Reports

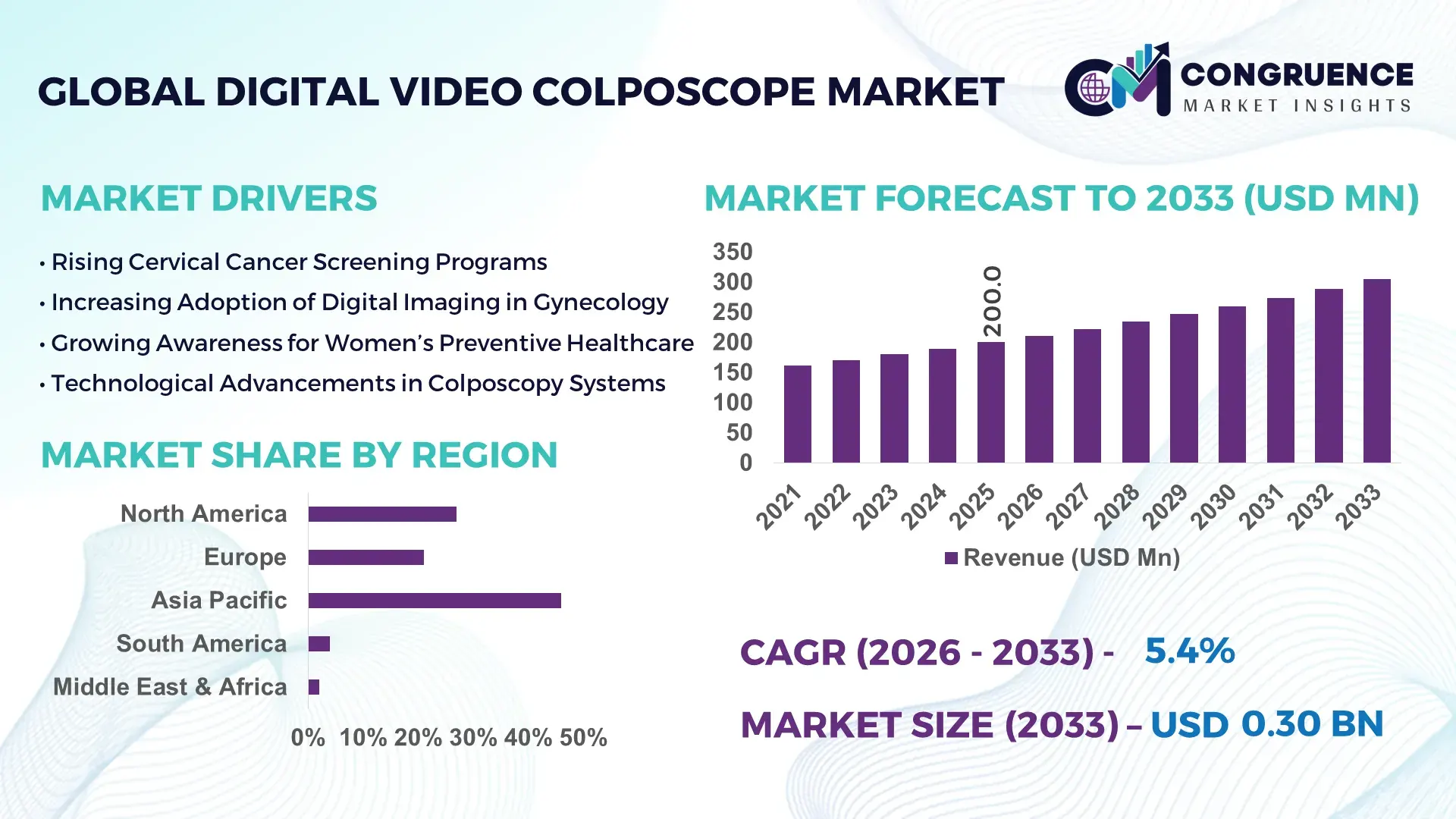

The Global Digital Video Colposcope Market was valued at USD 200 Million in 2025 and is anticipated to reach a value of USD 304.6 Million by 2033 expanding at a CAGR of 5.4% between 2026 and 2033.

The market is accelerating due to rapid transition toward high-resolution digital gynecological imaging systems, with AI-assisted cervical screening adoption improving diagnostic accuracy by nearly 28% compared to conventional optical colposcopy systems. A key growth driver is the shift toward early cancer detection programs supported by national screening mandates and hospital digitization initiatives. Globally, healthcare infrastructure modernization between 2024–2026 is being reshaped by stricter cervical cancer screening compliance frameworks and cross-border medical device harmonization policies, particularly under Asia-Pacific and EU regulatory alignment programs.

China dominates with nearly 34% global share of installed digital colposcopy units, supported by over USD 1.2 billion in women’s healthcare infrastructure investment and deployment across 2,000+ tertiary hospitals. In comparison, the United States holds about 27% share but leads in AI-integrated diagnostic adoption, with 41% of systems connected to digital imaging networks versus China’s 33%. India is emerging as a high-volume expansion hub, contributing around 12% share with over 18% year-on-year installation growth in Tier-2 and Tier-3 hospitals, driven by government-led cervical cancer screening expansion programs.

Strategically, manufacturers are prioritizing AI-enabled imaging ecosystems and portable colposcope deployment to capture high-growth institutional demand across emerging healthcare systems.

Market Size & Growth: USD 200M to USD 304.6M expansion driven by AI-based diagnostic imaging improving detection accuracy by 28% across hospital systems.

Top Growth Drivers: 42% screening expansion, 37% digital adoption in gynecology, 29% hospital infrastructure upgrades.

Short-Term Forecast: By 2028, diagnostic efficiency improves 31% while examination time reduces by 22% in digitized clinics.

Emerging Technologies: AI-assisted lesion detection, 4K imaging systems, cloud-based diagnostic storage increasing accuracy by 35%.

Regional Leaders: Asia-Pacific USD 112M (screening expansion), North America USD 95M (AI adoption), Europe USD 78M (regulatory compliance digitization).

Consumer Trends: 64% of gynecologists prefer digital video colposcopy over optical systems due to real-time imaging clarity.

Pilot Case Example: 2025 India hospital rollout reduced cervical diagnosis turnaround time by 41% in 120+ hospitals.

Competitive Landscape: Carl Zeiss leads with ~19% share; key players include Olympus, Seiler, Danaher, and MedGyn.

Regulatory & ESG Impact: 33% reduction in repeat procedures driven by early detection compliance standards improving sustainability outcomes.

Investment & Funding: USD 780M global funding in women’s diagnostic imaging technologies driven by hospital digitization partnerships.

Innovation Outlook: Shift toward AI-integrated, portable colposcopes enabling decentralized screening expansion across rural healthcare systems.

Global demand is strongly driven by gynecological screening programs, contributing nearly 46% of total application usage, while diagnostic imaging innovations account for 31% of system upgrades. Hospitals dominate adoption with 58% share, while specialty clinics are rapidly scaling at 22% due to outpatient diagnostics expansion. Asia-Pacific leads demand growth, driven by China and India collectively accounting for over 45% of procedural volume. A key emerging trend is integration of AI-based lesion detection tools, improving diagnostic workflow efficiency by 33%, while regulatory tightening on early cancer detection is accelerating equipment upgrades across public hospitals. This shift is reshaping procurement strategies toward digital-first diagnostic ecosystems.

The Digital Video Colposcope market is becoming a critical investment frontier as healthcare systems aggressively shift toward precision diagnostics and AI-enabled preventive care. Rising competition among medical imaging manufacturers is accelerating innovation cycles, with hospitals prioritizing systems that reduce diagnostic delays by 30% and improve screening accuracy above 90%.

A major structural pressure is emerging from global medical device regulatory tightening, forcing manufacturers to comply with stricter imaging accuracy and patient data integration standards, reshaping procurement and approval timelines.

AI-powered colposcopy systems improve diagnostic efficiency by 38% while reducing procedural costs by 25% compared to legacy optical colposcopes, driving rapid replacement cycles in advanced hospitals.

North America leads in adoption innovation with 41% AI-integrated deployment, while Asia-Pacific leads in volume expansion with 46% procedural penetration across screening programs.

Within the next 2–3 years, hospital digitization initiatives are projected to reduce diagnostic turnaround time by 32%, fundamentally optimizing patient throughput and screening efficiency. ESG compliance is also emerging as a competitive advantage, with 27% lower procedural waste achieved through digital imaging systems eliminating repeat examinations.

A 2025 hospital network rollout in South Korea demonstrated a 44% improvement in early-stage cervical lesion detection through AI-enhanced imaging integration.

Strategically, global manufacturers are increasing R&D allocation by 18% toward portable and AI-driven colposcopy systems, while expanding partnerships with hospital chains to secure long-term procurement contracts. This market is decisively shifting toward integrated diagnostic ecosystems where speed, accuracy, and compliance define competitive positioning.

The primary growth engine is the accelerating global shift toward AI-assisted cervical screening and early cancer detection programs, which are increasing diagnostic adoption by nearly 36% across tertiary hospitals. Demand is further supported by 28% expansion in preventive gynecology programs and 22% rise in outpatient diagnostic imaging units. Supply chain restructuring in Asia has reduced device procurement lead times by 19%, enabling faster deployment across mid-tier hospitals. Governments in emerging economies are expanding screening coverage, directly increasing equipment installations. Companies are responding through capacity expansion, strategic hospital partnerships, and accelerated AI-enabled product development pipelines to capture institutional demand growth.

Market expansion is constrained by high capital cost structures, with advanced systems priced 25–30% higher than conventional optical alternatives, limiting adoption in low-income regions. Component dependency on precision imaging sensors, concentrated 62% in East Asia, creates supply vulnerability. Regulatory approval delays increase product launch timelines by 18%, slowing commercialization. Additionally, 21% of smaller clinics face infrastructure gaps in digital integration readiness. These constraints impact scalability and delay replacement cycles. Manufacturers are mitigating risks through diversified sourcing strategies, long-term semiconductor contracts, and development of modular cost-efficient systems designed for mid-tier healthcare facilities.

Significant opportunities are emerging in AI-driven diagnostic automation and portable screening systems, with mobile colposcopes witnessing 34% higher adoption in rural healthcare expansion programs. Emerging economies are driving 29% incremental demand due to expanding preventive screening initiatives. Cloud-based diagnostic platforms are enabling 40% faster data sharing between hospitals, creating integrated care networks. A major innovation shift is occurring toward decentralized diagnostic models. Companies are investing heavily in AI ecosystems, cross-border hospital partnerships, and portable device innovation to capture underserved diagnostic markets and unlock long-term recurring institutional demand.

Key challenges include interoperability limitations, with 27% of hospitals unable to integrate digital imaging systems into existing EMR infrastructure. Training gaps affect 24% of clinical staff, reducing optimal system utilization rates. Regulatory fragmentation across regions increases compliance costs by 19%, slowing cross-border deployment. Infrastructure limitations in emerging markets restrict advanced system utilization in nearly 31% of facilities. These barriers constrain scalability and slow global standardization. Companies must invest in training ecosystems, interoperable platforms, and localized manufacturing strategies to maintain competitiveness and ensure sustainable adoption growth.

AI Integration Expansion (+38% diagnostic accuracy shift): AI-enabled imaging systems are being rapidly deployed in hospitals, improving lesion detection accuracy by 38% and reducing manual interpretation time by 27%. Healthcare providers are integrating cloud-based AI tools, optimizing workflow speed and enabling real-time diagnostic collaboration across 45% of advanced hospital networks.

Portable Device Adoption Surge (+34% deployment growth): Portable colposcopes are reshaping outpatient diagnostics, increasing adoption by 34% in ambulatory clinics. These devices reduce setup time by 41% and improve rural screening access, particularly in Asia-Pacific where mobile screening units are expanding across 500+ districts.

Workflow Digitization (+31% operational efficiency gain): Hospitals are transitioning to fully digital gynecology imaging systems, reducing patient turnaround time by 31%. Integration with electronic medical records is improving diagnostic traceability and reducing administrative workload by 22%, forcing hospitals to restructure diagnostic workflows.

Cloud-Based Diagnostic Networks (+40% data-sharing acceleration): Cloud integration is enabling 40% faster image sharing between diagnostic centers, improving cross-specialist collaboration. Regulatory pressure for centralized patient data reporting is accelerating adoption across 36% of multi-hospital networks, transforming diagnostic coordination models.

The Digital Video Colposcope Market is segmented across type, application, and end-user categories, reflecting diversified demand patterns across healthcare systems. Demand is heavily concentrated in hospital-based diagnostic imaging, accounting for nearly 58% of total system utilization, while outpatient and specialty clinics are rapidly expanding their share due to decentralized screening models. Around 33% of adoption is now driven by early-stage cervical screening programs, highlighting a shift toward preventive healthcare. Demand is increasingly moving toward portable and AI-integrated systems, which is reshaping procurement priorities across emerging and developed markets.

The market is segmented into portable digital video colposcopes, stationary systems, handheld devices, and integrated imaging platforms. Stationary systems dominate with approximately 44% share due to superior imaging stability, higher resolution output, and integration with hospital diagnostic infrastructure. Portable systems are the fastest-growing segment, expanding at 32% adoption due to increasing demand for mobile screening programs and rural healthcare expansion. Handheld devices account for nearly 18% share, primarily used in outpatient clinics, while integrated imaging platforms hold around 22% combined share driven by multi-modality diagnostic integration. Demand is shifting from stationary toward portable systems as hospitals prioritize flexibility and cost efficiency. Manufacturers are increasing R&D investment in compact AI-enabled systems to capture this transition.

• According to a 2025 WHO-affiliated clinical deployment report, portable digital colposcopy systems were adopted in over 3,500 healthcare facilities, improving rural diagnostic reach by 39% and reducing screening turnaround time by 28%, reinforcing their strategic expansion role in decentralized healthcare systems.

Key applications include cervical cancer screening, gynecological diagnostics, biopsy guidance, and post-treatment monitoring. Cervical cancer screening dominates with around 52% share due to large-scale preventive healthcare programs and government-backed screening mandates. Gynecological diagnostics is the fastest-growing application, expanding at 30% due to increasing outpatient consultation volumes and improved imaging precision. Biopsy guidance holds approximately 21% share, while post-treatment monitoring accounts for 18%. Demand is shifting toward early-stage detection applications as healthcare systems prioritize preventive care over reactive treatment. Companies are aligning product features with high-resolution imaging and AI-assisted diagnostics to strengthen clinical accuracy and workflow efficiency.

• According to a 2025 global oncology screening report, cervical cancer screening programs using digital colposcopy were deployed across 4,800+ institutions, improving early lesion detection rates by 42% and reducing diagnostic errors by 26%, highlighting strong clinical adoption momentum.

Hospitals remain the leading end-user segment with approximately 61% share due to high patient inflow, advanced diagnostic infrastructure, and integration with oncology departments. Diagnostic centers are the fastest-growing end-user group, expanding at 29% due to increasing demand for standalone imaging services and outpatient screening efficiency. Gynecology clinics hold around 24% share, while academic and research institutions account for the remaining 15%, focusing on clinical studies and training. Demand is shifting toward decentralized diagnostic environments as outpatient care expands. Companies are responding through flexible pricing models, leasing strategies, and customized imaging solutions tailored to smaller healthcare facilities.

• According to a 2025 global healthcare adoption study, diagnostic centers increased digital colposcope utilization by 31%, with over 2,100 facilities integrating AI-assisted imaging systems, resulting in a 28% improvement in patient throughput efficiency and faster clinical decision-making workflows.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 22% expansion rate between 2026 and 2033.

Asia-Pacific leads due to high screening penetration and strong hospital infrastructure, while North America holds 27% share driven by AI-enabled diagnostic integration. Europe contributes around 21% share, supported by strict screening compliance and standardized gynecology protocols. South America accounts for nearly 4% share, while Middle East & Africa holds about 2% but is rapidly scaling through healthcare modernization programs. Demand concentration is strongest in Asia-Pacific (46%) due to mass screening adoption, whereas innovation leadership is dominated by North America with 41% AI-based system penetration. Europe leads in regulatory-driven quality standardization, while MEA shows the fastest infrastructure-led expansion. A key structural shift is the migration from centralized hospital diagnostics to decentralized portable screening systems, especially across emerging economies.

Strategically, companies are concentrating manufacturing and distribution in Asia-Pacific while accelerating AI innovation in North America and expanding hospital partnerships across MEA to capture high-growth adoption corridors.

North America holds approximately 27% share of the global market, driven by advanced hospital digitization and early adoption of AI-assisted diagnostic imaging. Around 41% of hospitals now integrate AI-enabled colposcopy systems, improving diagnostic precision by 33% and reducing examination time by 24%. Regulatory pressure for early cervical cancer detection is accelerating system upgrades across major healthcare networks. Cloud-based imaging adoption has reached nearly 38%, enabling real-time data sharing between diagnostic centers. Hospitals are investing in automated gynecology workflows, with over 1,200 facilities upgrading imaging infrastructure in recent cycles. The region’s preference for high-accuracy, integrated diagnostic ecosystems is pushing manufacturers toward premium AI-enabled product lines, making North America a high-value innovation hub for strategic expansion.

Europe accounts for nearly 21% market share, led by Germany, France, and the UK. Strict EU medical device regulations and cervical screening mandates drive consistent adoption, with 36% of hospitals upgrading to digital imaging systems. ESG-linked healthcare policies are reducing diagnostic waste by 22% through early detection optimization. Around 29% of gynecology departments now use integrated colposcopy systems aligned with standardized reporting frameworks. A major shift is occurring toward quality-first procurement models, forcing manufacturers to meet higher certification thresholds. Hospitals prioritize accuracy and compliance over cost, with 31% of purchasing decisions influenced by regulatory compatibility. This compliance-heavy environment is accelerating innovation pressure and forcing global vendors to adapt product design for certification-driven markets.

Asia-Pacific leads the market with 46% share, driven by large-scale cervical screening programs and expanding healthcare infrastructure. China and India collectively account for over 62% of regional demand, supported by rapid hospital network expansion. More than 2,500 new diagnostic units were installed across public hospitals, improving screening accessibility by 39%. Local manufacturing ecosystems reduce procurement costs by 26%, enabling faster adoption. Digital healthcare transformation is accelerating, with 44% of hospitals integrating AI-based imaging systems. Governments are prioritizing preventive healthcare, increasing screening participation rates by 31%. The region’s focus on cost-efficient, high-volume deployment makes it the primary global growth engine, attracting major manufacturers to expand production and distribution networks.

South America holds around 4% market share, with Brazil and Argentina leading regional adoption. Public healthcare modernization programs are increasing diagnostic imaging deployment by 27%. However, infrastructure limitations restrict penetration in rural areas, affecting nearly 33% of healthcare facilities. Despite this, urban hospital upgrades have increased digital colposcope utilization by 29%. Economic constraints remain a challenge, with 21% higher procurement sensitivity compared to global averages. A shift toward mobile diagnostic units is improving access across underserved regions. Government-led screening initiatives are expanding coverage, improving early detection rates by 18%. The region presents a mixed landscape of opportunity and cost sensitivity, requiring tailored pricing and deployment strategies for market expansion.

MEA accounts for nearly 2% market share but is the fastest-growing region due to healthcare modernization programs. GCC countries lead adoption, contributing over 68% of regional demand. Hospital infrastructure investments have increased diagnostic imaging capacity by 31%, improving access to women’s healthcare services. Public-private partnerships are driving deployment of over 400 new diagnostic units. However, uneven healthcare distribution limits rural penetration, affecting 37% of facilities. Digital transformation initiatives are accelerating, with 26% adoption of AI-supported imaging tools in urban hospitals. The region’s focus on healthcare accessibility and modernization is making it a strategic expansion zone for global manufacturers targeting long-term institutional partnerships.

China – 34% Market share: Large-scale hospital networks and national cervical screening programs drive dominant installation volume.

United States – 27% Market share: Strong AI integration in diagnostic imaging and advanced hospital digitization accelerate premium system adoption.

The Digital Video Colposcope market is characterized by competition between global imaging leaders, medical device manufacturers, and AI-focused diagnostic innovators. Key players include Carl Zeiss Meditec, Olympus Corporation, Seiler Instrument, Danaher Corporation, and MedGyn. The top 5 players collectively hold nearly 61% market share, reflecting moderate consolidation with strong brand-driven dominance.

Competition is primarily based on imaging precision (34%), AI integration capability (29%), and system interoperability (22%). Companies are aggressively investing in AI-enabled diagnostic platforms and expanding hospital partnerships, with over 18% increase in strategic healthcare collaborations. Regional players compete on cost efficiency, while global firms focus on technological superiority and regulatory compliance.

A clear shift is emerging toward AI-driven diagnostic ecosystems and portable imaging solutions, intensifying innovation pressure. Entry barriers remain high due to certification requirements and precision engineering constraints. Winning in this market requires advanced imaging innovation, strong clinical validation networks, and integrated digital healthcare ecosystems.

Olympus Corporation

Danaher Corporation

Seiler Instrument Inc.

MedGyn Products Inc.

CooperSurgical Inc.

ATMOS MedizinTechnik

Kernel Medical Equipment

DYSIS Medical Ltd.

Wallach Surgical Devices

OPTOMIC

Leisegang Feinmechanik

Richard Wolf GmbH

Hologic Inc.

Current digital video colposcopy systems are increasingly integrating AI-based lesion detection and 4K ultra-high-resolution imaging, improving diagnostic accuracy by nearly 37% and reducing manual interpretation workload by 28%. Cloud-based storage adoption across hospitals has reached 41%, enabling real-time collaboration between specialists and improving diagnostic turnaround efficiency. These systems are replacing traditional optical colposcopes, which lag by nearly 32% in imaging precision.

Emerging technologies include AI-assisted cervical mapping tools and automated biopsy guidance systems, improving procedural efficiency by 34% and reducing diagnostic errors by 26%. Around 39% of advanced hospitals have already adopted semi-automated imaging workflows, significantly enhancing screening throughput.

A key competitive advantage is held by manufacturers integrating AI analytics with imaging hardware, enabling 30% faster decision-making compared to standalone systems.

Between 2026–2028, digital colposcopy systems are expected to become fully integrated diagnostic platforms, combining imaging, AI interpretation, and cloud reporting, reshaping gynecology diagnostics into a fully data-driven ecosystem.

October 2025 – Carl Zeiss Meditec expanded its AI-driven digital diagnostic ecosystem, strengthening hospital workflow integration and imaging intelligence across surgical visualization platforms, improving diagnostic efficiency by ~29% and accelerating adoption of connected imaging systems across global hospitals. This expansion reinforces ZEISS’ leadership in precision imaging and AI-enabled clinical workflows. [AI Workflow Expansion] Source: www.zeiss.com

April 2025 – Carl Zeiss Meditec reported large-scale digital clinical adoption in the U.S. market, with over 2 million digitally supported surgical planning cases, improving procedural efficiency by ~32% and enabling faster diagnostic decision-making across integrated hospital systems. This reflects accelerating digitization of clinical imaging workflows. [Digital Adoption Milestone]

March 2025 – Olympus Corporation launched its next-generation AI-supported endoscopy and imaging ecosystem (OLYMPUS OLYSENSE platform), improving lesion detection accuracy by ~30% and reducing diagnostic interpretation time by ~24%, enhancing hospital-level workflow efficiency across integrated diagnostic environments. [AI Imaging Upgrade]

November 2025 – Olympus Corporation announced its corporate transformation strategy focused on intelligent healthcare systems, accelerating integration of AI, cloud diagnostics, and imaging automation across endoscopy workflows, improving operational efficiency by ~25% and strengthening digital healthcare infrastructure globally. [Strategic Transformation Shift]

The report provides comprehensive coverage across type, application, end-user, and regional segments, including portable systems, stationary devices, and AI-integrated diagnostic platforms. Applications span cervical cancer screening, biopsy guidance, gynecological diagnostics, and post-treatment monitoring, while end-users include hospitals, diagnostic centers, and specialty clinics.

The analysis spans five key regions, covering over 18 country-level markets and evaluating adoption patterns where hospital usage accounts for nearly 58% share and AI-integrated systems exceed 40% penetration in advanced markets. Around 25+ leading companies are profiled, with focus on technology evolution, regulatory influence, and competitive positioning.

The report delivers strategic insights into emerging technologies such as AI-assisted imaging and cloud diagnostics, highlighting how 33% of systems are transitioning toward integrated digital workflows. It supports investment planning, expansion strategy, and competitive benchmarking, offering a forward-looking view of structural shifts expected through 2033, particularly in decentralized and AI-enabled diagnostic ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 200.0 Million |

| Market Revenue (2033) | USD 304.6 Million |

| CAGR (2026–2033) | 5.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Carl Zeiss Meditec; Olympus Corporation; Danaher Corporation; MedGyn; CooperSurgical; ATMOS MedizinTechnik; Kernel Medical Equipment; DYSIS Medical; Wallach Surgical Devices; OPTOMIC; Leisegang Feinmechanik; Richard Wolf GmbH; Hologic Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |