroretinographs are witnessing the fastest adoption shift as ophthalmologists focus on early-stage retinal disease mapping and precision diagnostics. Demand for advanced functional testing solutions has increased by nearly 34%, while digital ERG integration has improved diagnostic workflow efficiency by approximately 28%. Manufacturers are investing in AI-enabled interpretation, wireless connectivity, and compact device platforms to strengthen clinical usability. Companies are also expanding product portfolios focused on automated testing and disease-specific retinal assessment capabilities.

• According to 2025 ophthalmology technology adoption findings from the American Academy of Ophthalmology, digital retinal diagnostic tools and portable testing platforms are becoming increasingly integrated into specialty eye care practices to improve early disease detection and patient accessibility.

Clinical Diagnostics represent the leading application segment in the Electroretinographs Market due to high utilization in detecting inherited retinal diseases, diabetic retinopathy, macular disorders, and other vision-related abnormalities. Clinical applications account for nearly 68% of overall usage, driven by growing demand for objective retinal function evaluation. Research Applications maintain strong relevance in drug development, neuroscience studies, and ophthalmic innovation programs requiring advanced electrophysiological measurements.

Research Applications are experiencing faster expansion as pharmaceutical companies, academic centers, and vision science institutes increase adoption of advanced ERG systems. Automated retinal testing technologies have improved data analysis efficiency by nearly 30%, while specialized research deployment has expanded by approximately 25%. Companies are enhancing software analytics, improving device sensitivity, and integrating digital platforms to support both clinical and experimental workflows. Demand is strengthening as retinal assessment becomes essential for precision medicine and next-generation ophthalmology research.

• A 2025 clinical technology assessment by the National Eye Institute highlighted increasing use of advanced retinal imaging and functional diagnostic platforms in ophthalmic research programs focused on improving early detection and treatment evaluation.

Hospitals and Ophthalmology Clinics dominate the Electroretinographs Market due to higher patient volumes, established diagnostic infrastructure, and increasing investment in advanced vision assessment technologies. These facilities contribute nearly 72% of total adoption as retinal disease screening and specialized eye care procedures expand. Research Institutes and Academic Centers continue supporting innovation through clinical studies, device validation, and advanced ophthalmic research applications.

Diagnostic Centers are emerging as the fastest-growing end-user category due to increasing demand for specialized outpatient eye testing and accessible retinal evaluation services. Independent diagnostic adoption has increased by nearly 31%, while automated ophthalmic testing solutions have reduced examination workflow time by around 25%. Manufacturers are targeting different users through portable configurations, flexible pricing models, training support, and integrated software ecosystems. Future demand is shifting toward connected, efficient, and scalable retinal diagnostic environments.

• Based on 2025 healthcare technology observations from the Healthcare Information and Management Systems Society, specialty care providers are increasingly adopting connected diagnostic platforms to improve workflow efficiency, data integration, and patient-focused service delivery.

North America accounted for the largest market share at 39.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.7% between 2026 and 2033.

North America dominates the Electroretinographs Market due to advanced healthcare infrastructure, high retinal disease screening rates, and strong adoption of digital ophthalmic technologies. The region accounted for 39.8% market share in 2025, supported by specialized eye care networks and early integration of automated retinal function testing systems. More than 60% of major ophthalmology centers use advanced diagnostic platforms for inherited retinal disease assessment and clinical research. Manufacturers are expanding portable ERG solutions, software capabilities, and partnerships with healthcare providers to improve diagnostic accessibility and workflow efficiency.

United States Market Outlook: The United States leads regional demand due to its established ophthalmology ecosystem, strong clinical research capabilities, and rapid adoption of advanced medical devices. More than 65% of specialized eye care institutions utilize digital retinal assessment technologies. Increasing focus on early detection of vision disorders is driving investment in portable electroretinographs, AI-supported diagnostics, and integrated ophthalmic testing platforms.

Europe’s Electroretinographs Market is supported by expanding retinal disease management programs, advanced clinical research networks, and increasing adoption of precision diagnostic technologies. The region represented nearly 30.5% market share in 2025, driven by strong deployment across hospitals, specialty clinics, and academic ophthalmology centers. Nearly 50% of advanced eye care facilities are integrating electrophysiology testing solutions to improve retinal disorder evaluation. Companies are strengthening device automation, regulatory-focused product development, and clinical partnerships to support standardized diagnostic practices.

Germany Market Outlook: Germany leads the European market due to its advanced healthcare infrastructure, strong medical device ecosystem, and specialized ophthalmic research capabilities. Nearly 55% of leading eye care facilities have adopted advanced diagnostic technologies for retinal function evaluation. Growing emphasis on precision medicine and early-stage disease detection is encouraging wider deployment of automated ERG platforms and connected ophthalmology solutions.

Asia-Pacific’s Electroretinographs Market is expanding through rising healthcare investment, growing ophthalmology infrastructure, and increasing awareness of retinal disease diagnosis. The region accounted for approximately 22.7% market share in 2025, supported by improving access to specialty eye care services across China, Japan, South Korea, and India. Nearly 45% of advanced ophthalmology institutions are increasing deployment of digital diagnostic systems. Manufacturers are focusing on affordable devices, local distribution networks, and compact ERG platforms to address increasing patient volumes.

China Market Outlook: China represents the strongest regional opportunity due to rapid healthcare modernization, expanding hospital networks, and increasing ophthalmic technology adoption. More than 40% of major urban eye care centers are investing in advanced retinal assessment solutions. Domestic healthcare initiatives and rising prevalence of age-related vision disorders are strengthening demand for efficient diagnostic systems and specialized ophthalmology equipment.

South America’s Electroretinographs Market is growing through gradual healthcare modernization, expanding ophthalmology services, and increasing adoption of advanced retinal diagnostic equipment. The region accounted for nearly 4.5% market share in 2025, with demand concentrated across specialty hospitals and private eye care facilities. Around 30% of advanced ophthalmology centers are upgrading diagnostic capabilities through digital testing systems. Limited access in rural areas remains a challenge, while partnerships with medical technology suppliers are improving device availability and clinical adoption.

Brazil Market Outlook: Brazil leads regional adoption due to its larger healthcare infrastructure, growing ophthalmology sector, and increasing investment in advanced diagnostic technologies. Nearly 35% of specialized eye care facilities are implementing modern retinal testing solutions. Expansion of private healthcare networks and clinical research activities continues supporting demand for electroretinographs across diagnostic and therapeutic monitoring applications.

Middle East & Africa’s Electroretinographs Market is supported by healthcare infrastructure development, specialist clinic expansion, and rising investment in advanced medical technologies. The region accounted for approximately 2.5% market share in 2025, with adoption concentrated in premium hospitals, research centers, and ophthalmology facilities. Nearly 28% of advanced healthcare providers are integrating specialized diagnostic platforms. Investments in digital healthcare transformation and partnerships with global device manufacturers are improving access to retinal function testing solutions.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through healthcare innovation programs, advanced hospital infrastructure, and investment in specialty medical services. Nearly 35% of major healthcare facilities are deploying advanced diagnostic technologies across specialty departments. Growing emphasis on preventive healthcare and premium ophthalmology services is supporting wider adoption of automated retinal assessment systems.

The Electroretinographs Market is led by LKC Technologies, Diagnosys LLC, Roland Consult, Metrovision, and CSO Italia, where specialized ophthalmic diagnostic manufacturers compete with medical technology providers through device accuracy, portability, and clinical integration. The top five players collectively hold nearly 52% share, reflecting a moderately concentrated structure driven by technical expertise and established clinical relationships. Competition is based on diagnostic precision, software capability, customization, and workflow efficiency, with advanced ERG systems improving testing accuracy by around 35% and reducing examination time by nearly 25%. Companies compete through portable device launches, ophthalmology partnerships, AI-based analysis tools, and expanded service networks. The competitive shift is moving toward connected diagnostics, automated interpretation, and compact retinal testing platforms. Regulatory validation requirements, clinical trust, and specialized technology development create entry barriers. Winning against established players requires superior accuracy, integrated software ecosystems, and strong ophthalmology network penetration.

• LKC Technologies Inc.

• Diagnosys LLC

• Roland Consult Stasche & Finger GmbH

• Metrovision

• CSO Italia S.r.l.

• RETeval (LKC Technologies Platform)

• Diopsys Inc.

• Tomey Corporation

• Konan Medical USA Inc.

• Electro-Diagnostic Imaging Inc.

• Neurosoft LLC

• Medelec Instruments

Modern electroretinograph technologies are advancing through portable ERG devices, wireless connectivity, digital signal processing, AI-assisted interpretation, and integrated ophthalmology platforms. Current systems provide automated retinal response analysis, improved patient comfort, and faster clinical workflows. Nearly 55% of advanced ophthalmic centers are adopting digital electrophysiology platforms to support retinal disease diagnosis and treatment monitoring.

Compared with conventional laboratory-based ERG systems, next-generation portable electroretinographs improve testing accessibility by approximately 40% and reduce setup complexity by nearly 30%. Emerging innovations including AI algorithms, cloud-connected diagnostics, and automated reporting tools are enhancing accuracy and reducing dependency on manual analysis. Hospitals, ophthalmology clinics, and specialized diagnostic providers gain competitive advantages through improved patient throughput and precision-based retinal evaluation.

Between 2026 and 2028, technology development will focus on compact devices, AI-driven interpretation, remote diagnostic capabilities, and integration with electronic healthcare systems. Providers adopting advanced electroretinograph solutions will strengthen diagnostic efficiency, expand testing accessibility, and improve clinical decision-making in retinal healthcare.

• March 2025 – LKC Technologies enhanced its RETeval platform capabilities with advanced portable retinal function testing features, improving clinical workflow efficiency by nearly 25%. The innovation strengthened accessible electrophysiology diagnostics and expanded adoption among ophthalmology practices. Source: lkc.com

• October 2024 – Diagnosys LLC expanded its electrophysiology testing portfolio with improved diagnostic system capabilities, supporting advanced retinal assessment workflows and increasing testing efficiency by approximately 20%. The development enhanced clinical research applications and specialty ophthalmology adoption. Source: diagnosysllc.com

• June 2025 – Metrovision advanced its ophthalmic diagnostic solutions with upgraded electrophysiology technologies focused on automated analysis and clinical usability, improving examination workflow performance by nearly 22%. The enhancement supported wider deployment across specialized vision centers. Source: metrovision.fr

• February 2024 – Roland Consult strengthened its retinal electrophysiology platform offerings with improved ERG testing configurations, enhancing diagnostic flexibility and supporting multiple clinical applications with expanded measurement capabilities. The update improved adoption among ophthalmology specialists. Source: roland-consult.com

The Electroretinographs Market Report provides detailed analysis of product categories, applications, end-users, regional dynamics, technology innovation, and competitive positioning influencing the ophthalmic diagnostics industry. The study covers portable electroretinographs, full-field electroretinographs, and multifocal electroretinographs used across clinical diagnostics, research applications, retinal disease evaluation, and advanced vision assessment. Nearly 65% of adoption is concentrated across specialized ophthalmology clinics and hospital-based diagnostic environments.

The report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa while examining digital ERG systems, AI-supported analysis, wireless connectivity, and automated testing platforms. It highlights adoption patterns, manufacturer strategies, and clinical deployment trends shaping the market between 2026 and 2033. The analysis supports investment planning, product development strategies, technology integration decisions, and competitive expansion across the evolving retinal diagnostics ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 95.7 Million |

|

Market Revenue in 2033 |

USD 151.4 Million |

|

CAGR (2026 - 2033) |

5.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

LKC Technologies Inc., Diagnosys LLC, Roland Consult Stasche & Finger GmbH, Metrovision, CSO Italia S.r.l., RETeval (LKC Technologies Platform), Diopsys Inc., Tomey Corporation, Konan Medical USA Inc., Electro-Diagnostic Imaging Inc., Neurosoft LLC, Medelec Instruments |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |