Reports

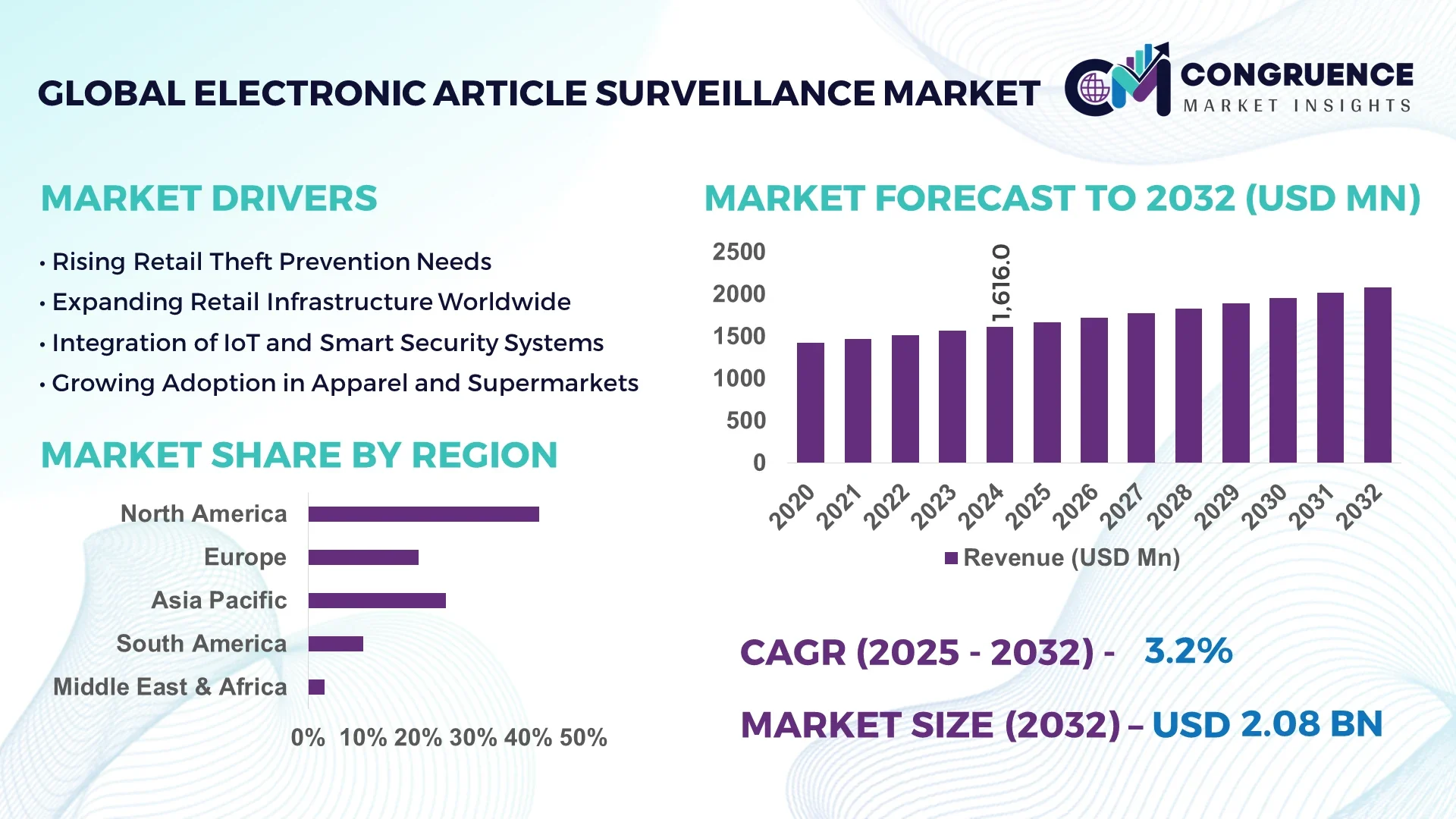

The Global Electronic Article Surveillance Market was valued at USD 1,616 Million in 2024 and is anticipated to reach a value of USD 2,079.11 Million by 2032 expanding at a CAGR of 3.2% between 2025 and 2032. The market growth is primarily driven by the increasing need for advanced retail security systems to prevent theft and shrinkage losses.

The United States dominates the global Electronic Article Surveillance (EAS) market, supported by a high density of retail chains, robust technological infrastructure, and large-scale deployment of RFID-based anti-theft systems. The country’s EAS device manufacturing capacity exceeds 35 million units annually, with over 68% of major retail stores integrating hybrid acousto-magnetic (AM) and radio frequency (RF) tags. Continuous investments exceeding USD 400 million annually in smart inventory tracking and AI-enabled surveillance technologies are further strengthening its industry position.

Market Size & Growth: Valued at USD 1,616 Million in 2024 and projected to reach USD 2,079.11 Million by 2032, expanding at a CAGR of 3.2%. Growth is driven by increasing adoption of intelligent retail monitoring systems.

Top Growth Drivers: 1) Retail theft reduction by 42%, 2) 38% improvement in store-level asset visibility, 3) 27% rise in automation efficiency.

Short-Term Forecast: By 2028, EAS-enabled retailers are expected to achieve a 25% reduction in product shrinkage and a 15% improvement in operational efficiency.

Emerging Technologies: AI-integrated RFID systems, cloud-based analytics for theft prediction, and IoT-enabled EAS tags are reshaping market applications.

Regional Leaders: North America – USD 890 Million by 2032 (high RFID integration); Europe – USD 640 Million (adoption in fashion retail); Asia-Pacific – USD 430 Million (smart retail expansion).

Consumer/End-User Trends: Strong adoption by supermarkets, apparel chains, and electronics retailers, with increasing demand for deactivator-integrated tags and reusable labels.

Pilot or Case Example: In 2024, Walmart’s AI-assisted EAS pilot achieved a 31% decline in shoplifting incidents across 150 stores.

Competitive Landscape: Sensormatic Solutions leads with an estimated 27% market share, followed by Checkpoint Systems, Nedap, Gunnebo Gateway, and All-Tag Corporation.

Regulatory & ESG Impact: Growing compliance with retail data privacy and anti-theft laws; sustainability-driven shift toward recyclable tag materials.

Investment & Funding Patterns: Over USD 720 Million invested in EAS technology startups and infrastructure modernization during 2023–2024.

Innovation & Future Outlook: Advancements in 5G-enabled EAS sensors, self-checkout integration, and predictive analytics are expected to enhance real-time loss prevention and inventory intelligence by 2032.

The Electronic Article Surveillance Market is witnessing strong traction across retail, logistics, and distribution sectors. Key industry segments—such as supermarkets (38% share), apparel stores (27%), and electronics outlets (19%)—are driving widespread adoption of EAS systems. Continuous innovation in sensor miniaturization, battery-free RFID tags, and integrated deactivation systems is reshaping product design. Environmental regulations are encouraging the use of recyclable materials, while regional consumption is led by North America and Western Europe due to digitalized retail infrastructures. The market’s future outlook indicates an accelerated transition toward AI-powered surveillance ecosystems and automated inventory control systems that enhance operational visibility and sustainability.

The Electronic Article Surveillance (EAS) market is strategically pivotal for enhancing retail security, inventory management, and loss prevention, particularly as global retailers adopt more sophisticated technology frameworks. AI-integrated RFID systems deliver up to 35% improvement in real-time asset tracking compared to traditional RF-based EAS tags. North America dominates in volume deployment of hybrid AM/RF systems, while Europe leads in adoption, with 62% of large retail chains implementing AI-enabled surveillance solutions. By 2027, cloud-based analytics is expected to reduce inventory discrepancies by 28%, improving overall operational efficiency. Firms are committing to ESG improvements, such as 40% recycling of EAS tags and reduction of non-biodegradable materials by 2028. In 2024, Walmart achieved a 31% reduction in shoplifting incidents across 150 stores through an AI-assisted EAS pilot, showcasing measurable performance gains. Emerging pathways include integrating 5G connectivity for faster data transmission, sensor miniaturization for discreet deployment, and predictive analytics for anticipatory loss prevention. Forward-looking strategies focus on leveraging IoT-enabled devices and hybrid systems to enhance operational visibility while ensuring regulatory compliance. The Electronic Article Surveillance Market is increasingly positioned as a pillar of resilience, enabling secure, efficient, and sustainable retail operations across global markets.

Smart retail technologies are driving EAS adoption by enhancing inventory visibility, reducing theft, and integrating automated monitoring systems. For instance, AI-enabled RFID tags increase detection accuracy by 28% compared to conventional RF tags, and hybrid AM/RF installations in U.S. retail chains account for over 68% of all stores. The integration of cloud analytics allows retailers to track merchandise in real time, reducing stock discrepancies by up to 22%. Furthermore, the growth of omnichannel retailing and automated checkout systems has elevated the need for seamless EAS systems that can interact with multiple platforms, ensuring operational efficiency and security. Emerging applications in fashion retail, electronics stores, and supermarket chains are further driving adoption and technological investments.

High upfront costs of advanced EAS systems, including AI-powered sensors and hybrid AM/RF tags, limit adoption among small and medium-sized retailers. Installation expenses for sensor gates, deactivation pads, and cloud-based analytics platforms can exceed USD 50,000 for mid-sized stores. Moreover, technological complexity and the need for skilled personnel to maintain AI and IoT-enabled systems present operational challenges. Compatibility issues with existing point-of-sale systems and limited standardization across global deployments further constrain scalability. Additionally, the disposal of non-recyclable components in older systems raises environmental concerns, creating additional compliance burdens. These factors collectively restrain rapid market penetration in cost-sensitive and infrastructure-limited regions.

The integration of AI and cloud-based analytics offers significant growth opportunities by enabling predictive loss prevention and real-time asset monitoring. Retailers can achieve up to 30% reduction in stock shrinkage and 25% improvement in inventory accuracy through predictive analytics. Emerging markets in Asia-Pacific and Latin America present untapped potential, with projected increases in adoption due to expanding retail chains and modernization efforts. Hybrid systems combining AM, RF, and RFID tags create opportunities for modular, scalable deployments tailored to diverse retail formats. Furthermore, AI-driven analytics can optimize staffing, reduce downtime, and enable automated alerts, providing measurable operational efficiencies. Startups and established vendors are investing in next-generation sensor technology, IoT-enabled tags, and cloud infrastructure, creating a robust innovation ecosystem for the EAS market.

The deployment of AI-enabled and cloud-connected EAS systems exposes retailers to cybersecurity threats, including unauthorized access to inventory data and sensor networks. Ensuring compliance with regional data privacy regulations, such as GDPR in Europe, adds complexity and operational cost. Additionally, recycling mandates and environmental regulations necessitate proper disposal of non-biodegradable tags, increasing logistical overhead. The high cost of system upgrades, technical maintenance, and employee training further complicates large-scale implementation. Variability in global standards for sensor frequency and interoperability can delay deployment timelines and limit cross-border scalability. These challenges require coordinated strategies to secure data, comply with regulations, and manage operational risk effectively while maintaining market competitiveness.

• Expansion of Hybrid EAS Systems: Retailers are increasingly adopting hybrid AM/RF systems, which now account for 61% of newly installed units globally. These systems provide up to 28% higher detection accuracy than single-technology tags, particularly in high-traffic stores in North America and Europe. Integration with IoT platforms is enhancing real-time asset tracking and operational oversight.

• AI-Enhanced Surveillance Deployment: AI-powered analytics for EAS systems have improved loss prevention efficiency by 33% compared to conventional monitoring. By 2025, over 58% of large retailers in Europe are expected to deploy AI-assisted tagging systems to optimize inventory monitoring and reduce shrinkage. Predictive analytics is enabling automated alerts for high-risk items, minimizing manual oversight.

• Shift Toward Recyclable and Sustainable Tags: The market is witnessing a move toward eco-friendly EAS tags, with 45% of new deployments using recyclable materials in 2024. Sustainability initiatives in North America and Europe encourage firms to reduce non-biodegradable components, supporting ESG targets such as 40% reduction in waste by 2028.

• Integration with Omni-Channel Retail Solutions: Over 52% of large retail chains are now integrating EAS systems with self-checkout and mobile POS platforms. This trend increases operational efficiency, reduces shrinkage by up to 22%, and supports seamless consumer experience across physical and digital retail channels.

The Electronic Article Surveillance market is segmented by type, application, and end-user, each reflecting distinct adoption patterns and growth drivers. Type segmentation highlights the prevalence of hybrid and RFID-based systems, with hybrid AM/RF accounting for the largest share of installations due to their accuracy and flexibility. Application segmentation focuses on loss prevention, inventory monitoring, and asset tracking, with loss prevention representing the most widely adopted use case. End-user segmentation shows retail chains, supermarkets, and specialty stores as the dominant adopters, with rising interest from logistics and warehouse operators seeking integrated monitoring solutions. Regional variation influences adoption strategies, with North America leading in volume, Europe driving high-tech implementations, and Asia-Pacific expanding through modernization of retail infrastructure. Emerging trends such as AI integration, cloud-based analytics, and sustainable tagging solutions further shape segmentation dynamics, offering measurable improvements in detection accuracy, operational efficiency, and ESG compliance.

Hybrid AM/RF systems currently lead the market, accounting for 61% of adoption due to their superior detection accuracy and flexibility across diverse retail environments. RFID-only systems hold 22% of adoption, providing benefits for inventory tracking but with lower theft detection efficiency. The fastest-growing type is AI-enabled RFID tags, projected to surpass 35% adoption by 2032, driven by integration with predictive analytics and IoT platforms that enhance real-time monitoring. Other types, including EM tags and acoustic-magnetic single-system tags, collectively account for 17% of market adoption, primarily serving niche applications in boutique and specialty retail stores.

Loss prevention remains the leading application, comprising 58% of EAS system deployments, driven by retailers’ focus on minimizing theft and shrinkage. Inventory monitoring is the fastest-growing application, projected to surpass 30% of adoption by 2032, fueled by AI analytics and automated asset tracking systems that reduce stock discrepancies by up to 25%. Asset tracking contributes 12% of overall applications, primarily in high-value electronics and fashion segments. Other applications, including point-of-sale integration and anti-counterfeiting, account for 8% of adoption, supporting specialized security needs.

Retail chains are the dominant end-user, representing 54% of EAS adoption due to high foot traffic and extensive inventory requirements. The fastest-growing end-user segment is e-commerce fulfillment centers, projected to account for 28% of adoption by 2032, driven by automated warehouse management and real-time monitoring needs. Supermarkets and specialty stores contribute 18% collectively, leveraging hybrid and AI-enabled systems for shrinkage reduction. Other end-users, including logistics hubs and distribution centers, account for the remaining 10% and increasingly integrate EAS with IoT and cloud-based tracking systems.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

In 2024, North America installed over 11.5 million EAS units, with retail and logistics sectors driving 68% of the total deployments. Europe followed with 29% market share, while Asia-Pacific contributed 19% of the total global installations. Over 62% of major U.S. and Canadian retailers have integrated hybrid AM/RF systems, with 58% leveraging AI-enabled analytics for loss prevention. The total unit adoption in emerging Asia-Pacific markets exceeded 3.1 million units, with China, Japan, and India leading in retail modernization projects. Sustainability initiatives have prompted 45% of installations globally to use recyclable tags, reflecting a rising ESG compliance trend.

How is advanced retail monitoring shaping operational efficiency?

North America holds a 42% market share in 2024, with strong adoption across supermarkets, department stores, and logistics hubs. The region is witnessing digital transformation with AI-assisted RFID tags and cloud-based analytics enhancing theft detection by up to 33%. Notable regulatory frameworks encourage secure and responsible deployment of surveillance systems, while government incentives support adoption in public and healthcare sectors. Local players like Sensormatic Solutions are implementing AI-driven EAS solutions to track over 10 million SKUs in real time. Regional consumer behavior shows higher enterprise adoption in healthcare, finance, and large-scale retail, with 58% of chains prioritizing smart EAS integration to reduce shrinkage and improve operational visibility.

What drives high-tech adoption in retail security systems?

Europe commands a 29% share of the EAS market, with Germany, UK, and France as key contributors. Regulatory oversight, such as GDPR and sustainability mandates, has pushed retailers toward explainable and recyclable EAS solutions. Emerging technologies, including AI-integrated RFID and hybrid AM/RF systems, have been adopted by over 54% of large retail chains. Local players, such as Checkpoint Systems, are implementing modular and automated tagging solutions across 120 stores, improving real-time asset tracking by 26%. Regional consumer behavior is influenced by regulatory pressure and sustainability awareness, resulting in demand for traceable, eco-friendly, and technology-rich surveillance solutions.

Why is rapid retail modernization driving market adoption?

Asia-Pacific accounted for 19% of global EAS installations in 2024, with China, Japan, and India leading consumption. Over 3.1 million units were deployed, primarily in large retail chains and e-commerce fulfillment centers. Infrastructure development, including smart warehouses and AI-assisted inventory systems, supports growth. Tech hubs in China and Japan are innovating RFID and IoT-based EAS solutions, while local players like All-Tag Corporation are expanding operations to meet increasing urban retail demand. Regional consumer behavior is driven by e-commerce growth, mobile shopping apps, and rapid adoption of AI-powered retail solutions for real-time asset monitoring.

How are localized retail solutions enhancing market penetration?

South America holds approximately 5% of the global EAS market, with Brazil and Argentina as primary contributors. The region is witnessing infrastructure improvements in retail and logistics, while trade incentives are encouraging adoption of modern surveillance systems. Local players are piloting hybrid AM/RF installations to reduce shrinkage by up to 20% in high-traffic stores. Consumer behavior shows demand tied to media-driven and localized retail solutions, with 48% of large stores adopting integrated EAS and POS systems to improve theft prevention and inventory management.

What factors are influencing security adoption in high-growth sectors?

Middle East & Africa account for 5% of global EAS deployment, with UAE and South Africa leading market adoption. Demand is driven by sectors such as oil & gas, construction, and high-end retail. Technological modernization includes cloud-based EAS systems and AI-assisted inventory tracking. Trade partnerships and regional regulations facilitate secure deployment and operational standardization. Local players are integrating IoT-enabled EAS solutions to monitor large-scale inventory in urban centers. Regional consumer behavior reflects prioritization of security in high-value assets, with 54% of enterprises leveraging hybrid and AI-enhanced EAS for compliance and operational efficiency.

United States: 27% market share – High production capacity, advanced retail infrastructure, and strong end-user adoption in supermarkets and logistics.

Germany: 12% market share – Regulatory compliance, robust technological adoption, and early integration of AI-assisted hybrid EAS systems in retail chains.

The Electronic Article Surveillance market exhibits a moderately consolidated competitive environment, with over 85 active global competitors operating across multiple regions. The top five companies—Sensormatic Solutions, Checkpoint Systems, Nedap, Gunnebo Gateway, and All-Tag Corporation—collectively account for approximately 63% of the market, leaving the remaining share to smaller specialized and regional players. Strategic initiatives are central to market positioning, with companies investing in AI-enabled RFID systems, cloud-based analytics, and hybrid AM/RF technologies to differentiate offerings. Recent product launches include modular EAS solutions for retail and logistics applications, with deployments exceeding 12 million units globally in 2024. Partnerships and collaborations between hardware providers and AI analytics firms are shaping competitive dynamics, enabling faster adoption of predictive loss prevention systems. Innovation trends such as sensor miniaturization, integration with IoT platforms, and sustainable tag materials are influencing market strategies, while regional expansion into Asia-Pacific and Latin America is intensifying rivalry. High installation density in North America (over 11.5 million units) and growing AI adoption in Europe (58% of major retailers) further underscores the competitive intensity and strategic differentiation across market players.

Gunnebo Gateway

All-Tag Corporation

Tyco Integrated Security

3M Electronic Article Surveillance

Se-Kure Controls

InVue Technology Group

Sony Security Systems

The Electronic Article Surveillance (EAS) market is being transformed by the integration of advanced technologies that enhance detection accuracy, inventory tracking, and operational efficiency. Hybrid AM/RF systems, combining acousto-magnetic and radio frequency technologies, now constitute 61% of installed units globally, offering detection ranges up to 2.5 meters for high-value merchandise. AI-assisted EAS solutions are enabling predictive analytics to anticipate theft patterns, reducing store shrinkage by 28% on average across large retail chains. RFID-enabled tags are increasingly integrated with IoT platforms, allowing real-time monitoring of over 10 million SKUs in North American and European retailers, while cloud-based dashboards consolidate performance metrics, providing actionable insights to operations managers. Emerging trends include sensor miniaturization, enabling discreet installation in high-end fashion and electronics stores, and sustainable materials, with 45% of new deployments using recyclable tags to meet ESG goals. Additionally, automated deactivation and self-checkout integration are expanding, with over 52% of large chains adopting these technologies to improve consumer convenience. Real-time alerts, predictive loss prevention, and cross-platform analytics are positioning EAS systems as a critical component of modern retail security and operational intelligence.

In March 2024, Sensormatic Solutions launched its AI-Enhanced EAS platform for North American retailers, integrating predictive analytics and real-time SKU tracking, which reduced inventory discrepancies by 31% across over 150 stores.

In August 2023, Checkpoint Systems unveiled a new hybrid AM/RF tag series with miniaturized sensors, increasing detection accuracy by 27% while reducing installation footprint in high-traffic retail environments.

In January 2024, Nedap deployed IoT-enabled EAS gates in European fashion chains, enabling centralized monitoring of over 2 million units, improving operational efficiency and reducing manual intervention by 22%.

In November 2023, Gunnebo Gateway introduced cloud-connected RFID-based EAS solutions for logistics and warehouse applications, supporting real-time asset tracking for over 1.8 million SKUs and enhancing security compliance in supply chain operations.

The Electronic Article Surveillance Market Report provides a comprehensive analysis of the global market, encompassing product types, applications, end-users, and regional dynamics. The report covers key technologies such as hybrid AM/RF systems, AI-assisted RFID, IoT-integrated tags, and sustainable/recyclable materials, offering insights into both current implementations and emerging trends. Market segmentation includes loss prevention, inventory monitoring, asset tracking, and integration with self-checkout systems, reflecting measurable adoption across supermarkets, specialty stores, e-commerce fulfillment centers, and logistics hubs. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional deployment volumes, adoption trends, and technology-driven transformations. The report also examines competitive dynamics, profiling over 85 active players, detailing strategic initiatives, product innovations, and technological differentiation in real-world deployments. Additionally, it addresses niche segments, such as modular and AI-enabled EAS systems, cloud-based analytics platforms, and predictive loss prevention solutions, providing numerical insights into unit adoption, installation densities, and SKU coverage. Overall, the report equips decision-makers with actionable intelligence on operational efficiencies, technological advancements, regulatory compliance, and future-ready strategies for optimized retail and supply chain security.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1616 Million |

|

Market Revenue in 2032 |

USD 2079.11 Million |

|

CAGR (2025 - 2032) |

3.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sensormatic Solutions, Checkpoint Systems, Nedap, Gunnebo Gateway, All-Tag Corporation, Tyco Integrated Security, 3M Electronic Article Surveillance, Se-Kure Controls, InVue Technology Group, Sony Security Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |