Reports

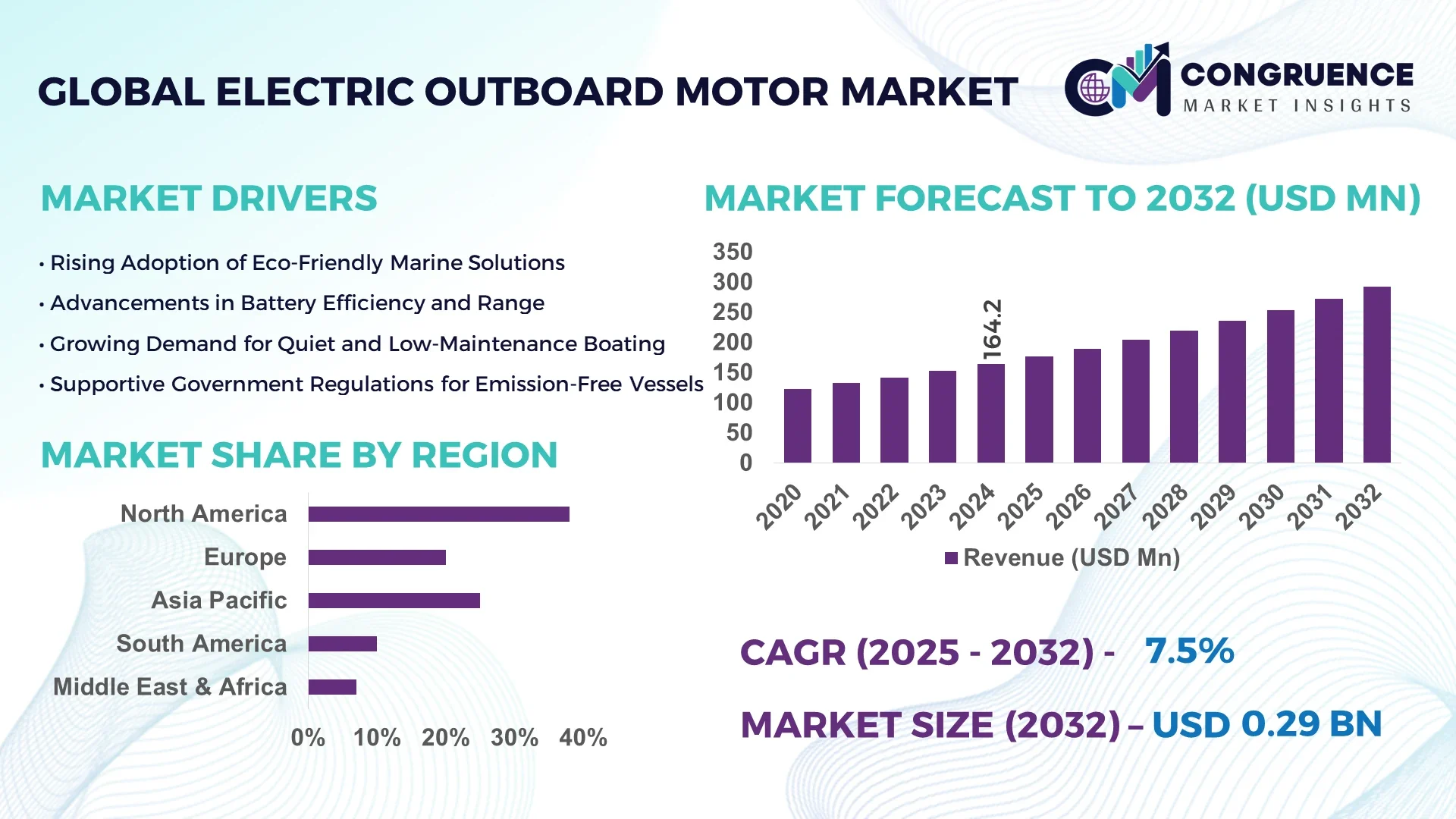

The Global Electric Outboard Motor Market was valued at USD 164.21 Million in 2024 and is anticipated to reach a value of USD 292.87 Million by 2032 expanding at a CAGR of 7.5% between 2025 and 2032. The market growth is driven by the increasing shift toward sustainable marine propulsion technologies and the rising adoption of electric mobility solutions in recreational and commercial boating.

The United States dominates the Electric Outboard Motor market due to its robust marine manufacturing base, high consumer spending on recreational boating, and significant investment in electrification infrastructure. The U.S. accounts for over 35% of global electric outboard motor production, supported by over 120 active manufacturers and R&D centers focusing on battery efficiency and lightweight motor designs. Consumer adoption exceeds 40% in coastal regions, particularly in Florida and California, where advanced lithium-ion propulsion systems are widely deployed across fishing and leisure vessels.

• Market Size & Growth: Valued at USD 164.21 Million in 2024, projected to reach USD 292.87 Million by 2032, expanding at a CAGR of 7.5%, driven by the global transition to low-emission marine transport.

• Top Growth Drivers: Rising recreational boat electrification (28%), improved motor efficiency (22%), and government incentives for clean marine technologies (18%).

• Short-Term Forecast: By 2028, operational cost reduction expected to improve by 25% with advancements in battery density and charging speed.

• Emerging Technologies: Integration of solid-state batteries, digital twin motor diagnostics, and AI-driven propulsion optimization.

• Regional Leaders: North America (USD 118 Million by 2032), Europe (USD 92 Million), and Asia-Pacific (USD 60 Million), each showing distinct adoption patterns driven by sustainability mandates and consumer demand.

• Consumer/End-User Trends: Growing adoption among recreational boaters, fishing communities, and small-scale commercial operators for low-noise and emission-free performance.

• Pilot or Case Example: In 2024, a 40-foot hybrid-electric boat pilot in Norway achieved a 32% efficiency gain and 18% downtime reduction using advanced battery cooling systems.

• Competitive Landscape: Market leader Torqeedo GmbH holds approximately 21% share, followed by Elco Motor Yachts, ePropulsion, Pure Watercraft, and Yamaha Motor Co., Ltd.

• Regulatory & ESG Impact: Stringent emission regulations under IMO and incentives promoting electric propulsion adoption are accelerating eco-friendly marine innovations.

• Investment & Funding Patterns: Over USD 450 Million invested globally in 2023–2024 toward R&D, fleet electrification projects, and battery innovation initiatives.

• Innovation & Future Outlook: Future trends include modular motor systems, smart energy management, and increased integration with solar-assisted charging technologies.

The Electric Outboard Motor Market is witnessing strong momentum across sectors such as leisure boating, fishing, tourism, and coastal transportation. Innovations in lithium-ion and solid-state batteries, coupled with lightweight composite materials, are reshaping product design and efficiency benchmarks. Governments are incentivizing electric propulsion to meet carbon reduction targets, while regulatory frameworks in Europe and North America are accelerating compliance-driven adoption. Rising consumer preference for silent, maintenance-free operations and cost-efficient propulsion systems is fostering demand growth. The market outlook remains positive with increasing global investments, enhanced charging infrastructure, and steady advancements in power density and performance optimization across marine applications.

The strategic relevance of the Electric Outboard Motor Market lies in its alignment with the global shift toward low-emission mobility, technological modernization, and ESG-driven transformation in marine propulsion systems. The industry is transitioning from conventional gasoline outboards to advanced electric alternatives, where lithium-ion propulsion systems deliver 45% improvement in energy efficiency compared to traditional combustion models. Europe dominates in production volume, while North America leads in adoption, with 47% of small and mid-sized boating enterprises already transitioning to electric propulsion systems. By 2027, AI-enabled energy optimization algorithms are expected to enhance motor performance by up to 30% and reduce operational energy consumption by nearly 20%.

Manufacturers are integrating digital twin and predictive analytics technologies to streamline maintenance cycles and enhance battery lifecycle management. In 2024, a Scandinavian marine operator achieved a 26% reduction in operational costs through the adoption of AI-powered battery monitoring platforms. Firms are committing to ESG metrics such as achieving a 35% reduction in lifecycle emissions and 50% battery recycling rate by 2030 under new EU and IMO sustainability frameworks. The Electric Outboard Motor Market is evolving into a core enabler of sustainable marine transport, combining compliance readiness, technological innovation, and resilience to future fuel and regulatory transitions.

The demand for sustainable and zero-emission marine transport is a significant growth driver for the Electric Outboard Motor Market. Governments across the EU, U.S., and Asia-Pacific are implementing strict marine emission norms, accelerating the replacement of internal combustion engines with electric propulsion systems. Around 60% of newly registered leisure boats in Scandinavia now feature hybrid or fully electric motors, reflecting a rapid adoption curve. Technological advances, such as high-density lithium-ion batteries with 35% longer operating time and lightweight composite materials reducing motor weight by 18%, are also promoting faster electrification. This shift supports both commercial and leisure applications, aligning with national carbon neutrality goals.

High initial investment and limited charging infrastructure remain notable restraints in the Electric Outboard Motor Market. The average electric propulsion setup costs 25–40% more than a comparable gasoline-powered system, primarily due to expensive battery packs and advanced motor controllers. The lack of widespread marine charging stations further slows adoption, particularly in developing regions where grid reliability is low. Additionally, extended charging durations—averaging 3–6 hours for large-capacity motors—create operational downtime for commercial users. Despite decreasing battery costs at a rate of 7–10% annually, affordability remains a key barrier for small-scale operators and private boat owners in cost-sensitive markets.

The growing focus on high-performance energy storage and hybrid system integration presents significant opportunities for the Electric Outboard Motor Market. Solid-state battery technologies, expected to enter large-scale production by 2026, promise a 50% improvement in energy density and faster charging times. Hybrid propulsion models that combine solar-assisted power with electric motors are gaining traction, particularly in coastal tourism and inland waterway transport sectors. Furthermore, the expansion of smart grid-based charging docks in North America and Europe offers scalability for commercial fleet electrification. These developments are enabling longer operational range, improved sustainability outcomes, and broader adoption across multi-application marine segments.

Supply chain instability and the shortage of critical components such as lithium, semiconductors, and high-grade aluminum pose significant challenges to the Electric Outboard Motor Market. Global battery material shortages have led to a 15–20% delay in production schedules among leading manufacturers. Moreover, dependency on limited suppliers for motor controllers and power management systems increases production vulnerability. Logistics bottlenecks and fluctuating raw material prices further impact cost structures and delivery timelines. The market also faces challenges in standardizing battery modules and propulsion systems across brands, slowing interoperability and scalability. Addressing these supply constraints is crucial to ensuring sustained market growth and global competitiveness.

• Advancements in Battery Energy Density and Charging Efficiency: The Electric Outboard Motor market is witnessing rapid technological improvement in energy storage systems. Battery energy density has increased by nearly 38% between 2021 and 2024, allowing vessels to operate 40% longer on a single charge. Charging efficiency has also improved by 27%, reducing downtime from 5 hours to approximately 3.6 hours on average. Manufacturers are integrating adaptive charging algorithms that adjust to temperature and voltage levels, enhancing safety and battery lifespan by 22%. These developments are setting new benchmarks for reliability in both leisure and commercial marine segments.

• Expansion of Lightweight and Composite Motor Designs: The industry is experiencing a design transformation with lightweight and corrosion-resistant composite materials reducing motor mass by up to 30%. This reduction contributes to 18% better fuel-to-thrust conversion efficiency and lower structural vibration. Approximately 62% of newly released electric outboard models in 2024 featured hybrid composite casings and magnetic cooling technology, improving motor longevity by 25%. This trend supports the growing demand for efficient, silent, and high-performance propulsion systems for small and mid-sized vessels.

• Integration of IoT and Smart Connectivity Features: Over 45% of electric outboard motors launched in 2024 were equipped with IoT-based telemetry and cloud analytics systems, enabling real-time performance tracking and predictive maintenance. Smart connectivity solutions have reduced unplanned maintenance incidents by 28%, ensuring optimized power usage and longer operational cycles. The introduction of AI-based fleet management platforms has allowed commercial operators to monitor up to 100 units simultaneously, improving energy allocation and reducing maintenance costs by 15%.

• Growth of Hybrid and Solar-Assisted Propulsion Systems: Hybrid and solar-assisted propulsion technologies are emerging as key trends, with adoption growing by 31% annually between 2022 and 2024. These systems extend cruising range by 45% and cut CO₂ emissions by 50% compared to fully fuel-powered systems. Around 40 marinas in Europe and Asia have adopted hybrid charging docks, integrating solar arrays that provide up to 25% of total charging energy. This combination of sustainability and efficiency is making hybrid propulsion a preferred solution for tourism, ferry, and coastal transportation operators.

The Electric Outboard Motor Market is segmented by type, application, and end-user, reflecting the industry’s evolving product and usage landscape. By type, motors are differentiated by power range and design configuration, with low- and mid-power segments capturing significant consumer adoption. Applications vary across recreational boating, fishing, commercial transport, and government operations, each driven by unique operational requirements. End-user analysis reveals strong penetration among leisure boat owners, followed by growing adoption across tourism operators and marine service providers. With over 58% of current installations in recreational and fishing sectors, the market demonstrates a clear shift toward sustainable and efficient propulsion alternatives, supported by technological advancements in battery systems and connectivity.

Electric outboard motors are broadly categorized into low-power (below 20 kW), mid-power (20–50 kW), and high-power (above 50 kW) systems. Mid-power motors currently account for 46% of total adoption, driven by their balance of efficiency and performance across small commercial and recreational vessels. Low-power models hold approximately 34%, favored for compact boats and fishing applications due to their affordability and lightweight structure. However, the high-power segment, representing 20% today, is the fastest-growing, with an expected CAGR of 9.3% from 2025–2032, as battery innovation enables extended range and higher thrust capacity. Collectively, other niche models like dual-propeller and hybrid-drive systems contribute to 8% of the remaining share, supporting specific industrial and defense applications.

Recreational boating remains the dominant application segment in the Electric Outboard Motor Market, accounting for 48% of global installations due to rising consumer spending on eco-friendly leisure vessels. Fishing applications follow at 27%, supported by low-noise and high-efficiency requirements. The commercial transport segment holds around 18% share but is expanding rapidly, projected to register a CAGR of 8.7% through 2032, as coastal transport operators integrate clean propulsion systems for tourism and short-haul operations. Government and defense applications collectively represent 7%, focusing on low-maintenance and stealth propulsion systems.

Leisure and personal boating users currently dominate the Electric Outboard Motor Market with 52% share, driven by increased consumer preference for quiet, emission-free propulsion and enhanced efficiency. The tourism and hospitality sector follows with 24%, where hotels and marine tour operators are electrifying fleets to meet sustainability goals. The commercial and industrial end-user group holds about 16% share but is the fastest-growing segment, expected to register a CAGR of 9.1% from 2025–2032, fueled by electrification of small-scale transport and rental fleets. Other end-users, including research institutes and government bodies, account for the remaining 8%, focusing on environmental monitoring and defense applications.

North America accounted for the largest market share at 38% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2025 and 2032.

Europe followed closely with a 32% share, reflecting its strong environmental regulations and early electrification of marine fleets. The Middle East & Africa collectively contributed 7%, while South America represented 6% of the total volume. North America led the market with over 140,000 electric outboard units deployed, driven by recreational boating and coastal tourism. Asia-Pacific’s growth is supported by large-scale manufacturing in China, rising eco-tourism in Thailand, and strong government funding in Japan and South Korea. Europe continues to lead in innovation, with 65% of its new boat registrations in 2024 being electric or hybrid, while North America recorded the highest private adoption rate of 48% among coastal users, signaling a strong consumer shift toward low-emission propulsion.

North America held approximately 38% of the global Electric Outboard Motor market in 2024, supported by strong consumer demand in the U.S. and Canada. Key industries driving adoption include recreational boating, coastal transport, and fishing, particularly in states such as Florida and California. Government initiatives such as federal tax rebates on electric marine equipment and coastal electrification programs have accelerated fleet transitions. Technological advancements include AI-based power management and fast-charging systems reducing charging times by 35%. Leading players such as Pure Watercraft and Flux Marine are expanding local assembly plants to boost domestic production. Consumer behavior in North America shows higher adoption among private boat owners, with nearly 45% of new registrations opting for electric propulsion, reflecting both environmental awareness and cost-efficiency trends.

Europe accounted for 32% of the global Electric Outboard Motor market in 2024, led by countries such as Germany, Norway, and the United Kingdom. The European Commission’s maritime decarbonization policies have spurred significant investment in zero-emission marine systems. Over 65% of newly registered recreational boats in Nordic countries are now fully electric. The region is a pioneer in integrating renewable energy with marine propulsion, with advanced charging ports and grid-powered docks along the Mediterranean and Baltic coasts. Players such as Torqeedo GmbH continue to innovate in lightweight motor design and battery efficiency. Consumer behavior in this region is driven by strong regulatory pressure and eco-conscious purchasing, leading to steady growth in both recreational and commercial electric vessels.

Asia-Pacific ranked second in market volume in 2024, accounting for 24% of global Electric Outboard Motor installations. Countries such as China, Japan, and South Korea are leading this momentum, supported by government incentives for clean marine energy and battery innovation. China dominates manufacturing, producing over 50,000 units annually, while Japan’s R&D efforts are focused on energy-dense solid-state batteries improving operational range by 40%. Technological hubs in Shenzhen and Osaka are accelerating localized component production and software integration. Consumer behavior is shifting rapidly, with a 30% year-on-year increase in electric-powered leisure boats, particularly across coastal tourism and small-scale transport sectors.

South America represented 6% of the Electric Outboard Motor market in 2024, with Brazil and Argentina being the primary contributors. Regional growth is supported by expanding renewable energy grids and government-backed green mobility programs along major waterways. Brazil’s ports in São Paulo and Rio de Janeiro are increasingly integrating electric boat fleets for tourism and transport. Local players have begun small-scale assembly, enhancing accessibility and reducing import dependence. Consumer adoption is concentrated in commercial and tourism fleets, with around 20% of marina operators transitioning to electric outboards. Renewable energy availability, combined with lower operational costs, continues to drive the region’s modernization trend.

The Middle East & Africa held a 7% share of the global Electric Outboard Motor market in 2024, driven by emerging sustainability mandates in the UAE, Saudi Arabia, and South Africa. Demand is primarily coming from eco-tourism, port management, and government environmental projects. UAE’s “Green Marine Vision 2030” initiative promotes electric and hybrid propulsion across coastal operations. Technological modernization, including solar-integrated charging docks, has improved operational efficiency by 25% in select marinas. Local manufacturers and distributors are partnering with European technology providers to introduce low-maintenance propulsion systems. Consumer behavior is largely institutional, with growing adoption among government and commercial operators focusing on emission reduction and operational reliability.

• United States – 28% Market Share: Dominance driven by strong recreational boating demand, rapid electrification incentives, and a large domestic manufacturing ecosystem.

• Germany – 18% Market Share: Leadership supported by advanced marine engineering, strict emission compliance policies, and technological innovation in lightweight electric propulsion systems.

The Electric Outboard Motor market is highly fragmented, with more than 65 active competitors globally vying across power ranges, geographic segments, and functional niches. The combined share of the top 5 companies is approximately 38%, indicating a moderate level of concentration but with ample room for smaller players and local specialists. Leading players maintain their positions through strategic product differentiation, alliances, and innovation. Many firms engage in partnerships with battery makers, navigation software providers, or marina infrastructure developers to deliver integrated propulsion ecosystems. Several companies have launched new lines in the past two years—such as higher-power modular units or smart diagnostic systems—to strengthen competitive moats.

Competition is intensifying around digital features, battery modularity, and service offerings. Some firms are adopting subscription models or battery-as-a-service (BaaS) to reduce initial purchase barriers and improve customer retention. Mergers and acquisitions are gradually reshaping the landscape: larger players absorb regional players to gain supply chain control or local market access. In many regional markets, local or niche manufacturers undercut incumbents on price or customization, especially in Asia and South America. Innovation trends such as AI-driven propulsion optimization, predictive maintenance, and integration with solar charging modules are key battlegrounds. Firms with strong R&D budgets are pushing shorter upgrade cycles, which places pressure on leaner companies. In this competitive environment, success depends on having a differentiated value proposition, scalable production, strong go-to-market partnerships, and the agility to respond to rapid shifts in battery and software technologies.

Evoy

Yamaha Motor Co.

Brunswick Corporation

Minn Kota

AquaWatt

Krautler Elektromaschinen

CSM Tech

Elco Motor Yachts

The Electric Outboard Motor market is being transformed by advanced propulsion technologies, battery innovations, and digital integration systems aimed at improving efficiency, range, and sustainability. The adoption of lithium-ion and solid-state batteries has enhanced power density by over 35% compared to traditional lead-acid batteries, allowing longer operational hours and faster charging cycles. Brushless DC (BLDC) motor technology delivers nearly 90–95% energy conversion efficiency, reducing mechanical losses and ensuring smoother torque output. Additionally, permanent magnet synchronous motors (PMSM) are gaining traction due to their compact design and low noise emissions, making them ideal for both recreational and commercial vessels.

The integration of Internet of Things (IoT) and onboard diagnostic systems enables real-time monitoring of battery health, performance analytics, and predictive maintenance. By 2027, AI-powered navigation systems are projected to improve route optimization and energy management efficiency by over 40%. Moreover, advancements in lightweight composite materials and 3D printing technologies have cut overall motor weight by 20%, contributing to higher energy efficiency.

Wireless charging and modular battery-swapping infrastructure are emerging as next-generation solutions to reduce downtime and enhance user convenience. Furthermore, manufacturers are aligning with environmental compliance standards, integrating recyclable materials and energy recovery systems. Collectively, these innovations position electric outboard motors as a critical enabler of sustainable marine mobility and digital transformation in the maritime industry.

• In October 2023, ePropulsion launched its X-40 40 kW / 60 HP electric outboard, delivering equivalent performance to a fossil fuel engine while reducing weight by 20% and achieving a powertrain efficiency rating of 88.2%.

• In January 2024, ePropulsion unveiled the eLite direct-drive outboard at boot Düsseldorf, featuring advanced propeller design and near-silent operation aimed at minimizing maintenance and enhancing efficiency for small tender vessels.

• In May 2024, the ePropulsion eLite 500 W model was recognized among the top marine innovations of the year, offering a top speed of 4 knots for 40 minutes and a range of 9 miles at cruising speed in a compact and lightweight form.

• In September 2024, Mercury Marine introduced two new Avator electric outboard models, Avator 75e and 110e, expanding its electric propulsion lineup for larger vessels with improved range, torque output, and battery modularity.

The Electric Outboard Motor Market Report provides a comprehensive evaluation of technologies, applications, end-users, and geographical markets shaping the industry landscape. It analyzes product types including low-power, mid-power, and high-power motors, alongside hybrid configurations and modular systems optimized for various marine environments. Application coverage spans recreational boating, fishing, commercial transport, government fleets, and tourism operations. End-user insights include private boat owners, commercial fleet managers, marine service providers, and coastal authorities adopting clean propulsion solutions.

Regional segmentation encompasses North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with detailed insights into key markets such as the U.S., Germany, China, Japan, Brazil, and the UAE. The report also explores innovations in lithium-ion, solid-state, and swappable battery systems, integration of IoT-enabled monitoring, and digital twin technologies for predictive maintenance. It further evaluates advancements in solar-assisted docks, wireless charging systems, and portable energy solutions that enhance operational efficiency. Additionally, the scope covers strategic developments in R&D, product diversification, and marine sustainability programs, offering actionable intelligence for investors, manufacturers, and policymakers driving the shift toward electrified marine mobility.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 164.21 Million |

|

Market Revenue in 2032 |

USD 292.87 Million |

|

CAGR (2025 - 2032) |

7.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Torqeedo GmbH, ePropulsion Technology, Pure Watercraft, Evoy, Yamaha Motor Co., Brunswick Corporation, Minn Kota, AquaWatt, Krautler Elektromaschinen, CSM Tech, Elco Motor Yachts |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |