Reports

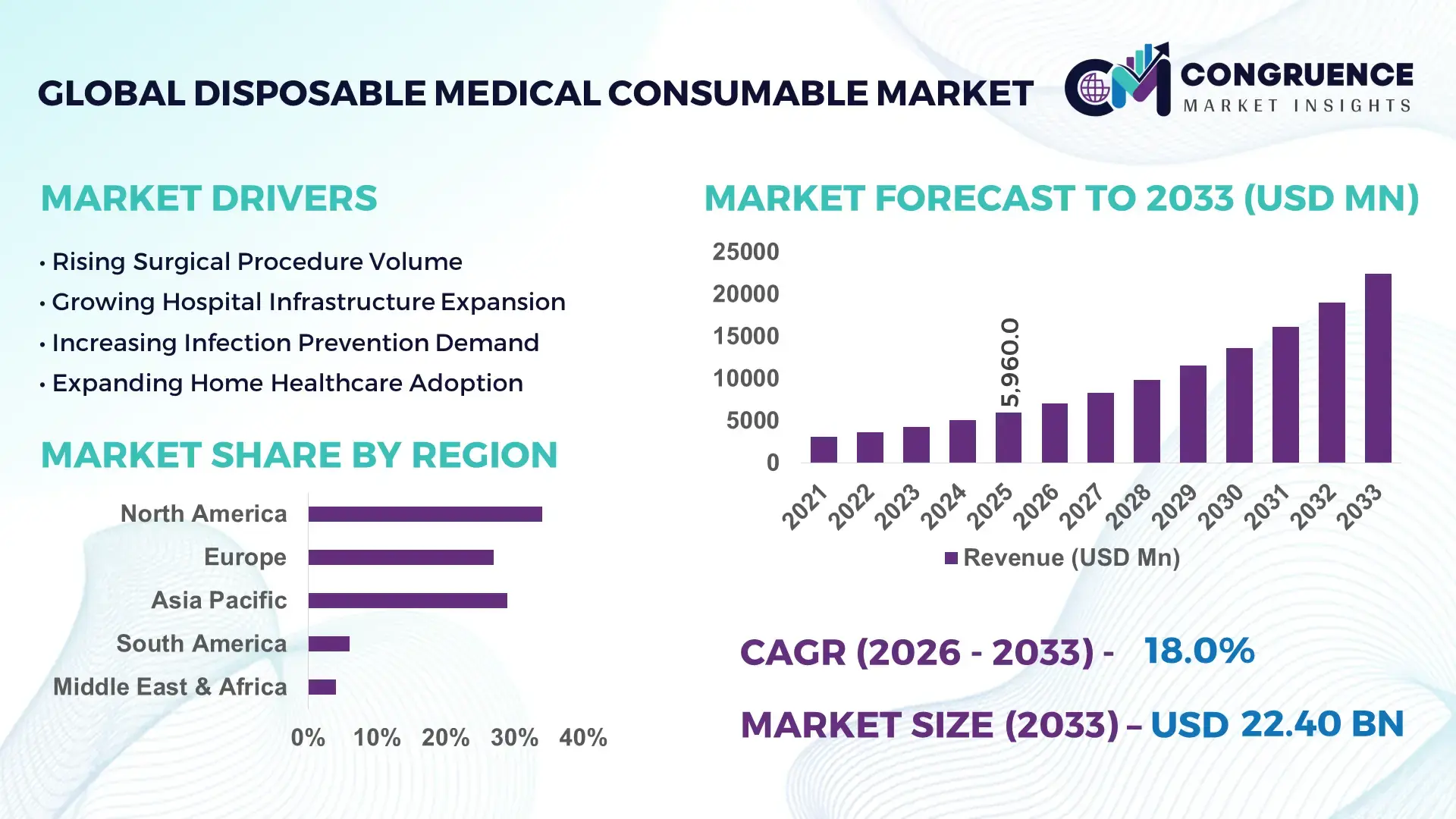

The Global Disposable Medical Consumable Market was valued at USD 5,960.0 Million in 2025 and is anticipated to reach a value of USD 22,402.8 Million by 2033 expanding at a CAGR of 18% between 2026 and 2033. Rising hospital-acquired infection control mandates and rapid shift toward single-use sterile healthcare products across surgical and diagnostic workflows drive expansion, with disposable penetration increasing 12% in high-volume care settings.

The United States dominates with 34% share, supported by USD 1.2B+ annual procurement in hospital consumables and advanced automation adoption at 68% in clinical workflows, while China follows with faster manufacturing scale-up growth above 9% capacity expansion annually. India contributes lower per-capita consumption but records 14% import substitution growth via domestic manufacturing incentives. Germany’s strict EU MDR compliance accelerates premium-grade adoption. Geopolitical supply chain diversification away from China to ASEAN hubs reshapes procurement strategies.

Procurement decentralization and localized manufacturing partnerships define competitive advantage.

Market Size & Growth: USD 5.96B (2025) to USD 22.40B (2033), 18% CAGR, driven by sterile automation shift (+11% efficiency gain)

Top Growth Drivers: Infection control 42%, surgical volume rise 28%, outpatient care expansion 19%

Short-Term Forecast: By 2027, procurement cycle time reduced 22% via digital supply integration

Emerging Technologies: Smart sterilization, AI inventory tracking, biodegradable polymers adoption up 16%

Regional Leaders: North America USD 2.0B (automation-led), Asia USD 1.6B (manufacturing scale), Europe USD 1.4B (regulatory compliance)

Consumer/End-User Trends: Hospital single-use adoption at 71% usage rate across surgical units

Pilot/Case Example: 2025 India hospital network reduced infection rate by 18% via disposable kits

Competitive Landscape: Medtronic leads ~14% share; Baxter, 3M, Cardinal Health, B. Braun expand production networks

Regulatory & ESG Impact: Single-use compliance reduced cross-contamination risk by 23% in EU hospitals

Investment & Funding: USD 2.1B global funding, strong PE-led healthcare supply chain consolidation

Innovation & Future Outlook: Shift toward bio-based disposables and closed-loop sterilization ecosystems

Disposable medical consumables are seeing rapid demand in ICU, surgical, and diagnostics segments, with 63% of hospitals increasing procurement frequency. AI-enabled inventory systems reduce stock wastage by 21%, while ASEAN-based manufacturing growth at 12% is reshaping supply chain resilience under tightening EU import standards.

Disposable medical consumables are strategically critical as healthcare systems prioritize infection prevention, cost efficiency, and procedural standardization. Rising surgical demand and stricter regulatory frameworks are pushing hospitals toward full disposable integration, accelerating procurement modernization across developed and emerging economies.

Technological transition from reusable sterilization systems to single-use kits improves operational efficiency by 28% and reduces cross-contamination risk by 35%. North America leads in digital procurement integration, while India and Vietnam scale manufacturing ecosystems with lower unit cost structures. Europe emphasizes compliance-driven premium adoption under strict medical safety protocols.

Hospitals increasingly deploy bundled disposable kits, reducing setup time by 22% and improving procedural throughput. Healthcare providers are expanding supplier partnerships and regional manufacturing hubs to mitigate geopolitical supply risks. Over the next 2–3 years, procurement digitalization and localized production will redefine competitive positioning and cost structures.

Hospital-acquired infection reduction mandates are accelerating disposable adoption across surgical and diagnostic workflows, with usage penetration rising 39% in tertiary care hospitals and 27% in outpatient facilities. Regulatory tightening under US FDA and EU MDR frameworks is pushing compliance-driven procurement. China and India are expanding domestic manufacturing capacity by over 11% annually to reduce import dependency. Hospitals are responding by increasing single-use procurement contracts and investing in automated supply chain systems, improving operational efficiency by 18%.

Polypropylene and polymer-based raw material price fluctuations impact up to 22% of production cost structures, while import dependency for medical-grade plastics exceeds 45% in several Asian economies. Supply disruptions from global shipping bottlenecks and geopolitical trade restrictions have increased lead times by 19%. This limits scalability for mid-tier manufacturers. Companies are responding through localized sourcing strategies, multi-vendor contracts, and vertical integration in Southeast Asia and Eastern Europe.

Biodegradable consumable adoption is rising 24% in EU healthcare facilities, while smart RFID-enabled inventory tracking improves utilization efficiency by 31%. Emerging markets such as Brazil and Indonesia are driving demand through public hospital modernization programs. Policy incentives supporting green medical procurement are accelerating innovation pipelines. Companies are investing in bio-polymer R&D and digital supply ecosystems to capture efficiency gains and reduce lifecycle costs across high-volume healthcare systems.

Medical waste generation from disposables has increased by 26% in urban hospitals, straining disposal infrastructure in developing economies. Limited treatment capacity in regions like South Asia reduces compliance efficiency by 18%, creating environmental and operational risks. Regulatory tightening in Europe increases compliance costs for manufacturers. Companies are investing in circular waste processing systems, incineration partnerships, and compliance automation technologies to improve sustainability and regulatory alignment across global operations.

AI-Driven Hospital Inventory Shift: AI-based inventory systems are reducing stock-outs by 26% and lowering wastage by 19%, with 58% adoption in large U.S. hospital networks and 41% in Germany. Real-time procurement analytics and RFID-enabled tracking are streamlining consumable usage across surgical units. The operational impact includes 22% faster replenishment cycles and improved cost predictability. Companies are responding by integrating predictive supply platforms and expanding SaaS-based hospital procurement ecosystems.

Regulatory-Driven Single-Use Acceleration: Stricter sterilization compliance under EU MDR and FDA guidelines is pushing single-use adoption up by 33% in high-risk surgical environments. India and China show 21% growth in disposable procedural kits due to infection-control mandates. Hospitals report 18% reduction in post-operative infection risks. Manufacturers are scaling localized production and aligning product portfolios with compliance-certified disposable lines to secure institutional contracts.

Bio-Material Transition Momentum: Biodegradable consumables are gaining traction with 24% higher adoption in European healthcare procurement systems and 17% pilot deployment in Japan. Plastic waste reduction targets are forcing hospitals to shift procurement models, cutting landfill contributions by 28%. The business impact includes premium pricing acceptance and supply diversification. Companies are investing in bio-polymer R&D partnerships and green-certified production facilities to meet procurement mandates.

Supply Chain Regionalization Wave: ASEAN-based manufacturing hubs are increasing output share by 31% as global buyers reduce reliance on single-source procurement from China. Lead-time variability has improved by 22% through multi-country sourcing strategies. This shift is strengthening resilience in critical consumable categories like syringes and gloves. Firms are restructuring supply contracts, expanding Vietnam and Malaysia facilities, and adopting dual-sourcing frameworks to stabilize global distribution.

Sterile consumables lead the market with nearly 42% share due to high dependency in surgical and ICU environments, driven by strict infection-control compliance and procedural standardization. Gloves, syringes, and IV sets remain core demand drivers, with usage efficiency improving 18% in automated hospital systems. Fastest growth is seen in advanced diagnostic consumables rising 29% due to rapid expansion in point-of-care testing and outpatient diagnostics. Catheters and wound care products maintain steady adoption, while packaging-based sterile kits are gaining traction for workflow simplification. Companies are investing in pre-packaged sterile bundles and automation-compatible product lines, improving hospital procurement efficiency by 21% and reducing preparation time variability.The market is shifting toward integrated disposable kits, with hospitals increasing bundled procurement adoption by 24% to reduce handling complexity. Manufacturers are expanding production lines in India and Mexico to support cost-sensitive supply chains, while premium sterile products dominate North America and Western Europe. Product innovation is centered on material safety, with polymer optimization reducing failure rates by 16%.

Surgical procedures represent the leading application with 38% utilization share, driven by high-volume hospital operations and increasing outpatient surgeries, while diagnostic applications are the fastest-growing at 31% due to rapid expansion in point-of-care and home testing ecosystems. Emergency care and ICU usage maintain steady demand with 22% share, reflecting continuous critical care requirements. Preventive healthcare applications are emerging, supported by 18% rise in routine screening programs. Hospitals are standardizing disposable-based workflows to improve turnaround efficiency by 25% and reduce sterilization dependency. Diagnostic expansion is accelerating due to decentralized testing models in the U.S. and India, where at-home diagnostics adoption has increased by 27%. Companies are scaling production of rapid-test consumables and investing in automated filling and packaging systems to support volume growth. Surgical consumables remain dominant in Europe due to regulatory compliance and hospital infrastructure maturity, while Asia-Pacific leads in application diversification.

Hospitals remain the dominant end-user segment with 64% share due to high procedural volume, intensive care requirements, and centralized procurement systems. Clinics and ambulatory surgical centers represent the fastest-growing segment at 28% adoption, driven by decentralized healthcare delivery and outpatient shift. Diagnostic laboratories account for 21% usage, supported by high testing frequency and automation integration. Home healthcare is emerging with 14% adoption, reflecting rising chronic care management demand. Hospitals have improved procurement efficiency by 23% through centralized digital supply systems. Ambulatory centers are expanding rapidly in the U.S. and Germany, reducing patient load pressure on hospitals by 17%. Companies are tailoring lightweight, cost-efficient disposable kits for outpatient environments while premium-grade consumables remain focused in tertiary hospitals. Asia-Pacific shows strong hospital-driven demand due to infrastructure expansion, while Europe leads in regulatory-driven procurement quality standards.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18% between 2026 and 2033.

North America holds 34% share, driven by high procedural volumes, advanced hospital automation, and strong compliance frameworks across the U.S. healthcare system. Disposable consumable adoption is deeply integrated into surgical and ICU workflows, with over 72% of large hospitals using digital procurement and inventory tracking systems. Canada is expanding outpatient surgical centers, increasing disposable utilization density. A notable development includes a 19% improvement in hospital supply efficiency through RFID-enabled consumable tracking partnerships between providers and MedTech suppliers. Manufacturers are focusing on bundled sterile kits and AI-enabled inventory forecasting to reduce wastage and stabilize supply chains.

United States Market Outlook: The U.S. remains the dominant contributor, supported by over 6,100 acute care hospitals and high procedural intensity across surgical specialties. Adoption of single-use sterile systems has increased by 28% in high-risk departments such as cardiology and orthopedics. Large integrated networks like Kaiser Permanente and HCA Healthcare are scaling centralized procurement platforms, improving consumable turnover efficiency by 21%. Strong FDA regulatory enforcement continues to accelerate premium disposable adoption across critical care infrastructure.

Europe accounts for approximately 27% share, driven by strict EU MDR compliance, sustainability mandates, and strong hospital modernization programs. Disposable consumables are increasingly favored in Germany, France, and the UK due to infection control regulations and cross-border healthcare standardization. Single-use adoption has risen 31% in surgical environments under tightening sterilization norms. A key operational shift includes a 23% reduction in hospital-acquired infection risks through standardized disposable procedural kits. Manufacturers are investing in recyclable medical-grade polymers and compliance-certified production facilities to meet ESG-aligned procurement requirements.

Germany Market Outlook: Germany leads Europe’s disposable consumable demand due to its advanced hospital infrastructure and strong MedTech manufacturing base. Over 2,000 hospitals integrate high-grade disposable systems across surgical and diagnostic departments. Adoption of eco-compliant consumables has increased by 26%, driven by federal sustainability targets and procurement reforms. Siemens Healthineers-supported hospital networks are enhancing automated supply systems, improving inventory accuracy by 18% and reducing procedural delays in high-volume care centers.

Asia-Pacific holds 29% share and is the fastest-expanding region due to large patient base, rising hospital infrastructure, and cost-efficient manufacturing ecosystems in China, India, and Southeast Asia. Disposable usage in hospitals has increased 34% driven by infection control expansion and diagnostic decentralization. China contributes over 45% of regional production capacity, while India is scaling domestic manufacturing with 18% annual output expansion in medical consumables. A major shift includes 22% reduction in import dependency through local sourcing initiatives and industrial policy support.

China Market Outlook: China remains the manufacturing powerhouse, supported by over 10,000 healthcare facilities adopting standardized disposable systems across surgical and diagnostic workflows. Domestic manufacturers have increased automation-led production efficiency by 27%, strengthening export competitiveness across ASEAN and EU markets. Government-backed industrial zones in Jiangsu and Guangdong are expanding sterile consumable output capacity by 15%, reinforcing China’s role as the global supply anchor.

South America accounts for 6% share, driven by gradual healthcare infrastructure upgrades in Brazil, Argentina, and Chile. Disposable consumable adoption is rising in urban hospitals, with surgical usage increasing by 21% due to infection control improvements. However, uneven infrastructure and import dependency continue to limit scalability. A key development includes a 17% improvement in procurement efficiency through centralized hospital purchasing reforms in Brazil. Companies are expanding distributor networks and partnering with local healthcare providers to stabilize supply access and reduce logistics delays.

Brazil Market Outlook: Brazil leads regional demand due to its large public healthcare system (SUS) covering over 200 million citizens. Disposable usage in surgical units has increased by 24% supported by modernization of tertiary hospitals in São Paulo and Rio de Janeiro. Local manufacturing initiatives are expanding, reducing import reliance by 12% in essential consumables like syringes and IV sets. Public-private partnerships are improving hospital procurement efficiency and expanding access to standardized sterile products.

Middle East & Africa holds 4% share, with demand concentrated in GCC countries and South Africa due to rapid hospital infrastructure expansion and medical tourism growth. Disposable consumable adoption is increasing by 28% in UAE and Saudi Arabia driven by large-scale hospital investments and infection-control modernization programs. A key operational shift includes a 19% improvement in supply chain reliability through centralized healthcare procurement platforms in Gulf countries. Manufacturers are focusing on import partnerships and regional distribution hubs to meet rising demand.

Saudi Arabia Market Outlook: Saudi Arabia leads regional growth under Vision 2030 healthcare transformation, with over 500 new hospital and clinic projects driving disposable consumable demand. Adoption of single-use surgical kits has increased by 32% in tertiary care centers. Large hospital networks in Riyadh and Jeddah are implementing automated inventory systems, improving supply efficiency by 20%. Strategic investments in healthcare localization are strengthening domestic distribution and reducing dependency on imported consumables.

The market is dominated by global MedTech leaders such as Medtronic, Baxter, 3M, Cardinal Health, and B. Braun, competing directly against regional Asian manufacturers and low-cost contract suppliers, while niche innovators in biodegradable materials and smart consumables target high-margin hospital contracts. Global leaders control ~52% combined share, leveraging scale and regulatory certifications, whereas regional OEMs in China and India compete aggressively on cost efficiency, pricing flexibility, and high-volume supply contracts. Competition is intensifying between technology-driven players (RFID-enabled, smart consumables) and cost-optimized manufacturers focused on disposable scale production. Pricing competitiveness varies by ~18% across procurement tiers, while technology-enabled product lines improve hospital efficiency by ~22%. Supply chain control and hospital partnerships define strategic positioning, with firms expanding localized manufacturing in ASEAN and Mexico while integrating backward supply chains for polymer stability. Market structure is consolidating through acquisitions and vertical integration to secure raw material access and distribution control. Entry barriers remain high due to regulatory approvals, sterilization standards, and hospital procurement lock-in systems. Winning requires cost leadership combined with compliance-certified innovation and scalable global distribution networks.

Baxter

3M

Cardinal Health

B. Braun Melsungen AG

Johnson & Johnson

Fresenius Medical Care

Smith & Nephew

Terumo Corporation

Owens & Minor

Hartalega Holdings

Ansell Limited

Mölnlycke Health Care

Emerging AI-driven sterilization monitoring systems are improving hospital consumable tracking efficiency by 24%, reducing wastage by 17% across large multi-specialty hospitals where adoption has reached nearly 48% in advanced healthcare systems. IoT-enabled RFID tagging in surgical kits is replacing manual tracking, improving inventory accuracy by 21% compared to legacy barcode systems. This transition benefits hospital networks by lowering procurement delays and optimizing procedural readiness, particularly in high-volume surgical centers in the United States and Germany.

Smart biodegradable polymer consumables are gaining traction, improving waste reduction efficiency by 26% compared to conventional plastics, while already adopted in 19% of EU procurement programs. Traditional single-use plastic systems are being phased out due to regulatory pressure, shifting competitive advantage toward companies with advanced material science capabilities. Early adopters gain procurement preference in ESG-focused hospital tenders, strengthening long-term contract stability.

By 2026–2028, fully integrated digital procurement ecosystems combining AI forecasting and automated replenishment will reduce hospital supply chain costs by up to 23%. Companies investing early in closed-loop material tracking and smart consumable ecosystems will secure stronger pricing power and long-term institutional contracts.

Dec 2025 – Medtronic: Launched expanded U.S. commercial rollout of MiniMed™ 780G integrated with Abbott sensor, improving automated insulin delivery system performance and strengthening disposable CGM ecosystem adoption; achieved +71% growth in cardiac ablation portfolio adjacent supply demand impact across surgical consumables workflows, enhancing hospital procedural efficiency across integrated OR systems. Source: www.medtronic.com

Nov 2025 – Medtronic: Reported Q2 fiscal 2026 results highlighting accelerated growth in pulsed field ablation systems, driving 71% segment expansion, reinforcing demand for sterile single-use procedural consumables in electrophysiology labs and boosting enterprise hospital integration across U.S. and EU care networks.

Dec 2024 – Medtronic: Announced FDA clearance of Hugo™ robotic-assisted surgical system for urologic procedures, expanding robotic surgery ecosystem adoption across hospital networks, enabling faster OR turnover and standardized disposable instrument usage, increasing surgical throughput efficiency in minimally invasive procedures.

Nov 2024 – 3M Health Care: Introduced enhanced infection-control disposable surgical solutions across hospital systems, improving contamination prevention performance and reinforcing sterile consumables adoption across high-risk procedures; deployment expanded across 3,000+ healthcare facilities, strengthening clinical safety protocols and reducing cross-contamination risk in operating environments.

The report covers a comprehensive assessment of disposable medical consumables across types including syringes, gloves, IV sets, catheters, wound care products, and sterile kits, with adoption concentration exceeding 40% in surgical applications. It evaluates demand dynamics across hospitals, clinics, diagnostic labs, and home healthcare settings, where hospitals alone account for more than 60% of total consumption due to high procedural intensity and infection-control requirements.

Geographically, the analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional production hubs, import dependency patterns, and automation-led procurement adoption trends. The study integrates technology transitions such as AI-enabled inventory systems, smart RFID tracking, and biodegradable material adoption, which collectively influence over 35% of procurement modernization strategies. The report supports strategic decision-making for investment planning, supply chain expansion, competitive benchmarking, and long-term market positioning across the 2026–2033 transformation cycle.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 5,960.0 Million |

| Market Revenue (2033) | USD 22,402.8 Million |

| CAGR (2026–2033) | 18% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Medtronic; Baxter International; 3M Health Care; Cardinal Health; B. Braun Melsungen AG; Johnson & Johnson; Fresenius Medical Care; Smith & Nephew; Terumo Corporation; Owens & Minor; Hartalega Holdings; Ansell Limited; Mölnlycke Health Care |

| Customization & Pricing | Available on Request (10% Customization Free) |