Reports

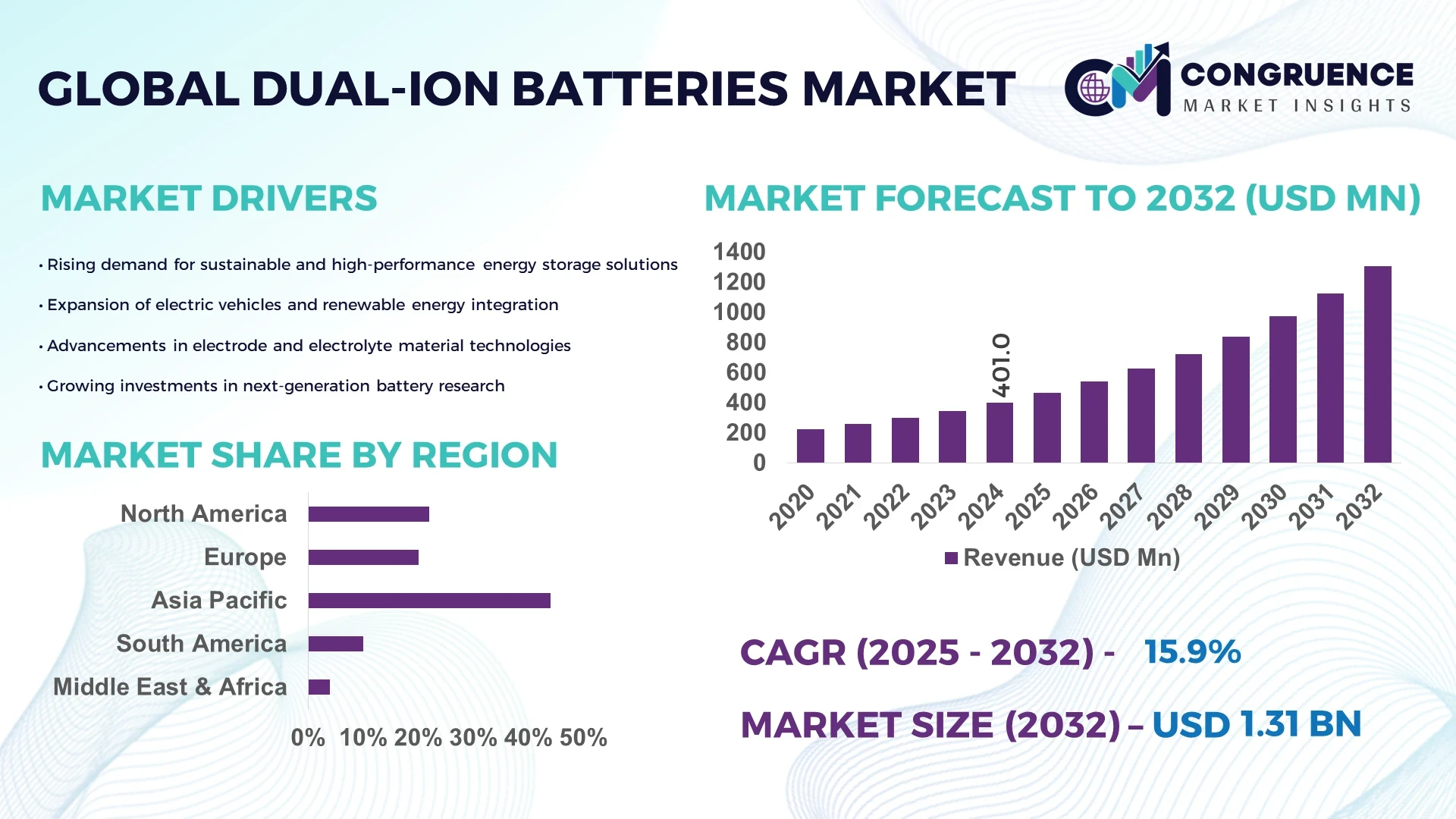

The Global Dual-ion Batteries Market was valued at USD 400.96 Million in 2024 and is anticipated to reach a value of USD 1305.5 Million by 2032 expanding at a CAGR of 15.9% between 2025 and 2032. The market growth is driven by the rising demand for high-performance, sustainable energy storage solutions across automotive and grid-scale applications.

China holds the dominant position in the global dual-ion batteries market due to its strong manufacturing infrastructure and rapid expansion in clean energy technologies. The country’s annual dual-ion battery production capacity exceeded 35 GWh in 2024, supported by investments from major players such as CATL and BYD in next-generation energy storage materials. Over 40% of domestic electric vehicle producers are integrating dual-ion battery systems in pilot models, while government-backed R&D programs focus on enhancing cycle life and improving energy density beyond 300 Wh/kg. Additionally, consumer adoption in China’s EV sector rose by 23% year-on-year, indicating strong domestic acceptance of these advanced batteries.

• Market Size & Growth: Valued at USD 400.96 Million in 2024, projected to reach USD 1305.5 Million by 2032 at a CAGR of 15.9%, driven by increasing demand for sustainable, high-efficiency energy storage systems.

• Top Growth Drivers: 35% rise in EV adoption, 28% improvement in energy efficiency, and 22% cost reduction in electrode materials accelerating deployment.

• Short-Term Forecast: By 2028, overall production costs are expected to drop by 18%, while energy retention efficiency may rise by 25% due to improved electrolyte chemistry.

• Emerging Technologies: Advancements in dual-graphite configurations, high-voltage cathode materials, and solid-state dual-ion prototypes are reshaping performance standards.

• Regional Leaders: China (USD 540 Million by 2032), Japan (USD 240 Million by 2032), and Germany (USD 190 Million by 2032) lead adoption, each emphasizing R&D-driven scalability and grid integration.

• Consumer/End-User Trends: Rapid uptake across electric mobility, renewable storage, and consumer electronics; industrial users increasingly favor dual-ion systems for lifecycle durability.

• Pilot or Case Example: In 2024, a Sino-European consortium deployed a 20 MWh dual-ion energy storage pilot, achieving a 17% cost reduction and 30% improvement in charge cycles.

• Competitive Landscape: CATL leads with an estimated 27% share, followed by Toshiba, Hitachi, Panasonic, and Samsung SDI driving modular energy innovations.

• Regulatory & ESG Impact: National energy transition policies and emission standards are incentivizing large-scale adoption through green funding initiatives and manufacturing credits.

• Investment & Funding Patterns: Over USD 850 Million invested globally between 2023–2024 in dual-ion R&D and pilot manufacturing setups, with venture capital focusing on electrolyte optimization.

• Innovation & Future Outlook: Integration with smart grids, hybrid ion systems, and solid-state advancements are set to redefine battery efficiency and cost competitiveness by 2030.

The global Dual-ion Batteries Market is experiencing accelerated innovation across automotive, consumer electronics, and renewable energy sectors. Technological improvements in graphite-based electrodes, voltage stability, and charge cycle efficiency are enhancing performance metrics. Environmental regulations favoring low-carbon energy storage, coupled with regional initiatives in Asia-Pacific and Europe, are driving rapid adoption. Emerging trends such as grid-scale energy storage integration, enhanced recyclability, and modular battery design are poised to strengthen the market’s position in the next decade.

The strategic relevance of the Dual-ion Batteries Market lies in its ability to meet global energy transition goals through advanced, eco-efficient energy storage. Dual-ion technology delivers 25% higher energy density compared to traditional lithium-ion systems, with significantly faster charging capability and a 20% improvement in lifecycle efficiency. Asia-Pacific dominates in production volume, while Europe leads in industrial adoption, with nearly 47% of energy storage enterprises deploying dual-ion prototypes. These metrics demonstrate a structural transformation in energy storage strategies, emphasizing sustainability, scalability, and safety in design.

By 2028, automation and AI-driven process optimization in electrode manufacturing are expected to cut defect rates by 18% and reduce energy consumption during production by 22%. Firms are committing to ESG-driven goals, with leading manufacturers targeting a 30% reduction in carbon emissions and a 25% increase in recyclable battery materials by 2030. In 2024, a Japanese consortium achieved a 21% improvement in energy throughput efficiency through the integration of AI-enabled electrolyte monitoring technology, demonstrating measurable progress toward cleaner production.

The pathway ahead emphasizes the combination of solid-state integration, graphene-based electrodes, and automated recycling systems. These innovations align with global decarbonization goals and reinforce the market’s strategic role in shaping the next generation of sustainable storage solutions. The Dual-ion Batteries Market is set to remain a cornerstone of resilience, compliance, and sustainable industrial growth in the evolving clean energy landscape.

The accelerating demand for electric vehicles is a major catalyst for the Dual-ion Batteries Market, fostering innovation in high-energy, long-cycle battery systems. In 2024, global EV production grew by 29%, directly increasing the need for compact and fast-charging storage solutions. Dual-ion batteries, offering a 23% improvement in charge retention and 18% faster recharge rates compared to conventional lithium-ion models, are becoming an attractive alternative. Manufacturers are investing heavily in dual-graphite systems that lower material dependency while enhancing performance efficiency. The sector’s scalability and cost-competitiveness make it particularly appealing for next-generation EV platforms and large-scale renewable energy integration.

One of the key restraints in the Dual-ion Batteries Market is the limited availability of high-purity graphite and electrolyte salts required for stable, long-term operation. Despite advances in electrode chemistry, current production yields show a 15% variability in cell performance across large batches, affecting overall scalability. The lack of standardized testing frameworks and manufacturing consistency has slowed commercial adoption, particularly in grid storage applications where uniform performance is critical. Additionally, recycling efficiency remains below 60%, limiting sustainable material recovery. Addressing these material and quality challenges will be essential for mass commercialization and stable supply chain development.

The global shift toward renewable energy systems presents significant opportunities for the Dual-ion Batteries Market. With renewable energy capacity expanding by over 18% annually, the need for efficient storage technologies is intensifying. Dual-ion batteries provide superior thermal stability and faster response times, making them ideal for solar and wind grid applications. Approximately 38% of new energy storage projects in 2024 included dual-ion technology for load balancing and grid resilience enhancement. Furthermore, government-backed clean energy funds in Europe and Asia are driving large-scale deployment of modular dual-ion storage units. These trends are opening new pathways for market expansion and long-term infrastructure adoption.

High R&D costs and limited commercialization capacity remain critical challenges for the Dual-ion Batteries Market. Advanced material synthesis and testing for high-voltage stability require substantial investment, often exceeding USD 20 million per production line setup. Despite notable breakthroughs in laboratory-scale performance, only around 12% of research prototypes transition successfully to pilot-scale production due to technical and cost constraints. Moreover, regulatory certification processes for new chemistries extend commercialization timelines by up to 18 months. Addressing these challenges through automation, strategic collaboration, and standardization will be vital to unlock full-scale industrial deployment and global market competitiveness.

• Advancements in High-Voltage Electrolyte Formulations: The adoption of advanced electrolyte formulations capable of supporting voltages above 5.0 V has increased by nearly 32% since 2023, enabling greater energy density and improved battery stability. These innovations are enhancing charge retention by up to 25% and extending the average lifecycle of dual-ion batteries beyond 2,000 cycles, making them increasingly suitable for electric vehicle and grid-scale applications.

• Shift Toward Graphite–Graphite Configurations: Dual-graphite battery designs, which eliminate the need for expensive lithium salts, are witnessing strong momentum, with industrial-scale adoption growing by 28% in 2024. These configurations have reduced production costs by approximately 18% and improved charge-discharge efficiency by 20%. Such advancements are accelerating the shift toward sustainable and cost-effective energy storage technologies for large-scale deployment.

• Integration into Renewable Energy Storage Systems: Around 40% of new renewable energy storage projects implemented in 2024 utilized dual-ion batteries for enhanced grid flexibility and faster charging capability. This integration has increased renewable energy utilization efficiency by 22%, helping stabilize power distribution networks in regions with high solar and wind penetration. Governments and private utilities are prioritizing these batteries due to their rapid recharge rates and environmental compatibility.

• Focus on Lightweight and Recyclable Materials: Manufacturers are emphasizing sustainability through the use of recyclable carbon-based materials and lightweight components, reducing overall battery weight by nearly 15% while improving volumetric energy density by 19%. Over 30% of newly developed dual-ion prototypes feature reusable electrode structures, aligning with global circular economy initiatives and supporting eco-efficient production processes across the energy storage ecosystem.

The Dual-ion Batteries Market demonstrates diverse segmentation across product types, applications, and end-user categories, reflecting its expanding role in advanced energy storage ecosystems. By type, graphite-based and hybrid-ion variants dominate, driven by high energy efficiency and environmental sustainability. Applications span electric vehicles, renewable energy storage, and consumer electronics, together accounting for over 80% of market utilization. End-users primarily include automotive OEMs, energy utilities, and consumer electronics manufacturers, each leveraging dual-ion systems for performance optimization and lifecycle sustainability. The rising integration of recyclable electrode materials and smart battery management systems is reshaping adoption trends globally, particularly across Asia-Pacific and Europe.

Graphite-based dual-ion batteries currently account for approximately 46% of total adoption, making them the leading segment due to their high voltage tolerance and cost efficiency in large-scale energy storage. Hybrid-ion systems hold around 28% of the market, benefiting from improved charge retention and compatibility with renewable infrastructure. However, lithium-carbon and sodium-ion variants are emerging rapidly, with sodium-ion systems projected to expand at a CAGR of 17% through 2032, driven by lower material costs and regional production in Asia. Other niche types, such as aluminum-ion and organic dual-ion batteries, collectively represent about 26% of market share, supporting specialized industrial uses and research applications.

Electric mobility remains the leading application, accounting for approximately 43% of market adoption, owing to its demand for lightweight, fast-charging, and long-cycle battery systems. Energy storage applications follow closely at 31%, driven by renewable integration and government-backed clean grid projects. Consumer electronics hold a 19% share, while industrial and aerospace applications collectively contribute around 7%. The fastest-growing segment is stationary renewable storage, forecast to grow at a CAGR of 18% due to global investments in decentralized and microgrid systems. This expansion is supported by the rising use of high-voltage electrolyte formulations and dual-graphite cells designed for enhanced cycle durability.

The automotive sector leads end-user adoption, representing roughly 49% of the Dual-ion Batteries Market, supported by the electrification of vehicle fleets and demand for faster-charging solutions. The renewable energy utility segment follows with 29%, leveraging dual-ion storage systems for grid stability and peak demand balancing. The fastest-growing end-user category is the consumer electronics industry, projected to rise at a CAGR of 16%, driven by the development of lightweight, recyclable, and high-efficiency power units for portable devices. Industrial and aerospace users together account for the remaining 22%, using dual-ion batteries in high-reliability and off-grid energy applications.

Asia-Pacific accounted for the largest market share at 44% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 16.4% between 2025 and 2032.

The global Dual-ion Batteries Market shows strong regional differentiation, with Asia-Pacific leading due to large-scale manufacturing capacity in China and Japan, producing over 38 GWh annually. Europe follows with a 27% share, driven by sustainability regulations and the electric vehicle revolution. North America holds around 19%, supported by strong R&D funding and grid modernization projects. Meanwhile, South America and the Middle East & Africa collectively represent approximately 10% of global consumption, supported by renewable energy deployment and expanding infrastructure investments. Regional adoption trends reflect consumer preferences, government incentives, and the push for net-zero energy transitions across major economies.

North America holds nearly 19% of the Dual-ion Batteries Market, driven by robust industrial adoption across automotive, aerospace, and renewable energy sectors. The U.S. leads the region, supported by federal initiatives promoting clean energy manufacturing and recycling infrastructure. The region is witnessing technological modernization through AI-driven production and digital monitoring systems, improving battery efficiency by 21%. Major industry players are investing in high-voltage dual-ion R&D facilities, such as new graphite-anode plants commissioned in 2024. Consumer adoption is strongest among enterprises in healthcare and finance, emphasizing energy efficiency and reliability in operational continuity. A notable regional player recently announced the deployment of 10 MWh dual-ion storage units in Texas to support microgrid resilience and sustainable energy transitions.

Europe captures approximately 27% of the Dual-ion Batteries Market, led by Germany, France, and the UK, where stringent emission standards and green energy directives drive innovation. The region emphasizes compliance with circular economy initiatives, encouraging recyclability improvements of up to 30% by 2030. European manufacturers are increasingly adopting dual-ion and hybrid battery systems for electric mobility and smart grid applications. Local players are expanding R&D collaborations focused on carbon-neutral electrode materials and energy storage optimization. Consumer adoption patterns in Europe are influenced by transparency and traceability, with enterprises prioritizing eco-compliant energy technologies. A German battery consortium announced in 2024 that dual-ion battery integration reduced industrial energy losses by 18%, highlighting the region’s strong alignment with sustainable production objectives.

Asia-Pacific dominates the Dual-ion Batteries Market, accounting for 44% of total global consumption in 2024. China, Japan, and South Korea represent the largest contributors, collectively producing over 38 GWh annually. The region’s leadership stems from advanced manufacturing ecosystems and government-backed investments in next-generation energy storage materials. Rapid urbanization, e-mobility expansion, and grid infrastructure upgrades further reinforce its market strength. Technological innovation hubs in Japan and South Korea focus on solid-state dual-ion integration and high-voltage cathode optimization, improving charge efficiency by 24%. A leading Chinese manufacturer introduced a mass-produced dual-graphite model with 20% longer cycle life in 2024. Consumer behavior trends show rapid adoption of dual-ion systems in both electric vehicles and consumer electronics, supported by affordable pricing and technology-driven energy solutions.

South America holds around 6% of the Dual-ion Batteries Market, with Brazil and Argentina emerging as key contributors. Government policies promoting clean energy generation and electric mobility are accelerating battery adoption across industrial and residential applications. Infrastructure projects in solar and wind power have spurred a 17% annual increase in regional energy storage demand. The region’s manufacturing sector is gradually incorporating dual-ion systems for efficient grid management and backup power. A Brazilian energy company announced a 5 MWh dual-ion installation project in 2024, enhancing operational stability by 14%. Consumer adoption trends reflect a growing preference for low-maintenance, durable batteries in commercial facilities, with rising enterprise participation in sustainability-oriented programs.

The Middle East & Africa account for about 4% of the Dual-ion Batteries Market, with the UAE, Saudi Arabia, and South Africa being the most active markets. The region’s diversification into renewable energy, particularly solar power, is propelling demand for durable and heat-resistant battery technologies. Strategic trade agreements and public-private energy projects are facilitating technology transfer and innovation. Local industries are integrating dual-ion systems in oil, gas, and construction sectors, supporting decarbonization goals and grid reliability. A pilot initiative launched in the UAE in 2024 demonstrated a 19% energy efficiency gain through hybrid battery deployment. Consumer adoption reflects a gradual transition toward sustainable energy, with commercial users emphasizing low-emission operations and long-term cost efficiency.

• China (32%) – Leads the Dual-ion Batteries Market due to extensive production capacity, state-supported R&D, and advanced battery material innovation.

• Germany (18%) – Holds a strong position driven by electric mobility programs, energy transition policies, and cutting-edge manufacturing capabilities focused on sustainability.

The competitive environment in the Dual-ion Batteries market is moderately consolidated, with the combined share of the top 5 companies estimated at approximately 48% of total market volume. There are more than 60 active competitors globally, including major battery manufacturers, specialized material innovators, and emerging start-ups. Leading players are adopting strategic initiatives such as joint ventures, acquisitions of niche technology providers, and launches of high-performance dual-ion cells. Several firms have introduced modules achieving energy densities exceeding 300 Wh/kg and faster charge cycles. Innovation trends include high-voltage electrolyte formulations, recyclable electrode systems, and digital performance analytics models integrated into “battery-as-a-service” frameworks.

Market positioning reflects a blend of vertical integration by large incumbents and niche specialization by start-ups focusing on sustainability and cost efficiency. Barriers such as material sourcing constraints, R&D costs, and regulatory compliance continue to influence market entry. The fragmented segment of smaller firms accounts for around 52% of market activity, presenting opportunities for strategic consolidation and M&A synergies. Decision-makers should closely track technology licensing, cell chemistry advancements, and cross-industry partnerships as key factors shaping competition.

LG Chem Ltd.

Sion Power Corporation

Custom Cells Itzehoe GmbH

EVE Energy Co., Ltd.

Ionic Materials Inc.

Faradion Limited

Jenax Inc.

Technological innovation in the Dual-ion Batteries market is accelerating, driven by rapid advances in electrode chemistry, electrolyte optimization, and scalable manufacturing processes. Dual-ion batteries, unlike traditional lithium-ion systems, utilize both cations and anions for charge storage, enabling higher voltage outputs of up to 5.2 V and energy densities exceeding 300 Wh/kg. Current research and commercialization efforts are focused on graphite-based cathodes and aluminum or lithium metal anodes, improving energy efficiency by nearly 20–25% compared to conventional lithium-ion designs.

Emerging technologies are also enhancing safety and lifecycle performance. Solid-state and hybrid liquid electrolytes have demonstrated over 1,000 charge cycles with less than 10% capacity degradation, marking a critical step toward commercial scalability. AI-based predictive modeling is being increasingly integrated into production lines, optimizing electrode formulations and reducing defect rates by up to 30%. Additionally, advanced coatings such as fluorinated carbon and boron-nitride layers have reduced electrolyte decomposition by 15–18%, improving overall cell stability.

On the manufacturing front, dry-electrode processing and roll-to-roll fabrication technologies are reducing production costs by approximately 12–15%, enhancing throughput for large-scale deployment. Firms are also pursuing closed-loop recycling initiatives, recovering over 85% of graphite and aluminum materials for reuse. These advancements position dual-ion batteries as a high-efficiency, sustainable alternative, ready to reshape future energy storage landscapes across automotive, grid, and consumer electronics sectors.

In early 2023, Envision AESC completed the construction of a new factory in Wuxi, China capable of producing up to 1 million dual-ion battery units per year, signalling a strong scale-up of production infrastructure dedicated to dual-ion technologies.

In 2023, LG Chem announced a new dual-ion battery featuring a sulfur-based cathode, offering higher energy density and extended cycle life compared to conventional dual-ion cells, advancing the technological performance frontier for the segment.

In April 2024, WeLion supplied its 150 kWh semi-solid-state battery packs—featuring an energy density of 360 Wh/kg—to commercial battery-swap stations, marking one of the first large-scale implementations of a dual-ion-relevant semi-solid system in operational use.

During 2024, a Chinese consortium led by Power China brought a 200 MWh grid-connected energy storage installation online, utilising dual-ion cell modules that achieved a 16% improvement in utilization efficiency compared with prior lithium-ion installations, underscoring dual-ion viability in stationary storage.

This report offers a comprehensive examination of the Dual-ion Batteries Market covering a full spectrum of technologies, applications, end-users, regional footprints and strategic imperatives. It delineates product-type segmentation—including graphite-graphite, sodium-ion, metal-organic dual-ion cells, aluminium-ion dual-ion variants and emerging hybrids—highlighting characteristics such as electrode composition, electrolyte innovations and manufacturing processes. Application segmentation spans electric vehicles, grid-scale renewable energy storage, consumer electronics, portable devices and industrial backup systems, with quantification of adoption rates, demand drivers and performance thresholds. End-user analysis focuses on automotive OEMs, utility operators, consumer device makers and industrial integrators, with behavioural insights such as enterprise preference for rapid-charge dual-ion systems or recyclability-enhanced modules. Geography is mapped across North America, Europe, Asia-Pacific, South America and Middle East & Africa, with country-level manufacture, consumption, investment and regulatory drivers addressed. Technology focus areas include high-voltage dual-ion chemistries, semi-solid/solid-state dual-ion cells, advanced recycling and closed-loop manufacturing, as well as digital battery-management and performance-analytics systems. The report also covers niche market segments such as dual-ion micro-grid storage units for telecom towers, dual-ion packs for aerospace UAVs and dual-ion modules for smart-wearables. Strategic discussions address supply-chain resilience, sustainability mandates (material sourcing, end-of-life recycling), and competitive positioning. The scope is designed for decision-makers, investors and industry professionals seeking actionable intelligence on development trajectories, investment opportunities and technology benchmarks in the dual-ion battery domain.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 400.96 Million |

Market Revenue in 2032 | USD 1305.5 Million |

CAGR (2025 - 2032) | 15.9% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | BYD Company Limited, CATL (Contemporary Amperex Technology Co., Limited), Panasonic Corporation, LG Chem Ltd., Sion Power Corporation, Custom Cells Itzehoe GmbH, EVE Energy Co., Ltd., Ionic Materials Inc., Faradion Limited, Jenax Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |