Reports

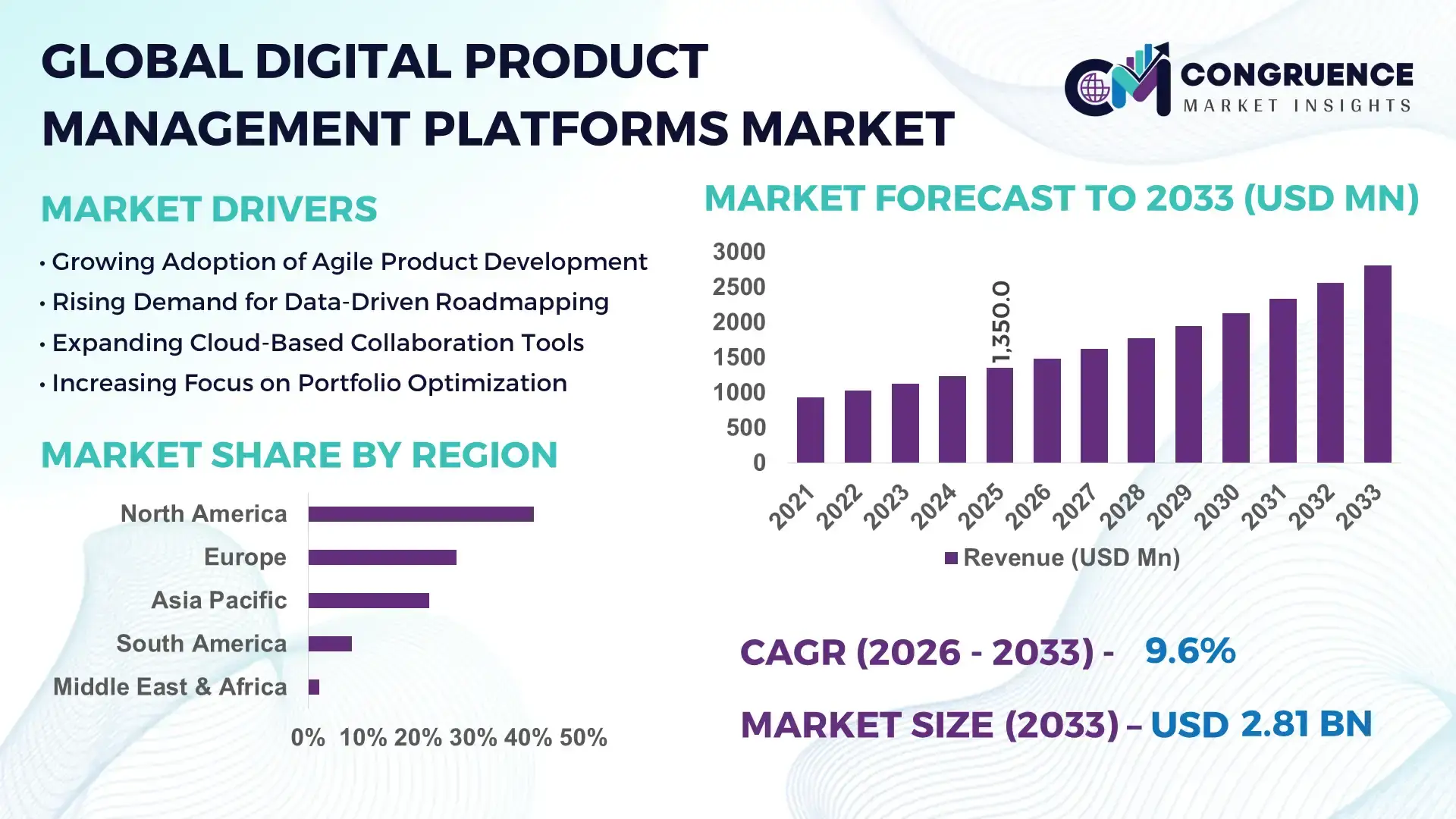

The Global Digital Product Management Platforms Market was valued at USD 1,350.0 Million in 2025 and is anticipated to reach a value of USD 2,810.7 Million by 2033 expanding at a CAGR of 9.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by increasing enterprise investment in integrated digital planning, cross‑functional automation, and enhanced product lifecycle orchestration.

The United States leads the Digital Product Management Platforms Market with extensive deployment capacity and innovation investment. In 2025, over 48% of enterprises in the U.S. had adopted advanced product management platforms, with annual enterprise spending on platform enhancements exceeding USD 2.5 billion. U.S. development hubs in Silicon Valley and Boston continually integrate AI‑assisted roadmapping and automated analytics, resulting in 35% faster release cycles for digital products. Local universities and tech incubators contribute skilled talent pools exceeding 150,000 professionals employed in platform development and digital product strategy annually.

Market Size & Growth: Valued at USD 1,350 M in 2025, projected to reach USD 2,810.7 M by 2033 at a 9.6% CAGR – fueled by rising enterprise adoption and workflow digitization.

Top Growth Drivers: Agile adoption growth at 67%, cross‑team collaboration efficiency up 52%, automation integration increase at 43%.

Short‑Term Forecast: By 2028, product delivery cycle times expected to improve by up to 29% across global enterprises.

Emerging Technologies: AI‑driven prioritization engines, natural language planning assistants, and real‑time analytics platforms.

Regional Leaders: North America projected USD 1,120 M by 2033 with enterprise resilience focus; Europe to reach USD 740 M with compliance automation; Asia‑Pacific USD 610 M with rapid SME uptake.

Consumer/End‑User Trends: Large corporations increasingly require modular, scalable platforms; SMEs favor SaaS models with 24/7 support and mobile access.

Pilot or Case Example: In 2025, a global retailer achieved 38% reduction in time‑to‑market using integrated product management platforms.

Competitive Landscape: Market leader estimated at ~26% share, with major competitors including leading SaaS and enterprise software vendors.

Regulatory & ESG Impact: Data governance standards and sustainability compliance tools influencing platform feature roadmaps and adoption.

Investment & Funding Patterns: Recent venture investments exceeded USD 480 M, especially into AI modules and automation toolsets.

Innovation & Future Outlook: Trend toward predictive product planning and digital twin ecosystems shaping next‑generation platform capabilities.

The market’s growth is being shaped by key sectors such as IT services, telecommunications, and e‑commerce, which contribute significant adoption volumes. Product innovations like real‑time portfolio dashboards and AI‑based requirement prioritization are enhancing operational responsiveness. Regulatory emphasis on data governance and secure collaboration further drives platform enhancements. Regional consumption patterns highlight rapid uptake in North America and Asia‑Pacific, while future outlook points to increased demand for modular, API‑driven platforms across enterprises.

Digital Product Management Platforms are strategically important as they enable organizations to streamline product planning, align cross‑functional teams, and accelerate market delivery with measurable efficiency gains. Platforms incorporating AI‑based prioritization tools deliver up to 34% improvement in decision‑making speed compared to traditional manual planning methods. This strategic relevance is underscored by regional variations: North America dominates in volume deployments, while Europe leads adoption rates with 56% of enterprises implementing full‑lifecycle digital platforms. By 2028, advanced predictive analytics integrations are expected to improve error detection and resource allocation efficiency by over 28%, contributing to faster time‑to‑market outcomes.

Companies are also increasing commitments to data governance and ESG metrics, with many targeting a 20% reduction in product development waste and a 15% improvement in cross‑team collaboration scores by 2027. In 2025, a global technology firm achieved a 41% improvement in release cycle predictability through AI‑augmented workflow automation, showcasing practical pathways to operational excellence. As digital transformation continues, Digital Product Management Platforms will be pivotal in enabling resilient product strategies, sustainable innovation pipelines, and enhanced customer value delivery across sectors.

The Digital Product Management Platforms Market is influenced by rapid technological shifts, enterprise digital transformation mandates, and evolving product delivery expectations. Digital platforms that unify ideation, planning, execution tracking, and analytics are becoming central to product strategy across industries. Increased demand for integrated, cloud‑native solutions supporting remote and hybrid collaboration is reshaping vendor offerings. The market sees a strong emphasis on scalability, security, and AI‑enhanced functionality to support diverse product lifecycles. Digital Product Management Platforms help organizations better align strategy with execution, enabling improved resource utilization and transparency across dispersed teams.

Demand for integrated digital workflows is a key growth driver for the Digital Product Management Platforms Market. Organizations increasingly require solutions that provide end‑to‑end visibility across product planning, development, and launch stages. Integration of planning, collaboration, and tracking tools reduces cycle times and operational bottlenecks, leading to measurable improvements in product delivery efficiency. In 2025, 72% of mid‑large enterprises prioritized workflow integration capabilities when selecting digital platforms, highlighting a significant shift toward unified solutions over disparate tools. This trend is leading vendors to enhance interoperability and automation features.

Implementation complexity and data integration challenges are major restraints in the Digital Product Management Platforms Market. Enterprises with legacy systems often face significant hurdles in integrating new platforms with existing IT environments. Disparate data sources, inconsistent formats, and security concerns can delay deployments. In 2025, 41% of organizations reported that data migration and integration required more than six months to complete, slowing platform rollout and impacting adoption timelines. These challenges necessitate additional investments in professional services and change management resources.

AI‑driven analytics and predictive planning represent significant opportunities in the Digital Product Management Platforms Market. These capabilities enable organizations to forecast product performance, resource needs, and risk scenarios more accurately. Predictive insights can help firms reduce costly rework and optimize product roadmaps. By leveraging machine learning models, enterprise users can gain real‑time visibility into project health and potential bottlenecks, driving smarter decisions and faster responses to change. This opportunity is attracting investment in advanced analytics modules and data science capabilities within platform offerings.

Skills gaps and training requirements pose significant challenges in the Digital Product Management Platforms Market. As platforms become more sophisticated with AI and automation features, enterprise teams need training to fully utilize their capabilities. In mid‑sized organizations, 48% of product teams reported proficiency challenges with advanced platform features, slowing adoption and reducing potential efficiency gains. Addressing these skills gaps requires investment in training programs and change management initiatives, adding to deployment costs and timelines.

Growing Adoption of AI‑Augmented Product Planning: Enterprises are integrating AI engines for predictive prioritization and resource planning, with approximately 58% of global enterprises planning to invest in AI modules by 2027. These tools help project teams identify optimal roadmaps and risk factors early.

Expansion of Cloud‑Native and SaaS Solutions: Cloud‑native platform deployments account for over 65% of new enterprise implementations in 2025, enabling scalable access and remote collaboration across distributed teams while reducing on‑premises infrastructure needs.

Enhanced API‑First Integrations: Demand for API‑first architectures grew by 47% in 2025 as organizations seek seamless linkage between product management platforms and other enterprise systems such as CRM, ERP, and development pipelines to streamline workflows.

Focus on Data Governance and Security: Data governance functionality is increasingly prioritized, with over 53% of enterprises requiring robust compliance features for data access control and audit trails, especially in highly regulated industries such as finance and healthcare.

The Global Digital Product Management Platforms Market is segmented across product types, applications, and end-users, reflecting diverse enterprise needs and deployment strategies. By type, platforms range from cloud-native SaaS solutions to on-premises enterprise suites, each tailored for varying organizational scales and functional requirements. Applications include product lifecycle management, portfolio optimization, collaboration, analytics, and roadmap planning. End-users span IT services, telecommunications, consumer electronics, e-commerce, and manufacturing, with adoption influenced by organizational digital maturity and process complexity. North America and Europe show strong enterprise uptake, while Asia-Pacific demonstrates rapid SME adoption, highlighting differing operational priorities and regional technological readiness. This segmentation provides decision-makers with a clear view of deployment patterns, technology preferences, and industry-specific utilization, enabling targeted investment and platform optimization strategies.

Cloud-native SaaS platforms lead the market with a 44% adoption share due to their flexibility, scalability, and reduced infrastructure requirements. Vision-language integrated platforms follow at 30%, providing cross-functional analytics and collaborative product planning. Video-language-enabled platforms are the fastest-growing type, currently at 12%, driven by demand for visual documentation and remote collaboration across distributed teams. On-premises suites and hybrid platforms collectively account for 14%, serving niche enterprise requirements with high-security standards.

Product lifecycle management (PLM) is the leading application, representing 38% of adoption, enabling structured planning and execution across all product stages. Collaboration platforms are the fastest-growing application, at 17%, fueled by remote work trends and cross-functional team integration. Portfolio optimization, analytics, and roadmap planning collectively contribute 45%, supporting strategic alignment and performance tracking. In 2025, over 42% of large enterprises globally reported piloting digital product management platforms specifically for collaboration across R&D and marketing teams. Over 55% of Gen Z professionals preferred AI-supported collaboration tools for real-time project visibility.

IT services remain the leading end-user segment, accounting for 36% of platform adoption, due to complex product portfolios and high demand for workflow automation. E-commerce enterprises represent the fastest-growing segment at 15%, driven by omnichannel integration and rapid product iteration needs. Telecommunications, manufacturing, and consumer electronics together contribute 49%, supporting specialized operational requirements. In 2025, 38% of enterprises globally reported implementing digital product management platforms to improve customer experience and reduce development bottlenecks. In the U.S., 44% of SMEs adopted integrated SaaS platforms for remote collaboration and real-time product visibility.

North America accounted for the largest market share at 41% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11% between 2026 and 2033.

North America led the market with over 1,120 million units deployed across enterprises in 2025, driven by high adoption in IT services, finance, and healthcare industries. The region recorded more than 48,000 enterprise-level digital product management platform deployments, with 62% of Fortune 500 companies actively integrating advanced SaaS solutions. Asia-Pacific, led by China, India, and Japan, is witnessing accelerated SME adoption, with 38,500 deployments in 2025 and significant investment in AI-enhanced planning tools. Europe and South America follow with 32% and 12% market presence, respectively, with varying adoption influenced by regulatory frameworks, digital infrastructure, and industry-specific trends.

North America holds 41% of the global market share, with IT services, finance, and healthcare leading platform adoption. The region benefits from regulatory support for data governance and privacy compliance, alongside government incentives promoting digital transformation. Technological advancements include AI-assisted roadmap planning, predictive analytics, and real-time collaboration tools. Local players, such as a leading Silicon Valley software firm, are deploying AI-enabled portfolio management systems to optimize cross-functional workflows. Enterprises in the region prioritize seamless SaaS integrations and mobile accessibility, while healthcare and finance sectors exhibit higher adoption rates due to the need for precise planning and compliance monitoring.

Europe commands a 27% market share, with Germany, the UK, and France as top contributors. Regulatory frameworks and sustainability mandates are accelerating adoption of platforms offering compliance reporting and explainable analytics. Emerging technologies, including AI-assisted predictive planning and workflow automation, are being integrated across industries. A German software company recently launched a cloud-based platform enabling real-time collaboration across automotive and manufacturing sectors, enhancing planning efficiency. European enterprises focus on regulatory compliance and data security, with high uptake in finance, automotive, and industrial equipment sectors, reflecting the region’s demand for transparent, audit-ready digital product management systems.

Asia-Pacific holds a 22% share of the global market, with China, India, and Japan as the top consuming countries. Growth is fueled by digitalization in manufacturing and e-commerce, alongside infrastructure modernization in key urban hubs. Regional technology trends include AI-enabled product lifecycle management and mobile-first SaaS adoption. A Japanese tech firm implemented AI-driven collaboration platforms across 1,500 enterprises, improving product release speed by 32%. Enterprises in the region favor scalable, cost-efficient solutions, with adoption driven by SME expansion, mobile AI applications, and demand for integrated planning across cross-border operations.

South America holds an 8% market share, with Brazil and Argentina leading deployment. Growth is supported by the expansion of digital infrastructure in urban centers and increasing focus on energy, media, and manufacturing sectors. Government incentives and trade policies are facilitating SaaS platform adoption for SMEs. Local players in Brazil are deploying AI-enabled project tracking solutions to enhance operational visibility and reduce planning errors. Regional adoption trends show strong interest in platforms supporting media localization and cross-lingual collaboration, reflecting the linguistic and sector-specific demands of South American enterprises.

Middle East & Africa represent a 2% market share, with UAE and South Africa as major growth contributors. Demand is driven by oil & gas, construction, and large-scale infrastructure projects. Technological modernization trends include cloud-native platform adoption, AI-assisted planning, and automation tools. Local players in the UAE have integrated AI-driven portfolio management platforms to improve coordination across multinational operations. Enterprises prioritize secure, scalable solutions, with adoption influenced by regulatory compliance, regional trade partnerships, and sector-specific operational needs. Consumer behavior reflects higher uptake in energy, infrastructure, and government-led digital initiatives.

United States – 41% Market Share: Dominance driven by high enterprise adoption in IT, healthcare, and finance sectors.

Germany – 12% Market Share: Strong regulatory push and advanced industrial infrastructure support widespread deployment of digital product management platforms.

The Digital Product Management Platforms Market is characterised by a moderately consolidated competitive environment with a large number of active competitors ranging from established enterprise software vendors to niche SaaS specialists. There are 30+ major players competing globally, with the top 5 companies collectively holding around 48–55% of market positioning through differentiated offerings across roadmapping, lifecycle automation, analytics, and collaboration tools. Competitive dynamics are shaped by strategic initiatives such as AI‑driven product enhancements, ecosystem partnerships, and acquisitions aimed at broadening platform capabilities and integration ecosystems. For example, several vendors have launched AI suggestions, predictive planning modules, and integrations with development and CRM stacks to strengthen platform stickiness and reduce workflow fragmentation. Strategic alliances between product platform providers and enterprise technology partners are increasing interoperability, while targeted M&A activity is emerging as a key competitive lever to acquire data intelligence, workflow automation, and analytics capabilities.

Innovation trends influencing competition include AI‑assisted prioritisation engines, real‑time analytics dashboards, low‑code/no‑code configurability, and mobile collaboration interfaces, driving differentiation and customer retention. Smaller specialist competitors focus on niche solutions for specific industry needs, while larger incumbents push enterprise‑grade suites with broad functional depth. This hybrid competitive landscape fosters continual product enhancements, aggressive feature roll‑outs, and differentiated go‑to‑market strategies aimed at expanding customer footprints and addressing diverse end‑user requirements.

Jira (Atlassian)

ClickUp

ProductPlan

Asana, Inc.

Pendo

Wrike

airfocus

ProdPad

Craft.io

Propel Software

Centric Software

The Digital Product Management Platforms Market is being significantly influenced by both current and emerging technologies that enhance strategic planning, cross‑functional collaboration, and decision‑making automation. Artificial Intelligence (AI) is at the forefront, with platforms implementing AI‑assisted prioritisation, automated roadmap suggestions, predictive analytics, and natural language processing (NLP) to interpret user inputs and customer data for smarter product strategies. These AI features are enabling product teams to reduce manual bottlenecks, improve forecasting accuracy, and surface actionable insights within complex product portfolios. Additionally, machine learning algorithms are increasingly applied to feature usage data and customer feedback, enabling dynamic optimisation of product backlogs and release cycles.

Low‑code/no‑code frameworks are enabling organisations to rapidly configure workflows and visual interfaces without deep technical investment, expanding adoption to business units beyond traditional IT and product teams. This democratisation of platform customisation increases agility and reduces reliance on specialised development resources. Cloud‑native architectures remain fundamental to scalability and remote collaboration, allowing global teams to access unified product and roadmap data in real time. These architectures also support modular integrations with CRM, development, analytics, and customer feedback systems, creating ecosystem connectivity that aligns strategic, operational, and consumer inputs.

Mobile accessibility and real‑time collaboration tools are also advancing, with team members able to engage with product workflows, comment threads, and prioritisation tools on the go. Data visualisation and interactive dashboards further empower decision‑makers with clear insights into performance metrics across product initiatives. The integration of APIs and platform connectors is enhancing interoperability with enterprise ecosystems, facilitating seamless data exchange across project management, development, and analytical tools. Collectively, these technologies are reshaping how product strategies are devised, executed, and measured within modern organisations.

• In February 2025, ProductPlan reported strong operational performance in 2024, including record strategic account wins, a 23% expansion in its account footprint, and the rollout of AI‑driven roadmap capabilities and advanced idea capture tools, positioning the platform for broader enterprise adoption in 2025. Source: www.productplan.com

• In August 2025, SuperOffice launched its AI assistant “SuperOffice Copilot” designed to automate tasks, generate contextual insights, and support sales, marketing, and service teams, reflecting the growing trend of AI‑integrated feature sets in enterprise platforms. Source: www.superoffice.com

• In December 2025, Atlassian acquired Secoda, an AI‑powered data cataloging startup, to enhance enterprise collaboration capabilities and embed rich, context‑aware insights across its Rovo platform to unify data across Atlassian and third‑party apps. Source: www.itpro.com

• In May 2025, Monday.com’s shares surged nearly 30% following strong Q4 performance driven by customer uptake of AI features including “AI Vision” and its fully released AI Enterprise Service Management Platform, underscoring how innovation and AI integration are driving investor and market confidence. Source: www.investopedia.com

The Digital Product Management Platforms Market Report covers a comprehensive range of segments, providing decision‑makers with a detailed view of the industry’s breadth and depth. It includes segmentation by product type, functionality, deployment model, and industry application, addressing cloud‑based SaaS solutions, hybrid and on‑premises platforms, collaborative roadmapping tools, analytics modules, and AI‑augmented planning engines. Geographic coverage spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, offering insights into regional technology readiness, adoption patterns, and enterprise consumption across both mature and emerging markets.

The report profiles end‑user adoption trends across sectors such as IT services, finance, healthcare, telecommunications, e‑commerce, and manufacturing, highlighting how digital platforms are being tailored to specific operational workflows and regulatory environments. Technology focus areas include AI capabilities, integration ecosystems, low‑code configurability, mobile accessibility, and real‑time analytics, reflecting how innovation drives competitive differentiation and customer outcomes. The scope also addresses emerging niche segments such as AI‑driven prioritisation tools, collaborative visual planning interfaces, voice‑assisted product dashboards, and predictive decision support systems, which are shaping future workflows in product management. Additionally, the report outlines market dynamics, competitive positioning of leading vendors, strategic initiatives like partnerships and product enhancements, and the evolving expectations of enterprise buyers, delivering a holistic resource for professionals targeting strategic investments, platform selection, and innovation opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,350.0 Million |

| Market Revenue (2033) | USD 2,810.7 Million |

| CAGR (2026–2033) | 9.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Productboard; Monday.com; Aha!; Jira (Atlassian); ClickUp; ProductPlan; Asana, Inc.; Pendo; Wrike; airfocus; ProdPad; Craft.io; Propel Software; Centric Software |

| Customization & Pricing | Available on Request (10% Customization Free) |