Reports

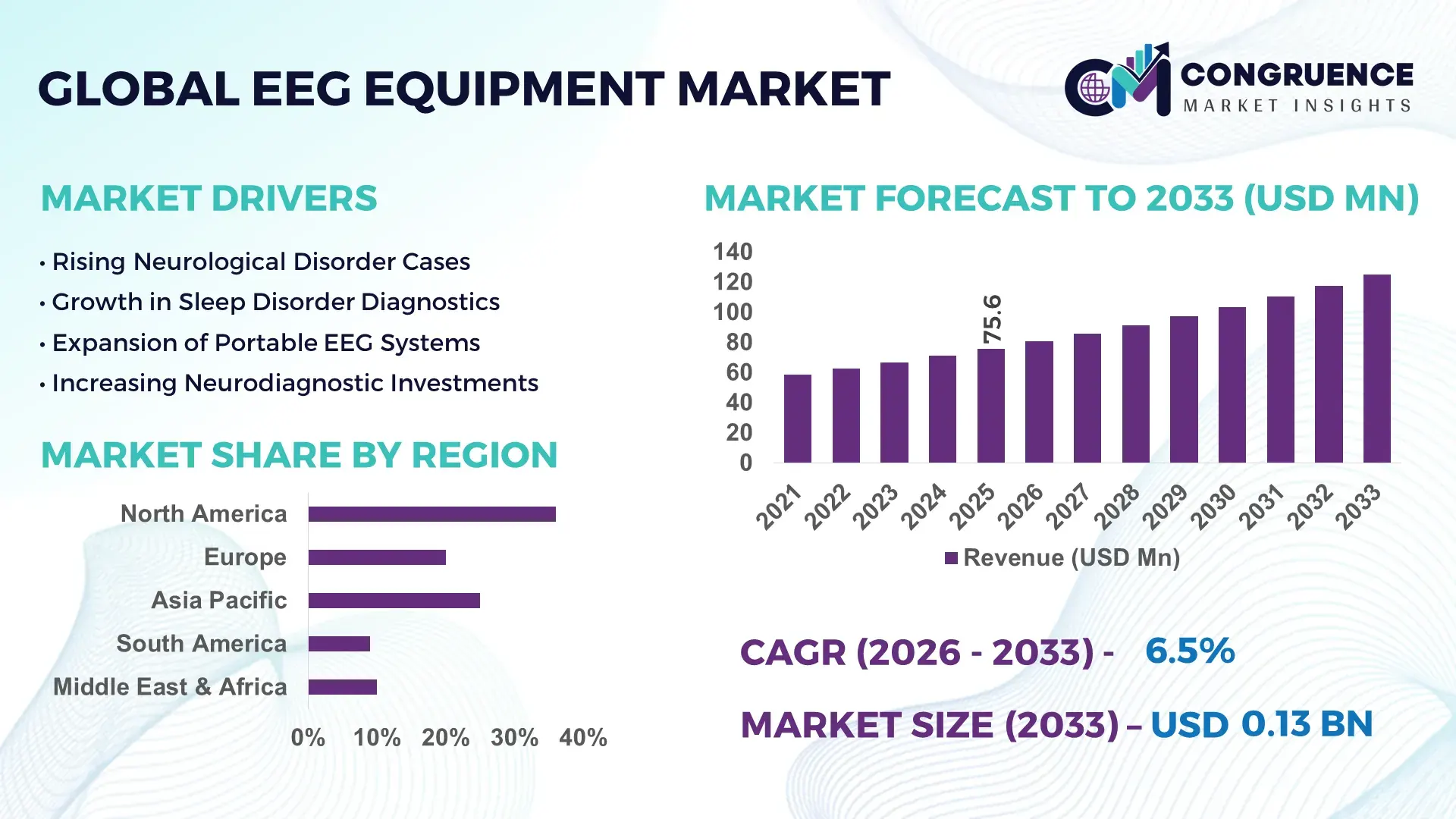

The Global EEG Equipment Market was valued at USD 75.61 Million in 2025 and is anticipated to reach a value of USD 125.14 Million by 2033 expanding at a CAGR of 6.5% between 2026 and 2033. Growth is being accelerated by rising neurological disorder screening volumes, AI-assisted brainwave diagnostics, and expanded neurocritical care infrastructure across tertiary hospitals and ambulatory monitoring centers.

The United States continues to dominate the global EEG equipment market with approximately 34% share, supported by advanced neurodiagnostic infrastructure, over USD 1.8 billion in annual neurological device procurement activity, and rapid integration of wireless EEG monitoring systems across hospital networks. More than 62% of major neurology centers in the country adopted AI-enabled EEG interpretation workflows by early 2026, improving diagnostic turnaround time by nearly 28% compared to conventional systems. Strong demand from epilepsy monitoring, sleep disorder diagnostics, and ICU-based continuous brain monitoring strengthened domestic manufacturing and procurement activity, while geopolitical pressure on semiconductor supply chains pushed manufacturers toward localized component sourcing and multi-region production strategies.

Manufacturers prioritizing portable, cloud-connected, and AI-integrated EEG platforms are positioned to secure stronger hospital contracts and long-term neurodiagnostic expansion opportunities through 2033.

Market Size & Growth: USD 75.61 Million in 2025 rising to USD 125.14 Million by 2033, driven by AI-enabled neurodiagnostic systems and higher neurological screening demand across hospitals.

Top Growth Drivers: Neurological disorder diagnostics increased 31%, portable EEG adoption rose 27%, and ICU brain-monitoring installations expanded 24% globally.

Short-Term Forecast: By 2028, wireless EEG systems are projected to reduce diagnostic setup time by 22% while improving monitoring efficiency by 19%.

Emerging Technologies: AI-based waveform analytics, cloud-connected EEG platforms, and dry-electrode systems improved workflow productivity by over 26% in advanced clinical settings.

Regional Leaders: North America surpassed USD 38 Million with AI integration growth, Europe crossed USD 29 Million through hospital modernization, and Asia-Pacific exceeded USD 33 Million due to rapid neurology infrastructure expansion.

Consumer/End-User Trends: More than 58% of tertiary hospitals adopted portable EEG monitoring solutions for faster emergency neurodiagnostic response and remote patient assessment.

Pilot/Case Example: In 2025, a multi-hospital neurodiagnostic deployment in Germany improved seizure detection accuracy by 21% using AI-assisted EEG interpretation systems.

Competitive Landscape: Leading manufacturers collectively controlled nearly 46% market share, with competition focused on wireless mobility, cloud analytics, and compact neurodiagnostic platforms.

Regulatory & ESG Impact: New medical device compliance standards improved EEG data security adoption by 32% while energy-efficient systems reduced operating consumption by 18%.

Investment & Funding: Global neurological device investments exceeded USD 900 Million in 2025, supported by hospital partnerships, regional manufacturing expansion, and digital health integration.

Innovation & Future Outlook: Next-generation wearable EEG systems and real-time predictive analytics are accelerating decentralized neuro-monitoring and strengthening high-growth outpatient diagnostic ecosystems.

Neurology and critical care applications account for nearly 48% of total EEG equipment demand, followed by sleep disorder diagnostics and cognitive research laboratories. Recent innovation has centered on lightweight wearable systems, dry-sensor technologies, and AI-supported waveform interpretation platforms that improve diagnostic speed and reduce technician workload. Asia-Pacific is witnessing strong procurement growth due to hospital digitization initiatives, while Europe is emphasizing regulatory-compliant neurodiagnostic modernization amid evolving medical data standards. Manufacturers are increasingly diversifying component sourcing to reduce semiconductor dependency and improve delivery resilience. Continuous advancement in portable neuro-monitoring systems is expected to reshape long-term competitive positioning across the global EEG equipment industry.

The EEG equipment market is becoming strategically critical as healthcare systems prioritize real-time neurological diagnostics, decentralized patient monitoring, and AI-supported clinical decision-making. Hospitals and neurodiagnostic networks are expanding continuous brain-monitoring capabilities to manage rising epilepsy, stroke, and sleep-disorder cases with faster intervention accuracy. Supply-chain restructuring following semiconductor shortages has accelerated localized component sourcing in the United States and Japan, while stricter digital health compliance standards are pushing manufacturers toward cloud-secure EEG ecosystems. More than 54% of newly procured EEG systems in advanced healthcare facilities now include wireless or remote-monitoring functionality, reshaping competitive differentiation across neurodiagnostic platforms.

AI-assisted EEG interpretation platforms are reducing waveform analysis time by nearly 30% compared to legacy manually reviewed systems, while dry-electrode technologies lower patient preparation time by approximately 25%. Germany and the United States are prioritizing high-end ICU-integrated EEG deployments, whereas India and China are focusing on portable and cost-efficient neurodiagnostic expansion across secondary hospitals. In 2025, several tertiary hospital groups integrated compact wireless EEG carts into emergency care units, improving neurological triage efficiency and reducing technician dependency during peak patient volumes.

Over the next 2–3 years, manufacturers are expected to accelerate partnerships with digital health providers, expand portable EEG production capacity, and strengthen AI-enabled analytics portfolios. Companies securing scalable software integration, cybersecurity compliance, and faster deployment models will gain stronger competitive positioning in modern neurodiagnostic infrastructure development.

Rapid deployment of AI-enabled neurodiagnostic systems across hospitals and critical care facilities is accelerating EEG equipment adoption. More than 61% of tertiary neurology centers in the United States implemented continuous EEG monitoring workflows by early 2026, while portable EEG utilization increased nearly 29% across emergency care settings. Rising neurological disorder incidence and higher ICU monitoring requirements are pushing healthcare providers toward faster diagnostic automation and remote interpretation capabilities. China expanded domestic neurodiagnostic manufacturing capacity to reduce import dependency following medical electronics supply disruptions, strengthening localized procurement strategies. Manufacturers are responding through AI software integration, cloud-based monitoring partnerships, and compact wireless system launches. A key operational shift is the movement from centralized neurology labs toward bedside and ambulatory EEG deployment models, improving patient throughput and equipment utilization efficiency.

EEG equipment deployment remains constrained by interoperability gaps between hospital information systems, legacy diagnostic infrastructure, and cloud-enabled neurodiagnostic platforms. Nearly 38% of mid-sized healthcare facilities continue operating outdated EEG architectures that lack compatibility with AI-assisted analytics tools, increasing integration expenses and workflow inefficiencies. Semiconductor component price fluctuations and sensor procurement delays raised production costs by approximately 17% during recent medical electronics supply-chain disruptions, particularly affecting manufacturers dependent on single-country sourcing models. Smaller hospitals in Brazil and Southeast Asia face limited reimbursement coverage for advanced neuro-monitoring systems, slowing procurement cycles and deployment scalability. Companies are mitigating these pressures through localized assembly operations, multi-vendor software compatibility strategies, and long-term supplier agreements. Operationally, manufacturers prioritizing modular system architectures are reducing upgrade complexity and improving lifecycle profitability.

Portable EEG systems and remote neurological monitoring platforms are creating significant expansion opportunities across outpatient diagnostics, emergency response, and home-based care environments. More than 46% of new neurodiagnostic procurement projects in India and South Korea now prioritize lightweight wireless EEG configurations to improve mobility and reduce infrastructure dependency. AI-supported predictive analytics platforms are improving seizure detection efficiency by nearly 24%, while dry-electrode technologies lower consumable usage and shorten patient setup procedures. Government-backed hospital digitization programs and tele-neurology expansion initiatives are accelerating decentralized diagnostics adoption. Manufacturers are increasing investments in wearable EEG R&D, cloud-connected ecosystems, and software subscription models to build recurring service revenue streams. A non-obvious strategic opportunity lies in integrating EEG platforms with broader digital rehabilitation and cognitive assessment ecosystems, expanding long-term clinical utility beyond traditional neurology departments.

As EEG systems become increasingly cloud-connected and AI-enabled, cybersecurity exposure and workforce shortages are emerging as major long-term operational challenges. Approximately 42% of healthcare organizations reported difficulties managing secure neurological data integration across multi-site monitoring networks, while technician shortages continue affecting deployment consistency in high-volume hospitals. Continuous EEG monitoring generates large-scale patient data streams, increasing infrastructure pressure on hospitals with limited digital storage and cybersecurity investment capacity. In the United Kingdom and Canada, stricter medical data governance requirements are extending software validation and deployment timelines for advanced neurodiagnostic platforms. Companies must strengthen encrypted data architectures, clinician training programs, and interoperable software frameworks to maintain scalability and compliance. Strategically, vendors capable of combining secure analytics infrastructure with simplified clinical workflows will secure stronger long-term positioning in digitally connected neurodiagnostic environments.

Wireless EEG Systems currently lead the EEG equipment market due to strong deployment flexibility, reduced cabling complexity, and compatibility with modern hospital monitoring infrastructure. Nearly 36% of newly installed neurodiagnostic systems in advanced healthcare facilities now utilize wireless configurations, particularly across ICU monitoring and ambulatory neurology applications. Portable EEG Systems are witnessing the fastest adoption growth as hospitals and outpatient providers prioritize mobility, emergency response efficiency, and decentralized neurological testing. Their deployment volume increased by approximately 28% during 2025, supported by expanding home-monitoring and remote-care initiatives. Video EEG Systems maintain strong relevance in epilepsy diagnostics where continuous behavioral correlation remains operationally critical, while Routine EEG Systems continue serving cost-sensitive diagnostic environments and secondary hospitals. Ambulatory EEG Systems are gaining traction for long-duration monitoring and outpatient workflow optimization. Manufacturers are increasingly investing in lightweight wearable architectures, AI-integrated reporting tools, and cloud-enabled platforms to strengthen product differentiation and improve clinician productivity across scalable neurodiagnostic environments.

Epilepsy Diagnosis remains the leading application segment due to high monitoring frequency, long-duration testing requirements, and expanding seizure-detection protocols across tertiary hospitals. Nearly 44% of EEG procedures globally are linked to epilepsy-related diagnostics, particularly within specialized neurology centers in the United States and Germany. ICU Monitoring is emerging as the fastest-growing application as critical care units expand continuous neurological surveillance for stroke, trauma, and post-surgical patients. Continuous EEG utilization in intensive care environments increased by approximately 26% during 2025 following broader adoption of AI-assisted monitoring workflows. Sleep Disorder Monitoring continues expanding through integrated sleep-lab modernization, while Brain Mapping and Cognitive Assessment applications are gaining relevance within neurorehabilitation and behavioral analytics programs. Neurological Research remains strategically important for academic institutions and pharmaceutical studies. Companies are responding through cloud-based analytics integration, multi-channel monitoring platforms, and specialized software ecosystems designed for high-volume neurodiagnostic environments.

Hospitals represent the dominant end-user segment due to extensive neurodiagnostic infrastructure, high patient throughput, and continuous monitoring requirements across emergency, ICU, and neurology departments. More than 52% of enterprise EEG procurement activity during 2025 originated from multi-specialty hospital networks integrating centralized neurological monitoring systems. Diagnostic Centers are emerging as the fastest-growing end-user category as outpatient neuro-testing demand increases and healthcare providers prioritize lower-cost decentralized diagnostics. Independent neurodiagnostic facilities expanded portable EEG deployment by approximately 24% to improve operational flexibility and testing capacity. Neurology Clinics continue investing in compact wireless systems for routine seizure and cognitive evaluations, while Research Institutes and Academic Medical Centers remain critical for advanced neurological studies and AI-driven waveform analysis development. Ambulatory Surgical Centers are gradually adopting EEG monitoring for perioperative neurological assessment. Manufacturers are targeting these segments through modular pricing strategies, cloud-connected software subscriptions, and customized deployment partnerships focused on workflow efficiency and scalable diagnostics integration.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

AI-Integrated Neurodiagnostic Expansion

North America maintains leadership in the EEG equipment market through advanced neurological care infrastructure, strong hospital digitization, and rapid deployment of AI-assisted neurodiagnostic systems. More than 63% of tertiary hospitals in the United States and Canada integrated continuous EEG monitoring platforms into ICU workflows by 2025, improving neurological response efficiency and patient monitoring accuracy. Enterprise demand is rising for cloud-connected EEG systems capable of supporting remote interpretation and centralized monitoring. Medical technology companies are expanding software partnerships, strengthening cybersecurity capabilities, and increasing domestic assembly operations to reduce supply-chain dependency. The region also benefits from high clinical trial activity and large-scale neurology research programs supporting advanced EEG adoption across emergency care, epilepsy diagnostics, and cognitive assessment applications.

The United States dominates the regional EEG equipment market due to extensive neurocritical care infrastructure and rapid AI-enabled monitoring adoption. Nearly 58% of advanced hospital networks deployed wireless EEG systems for ICU and emergency neurological monitoring, strengthening demand for scalable and interoperable neurodiagnostic platforms.

Regulatory-Led Digital Modernization

Europe represents a technologically advanced EEG equipment market supported by healthcare modernization programs, stricter medical device compliance frameworks, and rising demand for integrated neuro-monitoring systems. Germany, France, and the United Kingdom are accelerating adoption of cloud-secure EEG platforms to improve diagnostic standardization and operational efficiency. More than 46% of newly procured EEG systems across Western Europe include AI-supported analytics and remote-access capabilities. Regulatory pressure surrounding patient data governance is driving enterprise investment toward interoperable and cybersecurity-compliant neurodiagnostic ecosystems. Manufacturers are strengthening localized distribution partnerships and expanding energy-efficient production operations to align with sustainability-focused healthcare procurement standards. Continuous neurological monitoring demand is also increasing across stroke management and post-operative critical care environments.

Germany leads the European EEG equipment market through strong hospital infrastructure, precision medical engineering capabilities, and advanced neurology research activity. Approximately 41% of major neurological centers in the country adopted AI-assisted EEG interpretation workflows to improve diagnostic consistency and reduce specialist review time.

Large-Scale Portable EEG Deployment

Asia-Pacific is witnessing rapid EEG equipment expansion driven by hospital digitization, growing neurological disorder diagnosis rates, and increasing investment in decentralized healthcare infrastructure. China, India, Japan, and South Korea are scaling portable and wireless EEG deployment to strengthen neurological diagnostics beyond metropolitan healthcare centers. Nearly 34% of regional procurement projects during 2025 focused on compact EEG systems optimized for ambulatory and emergency-care use. Manufacturers are prioritizing Asia-Pacific for production scale, cost-efficient electronics sourcing, and high-volume enterprise contracts. Governments are also supporting domestic medical electronics manufacturing to reduce dependency on imported neurodiagnostic components. Strong outpatient diagnostic growth and tele-neurology adoption are accelerating demand for lightweight, cloud-enabled EEG architectures across public and private healthcare networks.

China leads the Asia-Pacific EEG equipment market through large-scale medical electronics manufacturing capacity and rapid healthcare infrastructure expansion. More than 49% of newly established tertiary neurological centers integrated wireless EEG monitoring systems during recent hospital modernization initiatives, strengthening domestic deployment scale and procurement activity.

Outpatient Neurodiagnostic Expansion

South America is experiencing gradual EEG equipment market development supported by expanding neurological diagnostics access, rising outpatient testing demand, and improving hospital infrastructure investment. Brazil and Argentina are increasing procurement of portable EEG systems to improve neuro-monitoring accessibility in secondary healthcare facilities and urban diagnostic centers. Approximately 27% of recent enterprise procurement activity in the region focused on ambulatory EEG solutions optimized for cost-efficient deployment. Private healthcare providers are expanding neurodiagnostic partnerships to address rising epilepsy and sleep disorder monitoring demand. However, import dependency, reimbursement limitations, and inconsistent healthcare funding continue affecting deployment speed and equipment replacement cycles. Companies are responding through localized distribution agreements, modular pricing models, and lower-maintenance EEG system offerings tailored to regional operational constraints.

Brazil dominates the South American EEG equipment market due to its large private healthcare network and expanding neurology diagnostics capacity. Nearly 31% of major urban diagnostic centers upgraded portable EEG infrastructure during 2025 to improve outpatient neurological testing efficiency and patient throughput.

Healthcare Infrastructure Transformation Investments

The Middle East & Africa EEG equipment market is expanding through healthcare infrastructure modernization, specialty neurology center development, and increasing investment in digital diagnostic technologies. Gulf countries are accelerating deployment of advanced neuro-monitoring systems within tertiary hospitals and critical care facilities to strengthen neurological emergency response capabilities. More than 22% of newly commissioned ICU infrastructure projects in the Gulf region incorporated continuous EEG monitoring functionality during 2025. Enterprise healthcare groups are prioritizing partnerships with international neurodiagnostic suppliers to improve clinical workflow automation and specialist access. In Africa, portable EEG systems are gaining relevance due to infrastructure limitations and rising demand for mobile neurological diagnostics. Companies are targeting the region through distributor expansion, clinician training programs, and scalable wireless monitoring platforms.

Saudi Arabia leads the Middle East & Africa EEG equipment market through large-scale hospital modernization initiatives and growing investment in digital healthcare infrastructure. Approximately 36% of tertiary hospitals integrated advanced neuro-monitoring systems into critical care expansion projects, increasing demand for AI-enabled EEG platforms and centralized neurological monitoring workflows.

United States – 34% market share in the EEG Equipment market, supported by advanced neurocritical care infrastructure, high AI-enabled EEG deployment, and strong enterprise hospital procurement activity.

China – 21% market share in the EEG Equipment market, driven by large-scale medical electronics manufacturing, expanding tertiary hospital infrastructure, and aggressive portable EEG deployment initiatives.

The EEG equipment market is led by global neurodiagnostic manufacturers competing against regional cost-focused suppliers and AI-driven digital health innovators. The top five players collectively control nearly 52% of market activity, with competition centered on wireless monitoring capability, AI-assisted interpretation speed, cloud integration, and supply-chain resilience. Advanced vendors improved diagnostic workflow efficiency by over 28% through automated analytics, while localized manufacturers reduced delivery timelines by approximately 19% using regional assembly strategies. Companies are strengthening hospital partnerships, expanding portable EEG portfolios, and integrating cybersecurity-focused software ecosystems. Rising interoperability requirements and regulatory validation costs are increasing entry barriers. Winning requires scalable neurodiagnostic platforms, enterprise-grade software integration, and operational reliability.

Natus Medical Incorporated

Nihon Kohden Corporation

Compumedics Limited

Cadwell Industries, Inc.

Electrical Geodesics, Inc.

Medtronic plc

Neurosoft

Micromed S.p.A.

Brain Products GmbH

ANT Neuro

NeuroWave Systems Inc.

EMS Biomedical

Clarity Medical Pvt. Ltd.

Neuroelectrics Barcelona S.L.U.

AI-assisted EEG interpretation platforms are transforming neurodiagnostic workflows through automated seizure detection, waveform classification, and predictive neurological analytics. More than 57% of advanced neurology centers integrated AI-supported EEG review systems by 2026, reducing diagnostic interpretation time by nearly 31% compared to conventional manual review models. Cloud-connected EEG architectures are also improving multi-site monitoring efficiency by approximately 24% through centralized neurological data access. Hospitals benefit from lower technician workload, faster triage decisions, and improved ICU neuro-monitoring consistency, while major manufacturers are expanding software ecosystems and cybersecurity-focused deployment frameworks to strengthen enterprise contracts.

Wireless and portable EEG technologies are rapidly replacing legacy wired configurations across emergency departments, ambulatory monitoring, and decentralized neurological care. Dry-electrode systems reduce patient preparation time by nearly 27% compared to gel-based legacy platforms, while lightweight wearable EEG devices improve monitoring mobility and patient compliance. Approximately 43% of newly deployed EEG units in Japan and the United States now support remote monitoring functionality. Companies investing in compact sensor engineering and battery-efficient architectures are gaining operational advantages in outpatient diagnostics and mobile neuro-monitoring expansion.

Between 2026 and 2028, disruptive technologies including EEG foundation models, edge AI processing, and brain-computer interface integration will reshape competitive positioning. Real-time embedded analytics platforms already improved continuous seizure detection accuracy by over 20% in pilot neurocritical care environments. Technology leaders with scalable AI infrastructure, interoperable cloud frameworks, and low-latency processing capabilities will secure stronger enterprise adoption as healthcare systems accelerate digital neurodiagnostic modernization.

November 2024 – Nihon Kohden acquired a 71.4% stake in NeuroAdvanced Corp., strengthening epilepsy-focused EEG and intracranial electrode integration across top U.S. hospitals. The expansion improved comprehensive neurodiagnostic deployment capability and advanced long-term neurology care positioning. Source: Nihon Kohden Global Site

March 2025 – Ceribell expanded deployment of its AI-powered point-of-care EEG system to more than 600 U.S. hospitals, while annual adoption increased 36%. The rollout strengthened rapid seizure detection workflows and accelerated emergency neuro-monitoring accessibility nationwide. Source: StockTitan

October 2025 – REVE Research Consortium introduced a large-scale EEG foundation model trained on 60,000 hours of neurological recordings from 25,000 subjects. The platform improved cross-dataset EEG generalization and accelerated AI-driven neurodiagnostic benchmarking efficiency. Source: arXiv

March 2026 – Firefly Neuroscience reported a 33x increase in EEG brain scan volumes and expanded its commercial network to 99 healthcare partners using NVIDIA-accelerated EEG analytics infrastructure, strengthening enterprise-scale AI neurodiagnostic deployment and neurological data processing capability. Source: Reddit – Pennystocks Discussion

The EEG Equipment Market report provides detailed analysis across Portable EEG Systems, Wireless EEG Systems, Video EEG Systems, Routine EEG Systems, and Ambulatory EEG Systems, covering operational adoption trends, deployment patterns, and enterprise purchasing behavior between 2026 and 2033. The study evaluates key applications including epilepsy diagnosis, ICU monitoring, cognitive assessment, neurological research, brain mapping, and sleep disorder monitoring. More than 52% of enterprise demand concentration is assessed across hospital-based neurodiagnostic infrastructure, while emerging outpatient and ambulatory deployment models are analyzed through workflow efficiency and portability metrics.

The report delivers region-wise intelligence across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting technology integration, manufacturing expansion, and regulatory modernization trends. It also examines AI-enabled neurodiagnostic systems, cloud-connected EEG ecosystems, wearable monitoring platforms, and cybersecurity-focused deployment frameworks. Strategic insights support investment planning, product positioning, partnership evaluation, competitive benchmarking, and expansion prioritization for manufacturers, healthcare providers, and digital neurodiagnostic technology companies operating within evolving neurological care environments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 75.61 Million |

|

Market Revenue in 2033 |

USD 125.14 Million |

|

CAGR (2026 - 2033) |

6.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Natus Medical Incorporated, Nihon Kohden Corporation, Compumedics Limited, Cadwell Industries, Inc., Electrical Geodesics, Inc., Medtronic plc, Neurosoft, Micromed S.p.A., Brain Products GmbH, ANT Neuro, NeuroWave Systems Inc., EMS Biomedical, Clarity Medical Pvt. Ltd., Neuroelectrics Barcelona S.L.U. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |