Reports

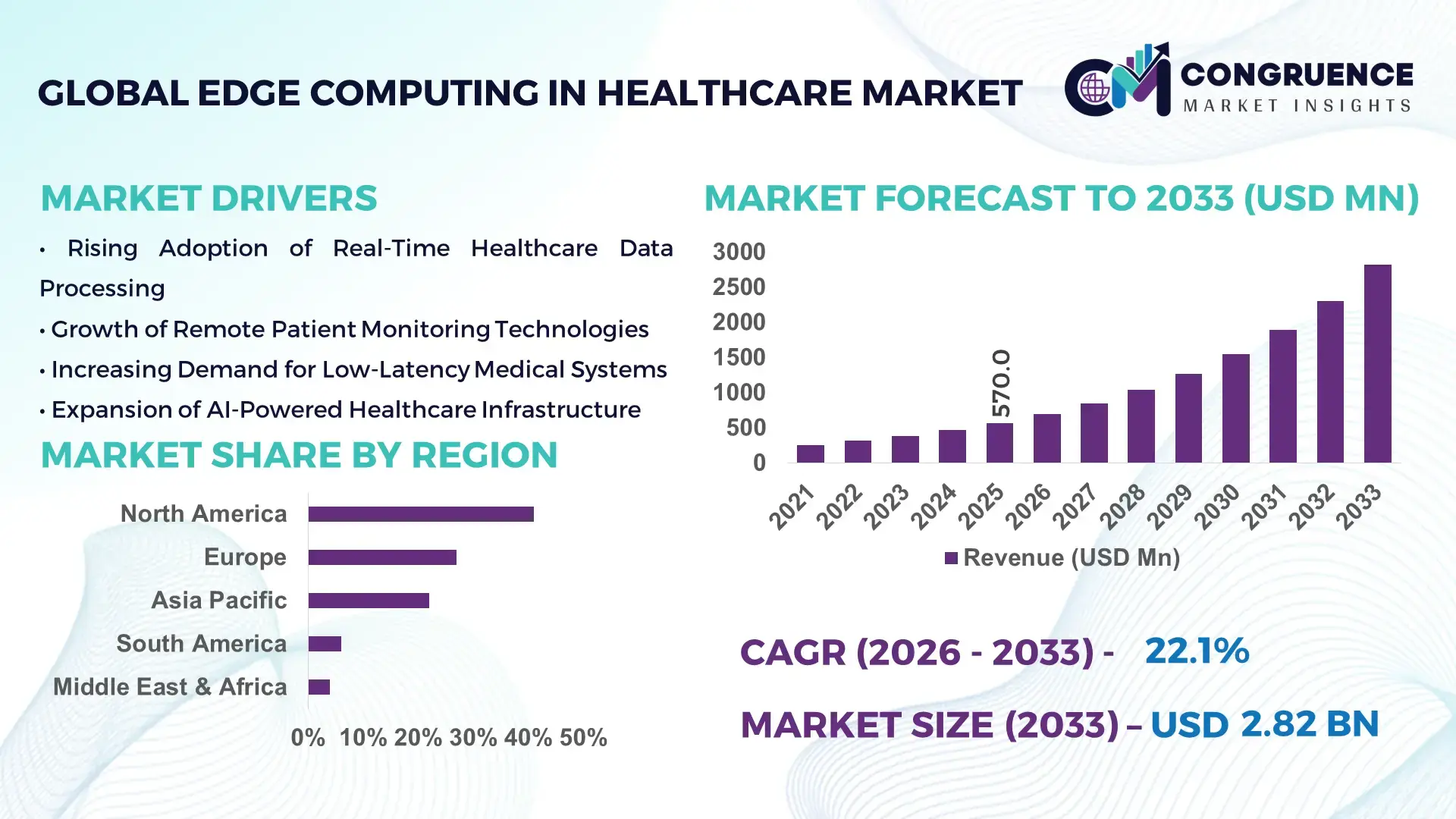

The Global Edge Computing in Healthcare Market was valued at USD 570.0 Million in 2025 and is anticipated to reach a value of USD 2,815.8 Million by 2033 expanding at a CAGR of 22.1% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily supported by increasing adoption of real-time healthcare data processing and connected medical devices requiring ultra-low latency computing.

The United States continues to play a central operational role in the Edge Computing in Healthcare Market through extensive healthcare digital infrastructure and strong investment in connected care technologies. The country hosts more than 6,100 hospitals and over 70% of them are actively integrating edge-enabled IoT devices for patient monitoring and diagnostics. Investments in healthcare AI and edge infrastructure exceeded USD 8 billion in 2024 across hospital networks and medical technology firms. Additionally, over 40% of telehealth platforms deployed in North America now integrate edge computing nodes to enable real-time analytics for remote patient monitoring and imaging diagnostics. Leading academic medical centers and research institutions are also testing distributed edge frameworks that process clinical imaging datasets locally, reducing latency by nearly 35% and improving response time for critical care applications.

Market Size & Growth:The market stood at USD 570.0 Million in 2025 and is projected to reach USD 2,815.8 Million by 2033, expanding at a CAGR of 22.1%. Growth is driven by rising demand for real-time patient monitoring and faster healthcare data analytics.

Top Growth Drivers:Adoption of IoT-enabled healthcare devices (62%), improvement in diagnostic processing efficiency (35%), and expansion of telemedicine infrastructure (48%).

Short-Term Forecast:By 2028, deployment of edge-enabled clinical analytics platforms is expected to improve data processing speed in hospital systems by nearly 40% while reducing cloud data transfer costs by around 28%.

Emerging Technologies:Integration of AI-powered edge nodes, 5G-enabled medical device connectivity, and federated learning for distributed clinical analytics are shaping next-generation healthcare infrastructure.

Regional Leaders:North America is projected to reach USD 1.2 Billion by 2033 with strong hospital IT investments; Europe is expected to reach USD 780 Million supported by digital health initiatives; Asia-Pacific may reach USD 620 Million driven by rapid hospital digitization.

Consumer/End-User Trends:Hospitals and diagnostic centers represent the largest adoption base, with over 55% deploying edge-enabled patient monitoring platforms to manage real-time clinical data and remote care workflows.

Pilot or Case Example:In 2024, a large hospital network deployed edge AI servers for radiology imaging analysis, improving diagnostic workflow efficiency by 32% and reducing imaging processing delays by nearly 40%.

Competitive Landscape:The market leader holds approximately 18% share, followed by several major competitors including prominent global cloud, networking, and healthcare IT providers competing through edge infrastructure and AI analytics solutions.

Regulatory & ESG Impact:Healthcare data privacy frameworks and digital health regulations are encouraging secure edge architectures, while sustainability initiatives are pushing vendors to reduce data-center energy consumption by nearly 20%.

Investment & Funding Patterns:Global investment in healthcare edge computing infrastructure exceeded USD 3.5 Billion in the last two years, with strong venture funding focused on AI-enabled clinical data processing platforms.

Innovation & Future Outlook:Advancements in edge-enabled medical imaging analytics, distributed AI healthcare models, and integration with hospital IoT ecosystems are expected to accelerate the digital transformation of healthcare delivery systems.

Edge computing solutions in healthcare are increasingly applied across hospital IT infrastructure, medical imaging diagnostics, telehealth platforms, and remote patient monitoring networks, contributing roughly 35%, 25%, 20%, and 20% of deployment share respectively. Rapid innovation in AI-enabled medical devices and distributed clinical data platforms is enhancing diagnostic speed and operational efficiency. Regulatory frameworks promoting digital health adoption, combined with growing demand for secure real-time healthcare analytics, are strengthening market expansion across North America, Europe, and emerging Asia-Pacific healthcare systems.

The Edge Computing in Healthcare Market is gaining strong strategic importance as healthcare systems increasingly require real-time analytics, low-latency data processing, and secure handling of sensitive medical information. Traditional centralized cloud models often introduce delays in critical healthcare workflows, especially in emergency diagnostics and continuous patient monitoring. Edge computing architecture enables healthcare providers to process patient data closer to the source, improving clinical response time and enabling distributed medical analytics.

Advanced edge-enabled AI diagnostics are significantly improving healthcare decision-making efficiency. For example, AI-powered edge medical imaging systems can process radiology scans locally and deliver diagnostic insights almost instantly. Edge-based AI diagnostics deliver nearly 45% faster clinical processing compared to traditional centralized cloud analysis, enabling hospitals to handle high volumes of imaging data while maintaining data privacy compliance.

Regional adoption patterns also demonstrate varied strategic pathways. North America dominates in deployment volume, supported by large hospital IT budgets and digital health infrastructure. Meanwhile, Asia-Pacific leads in enterprise adoption growth, with nearly 52% of large hospitals deploying pilot edge computing frameworksto support telemedicine, wearable device integration, and AI-driven diagnostics.

In the short term, digital health transformation initiatives will accelerate adoption. By 2028, AI-enabled edge analytics platforms are expected to improve remote patient monitoring efficiency by nearly 35%, particularly in managing chronic disease and home-based healthcare services.

Compliance and sustainability are also shaping market strategies. Healthcare organizations are committing to ESG targets by improving energy efficiency in computing infrastructure, with many hospital IT systems aiming for 30% reduction in data-center energy consumption by 2030through distributed edge architecture.

Micro-level implementations further demonstrate measurable benefits. In 2024, a major healthcare provider in Germany deployed edge AI infrastructure across multiple diagnostic centers, achieving a 38% reduction in medical imaging processing timewhile improving diagnostic throughput for emergency care units.

Looking forward, the Edge Computing in Healthcare Market is expected to evolve into a foundational pillar for digital healthcare ecosystems, enabling resilient healthcare operations, regulatory compliance, and sustainable data-driven clinical innovation.

The Edge Computing in Healthcare Market is evolving rapidly due to increasing digital transformation across global healthcare systems. Hospitals and medical institutions are generating massive volumes of clinical data from imaging equipment, wearable medical devices, and remote monitoring systems. Traditional centralized computing infrastructures struggle to process such data in real time, creating a strong demand for distributed edge architectures that can process information locally. Healthcare organizations are prioritizing technologies capable of delivering low-latency performance and secure patient data handling. Edge computing systems allow hospitals to analyze clinical data at the source, enabling faster response times for emergency care and improving operational efficiency in diagnostic departments. Additionally, the expansion of connected medical devices and hospital IoT networks is increasing the complexity of healthcare data environments. Many healthcare institutions are integrating edge computing frameworks to support AI-powered diagnostics, predictive analytics, and patient monitoring systems. The growing emphasis on digital health initiatives, regulatory compliance for patient data protection, and the need to improve healthcare infrastructure resilience are all shaping market dynamics. Healthcare technology vendors are increasingly focusing on developing scalable edge platforms that integrate AI, IoT, and secure cloud connectivity, allowing hospitals to build distributed healthcare data ecosystems capable of supporting modern clinical operations.

The rapid expansion of connected healthcare devices is one of the strongest drivers accelerating the Edge Computing in Healthcare Market. Hospitals and healthcare providers are deploying a growing number of wearable sensors, patient monitoring systems, and connected diagnostic equipment that continuously generate clinical data streams. Global healthcare IoT device installations have exceeded 50 million active devices across hospitals and remote patient monitoring platforms, creating a massive demand for localized data processing infrastructure. Edge computing enables these devices to process critical health data at the point of collection, reducing latency and allowing healthcare professionals to make faster medical decisions. For example, continuous patient monitoring systems can generate over 500 MB of data per patient each day, making centralized cloud processing inefficient for real-time diagnostics. Edge infrastructure helps reduce network congestion and enables hospitals to analyze data locally with response times reduced by up to 30%. Additionally, medical imaging systems such as CT scanners and MRI machines produce large datasets that require rapid processing for diagnostic evaluation. Edge-based AI processing allows imaging analysis to occur within hospital networks, improving workflow efficiency and accelerating treatment decisions. As hospitals continue expanding digital patient monitoring and telehealth services, the integration of edge computing infrastructure is becoming essential to support reliable, secure, and real-time healthcare data processing.

Despite its advantages, the adoption of edge computing in healthcare is constrained by high infrastructure and integration costs. Implementing distributed computing architectures requires hospitals to invest in specialized edge servers, secure networking equipment, and advanced data management software. Many healthcare facilities operate on limited IT budgets, making large-scale deployment of edge computing infrastructure financially challenging. Healthcare systems also require strict compliance with patient data protection regulations, which increases the complexity of deploying edge computing frameworks. Hospitals must implement secure encryption, identity management systems, and compliance monitoring tools to ensure that distributed edge nodes meet healthcare data privacy standards. These additional security requirements significantly increase deployment costs and implementation timelines. Integration with existing hospital IT systems is another challenge. Many healthcare organizations still rely on legacy electronic health record platforms and older medical devices that are not designed to support edge computing frameworks. Upgrading or integrating these systems can require extensive customization and technical expertise. As a result, some healthcare providers delay adoption due to concerns about operational disruption and high transition costs, slowing overall market expansion.

The rapid growth of telemedicine and remote healthcare services presents a major opportunity for the Edge Computing in Healthcare Market. Healthcare providers are increasingly offering virtual consultations, remote diagnostics, and continuous monitoring for chronic disease management. These services generate large volumes of real-time patient data from wearable devices, mobile health applications, and home monitoring systems. Edge computing enables healthcare providers to process this data locally, allowing faster analysis and reducing dependency on centralized cloud servers. This capability is particularly important for remote patient monitoring programs where continuous data streams must be analyzed quickly to detect medical anomalies. For example, wearable heart monitoring devices can generate thousands of physiological data points daily, requiring immediate processing to detect irregularities. Healthcare systems are also deploying edge computing to support rural healthcare delivery where network connectivity to centralized data centers may be limited. Localized processing allows medical facilities to perform diagnostic analysis and patient monitoring even with limited internet bandwidth. As telehealth adoption expands globally and healthcare providers invest in digital care delivery models, edge computing platforms will play a crucial role in enabling scalable and efficient remote healthcare ecosystems.

Cybersecurity and data governance issues represent significant challenges for the Edge Computing in Healthcare Market. Healthcare data is highly sensitive and must be protected under strict regulatory frameworks. Distributed edge architectures increase the number of network endpoints where patient data is processed and stored, creating additional security vulnerabilities. Each edge node must implement strong encryption protocols, identity verification systems, and continuous security monitoring to prevent unauthorized access to medical data. Healthcare cyberattacks have increased significantly in recent years, with hospitals becoming frequent targets of ransomware and data breaches. Managing cybersecurity across hundreds of distributed edge devices can be complex and resource-intensive for healthcare organizations. Data governance is another major challenge. Healthcare providers must ensure that patient data processed at edge locations remains compliant with privacy regulations and that data synchronization between edge systems and centralized healthcare databases is accurate. Maintaining consistent data standards across distributed computing environments requires advanced management platforms and trained cybersecurity professionals. These challenges create operational complexity for healthcare organizations adopting edge computing technologies, slowing deployment in some healthcare systems.

Rapid Expansion of Edge AI in Medical Imaging Diagnostics: Hospitals are increasingly deploying edge AI platforms to analyze CT scans, MRIs, and ultrasound data directly within hospital networks. Studies indicate that nearly 47% of large hospitalshave integrated AI-enabled imaging analysis systems capable of processing data locally, reducing diagnostic turnaround time by 35%and enabling real-time triage for emergency cases.

Surge in Remote Patient Monitoring Infrastructure: Remote patient monitoring programs are expanding rapidly with wearable healthcare devices and connected biosensors. Over 60% of chronic disease management programsnow integrate wearable monitoring platforms capable of transmitting patient data every few seconds. Edge computing nodes process these signals locally, reducing cloud bandwidth consumption by 30%while improving real-time alert systems.

Integration of 5G Networks with Healthcare Edge Systems: The rollout of 5G infrastructure is accelerating the adoption of edge computing in healthcare environments. More than 40% of new smart hospital projectsincorporate 5G-enabled edge networks to support telemedicine, robotic surgery support, and real-time medical imaging transfer. These deployments improve network latency performance by nearly 50%compared to legacy hospital networks.

Growth of Distributed Healthcare Data Platforms: Healthcare providers are increasingly shifting toward decentralized data processing models where clinical data is analyzed across distributed edge nodes. Approximately 52% of healthcare IT departmentsare investing in distributed data architectures that allow hospitals to process sensitive patient data locally while maintaining secure synchronization with central healthcare databases.

The Edge Computing in Healthcare Market is segmented based on type, application, and end-user categories, reflecting the wide range of technologies and operational environments where distributed computing is being deployed. Healthcare organizations are adopting edge infrastructure to manage high-volume clinical data streams generated by medical imaging systems, wearable devices, and hospital IoT networks.

Type segmentation highlights the technology components enabling edge deployment, including hardware platforms, software solutions, and service-based offerings. Hardware infrastructure such as edge servers and networking equipment forms the backbone of local data processing systems, while software platforms enable real-time analytics and device management. Application segmentation illustrates how edge computing is integrated across diagnostic imaging, patient monitoring, telemedicine, and hospital workflow management systems. End-user segmentation demonstrates the diverse healthcare organizations deploying edge solutions, including hospitals, diagnostic laboratories, research institutions, and telehealth providers. Hospitals represent the primary deployment environment due to their complex data infrastructure and continuous clinical data generation. Meanwhile, telehealth providers and digital health startups are increasingly leveraging edge computing to deliver scalable remote care platforms.

The Edge Computing in Healthcare Market by type includes Hardware, Software, and Services. Among these, Hardware currently represents the leading segment, accounting for approximately 48% of total deployments, as hospitals require high-performance edge servers, storage devices, and specialized networking equipment to process medical data locally. Medical imaging systems and patient monitoring infrastructure rely heavily on localized hardware processing capabilities, making edge servers a critical component of hospital IT architecture. Software solutions account for nearly 32% of deployments, supporting device management, real-time analytics, and integration with electronic health record systems. Healthcare organizations are increasingly deploying AI-driven edge software platforms that enable predictive analytics for patient monitoring and diagnostic support. Meanwhile, Services represent roughly 20% of the market, including consulting, integration, and managed services supporting healthcare IT modernization initiatives. The software segment is currently the fastest-growing type, expanding at an estimated CAGR of around 24%, driven by rising demand for AI-powered healthcare analytics platforms and real-time patient monitoring systems that can run directly on edge infrastructure. The remaining segments collectively contribute approximately 52% of the market, providing critical infrastructure support for distributed healthcare data ecosystems.

In 2024, a major academic medical research center deployed AI-enabled edge computing hardware for radiology analysis, enabling automated scan triage that reduced diagnostic waiting times for over 8,000 imaging cases annually.

The Edge Computing in Healthcare Market applications include Medical Imaging, Remote Patient Monitoring, Telemedicine, and Hospital Workflow Management. Medical imaging represents the leading application segment with approximately 38% adoption share, as imaging equipment generates extremely large datasets that must be processed rapidly for clinical diagnostics. Edge computing allows hospitals to analyze imaging data locally, enabling faster clinical interpretation and reducing dependence on centralized cloud servers. Remote patient monitoring accounts for nearly 27% of deployments, supported by the increasing use of wearable health devices and connected biosensors for chronic disease management. However, telemedicine applications are the fastest-growing segment with an estimated CAGR of around 25%, driven by expanding digital healthcare services and demand for remote consultations. Hospital workflow management and data integration systems collectively contribute approximately 35% of the application landscape, enabling hospitals to manage clinical operations and patient data flows more efficiently. In terms of adoption trends, around 45% of hospitals globally are currently testing AI-driven edge platforms to support imaging diagnostics and patient monitoring. Additionally, over 50% of telehealth providers are integrating edge infrastructure to improve real-time video consultation performance and data processing reliability.

In 2025, a national healthcare system deployed edge computing platforms across more than 120 hospitals to enable real-time imaging diagnostics, improving emergency department diagnostic efficiency by approximately 33%.

The Edge Computing in Healthcare Market by end-user includes Hospitals, Diagnostic Centers, Research Institutions, and Telehealth Providers. Hospitals dominate the market with nearly 55% deployment share, as they operate complex IT infrastructures that require high-performance data processing capabilities. Hospitals generate large volumes of patient monitoring data, imaging scans, and clinical records, making edge computing essential for managing data workloads and supporting real-time clinical decision-making. Diagnostic centers account for approximately 18% of the market, focusing heavily on imaging analysis and laboratory data processing systems. Telehealth providers represent the fastest-growing end-user segment with an estimated CAGR of around 26%, driven by the rapid expansion of virtual healthcare services and remote patient care platforms. Research institutions and healthcare innovation laboratories collectively contribute around 27% of the market, primarily using edge computing platforms to support AI model training, medical imaging research, and distributed clinical data analysis. In terms of adoption behavior, over 42% of hospitals in North America are actively piloting edge computing platforms for AI-driven diagnostic support systems. Additionally, nearly 35% of healthcare research institutions globally are integrating edge computing into clinical data analytics frameworksto accelerate medical research and patient data processing.

In 2024, a large European university hospital network implemented distributed edge computing infrastructure across 15 clinical research laboratories, enabling real-time genomic data processing and reducing research data processing time by nearly 40%.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 24.6% between 2026 and 2033.

North America leads global adoption due to the presence of more than 6,000 hospitals equipped with advanced digital health infrastructureand high integration of IoT-enabled medical devices. Over 65% of major healthcare networks in the region deploy edge computing platformsto support real-time imaging analytics and remote patient monitoring systems. Europe accounts for approximately 27% of global demand, supported by strong regulatory frameworks encouraging secure healthcare data processing and the expansion of digital hospital programs across Germany, France, and the United Kingdom. Meanwhile, Asia-Pacific represents roughly 22% of the global deployment base, but is experiencing the fastest infrastructure expansion as countries accelerate healthcare digitization programs. China and Japan together operate more than 35,000 hospital facilities, many integrating edge-enabled diagnostic equipment and AI-powered imaging platforms. South America holds close to 6% of the global market, led by Brazil and Argentina with increasing investments in hospital IT modernization. The Middle East & Africa account for around 4% share, driven by smart hospital projects in the UAE, Saudi Arabia, and South Africa that emphasize real-time healthcare data processing and telemedicine infrastructure.

North America represents approximately 41% of the global Edge Computing in Healthcare Market, making it the largest regional deployment hub for distributed healthcare computing infrastructure. The region benefits from a highly developed healthcare ecosystem with over 1 million hospital beds across major healthcare networks, generating vast volumes of clinical data that require real-time processing. Key industries driving demand include hospital networks, medical imaging diagnostics, telehealth providers, and healthcare IT services. The regulatory environment also supports digital healthcare innovation through frameworks emphasizing patient data protection and secure computing environments. Healthcare providers are increasingly adopting edge-based AI platforms capable of processing radiology images, genomic data, and patient monitoring signals locally within medical facilities. More than 70% of large hospital systems in the region operate connected medical device ecosystems, creating a strong requirement for localized data processing infrastructure. Technology adoption is further strengthened by the region’s leadership in cloud and networking technologies. For example, Cisco Systemshas been actively deploying edge infrastructure solutions designed specifically for hospital IT networks, enabling real-time clinical data analytics. Consumer behavior also plays a role in adoption trends. Healthcare institutions demonstrate high enterprise adoption rates of digital healthcare technologies, particularly for remote patient monitoring and AI-assisted diagnostics.

Europe accounts for roughly 27% of the global Edge Computing in Healthcare Market, driven by strong healthcare systems and regulatory frameworks supporting digital transformation. Key European markets include Germany, the United Kingdom, and France, which collectively represent over 60% of the region’s hospital IT modernization initiatives. The European healthcare sector includes more than 15,000 hospitals, many of which are integrating edge computing solutions to manage medical imaging data, patient monitoring systems, and AI-powered diagnostic applications. Regulatory bodies across the region emphasize strong data protection standards and secure processing of medical information, encouraging hospitals to adopt decentralized computing frameworks. Hospitals are increasingly implementing edge computing infrastructure to ensure that sensitive patient data is processed locally rather than transmitted to external cloud systems. Technological innovation is also shaping regional adoption. European research hospitals are experimenting with federated learning frameworks, where AI models are trained across multiple hospital datasets without transferring patient data between institutions. An example of regional industry activity includes Siemens Healthineers, which has developed advanced imaging and digital healthcare platforms that integrate edge-based processing capabilities for hospital diagnostic equipment. Consumer behavior across the region reflects strong compliance-driven adoption patterns, where healthcare providers prioritize secure and explainable digital health technologies.

Asia-Pacific represents approximately 22% of global deployment volumebut ranks as the fastest expanding regional ecosystem for edge-enabled healthcare technologies. Major consuming countries include China, Japan, India, and South Korea, where healthcare infrastructure modernization is accelerating rapidly. China alone operates more than 34,000 hospitals, while India has over 25,000 healthcare facilities, creating substantial demand for efficient medical data processing technologies. Healthcare infrastructure expansion and digital health initiatives are encouraging hospitals to deploy localized data analytics systems capable of supporting telemedicine and AI-driven diagnostics. Governments across the region are investing heavily in digital health platforms and connected hospital infrastructure. Innovation hubs in countries such as Japan and South Korea are developing next-generation medical technologies integrating edge computing with robotics-assisted surgery systems and real-time medical imaging analytics. A notable regional industry participant is Fujitsu, which has been developing distributed healthcare data platforms designed to support hospital AI analytics and patient monitoring systems. Consumer behavior in the region reflects strong technology adoption trends driven by mobile healthcare platforms and digital health applications, with more than 50% of urban hospitals experimenting with AI-assisted diagnostics and telehealth services.

South America accounts for roughly 6% of the global Edge Computing in Healthcare Market, with the majority of deployments concentrated in Brazil and Argentina. Brazil operates more than 7,000 hospitals and healthcare facilities, making it the largest healthcare market in the region. Healthcare providers are gradually integrating digital health infrastructure to improve clinical data management and patient monitoring systems. Healthcare IT modernization programs across the region emphasize improved hospital data processing capabilities and expansion of telemedicine platforms. Governments are supporting healthcare technology investments through digital infrastructure development initiatives and medical data management frameworks. Brazilian healthcare institutions are increasingly investing in AI-enabled diagnostic platforms capable of analyzing medical imaging and patient monitoring data locally within hospital networks. This reduces dependency on centralized cloud infrastructure and improves response time for clinical decision-making. Regional industry participation is growing, with technology providers collaborating with healthcare institutions to deploy secure computing platforms for clinical applications. Consumer behavior in the region indicates rising demand for digital healthcare services, particularly telemedicine platforms that allow remote consultations and monitoring of chronic diseases.

The Middle East & Africa region holds approximately 4% share of the global Edge Computing in Healthcare Market, with major growth centers located in the United Arab Emirates, Saudi Arabia, and South Africa. Healthcare infrastructure modernization projects across the region are introducing advanced hospital technologies including AI-enabled diagnostics, robotic surgery systems, and connected patient monitoring platforms. Smart hospital initiatives are a key driver of edge computing adoption. Countries such as the UAE and Saudi Arabia are investing heavily in digital healthcare ecosystems that integrate IoT-enabled medical devices and real-time patient data analytics. Many newly constructed hospitals are designed with integrated digital infrastructure capable of supporting distributed computing systems. Technological modernization programs also emphasize telemedicine and remote healthcare services, particularly in rural and underserved regions where centralized healthcare access may be limited. Regional technology firms and healthcare solution providers are collaborating to implement localized healthcare data processing systems that improve patient care efficiency and diagnostic speed. Consumer behavior across the region reflects increasing acceptance of digital health services, especially mobile-based healthcare platforms and AI-assisted clinical diagnostics.

United States – 34% market share: due to extensive hospital digital infrastructure, high adoption of AI-powered diagnostics, and strong investments in connected healthcare devices.

China – 18% market share: supported by large-scale healthcare digitization initiatives, extensive hospital networks, and rapid deployment of AI-enabled medical technologies.

The Edge Computing in Healthcare Market features a moderately fragmented competitive landscapewith a mix of global technology providers, healthcare IT vendors, networking companies, and specialized edge computing platform developers. More than 45 active companiescurrently operate in the market, offering solutions that combine edge infrastructure, AI-enabled healthcare analytics, IoT integration, and secure medical data processing.

The top five companies collectively account for nearly 42% of the global market presence, reflecting strong competition among leading technology firms that specialize in healthcare digital infrastructure. These companies focus on delivering scalable edge platforms capable of supporting hospital networks, medical imaging systems, remote patient monitoring technologies, and telemedicine platforms.

Strategic partnerships between healthcare institutions and technology vendors are becoming increasingly common. Hospitals are collaborating with technology companies to deploy distributed data processing systems capable of managing high volumes of clinical data generated by connected medical devices.

Innovation remains a major competitive differentiator. Companies are investing heavily in AI-powered diagnostic platforms, real-time healthcare analytics engines, and secure distributed data architecturesdesigned to process medical data closer to its source. Several vendors are also launching integrated healthcare edge platforms that combine hardware infrastructure, software analytics, and managed services.

Mergers and strategic acquisitions are further shaping the competitive environment as companies expand their capabilities in healthcare IT infrastructure and edge computing services. This dynamic environment is driving continuous innovation and strengthening the overall technological maturity of the market.

Dell Technologies

Hewlett Packard Enterprise

IBM Corporation

Microsoft Corporation

Intel Corporation

Siemens Healthineers

Fujitsu Limited

NVIDIA Corporation

Oracle Corporation

Schneider Electric

Red Hat

VMware

Huawei Technologies

Lenovo Group

Nokia Corporation

Technological advancements are playing a crucial role in shaping the Edge Computing in Healthcare Market, enabling healthcare providers to process massive volumes of patient data efficiently and securely. One of the most significant developments is the integration of artificial intelligence with edge computing platforms, allowing hospitals to perform real-time analytics directly at the point of care. AI-enabled edge systems are capable of processing medical imaging data such as CT scans and MRIs locally, reducing diagnostic processing times by nearly 35% compared to centralized data processing models.

Another important technological trend involves the deployment of 5G-enabled edge networks within hospital environments. These networks support ultra-low latency data transmission between connected medical devices, surgical robotics systems, and diagnostic equipment. Hospitals implementing 5G-enabled edge infrastructure report improvements in device communication efficiency of up to 45%, enabling faster response times in emergency care environments.

The integration of Internet of Medical Things (IoMT) devicesis also accelerating demand for distributed computing architectures. Healthcare facilities increasingly rely on wearable sensors, patient monitoring devices, and connected diagnostic tools that generate continuous streams of clinical data. Edge computing platforms allow hospitals to process this data locally, reducing bandwidth requirements while maintaining high levels of data security.

Another emerging technology is federated learning, which allows healthcare institutions to train AI models across multiple hospital datasets without transferring sensitive patient information outside institutional networks. This approach improves collaboration between healthcare providers while maintaining compliance with patient data protection regulations.

Additionally, vendors are developing micro data centers designed specifically for healthcare environments, capable of operating within hospital facilities and supporting high-performance computing workloads. These compact edge data centers enable hospitals to deploy scalable computing infrastructure capable of supporting AI diagnostics, telemedicine platforms, and advanced healthcare analytics.

• In March 2025, NVIDIAannounced a collaboration with GE HealthCareto develop autonomous diagnostic imaging systems using the NVIDIA Isaac™ for Healthcare simulation platform. The initiative enables development of autonomous X-ray and ultrasound systems that can automate tasks such as patient positioning, scanning, and quality validation through AI-driven imaging workflows. Source: www.nvidia.com

• In March 2024, NVIDIAlaunched more than 25 generative AI microservicesdesigned for healthcare, drug discovery, and digital health applications. The services integrate optimized models and APIs that allow hospitals and healthcare enterprises to build and deploy AI-enabled healthcare applications across cloud, on-premise, and edge environments.

• In June 2024, NVIDIAintroduced enterprise software support for the NVIDIA IGX platform with Holoscan, enabling real-time AI workloads for healthcare and other mission-critical edge environments. The platform allows hospitals and medical device manufacturers to run AI applications directly at the edge with improved security, reliability, and real-time processing capabilities.

• In March 2024, NVIDIAhighlighted the rapid expansion of AI-enabled medical technologies powered by its platforms, noting that over 700 FDA-cleared AI-enabled medical devicesare now available globally. Many of these devices use edge AI computing architectures to process imaging and diagnostic data locally within healthcare environments.

The Edge Computing in Healthcare Market Report provides a comprehensive analysis of the global healthcare technology ecosystem that supports real-time medical data processing and distributed computing infrastructure. The report covers a broad range of technology segments including edge hardware infrastructure, distributed analytics software platforms, and healthcare IT services that enable localized data processing within medical environments.

The scope includes analysis of multiple healthcare applications such as medical imaging diagnostics, remote patient monitoring systems, telemedicine platforms, hospital workflow management systems, and connected medical device ecosystems. These applications collectively generate vast volumes of clinical data that require high-performance computing infrastructure capable of delivering near real-time analysis.

The report also evaluates deployment patterns across different end-user environments including hospitals, diagnostic laboratories, healthcare research institutions, and telehealth providers. Hospitals represent the largest deployment environment due to their complex data processing needs and continuous clinical data generation from imaging equipment and patient monitoring systems.

Geographically, the report examines market activity across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing detailed insights into regional healthcare infrastructure development, digital health adoption trends, and technological innovation hubs.

Technology coverage includes AI-powered diagnostic analytics, IoMT device integration, 5G-enabled healthcare connectivity, distributed healthcare data platforms, and secure edge computing frameworksdesigned to process patient data locally while maintaining compliance with healthcare data privacy regulations. The report also explores emerging innovations such as federated learning models, micro data centers for hospitals, and next-generation healthcare analytics platforms.

Overall, the scope of the report provides decision-makers with strategic insights into healthcare digital transformation trends, technology adoption patterns, and the operational frameworks that will shape the future of distributed healthcare data processing systems worldwide.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 570.0 Million |

| Market Revenue (2033) | USD 2,815.8 Million |

| CAGR (2026–2033) | 22.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Cisco Systems; Dell Technologies; Hewlett Packard Enterprise; IBM Corporation; Microsoft Corporation; Intel Corporation; Siemens Healthineers; Fujitsu Limited; NVIDIA Corporation; Oracle Corporation; Schneider Electric; Red Hat; VMware; Huawei Technologies; Lenovo Group; Nokia Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |