Reports

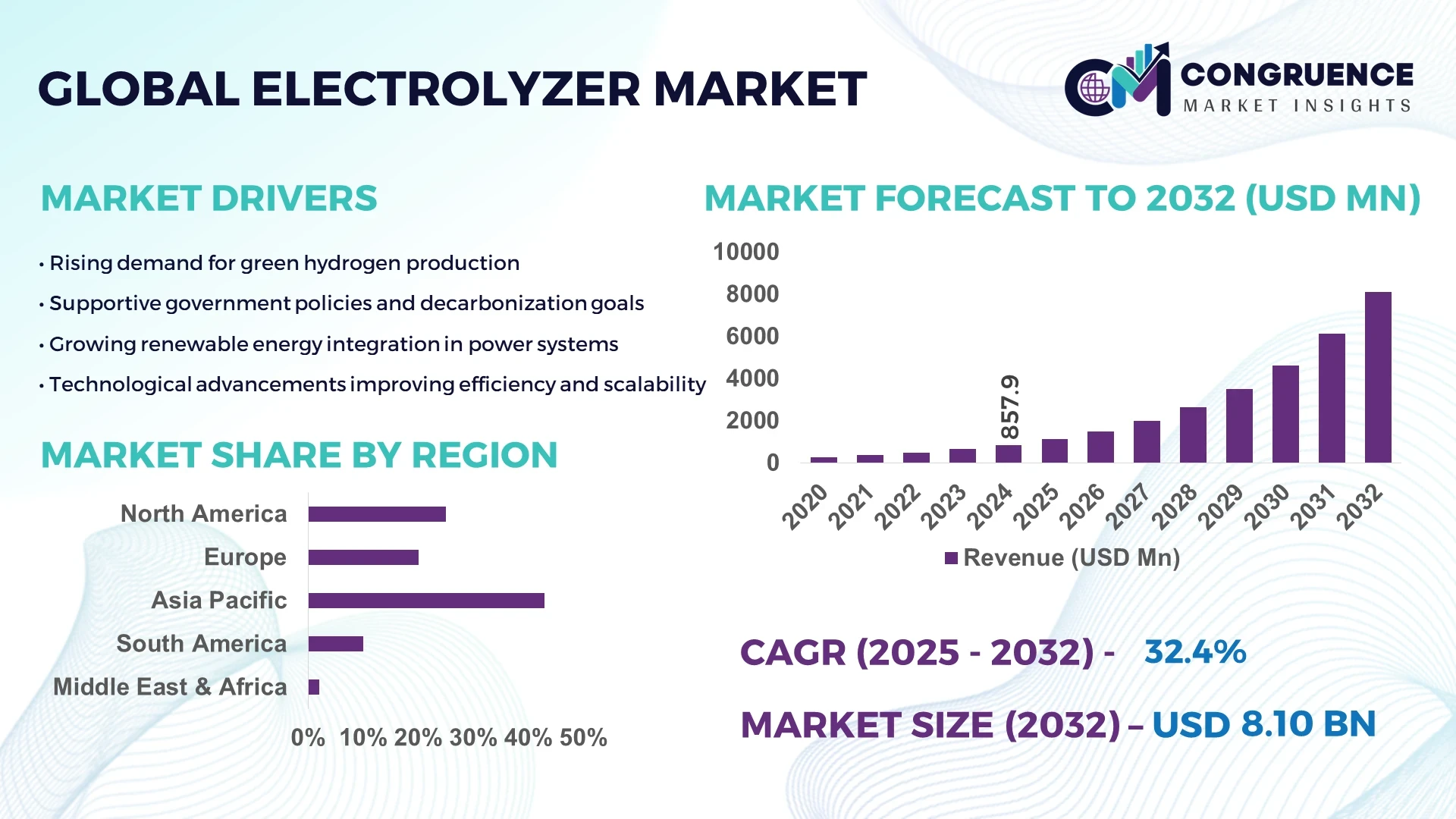

The Global Electrolyzer Market was valued at USD 857.9 Million in 2024 and is anticipated to reach a value of USD 8101.09 Million by 2032 expanding at a CAGR of 32.4% between 2025 and 2032. The market’s growth is primarily driven by the rising demand for green hydrogen across industrial, transportation, and energy storage applications.

China leads the global electrolyzer market, supported by large-scale manufacturing capacity exceeding 2.5 GW annually and government-backed green hydrogen projects under the 14th Five-Year Plan. Major players in China have invested over USD 4 billion since 2023 in scaling alkaline and PEM electrolyzer technologies. The country’s advanced hydrogen infrastructure, strong industrial base, and expanding renewable energy integration across steel, ammonia, and chemical sectors reinforce its position. Additionally, China’s electrolyzer technology efficiency improvements have reached up to 78%, making it a central hub for next-generation hydrogen systems.

Market Size & Growth: Valued at USD 857.9 Million in 2024 and projected to reach USD 8101.09 Million by 2032, expanding at a CAGR of 32.4% due to rapid industrial adoption of green hydrogen and large-scale renewable energy integration.

Top Growth Drivers: 62% rise in green hydrogen adoption, 45% improvement in electrolyzer efficiency, and 38% increase in renewable-powered hydrogen production projects.

Short-Term Forecast: By 2028, electrolyzer production costs are expected to decline by 30%, with system efficiency improving by 25% through enhanced material design.

Emerging Technologies: Solid oxide and anion exchange membrane electrolyzers are gaining traction, alongside AI-based process optimization for hydrogen production.

Regional Leaders: Asia-Pacific expected to reach USD 3.6 Billion by 2032 with strong industrial adoption; Europe projected at USD 2.9 Billion led by policy incentives; North America estimated at USD 1.8 Billion driven by clean energy mandates.

Consumer/End-User Trends: High adoption among chemical producers, refineries, and mobility operators using hydrogen-powered fleets; industrial sectors driving over 60% of demand.

Pilot or Case Example: In 2024, Siemens Energy’s 100 MW hydrogen electrolyzer project in Germany achieved a 20% reduction in production downtime and 18% higher output efficiency.

Competitive Landscape: Nel ASA leads with approximately 17% market share, followed by Plug Power, Thyssenkrupp Nucera, ITM Power, and Cummins.

Regulatory & ESG Impact: EU Hydrogen Strategy, U.S. Inflation Reduction Act, and China’s Hydrogen Development Guidelines promote low-carbon hydrogen initiatives and electrolyzer subsidies.

Investment & Funding Patterns: Over USD 10.2 Billion invested globally in 2023–2024 through public-private partnerships, venture funding, and energy transition financing.

Innovation & Future Outlook: Advancements in modular electrolyzers, digital twin integration, and hybrid renewable-hydrogen systems are expected to redefine efficiency standards and global deployment rates by 2030.

The electrolyzer market is witnessing robust growth across hydrogen-intensive sectors such as power generation, transportation, and chemicals, with industrial users accounting for the largest consumption share. Recent technological innovations in membrane durability, stack design, and AI-driven monitoring have enhanced performance and lowered operational costs. Regulatory frameworks emphasizing decarbonization, combined with regional incentives and green hydrogen targets, are accelerating market penetration. Emerging trends point toward increased localization of electrolyzer production, cross-sectoral integration with renewable grids, and strategic collaborations to establish global green hydrogen corridors by 2032.

The strategic relevance of the Electrolyzer Market lies in its central role in the global transition toward decarbonized industrial systems and clean energy ecosystems. Electrolyzers are pivotal in producing green hydrogen, supporting energy storage, transportation, and heavy industrial applications. Technological advancements, particularly in proton exchange membrane (PEM) and solid oxide electrolyzers, are enabling efficiency gains of up to 25% over conventional alkaline systems. For instance, PEM technology delivers 22% higher efficiency compared to traditional alkaline electrolyzers, enhancing scalability and reducing operational costs.

Regionally, Asia-Pacific dominates in production volume, with over 60% of installed capacity, while Europe leads in adoption, with 48% of enterprises integrating electrolyzer-based hydrogen generation in industrial and grid applications. By 2027, AI-integrated control systems are expected to improve operational efficiency by 30%, optimizing hydrogen output and energy utilization in real time. Firms are committing to ESG-driven decarbonization, with leading players targeting a 40% reduction in hydrogen production emissions by 2030 through renewable-powered electrolysis.

In 2024, Norway’s HydrogenPro achieved a 19% energy consumption reduction using AI-optimized load balancing in its 50 MW electrolyzer installation. Such measurable performance improvements signify the accelerating digital transformation of the market. The Electrolyzer Market thus stands as a foundation for sustainable industrial competitiveness, regulatory compliance, and long-term resilience in global clean energy infrastructure.

The growing global shift toward renewable power sources is directly accelerating Electrolyzer Market expansion. Over 75% of new hydrogen projects launched in 2023 were powered by solar and wind energy, reducing carbon intensity in industrial hydrogen production. With renewable power generation costs declining by nearly 20% annually, electrolyzers are increasingly being installed near solar farms and wind corridors for optimized energy utilization. The synergy between renewable capacity expansion and electrolyzer deployment is fostering continuous production of green hydrogen at lower operational costs. As a result, industries such as steel, ammonia, and mobility are rapidly adopting electrolyzers to meet decarbonization goals and replace fossil-fuel-based hydrogen.

The Electrolyzer Market faces constraints due to high capital expenditure and limited infrastructure readiness for large-scale hydrogen storage and distribution. Critical components such as platinum-group catalysts, nickel alloys, and advanced membranes contribute to significant upfront costs—often accounting for over 45% of total system expenses. Moreover, grid connectivity issues and uneven renewable power availability limit deployment efficiency in developing regions. The lack of standardized hydrogen pipelines and compression facilities adds logistical complexity, delaying commercial scalability. Although technological innovation is mitigating some cost barriers, achieving global affordability still requires supply chain optimization, increased local manufacturing, and policy-driven incentives to enable equitable adoption.

The global rollout of green hydrogen policies is opening substantial opportunities for electrolyzer manufacturers and integrators. Governments in more than 40 countries have introduced national hydrogen strategies, allocating over USD 100 billion toward infrastructure and R&D support. These initiatives are stimulating investment in large-scale electrolyzer facilities and pilot programs. For example, new incentives for renewable-powered hydrogen hubs in Europe and the U.S. are encouraging partnerships between energy developers and industrial players. The opportunity also extends to export markets, where nations such as Australia and Saudi Arabia are developing hydrogen corridors for international trade. This policy-driven acceleration is poised to enhance technological competitiveness and global electrolyzer adoption rates.

Electrolyzer systems face operational challenges stemming from efficiency losses, complex thermal management, and significant water consumption requirements. Producing one kilogram of hydrogen typically consumes about nine liters of water, raising sustainability issues in arid regions. Additionally, system degradation rates averaging 2–3% annually reduce long-term efficiency and increase maintenance costs. The need for ultrapure water supply and stable power inputs further complicates deployment, particularly in emerging markets with limited grid reliability. Although advanced designs like anion exchange membrane electrolyzers are improving durability and efficiency, addressing these technical and environmental concerns remains critical to ensuring the sustainable scalability of the Electrolyzer Market worldwide.

Growth of Modular and Prefabricated Electrolyzer Systems: The adoption of modular and prefabricated electrolyzer systems is transforming deployment efficiency across industrial hydrogen projects. Approximately 55% of new electrolyzer installations in 2024 incorporated modular designs, leading to 28% reductions in on-site assembly time and 20% lower installation costs. Prefabricated skid-mounted units are increasingly used in Europe and North America, optimizing space utilization and enabling rapid scalability for decentralized hydrogen production hubs.

Expansion of Large-Scale Green Hydrogen Projects: The Electrolyzer Market is witnessing rapid growth in large-capacity hydrogen facilities exceeding 100 MW per site, driven by national hydrogen initiatives. As of 2024, more than 35 projects above 200 MW capacity were in various stages of development worldwide. This trend reflects a 60% increase in project volume compared to 2022, propelled by industrial demand for low-carbon feedstocks. These giga-scale electrolyzers are enabling strategic energy storage and grid-balancing capabilities across major renewable corridors.

Integration of AI and Digital Twin Technologies: Advanced digital monitoring is redefining electrolyzer operations. By 2025, over 40% of operational electrolyzers are expected to employ AI-based predictive control systems, improving system uptime by 25% and cutting maintenance costs by 18%. Digital twin models are now simulating full plant behavior, enabling real-time fault detection and performance optimization across multi-stack configurations, particularly in Europe and East Asia.

Emergence of Low-Carbon Material Innovations: The use of low-carbon materials in electrolyzer manufacturing is accelerating sustainability objectives. Around 30% of global producers are shifting to recyclable and low-impact alloys, achieving up to 22% reductions in lifecycle emissions. Innovations such as nickel-iron composite electrodes and advanced polymer membranes are enhancing conductivity while extending unit life expectancy by 15%, reinforcing the sector’s movement toward circular and climate-resilient production systems.

The Electrolyzer Market is segmented by type, application, and end-user, each contributing distinctly to the industry’s overall expansion and technological diversification. Among the various segments, alkaline, PEM, and solid oxide electrolyzers dominate the landscape, with alkaline systems currently holding the largest share due to their proven operational reliability and cost advantages. Applications primarily span industrial hydrogen production, transportation fuel, and power generation, reflecting broad integration across energy-intensive sectors. End-user adoption is concentrated within industrial manufacturers, followed by energy and transportation sectors, which together account for more than 70% of installations worldwide. Increasing demand for decarbonization technologies, ongoing infrastructure investments, and regional policy frameworks are further shaping segment-specific growth trajectories.

Alkaline electrolyzers currently lead the global market, accounting for approximately 48% of total installations, driven by their long operational lifespans and lower capital requirements. These systems dominate industrial hydrogen production facilities due to proven reliability and easy scalability. PEM (Proton Exchange Membrane) electrolyzers, representing around 32% of market share, are the fastest-growing segment with an estimated growth rate exceeding 35% annually, fueled by demand for compact designs, high-purity hydrogen, and renewable energy compatibility. Solid oxide electrolyzers, though comprising about 12% of installations, are gaining traction in stationary energy storage and high-temperature industrial applications due to superior energy conversion efficiency. The remaining 8% includes emerging anion exchange membrane and hybrid systems targeting specialized R&D and pilot projects.

Industrial hydrogen production dominates the Electrolyzer Market, accounting for nearly 52% of total applications due to its integration within ammonia, methanol, and steel manufacturing. These applications rely on electrolyzers to replace fossil-based hydrogen with renewable alternatives, significantly reducing emissions intensity. Power generation and grid balancing constitute about 27% of installations, serving as the fastest-growing segment with a growth rate above 30% per annum, supported by renewable integration and storage demand. Mobility and transportation fuel cells represent another 14%, benefiting from increased investments in hydrogen-powered vehicles and refueling networks. The remaining 7% of applications span research facilities and small-scale distributed energy systems focusing on localized hydrogen ecosystems.

Industrial manufacturing remains the leading end-user of electrolyzers, holding approximately 46% of total adoption, driven by decarbonization goals across steel, chemical, and fertilizer sectors. The energy and power sector follows with around 31%, leveraging electrolyzers for grid stabilization and renewable storage, while the transportation and mobility sector, representing 15%, is the fastest-growing with an estimated 35% annual growth rate, supported by rising hydrogen mobility adoption and infrastructure expansion. The remaining 8% includes research institutions and government-backed innovation centers focusing on advanced electrolyzer designs.

Asia-Pacific accounted for the largest market share at 90.64% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 97% between 2025 and 2032.

In 2024, the Asia-Pacific region’s dominance was reinforced by its large manufacturing base and rapid deployment of electrolyzer systems across industrial and mobility sectors. With over 40.6% of regional capacity located in one country alone in 2024, capacity build-out and infrastructure scale-up are materially ahead of other geographies. The region’s volume of new installations in 2024 exceeded 70 GW of announced capacity, and investment levels rose by more than 60% year-on-year. Despite this dominance, regions such as Europe and North America are registering higher growth in adoption per enterprise – for example, more than 48% of European industrial hydrogen players deployed electrolyzer systems in 2024, while North America recorded over 35% of new project announcements tied to grid-balancing markets. The scale of Asia-Pacific’s production and manufacturing ecosystem, combined with its aggressive hydrogen strategies and export-oriented business models, underpin both high volume and rapid technological advancement across the electrolyzer market landscape.

North America holds approximately 7% of total global electrolyzer market share in 2024. Demand is largely driven by two key industries: industrial manufacturing (including refineries and chemicals) and power & utilities (especially grid-injection and renewable balancing). A significant regulatory change in 2023 saw the introduction of tax-credit incentives for green hydrogen production, boosting electrolyzer projects linking to renewable generation. Technological trends include modular electrolyzer skids and digital twin-enabled operational platforms, with local player EH2 announcing a 1.2 GW annual production capacity plant in Massachusetts scheduled from Q1 2024. In terms of regional consumer-behaviour variations, North American enterprises in manufacturing and energy are favouring large-scale, integrated projects as part of their decarbonisation strategies, contrasting with smaller, distributed systems seen elsewhere. The strong interplay of policy, heavy-industry demand and advanced manufacturing gives North America a unique deployment profile in the global electrolyzer market.

Europe commands roughly 12% of the global electrolyzer market share in 2024. Key markets include Germany, the UK and France, where industry decarbonisation mandates and renewable hydrogen strategies have driven uptake. Regulatory bodies such as the European Commission and national hydrogen roadmaps are incentivising electrolyzer deployment via subsidies, H₂ infrastructure funding and mandates for industrial feedstock substitution. Emerging technologies such as high-pressure PEM stacks and advanced solid-oxide systems are being adopted, often in pilot form across Germany and France. A local player, McPhy Energy (France), is manufacturing modular electrolyzers for mobility and industrial clients, reinforcing regional supply-chain capabilities. In behavioural terms, European industrial buyers are particularly sensitive to regulatory compliance and prefer electrolysis systems that meet explainable operational and sustainability criteria, driving demand for audited lifetime performance and transparency in the electrolyzer market.

Asia-Pacific leads in market volume, representing over 90% of global installations in 2024. Top consuming countries include China, India and Japan, while infrastructure and manufacturing trends show rapid build-out of both electrolyzer production and green hydrogen hubs. Manufacturing hubs are being established with localised supply chains, and innovation clusters are emerging in countries such as Japan and South Korea around compact PEM electrolyzers for mobility use. A local player, ITM Power, has partnered to deploy a 2 MW unit in Japan, illustrating regional adoption of advanced systems. In terms of consumer behaviour, Asia-Pacific industries—especially chemicals and fertilisers—are aggressively shifting to electrolyzer-based hydrogen production. They favour high-volume, scale-up models suited to heavy-industrial contexts, distinct from the smaller modular models seen in other regions.

In South America, key countries such as Brazil and Argentina are beginning to capture electrolyzer market presence, with the region accounting for approximately 3%–4% of global share in 2024. Infrastructure trends focus on coupling electrolyzers with abundant renewable power—particularly solar and wind—for both domestic hydrogen use and export-oriented clean-hydrogen corridors. Government incentives and trade policies are increasingly supporting green-hydrogen production, for example through export tax breaks and renewable energy auctions. A local player pilot in Chile is targeting 5 GW electrolyzer capacity by 2025, signalling scale-intention in the region. Consumer behaviour in South America reflects a premium on renewable-backed electrolyzer installations for regional export markets, rather than purely domestic consumption models typical in other regions.

The Middle East & Africa region represents roughly 6% of the global electrolyzer market share in 2024. Demand trends are being shaped by oil-&-gas companies transitioning to green hydrogen, large-scale solar-to-hydrogen hubs in countries like the UAE and Saudi Arabia, and technology modernisation in South Africa. Technological initiatives include high‐temperature solid-oxide electrolyzers and desert-scale renewables feeding hydrogen production. Trade partnerships are expanding, including export-oriented hydrogen pipelines and ammonia shipping routes. Regional consumer-behaviour variation includes large industrial and energy-sector adoption of electrolyzers as part of national export strategies rather than purely domestic applications common in mature markets. A local player in the UAE has announced a multi-gigawatt electrolyzer tender tied to solar development and hydrogen-ammonia export.

China: ~40.6% share in Asia-Pacific capacity for 2024 — high manufacturing capacity and aggressive hydrogen strategy.

United States: ~7% global share in 2024 — strong regulatory incentives and large industrial hydrogen demand.

The Electrolyzer market in 2024 exhibits a moderately consolidated competitive structure, with the top five companies collectively accounting for around 68% of the total global market share. Approximately 60 active competitors operate globally, ranging from established industrial manufacturers to new technology entrants focusing on green hydrogen integration. The market shows strong competition among players offering PEM, alkaline, and solid oxide electrolyzers, each emphasizing efficiency, cost, and scalability. Key competitive strategies include vertical integration, multi-GW production expansions, and strategic collaborations with renewable energy developers and governments. In 2024, over 15 large-scale partnerships were announced for electrolyzer deployment exceeding 1 GW capacity per project. The industry is increasingly shaped by innovation in catalyst reduction (up to 35% lower platinum-group metal use) and automation, which improves manufacturing productivity by 25–30%. Additionally, digital monitoring platforms are gaining traction, with over 40% of OEMs offering remote stack optimization. Overall, the market remains partly consolidated but continues to attract new entrants leveraging regional incentives and ESG-driven demand.

Plug Power Inc.

Sunfire GmbH

ITM Power

McPhy Energy

Cummins Inc.

Bloom Energy

John Cockerill

The Electrolyzer market is undergoing a significant technological transformation, with rapid advancements in efficiency, scalability, and material optimization shaping its trajectory. Alkaline Electrolyzers currently account for over 45% of global installations, favored for their durability and cost-effectiveness in large-scale hydrogen production. However, PEM (Proton Exchange Membrane) Electrolyzers, representing nearly 38% of deployed systems, are rapidly gaining traction due to their superior dynamic response and compatibility with variable renewable energy sources such as wind and solar.

Emerging technologies such as Anion Exchange Membrane (AEM) and Solid Oxide Electrolyzers (SOE) are reshaping the innovation landscape. AEM systems are showing a 25% reduction in capital cost compared to PEM units by reducing reliance on precious metals like iridium and platinum. Meanwhile, SOE technology delivers energy efficiencies up to 85%, utilizing high-temperature electrolysis suitable for industrial applications requiring process heat. The integration of AI-driven control systems and digital twin modeling has further optimized stack performance and predictive maintenance, improving uptime rates by up to 20%.

Additionally, the market is witnessing growing interest in modular electrolyzer systems, enabling scalable deployment from 1 MW to over 100 MW configurations. Manufacturers are increasingly incorporating automated stack assembly lines, which have improved production speed by 35% while reducing manual labor dependency. These technological evolutions are positioning electrolyzers as a cornerstone for green hydrogen ecosystems, supporting industrial decarbonization and sustainable infrastructure development globally.

Siemens Energy opened a new electrolyzer production facility in Berlin on November 8, 2023, targeting an annual production capacity of at least 3 gigawatts of stack assemblies by 2025. (siemens-energy.com)

Nel ASA entered into a technology-licensing agreement with Reliance Industries on May 21, 2024 which grants exclusive manufacture of Nel’s alkaline electrolyzers for the Indian market and captures potential global manufacturing scope. (Nel Hydrogen)

Thyssenkrupp Nucera’s 20 MW module series “scalum®” received the German Sustainability Award in November 2024, recognizing its modular structure, scalability and applicability to green-hydrogen infrastructure. (thyssenkrupp)

In October 2024 Nel ASA was awarded up to EUR 135 million in grants for industrializing next-generation electrolyzer technology in Norway, advancing low-cost and high-efficiency systems. (fuelcellsworks.com)

The Electrolyzer Market Report covers a comprehensive range of market segments, encompassing technology types, application areas, end-user industries and geographic regions. The technology types include alkaline, proton exchange membrane (PEM), solid oxide, anion exchange membrane (AEM) and hybrid electrolyzer systems, with detailed discussion of performance metrics, stack configuration, manufacturing scale-up and material innovation. Application areas span industrial hydrogen production (for refining, ammonia and steel), grid balancing and power generation, mobility and transport fuel (hydrogen-powered vehicles and refuelling networks), and emerging niche uses such as energy storage and fuel-cell backup systems. End-user industries addressed include heavy manufacturing, chemicals & petrochemicals, utilities and transportation fleets, outlining adoption rates, enterprise deployment behaviour and procurement criteria. Geographically, the report provides region-wise analysis across Asia-Pacific, Europe, North America, South America and Middle East & Africa, including country-level insights for leading markets such as China, India, Germany and the U.S., as well as supply-chain development, infrastructure maturity and local regulatory frameworks. The industry focus areas include manufacturing capacity expansions, modular and prefabricated system design, digitalisation and stack automation, ESG and decarbonisation drivers, and hydrogen value-chain integration. Emerging or niche segments such as distributed modular electrolyzers, hydrogen export hubs and high-temperature electrolysis (solid oxide) are also explored. The report is designed to provide business decision-makers and industry professionals with actionable insights into segment dynamics, competitive landscape, technology advancements and regional investment trends to support strategic planning and market positioning.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 857.9 Million |

Market Revenue in 2032 | USD 8101.09 Million |

CAGR (2025 - 2032) | 32.4% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Siemens Energy, Nel ASA, Thyssenkrupp Nucera, Plug Power Inc., Sunfire GmbH, ITM Power, McPhy Energy, Cummins Inc., Bloom Energy, John Cockerill |

Customization & Pricing | Available on Request (10% Customization is Free) |